Executive Summary

It has been a tumultuous first half of 2025, with many geopolitical and economic shocks that have begun to reorder the world. However, markets have demonstrated an underlying resilience that surprised many. The S&P 500 and STI Index are now at all-time highs. This highlights the unpredictability of markets, and that it is hard to predict the outcomes of any events accurately. Instead, capturing asset class returns via a diversified portfolio is likely to produce better outcomes for investors.

June Performance

It has been a tumultuous first half of 2025, marked by numerous geopolitical and economic shocks that have begun to reorder the world. One of these was the tariffs that President Trump announced on trading partners in April, which drove markets down, with the S&P 500 reaching a year-to-date low of -15.3%.

However, the market’s response was remarkable. It staged one of the fastest recoveries in history, demonstrating an underlying resilience that surprised many. The S&P 500 has since rebounded strongly and made new all-time highs in July. Investor sentiment has improved dramatically, and even fixed income markets are relatively calmer.

Outside of the US, stocks have done even better. European stocks, as measured by the Stoxx Europe 600, are up 24% in USD terms, and the local STI Index has reached new all-time highs of 4022 points, as investors rotate back into SGD yield to mitigate the impact of the weaker USD.

This highlights the unpredictability of markets, and that it is hard to predict the outcomes of any events accurately. Instead, capturing the asset class returns via a diversified portfolio is likely to produce better outcomes for investors.

Economic Headwinds Have Not Led to Recession

One of the major news topics during the first half of the year was the dynamic ups and downs of US tariff and trade policy. President Trump announced a set of increased tariffs on a wide range of countries, then paused or reduced some while keeping overall tariff levels higher than before he assumed office in January. While the US stock market has rebounded following the partial tariff easing, some clients might be wondering whether the ongoing tariff saga will induce a recession.

So far, the US economy has demonstrated remarkable resilience. The first quarter of 2025 saw Gross Domestic Product (GDP) contracting at an annualised rate of 0.2% – the first negative reading in three years. While this figure might initially appear worrisome, a closer look at the components of GDP reveals that this contraction was primarily caused by increased imports ahead of expected tariffs. Specifically, “gross private domestic investment” (business spending) spiked by 4%, a dramatic increase from prior levels due to business stockpiling goods, which actually added to GDP. This was offset by Net Exports declining significantly by 4.9%, due mostly to this import activity. Importantly, consumer spending, which is the backbone of the economy, remained positive and grew 0.8% for the quarter. While weaker than in prior quarters, it was not as bad as some had feared.

Despite the negative GDP figure, the underlying fundamentals of the US economy remain robust. Supporting consumer spending, the labour market remains a bright spot, with unemployment at only 4.2%, hovering within a narrow range between 4.0% and 4.2% for the past year. Inflation trends have also been encouraging. As of May, the Consumer Price Index (CPI) rose just 2.4% year-over-year, down from higher levels earlier in the year, and is slowly trending toward the Federal Reserve’s 2% target. Core inflation, which excludes food and energy components, accelerated to a 2.8% year-over-year increase. However, shelter costs were the biggest contributor to this figure; excluding this category results in what’s sometimes referred to as “supercore inflation,” which rose only 1.9% year-over-year. The combination of stable employment, moderating inflation, and a trade-driven GDP contraction likely reflects an economy in transition, not in crisis. While growth may be slower than in previous years, these conditions suggest that the foundations of the economy are still likely healthy.

The Fed Keeps Rates Unchanged for Now

The Federal Reserve (The Fed) publishes its Summary of Economic Projections (SEP) every quarter, and the latest release in June acknowledged increased uncertainty facing the economy while downgrading its 2025 economic growth forecast to 1.4%. This revision reflects concerns about the potential impact of trade policies, fiscal challenges, and global economic conditions. So far this year, the Fed has maintained the federal funds target range at 4.25% to 4.50%, preferring to be data-dependent in its decision making.

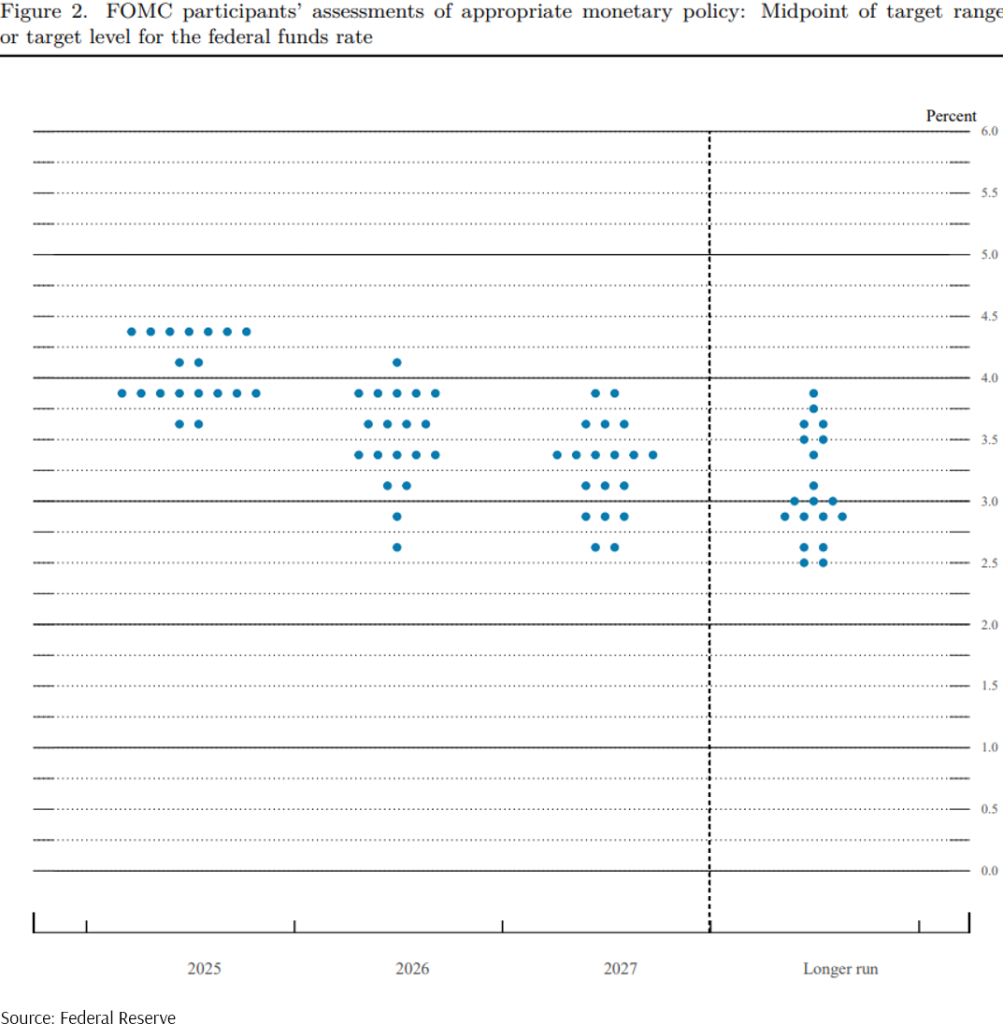

Looking ahead, Fed officials have emphasised their focus on underlying economic trends rather than short-term policy developments. The general consensus of Fed officials continues to be that there could be two rate cuts in 2025. Based on the Fed’s own projections, the Effective Federal Funds Rate (EFFR) is also expected to fall further in 2026 and 2027, eventually reaching a longer-run rate of 3.0%. These estimates are based on the dot plot chart that the Fed releases every quarter and are subject to change based on future events. However, we can expect that rates are likely to head lower should the economy maintain its momentum.

Exhibit 1: Fed Dot Plot June 2025

US Dollar Is Lower in 2025, but It’s Not a Surprise

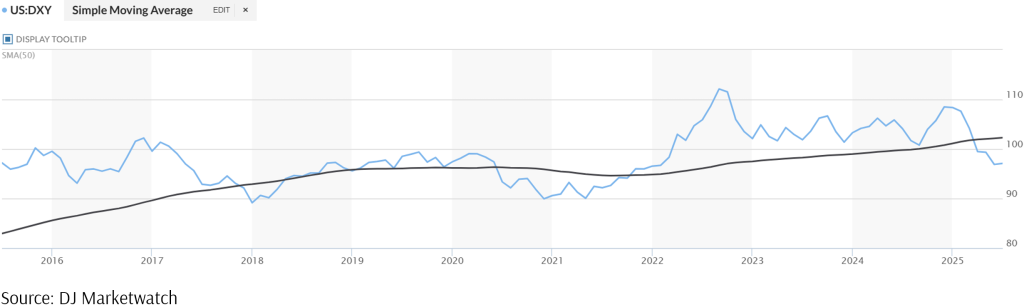

There has been a lot of concern about the US dollar in 2025. Its decline this year is often seen as representing a flight from US assets, especially during recent periods of volatility. However, at just below 100, the Dollar Index (DXY) is hovering at its average for the past decade. Zooming out more, the dollar is still near its strongest levels since 2008. Meanwhile, the trade-weighted dollar index has also declined, but it still remains above historical averages. This index measures the US dollar’s value relative to foreign currencies weighted according to the amount of trade the US conducts with each country.

Exhibit 2: DXY Index

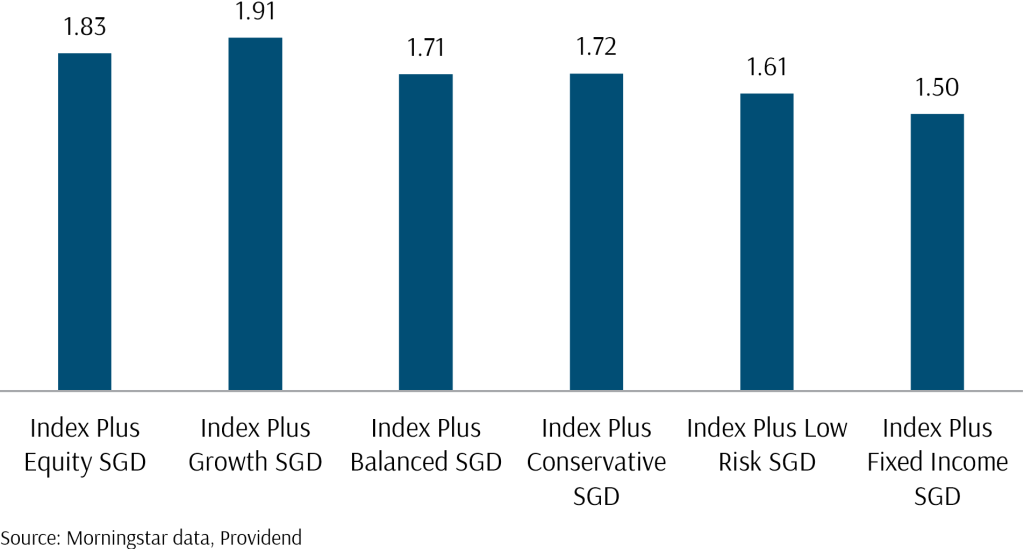

However, we do recognise that due to the foreign exchange moves this year, the performance of the portfolios in SGD might look very disappointing. This just highlights that our commitment to using SGD-hedged fixed income funds is an astute decision, despite the challenges of finding clean (no commissions) SGD-hedged share classes for global bond funds, as the SGD hedge has enabled us to deliver fixed income returns in SGD so far in 2025.

Portfolio Performance 1H 2025

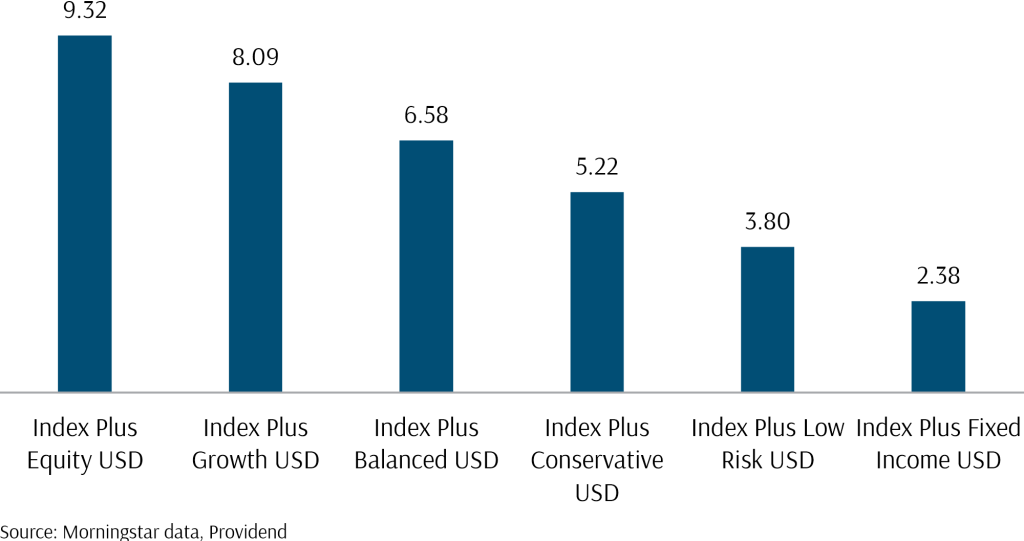

Exhibit 3: Index Plus Portfolios in USD (YTD 30 June 2025)

Exhibit 4: Index Plus Portfolios in SGD (YTD 30 June 2025)

If we look at our portfolio performance in the first half of 2025, we see that despite all the volatility, we have captured the returns from the market rebound, and all our portfolios are positive in 2025. The rebound in global stocks has been strong enough to overcome the weaker USD, with even our SGD portfolios doing well in 2025, delivering positive returns.

Our decision to add some index funds to our Index Plus portfolios is also starting to show the importance of diversifying even across factors. While we still believe in the long-term value of investing in lower-priced companies (the value premium), we also recognise that this can take time to show results, and it may not always align with every client’s time horizon. That is why we have taken steps to balance things out, so your portfolio can benefit more consistently across different market conditions.

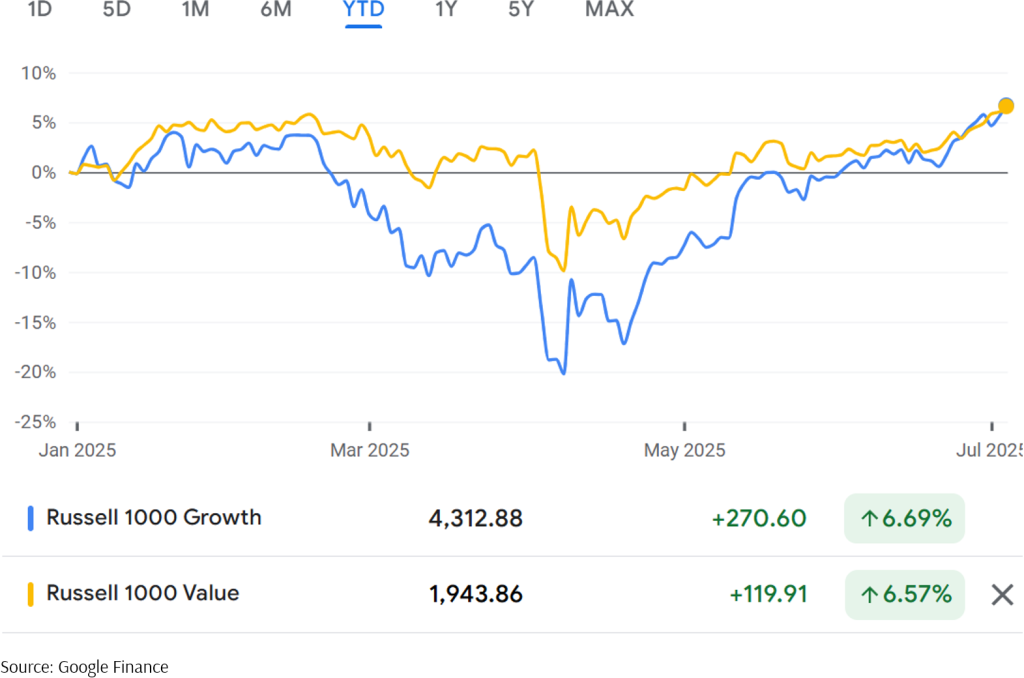

So far in 2025, growth stocks have slightly outperformed value, so our Index Plus portfolios are benefiting from the addition of the market-cap-weighted Amundi index funds to the portfolio.

Exhibit 5: Russell 1000 Growth vs Value Indexes YTD 4 July 2025 in USD

Conclusion: Preparing for the Second Half of 2025

As we begin the second half of 2025, several themes are likely to remain central to investors. The evolution of trade policy, the Fed’s decisions, and international developments will continue to be key factors investors keep an eye on. Importantly, there are many positive narratives at play. The resilience demonstrated by markets and the economy during the first half of the year suggests that fundamental strengths remain intact. US market corporate earnings growth also remains very healthy, with expectations of approximately 11% for the coming year. While these forecasts are subject to revision, they suggest that underlying business fundamentals continue to support market valuations.

As always, we will be monitoring the portfolios and walking alongside you through these volatile and uncertain times. Thank you for the continued trust and support you place in your Client Advisers at Providend. If you have any questions, please don’t hesitate to reach out.

For more related resources, check out:

1. Active Investing That Adds Value to the Client

2. Staying the Course: Investing With Confidence in Uncertain Times

3. Here’s Why We Charge a Higher Fee Than Robos

Download our Investment eBook titled “A More Reliable Way to Get Enough Investment Returns: Even During Times of Market Uncertainty” here.

With a minefield of financial misinformation out there, we promise to be a safe pair of hands and a second pair of eyes to help you avoid costly financial mistakes. Learn more about our investment philosophy here.

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current estate plan, investment portfolio, financial and/or retirement plan, make an appointment with us today.