Executive Summary

The S&P 500 was up 6.3% in May 2025, one of the best months in history. The rally has been driven largely by tech and communication companies that are either selling software or supporting the current boom in Artificial Intelligence (AI) technology. Companies that are impacted by the economic slowdown or tariff policies have not fared as well. While earnings were strong in Q1, there is uncertainty due to the slowdown in economic growth expected from Q2 onwards, which is something investors are watching closely.

May Performance

May 2025 was a month of notable gains across global equity markets, largely spurred by a perceived de-escalation in US-China trade tensions and resilient corporate earnings, particularly in the technology sector. The S&P 500 achieved its best monthly performance since November 2023, alongside strong showings from the Nasdaq Composite. The MSCI World Index also posted robust gains. Emerging markets continued their positive trajectory, aided by a weakening US dollar and specific regional strengths. However, the US Treasury market presented a more complex picture, with rising yields across the curve for the month. Central bank policies remained a focal point, with the Federal Reserve maintaining a cautious stance amidst inflation concerns, while the Bank of England delivered a surprise rate cut.

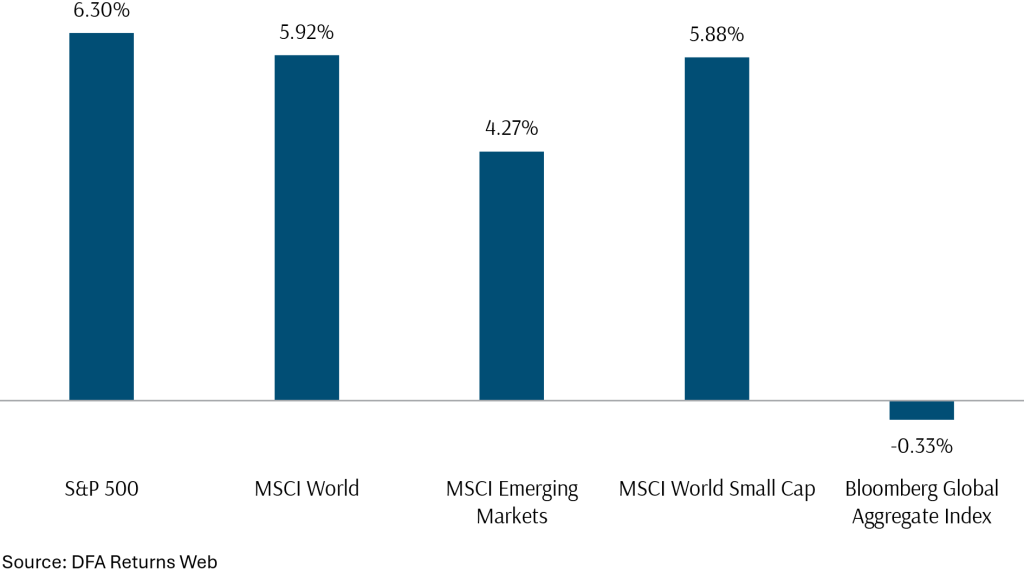

Exhibit 1: Major Indexes May 2025 (in USD)

Looking at the performance of the indexes in Exhibit 1, we can see that the S&P 500 rebounded strongly in May, lifting developed world stocks higher, while emerging market stocks continue to have a strong year as investors start to look beyond the US stock market. Small caps did well in May, but slightly underperformed larger stocks on the global stage. Bonds faced a challenging month as yields on US treasuries rose sharply, as investors are looking for a higher premium for holding US assets due to the uncertainty around economic and fiscal policy.

Earnings Resilience Has Supported Stocks

The Q1 2025 earnings season, largely concluding in May, was stronger than anticipated. Approximately 78% of S&P 500 companies reported positive earnings per share (EPS) surprises, and the blended year-over-year earnings growth rate for the index was robust, around 12.5% to 13.3% according to FactSet and Nasdaq. This marked the second consecutive quarter of double-digit earnings growth, exceeding the 10-year average for both the percentage of companies beating estimates and the magnitude of those surprises.

This was underscored by strong results from Microsoft and Nvidia, which led their market capitalisation back above the US$3 trillion level, and led the gains for US stocks in May.

However, markets trade on future expectations, so does the current level of the S&P 500 reflect reality, given the worsening economic outlook?

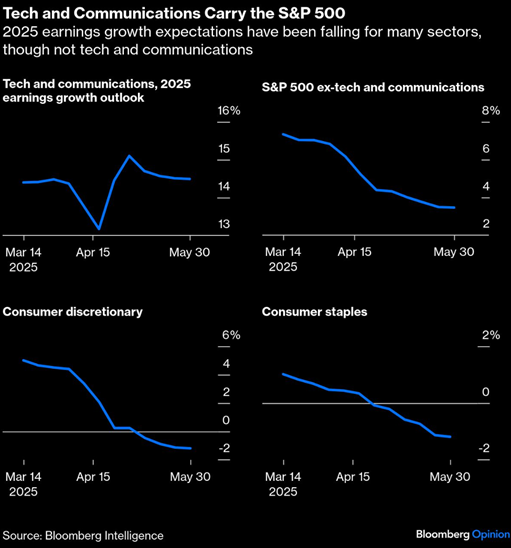

Exhibit 2: Earnings Growth Expectations – US Stocks

As we can see from the charts above, tech and communications earnings growth has remained flat since the “liberation day” tariff blip, so it is unsurprising that these sectors have led the market recovery. Excluding tech and communications, we are seeing a sharp fall in earnings growth from almost 8% to just below 4%, according to Bloomberg’s data.

Therefore, we can see that the market is still acting very rationally, rewarding companies that have pricing power or have some protection from tariffs in their business models, while companies that are more exposed to tariffs have not done as well.

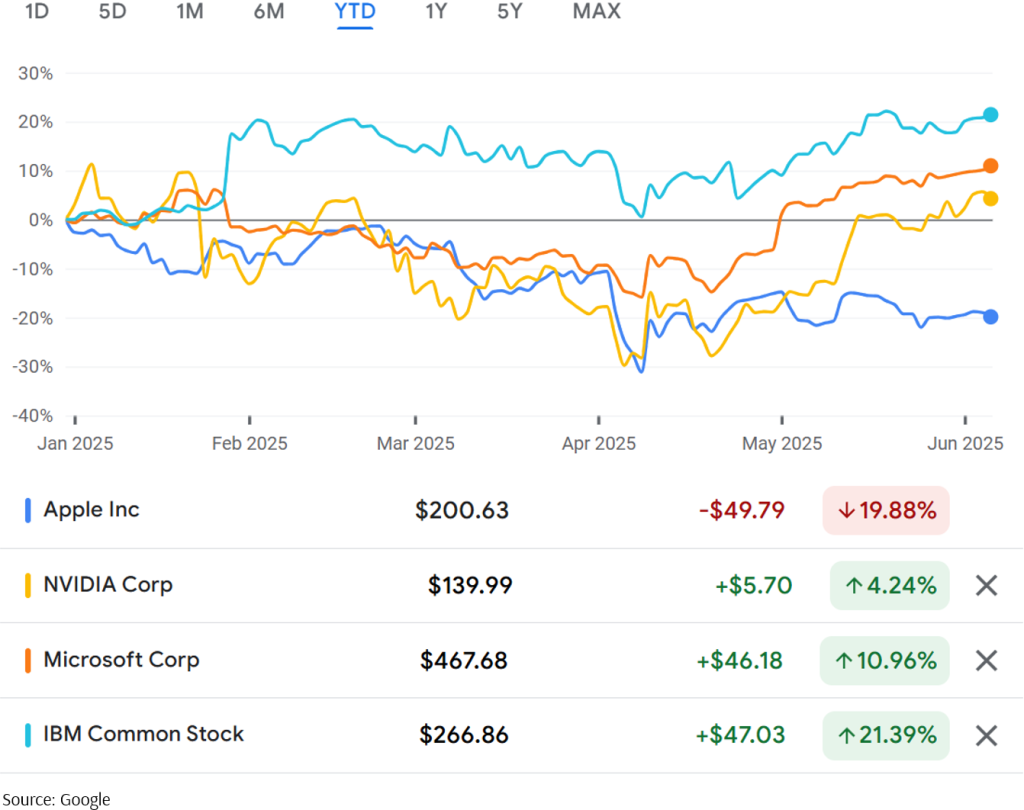

Exhibit 3: Share Price of AAPL vs MSFT, NVDA & IBM

A simple example of this would be to look at the performance of Apple, which is highly exposed to tariffs and slowing consumer demand, compared to the performance of Microsoft and IBM, which are largely software companies that depend more on stable corporate demand for their services.

Global Growth Is Likely to Slow

As we zoom out a little to look at the global economy, expectations are that it will slow, but growth remains. The Organisation for Economic Co-operation and Development (OECD) projects global GDP growth at 3.3% for both 2025 and 2026, with inflation expected to ease to 3.8% in 2025 and 3.0% in 2026. Escalating trade tensions are likely to dampen global growth, with US GDP growth potentially declining from 2.8% in 2024 to 1.6% in 2025. Similarly, the eurozone faces challenges, with the European Central Bank (ECB) cutting interest rates to 2% in response to falling inflation and potential growth risks from US tariffs. The ECB has revised its growth forecast downward to 0.9% for 2025, highlighting the impact of trade disputes on the region’s economy.

Valuations in US Stocks Remain Lofty

The strong gains in US stocks have again brought valuations into focus. The forward 12-month Price-to-Earnings (P/E) ratio for the S&P 500 stood at approximately 21.3 by the end of May. This was notably above both the 5-year average (around 19.9) and the 10-year average (around 18.4), indicating that the market is pricing in continued earnings growth and a favourable economic environment.

Stocks Have Recovered but Uncertainty Remains

It has been a roller coaster ride for investors, as the fear of a stock market crash has been replaced by the possibility of the S&P 500 reaching new all-time highs. While earnings in Q1 have remained strong, it remains to be seen if the momentum will carry on into the subsequent quarters, as the full impact of the tariffs has yet to be felt in the economy.

Alongside high valuations, slowing growth globally, and also uncertainty around the US fiscal policy, there remains lingering concerns that volatility might return in the later half of 2025.

However, as we have seen in May, we cannot accurately predict how markets and stocks will react to news. What seemed like a dire outcome for stocks in April turned into a strong rebound, and investors who stayed the course have seen their portfolios recover strongly.

We thank you for your continued trust and support, and we remain committed to supporting you as you journey towards your life goals in your wealth plan. As always, don’t hesitate to reach out to your Client Adviser if you have any questions or concerns.

For more related resources, check out:

1. Active Investing That Adds Value to the Client

2. Staying the Course: Investing With Confidence in Uncertain Times

3. Here’s Why We Charge a Higher Fee Than Robos

Download our Investment eBook titled “A More Reliable Way to Get Enough Investment Returns: Even During Times of Market Uncertainty” here.

With a minefield of financial misinformation out there, we promise to be a safe pair of hands and a second pair of eyes to help you avoid costly financial mistakes. Learn more about our investment philosophy here.

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current estate plan, investment portfolio, financial and/or retirement plan, make an appointment with us today.