Executive Summary

-

April 2026 delivered strong global equity returns, as markets recovered sharply from March’s geopolitically driven selloff. The MSCI All Country World IMI rose 10.12%, while the MSCI Emerging Markets IMI gained 14.54%. In the US, the S&P 500 rose 10.54%, the Nasdaq 100 gained 15.66%, the Russell 2000 added 12.08%, and the Dow Jones rose 7.27%. The USD weakened, with the DXY falling 1.91%. Bond yields rose modestly, with the US 10-year yield up 8 basis points. Oil prices declined from elevated levels as Strait of Hormuz disruptions partially eased. Growth stocks led decisively, with semiconductors up 32.16%.

-

This month’s discussion addresses whether the sharp April rally is justified or a sign of excessive optimism. Drawing on recent research, we examine the fundamental case for the recovery, the AI investment theme’s contribution to earnings growth, and highlight Amundi Institute’s research on why the current AI-driven market is yet to exhibit the characteristics of a speculative bubble.

-

May has opened with markets near all-time highs as Q1 earnings season delivers strong results and AI investment spending continues to drive upward earnings revisions. While geopolitical risks around Iran remain fluid, the combination of above-trend earnings growth, broadening AI adoption, and the potential for oil price normalisation provides a constructive backdrop for diversified portfolios. The ongoing strength of diversification and factor tilts continues to support portfolios through periods of elevated volatility.

April Market Summary

April was a strong month for global equity markets, characterised by a broad-based recovery from March’s sharp selloff. The rally was driven by an improving geopolitical outlook, a resurgence in the technology and AI investment theme, and continued earnings growth. Leadership was concentrated in growth-oriented and technology sectors, while defensive and energy-related areas lagged. The MSCI All Country World IMI returned 10.12%, more than reversing the losses incurred in March.

The US dollar weakened in April, with the DXY falling 1.91% as risk appetite improved. Commodity-linked currencies were notably strong. Oil prices eased from their March highs, although Strait of Hormuz shipping activity remained near March lows. Precious metals saw modest losses as safe-haven demand receded, and funding pressure from higher oil prices remained persistent.

The dominant story of the month was the improving geopolitical picture. On 7–8 April, the US and Iran agreed to a two-week ceasefire that included Israel. Both parties subsequently held face-to-face talks in Islamabad, the first direct discussions since 2016. While no deal was reached and President Trump announced a blockade of Iranian ports, both sides largely avoided escalatory strikes. On 16 April, a ceasefire between Israel and Lebanon was announced, followed by Iran declaring the Strait of Hormuz fully open, triggering a large decline in oil prices. The easing of geopolitical tensions allowed markets to reprice and remove the risk premiums that had been built into equities and commodities through March.

Alongside the geopolitical relief, the technology and AI investment theme experienced a resurgence. Accelerating enterprise adoption of AI applications, strong recurring revenue growth at leading AI companies, and the unveiling of more powerful AI models provided evidence that the AI buildout was continuing to deliver commercial results. The rally received further confirmation from late-April hyperscaler earnings, where cloud revenue growth reaccelerated at several of the largest platforms and revenue backlogs pointed to sustained strength in coming quarters. Results were more mixed at others, where elevated capital intensity and weaker non-AI segments weighed on sentiment. The positive momentum in technology spread through broader equity markets, driving indices to new highs through the middle of the month.

Outside the US, Asia extended its run of outperformance, led by Korea and Taiwan where the semiconductor and AI infrastructure buildout continued to drive extraordinary returns. Greater China also participated in the rally, and the breadth of gains across the region reflected Asia’s central position in the AI hardware supply chain.

On the macro front, Q1 US GDP came in at 2.0% annualised, slightly below expectations, with a substantial share of growth driven by AI-related business investment. Core PCE inflation for March was 3.2% year-on-year, remaining above the Fed’s target partly due to higher energy prices. The Federal Reserve held rates steady at its April meeting, with a more divided policy discussion than expected.

Equity Market Performance

US Equities

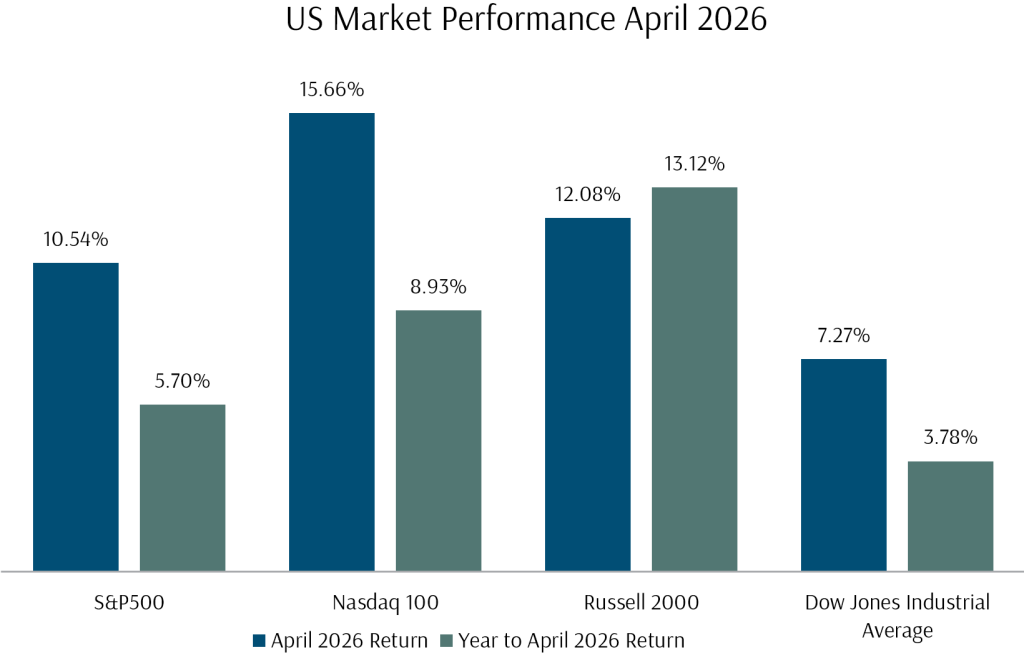

US equity markets were strongly positive in April, with the S&P 500 rising 10.54% and the Nasdaq 100 gaining 15.66%, its best monthly performance in over a year. The S&P 500’s gain was its sharpest monthly rise since April 2020. Technology sector strength was the defining feature of the month, reflecting the AI investment resurgence and improving geopolitical conditions.

Growth stocks outperformed decisively. The semiconductor sector was the standout, with the VanEck Semiconductor ETF gaining 32.16%, while the broader technology sector gained 20.01%. The Magnificent Seven returned 14.33%. Software stocks, which had been under sustained pressure since late 2025, posted a modest recovery of 4.82%.

US macroeconomic data was mixed but not a primary driver for the month. Q1 GDP rose 2.0% annualised, slightly below consensus, with business investment strong at 10.4% but consumption and housing softer. Core PCE inflation for March was 3.2% year-on-year, above the Fed’s target, though analysts noted much of the overshoot reflected energy passthrough and computer-related prices rather than broad demand-driven pressures. At its April meeting, the Federal Reserve held rates steady but the policy discussion was more divided than expected, with three members dissenting against the existing easing bias in the policy guidance. Chair Powell characterised the discussion as “vigorous” and noted the centre of the committee was moving toward a more neutral stance. Analysts expect the next cut in September at the earliest, with risks tilted toward a longer pause if inflation remains elevated.

Exhibit 1: Us Stock Market Performance April 2026 (USD)

International Equities

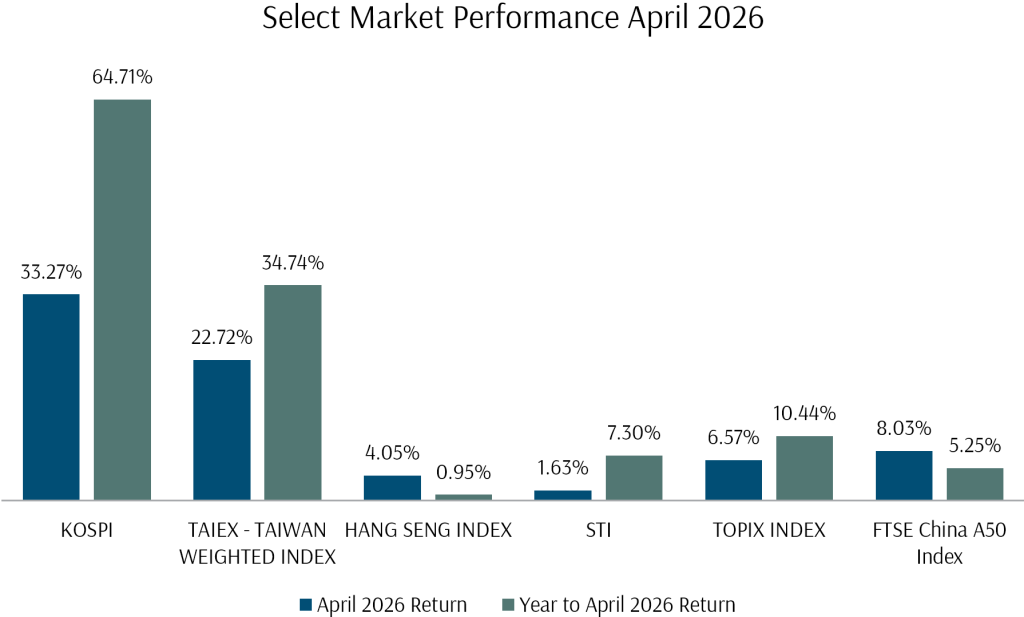

Elsewhere in the world, Asian markets delivered extraordinary returns, as the AI capex boom and semiconductor demand continued to drive large price gains.

Korea’s KOSPI index rose 33.27% in the month, as DRAM contract prices and memory demand continued to accelerate. Taiwan’s TAIEX gained 22.72%, supported by foundry and advanced packaging demand. Japan’s TOPIX rose 6.57%, benefiting from earnings growth and a weaker yen. Greater China participated in the rally, with the FTSE China A50 up 8.03% and the Hang Seng adding 4.05%, a more constructive performance following several months of relative weakness.

Locally, the STI index was up 1.63%, a modest gain relative to the broader regional rally, reflecting the index’s heavier weighting towards banks and industrial names rather than technology.

Exhibit 2: Select Market Performance April 2026 (Local Currency)

Global Summary

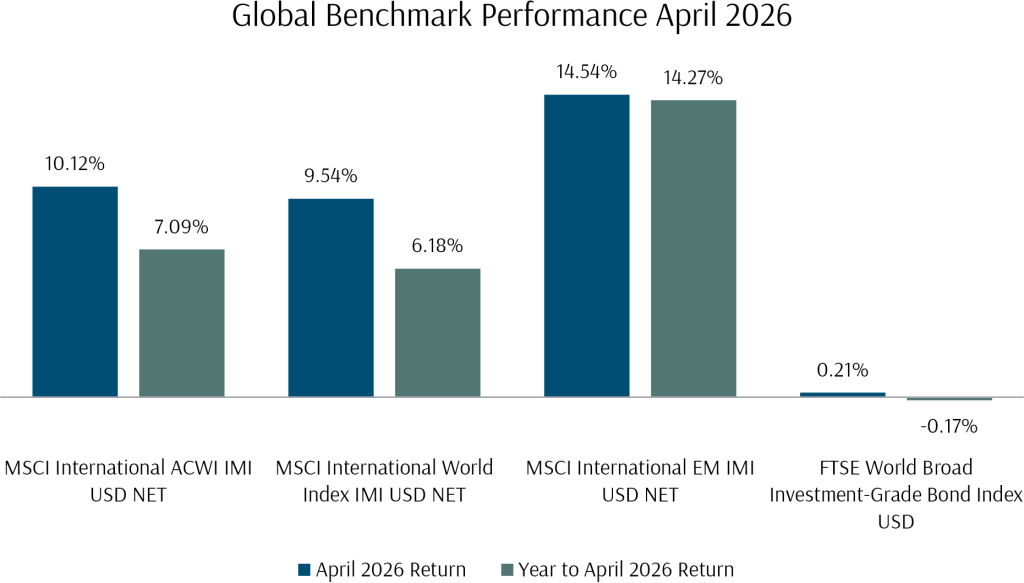

Globally, the combination of a sharp US recovery and continued Asian outperformance made April an excellent month for equity markets. The broad MSCI All Country World IMI returned 10.12%, bringing year-to-date returns through April to 7.09%.

Exhibit 3: Global Equity Benchmark Index Performance April 2026 (USD)

Cross-Asset Performance

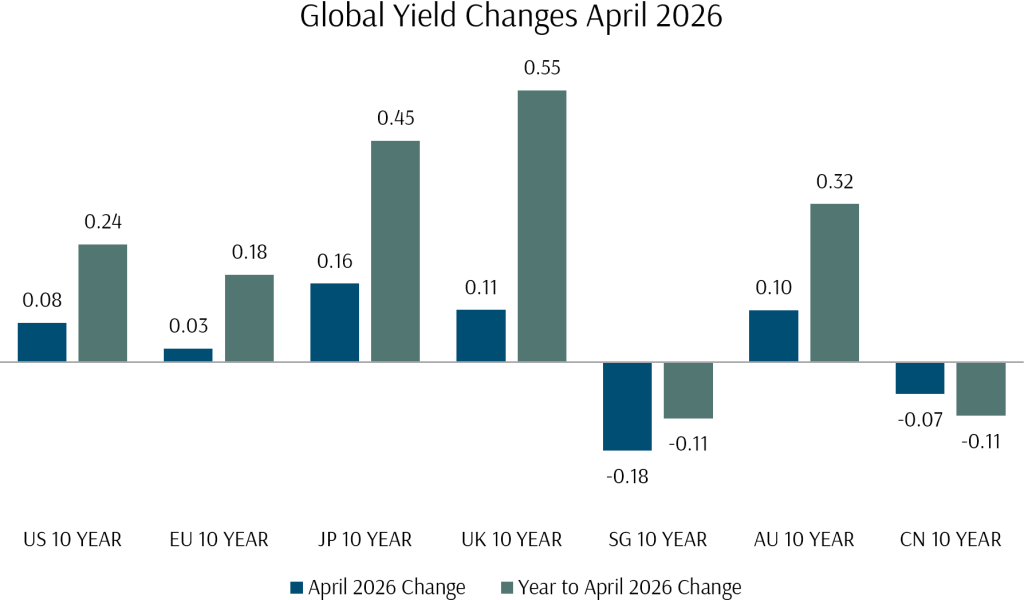

Fixed income markets were roughly flat in April, with the US 10-year Treasury yield ending 8 basis points higher as the recovery in risk appetite weighed on safe-haven demand and oil-related inflation concerns lingered. Other major sovereign yields also rose modestly, with the EU 10-year up 3 basis points, the UK 10-year up 11 basis points, and the Japanese 10-year up 16 basis points. Singapore was the exception, with the 10-year yield falling 18 basis points. Credit spreads tightened on the improved risk environment.

Overall, the FTSE World Broad Investment-Grade Bond USD Index returned +0.21% for the month.

Exhibit 4: Global Yield Changes April 2026

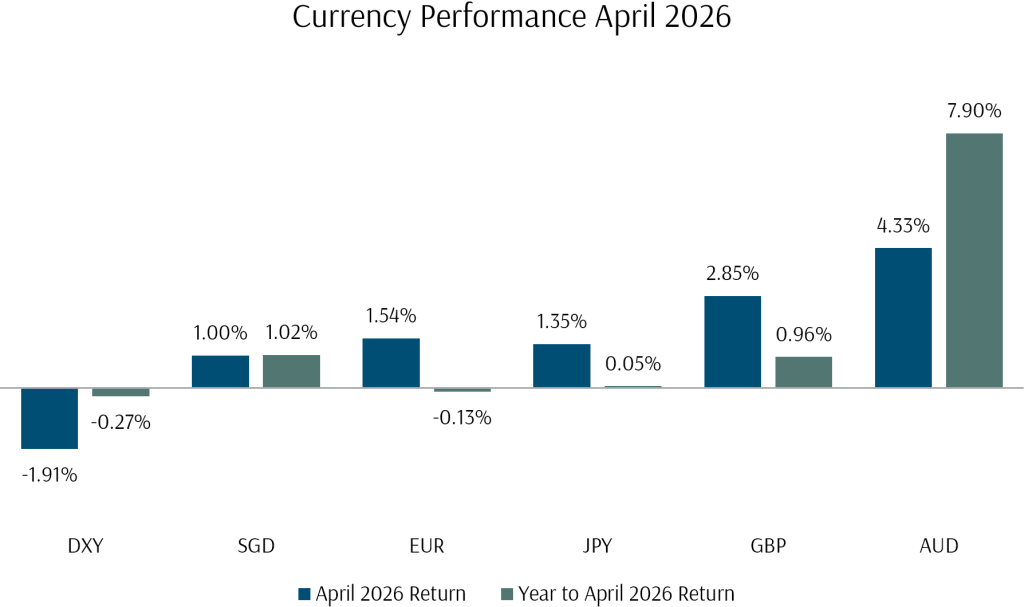

In other macro markets, the US Dollar Index fell 1.91% over the month, as the improving geopolitical picture and risk-on sentiment reduced demand for the dollar as a safe-haven asset. The SGD appreciated 1.00% against the dollar. Commodity-linked and EM-exposed currencies were notably strong, with the Australian dollar gaining 4.33%. The EUR rose 1.54% and the JPY gained 1.35%, while the GBP gained 2.85%.

Exhibit 5: Currency Performance April 2026

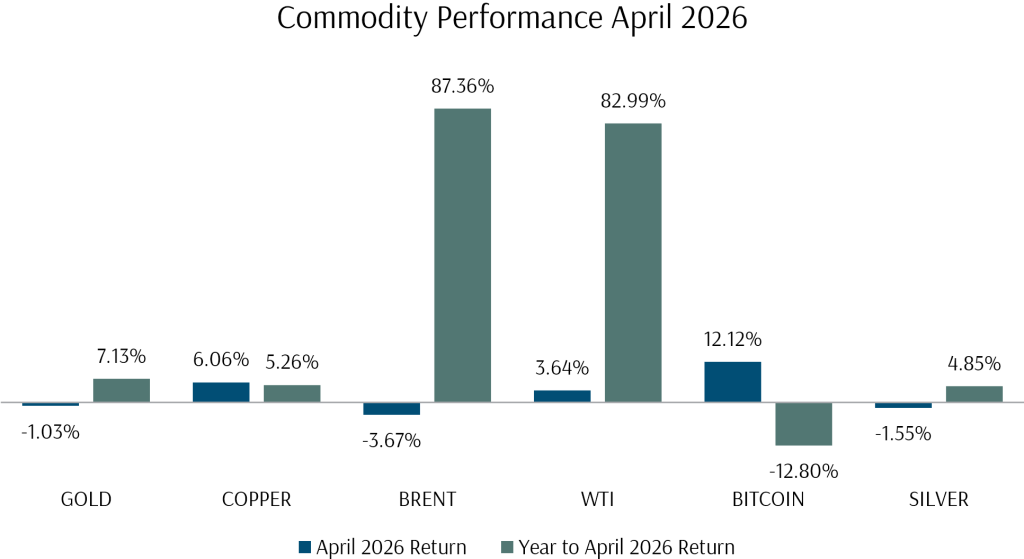

In commodity markets, the story was one of partial normalisation following March’s extreme moves. Crude oil declined from its elevated levels as the temporary Strait of Hormuz reopening removed some of the supply disruption premium, though prices remained well above start-of-year levels. Copper gained 6.06% on recovering industrial demand and growth sentiment. Precious metals gave back some gains, with gold down 1.03% and silver off 1.55%. Bitcoin rose 12.12%, partially recovering from its sharp February decline.

Exhibit 6: Commodity Performance April 2026

How Did Our Portfolio Funds Do in April?

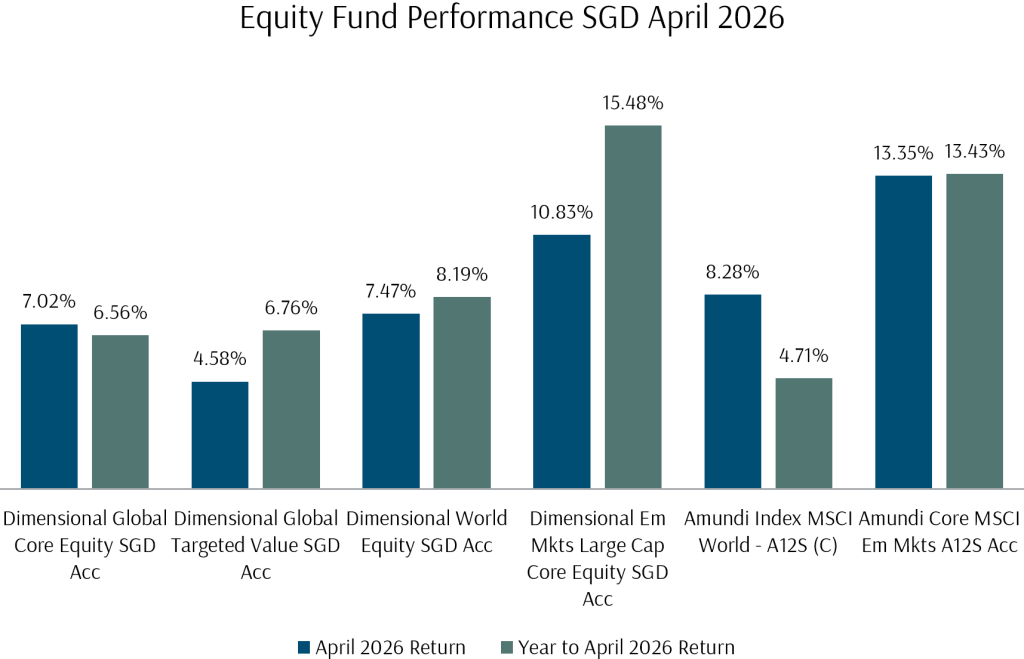

Exhibit 7: Equity Fund Performance April 2026 (SGD)

Portfolio fund performances were positive across the board, with equity funds posting strong gains and fixed income funds delivering modest positive returns.

April’s growth-led rally presented a headwind for value and small-cap factor tilts as technology and mega-cap growth stocks led the recovery. The DFA Global Core Equity Fund returned 7.02% in SGD terms, while the Amundi MSCI World Index Fund gained 8.28%. The DFA Global Targeted Value Fund returned 4.58%, reflecting the month’s growth leadership. Factor performance is inherently cyclical, and the value and small-cap tilts remain well supported by longer-term evidence, particularly as AI-related valuation concentration has increased dispersion within the market.

Emerging markets were again among the strongest performers. The Amundi MSCI EM fund gained 13.35% and the DFA EM Large Cap Core Equity Fund gained 10.83%, with the DFA fund’s value tilt explaining the gap. The breadth of the EM rally, spanning Korea, Taiwan, Greater China, and broader Asia, was notable.

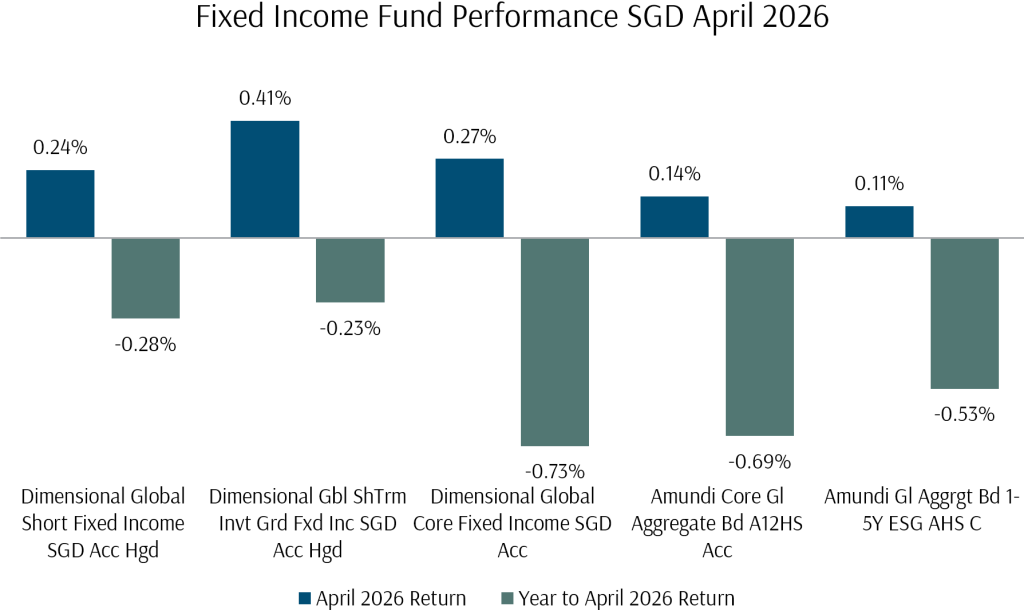

DFA fixed income funds delivered modest positive returns through April, with the Global Short-Term Investment Grade Fixed Income Fund gaining 0.41%, the Global Short Fixed Income Fund returning 0.24%, and the Global Core Fixed Income Fund adding 0.27% in SGD terms. The combination of modestly higher US yields and a stronger SGD resulted in muted fixed income returns, though the shorter-duration positioning of the DFA funds provided stability.

Exhibit 8: Fixed Income Fund Performance April 2026 (SGD)

Investment Questions: The April Rally and the Road Ahead

Q1: What drove the sharp rally in April?

April’s strong returns should be viewed in the context of March’s widespread declines, where the Iran conflict drove oil prices up approximately 63% and equity markets fell significantly. The recovery was driven by two reinforcing catalysts: first, the sequence of geopolitical developments through April, from the US-Iran ceasefire to the temporary reopening of the Strait of Hormuz, allowed markets to begin removing the risk premiums that had built up; second, the AI investment theme, which had been relatively stalled since late 2025, experienced a resurgence as commercial adoption accelerated and hyperscaler earnings confirmed the scale of the buildout.

The S&P 500’s 10.54% gain, while near historical highs for a single month, was consistent with the pattern observed in past recoveries from geopolitical shocks, where forward-looking markets reprice swiftly once the perception of resolution emerges.

Q2: Is the market getting ahead of itself?

The speed of the April rebound raised concerns that investors may have been overly optimistic. However, several factors suggested the rally had fundamental support.

For one, earnings estimates continued to rise. Consensus S&P 500 EPS estimates for 2026 and 2027 increased by approximately 4% since late January, according to research houses. This was in contrast to past episodes of geopolitical uncertainty, where earnings estimates typically flatlined or declined.

Valuations also became slightly cheaper through the rally. In mid-April, the S&P 500 forward price-to-earnings ratio sat at approximately 21 times, below the 22 times reached in January 2026 and near its five-year average. This was because earnings estimates had risen faster than prices.

Corporate actions, too, were supportive. Year-to-date share buyback authorisations reached a record $422 billion, and announced strategic M&A volumes were up more than 100% year-on-year. These were signals of corporate confidence in the outlook.

Q3: Is the AI boom becoming a bubble?

The question of whether the AI-driven rally constitutes a speculative bubble has been the subject of considerable debate. While we have written about this topic at length previously, a recent working paper from Amundi Research Institute provides a systematic comparison between the current AI-driven market and the dot-com bubble of the late 1990s, and the findings are informative.

Using a proprietary methodology that identifies AI-exposed stocks within the S&P 500, the researchers constructed AI and ex-AI portfolios and compared them with equivalent TMT (technology, media, and telecom) and ex-TMT portfolios from the dot-com era. The key findings are as follows.

On the surface, there are similarities. AI stocks have accounted for approximately 50% of the S&P 500’s total returns since 2023, comparable to the TMT portfolio’s contribution during the late 1990s. The cumulative performance of the AI portfolio from 2023 to 2025 bears some resemblance to the TMT portfolio during the 1997–1999 period. Market concentration is also elevated, with a narrower group of stocks driving a disproportionate share of returns.

However, the differences are more important. During the dot-com bubble, TMT valuations expanded continuously from 1997 to 1999, reaching price-to-earnings ratios above 54 times. In contrast, the AI portfolio’s price-to-earnings ratio has actually declined from 2023 to 2025, despite strong price appreciation. This means earnings growth has outpaced price gains, a pattern more consistent with fundamental re-rating than speculative excess. Statistical tests for explosive valuation dynamics, which were present in the dot-com period, are clearly absent in the current AI environment.

The dot-com boom was also characterised by strong momentum and trend-following behaviour, with TMT stocks showing little mean reversion in the late 1990s. The current AI rally shows more evidence of short-term corrections and pullbacks, suggesting that investors are reacting to fundamentals rather than pure hype.

The researchers conclude that the current AI episode lacks the “explosive valuation dynamics” typically associated with late-stage bubbles. The primary concern remains concentration risk. A narrow group of AI-related stocks has driven a large share of index-level returns, implying that standard index equity allocations carry significant implicit exposure to the AI factor, highlighting the need for broad diversification at the portfolio level.

Q4: What does the current earnings picture look like?

The earnings backdrop has been a key support for the rally. Q1 2026 earnings season, which was well underway by month-end, pointed to approximately 12% year-on-year EPS growth for the S&P 500, the strongest expectation heading into a quarter since 2021.

The late-April hyperscaler earnings releases provided concrete evidence that the AI investment cycle is translating into revenue and profit growth. Alphabet reported Google Cloud revenue growth of 63% year-on-year, with its revenue backlog nearly doubling quarter-on-quarter to approximately $460 billion, driven by enterprise AI demand. Amazon reported AWS revenue growth of 28% and total operating margins of 13.1%, the highest in the company’s history, while its Trainium custom silicon business grew 40% quarter-on-quarter. Results were more mixed elsewhere: Meta saw revenue near the high end of its guidance but operating income below expectations as elevated capital spending weighed on margins, while Microsoft delivered strong Azure growth of 39% but faced headwinds from weaker PC demand and rising component costs. Across the group, AI-related annual recurring revenue figures and revenue backlogs were consistently revised upward, pointing to sustained strength in coming quarters.

A substantial share of S&P 500 earnings growth is being driven by AI-related investment, estimated to account for roughly 40% of S&P 500 EPS growth this year. Hyperscaler capital expenditure is expected to total approximately $670 billion in 2026, a 64% increase over 2025. This spending is flowing through to revenues and earnings across the technology supply chain, from semiconductor manufacturers to data centre infrastructure providers to cloud services companies.

Q5: What about market breadth and concentration?

As noted above, the primary risk highlighted by research into the AI rally is concentration rather than valuation. S&P 500 market breadth has narrowed to one of its tightest levels since the dot-com era, with a small number of AI and technology stocks driving a large share of both index-level returns and earnings revisions. While this is not necessarily a bearish signal, as narrow breadth is a natural consequence of a rally driven by a specific catalyst. However, it does mean that any disappointment in AI-related earnings would have an outsized impact on index-level returns, and it reinforces the case for broad exposure and factor diversification.

Q6: What does this mean for my portfolio?

The events of March and April illustrate why attempting to time the market around geopolitical events is so difficult. Under the onslaught of alarming headlines at the end of March, investors who reduced their equity exposure or withheld new investments would have missed one of the strongest monthly recoveries in recent history. Markets reprice swiftly following the resolution, or the perception of resolution, of geopolitical events, and the window for re-entry is often extremely narrow.

Our portfolios are positioned to navigate both the risks and opportunities in this environment. The diversification and factor tilts that are core to our approach served their purpose through the March selloff, where value and non-US exposures cushioned the decline, and they continue to provide protection against the concentration risk that has built up in AI-related segments of the market. As discussed in the fund performance section, April’s growth leadership was a small headwind for these tilts, but over the year to date, the overall contribution has been constructive.

For investors looking to add to their investments, the residual geopolitical uncertainty and the potential for further oil-related volatility may present opportunities to deploy capital at more favourable levels. However, the most reliable path remains staying invested and allowing the long-term compounding effect to work. As the events of March and April have shown, the market’s ability to recover from shocks is often faster than expected, and investors who remain invested are the ones positioned to capture those recoveries.

Looking Forward to May 2026

Markets have entered May near all-time highs, with the S&P 500 holding the gains from its April rally and the Nasdaq continuing to push higher on the back of strong technology earnings. The MSCI All Country World IMI is up approximately 7% year-to-date, while emerging markets have been the standout performers, with the MSCI EM IMI up over 14% through April. Asia continues to lead, with the KOSPI’s year-to-date gain exceeding 64% as the semiconductor cycle extends.

The Q1 earnings season has been the focal point for markets. As detailed in this month’s Investment Questions section, the results have been supportive, with consensus earnings estimates for 2026 and 2027 continuing to rise through the reporting period. This provides fundamental support for the market’s advance and distinguishes the current environment from past episodes of geopolitical uncertainty, where earnings revisions typically stall.

One of the less discussed but increasingly relevant dynamics is the broadening of institutional participation in the AI theme. A significant pool of asset managers and allocators, many managing substantial institutional capital, may only now be beginning to engage with AI as an investment thesis. For much of the past two years, the rally has been driven by a relatively narrower set of investors who were early to recognise the scale of the opportunity. As these larger pools of capital begin to allocate, the demand dynamic for AI-exposed equities could strengthen further, particularly in the semiconductor and infrastructure segments where fundamentals, including high growth, strong margins, and relatively reasonable valuations, distinguish this cycle from previous technology booms.

On the geopolitical front, risks remain fluid. Iran’s flip-flopping on the Strait of Hormuz, declaring it open on 16 April before reversing course two days later, is a reminder that the conflict’s trajectory remains unpredictable. Oil prices have eased from their March peaks but remain well above start-of-year levels. On the monetary policy front, Chair Powell’s term as chair ends on 15 May, and he indicated he would remain as a governor for a period to be determined. The transition to a new chair introduces some uncertainty around the policy path, particularly given the growing divisions within the committee revealed at the April meeting. If a durable resolution to the Hormuz disruption materialises, the resulting decline in oil prices would ease inflation pressures and could allow the Fed to resume rate cuts, providing another catalyst for equity markets.

It is worth stepping back and noting that strong market gains are not, in themselves, evidence of excess. Just because markets have rallied sharply does not mean they are in a bubble. Just because a price chart resembles some prior episode does not mean a crash is coming. Sometimes strong gains are the result of fundamentals catching up to expectations, a fruition of patient investment rather than a warning sign. Nevertheless, markets that have risen this sharply in a short period are naturally more prone to bouts of profit-taking, and stretched positioning can amplify even modest catalysts on the way down. It would not be entirely surprising or alarming if a near-term pullback were to follow.

For diversified investors, the start to 2026 has been a useful reminder of both the risks and rewards of staying invested. Staying invested and grounded through periods of volatility and exuberance continues to be the most reliable path to growing wealth over time.

With a comprehensive plan already in place with your Client Adviser, covering near-term spending needs while allocating capital at a level of risk suitable for your longer-term goals, you can have the peace of mind to navigate market volatility and stay invested for the long term, allowing your wealth to compound and fulfil your ikigai. If you have any questions, please do not hesitate to reach out to your Client Adviser.

The writer of this market review, Glenn Tan, is Senior Portfolio Manager at Providend Ltd, Southeast Asia’s first fee-only comprehensive wealth advisory firm. He is also a CFA Charterholder and a Certified Financial Risk Manager (FRM).

For more related resources, check out:

1. Active Investing That Adds Value to the Client

2. Staying the Course: Investing With Confidence in Uncertain Times

3. Here’s Why We Charge a Higher Fee Than Robos

Download our Investment eBook titled “A More Reliable Way to Get Enough Investment Returns: Even During Times of Market Uncertainty” here.

With a minefield of financial misinformation out there, we promise to be a safe pair of hands and a second pair of eyes to help you avoid costly financial mistakes. Learn more about our investment philosophy here.

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current estate plan, investment portfolio, financial and/or retirement plan, make an appointment with us today.