Executive Summary

- May delivered strong global equity returns led by a return of technology and AI leadership. The S&P 500 reached a new all-time high, the Nasdaq posted its strongest monthly gain in years, and emerging markets continued to outperform on the back of the Asian semiconductor cycle. Bond yields diverged, with the US 10-year rising modestly while UK and Australian yields fell. Crude oil fell sharply on optimism surrounding a ceasefire with Iran, and gold pulled back after four consecutive months of gains.

- This month’s investment questions focus on the apparent contradiction between resilient equity markets and persistent headwinds from elevated oil prices, rising bond yields, and hawkish central bank rhetoric. We address why economic and earnings fundamentals have so far supported the rally, and why the inflation impulse from oil may prove less durable than feared.

- June opens with markets near record highs but facing a crowded list of risks, including the June FOMC meeting, elevated headline inflation, and an unresolved conflict with Iran. The AI capital expenditure cycle remains the dominant structural support for global equities, but valuations are stretched, market breadth is narrow, and the near-term path for oil prices remains uncertain. Diversified portfolios with factor tilts continue to provide balance across these competing forces.

May Market Summary

May was a strong month for global equities, driven by a return to technology and AI leadership after months of rotation into value, defensive, and non-US names. The S&P 500 closed the month at a new all-time high, completing its ninth consecutive weekly gain. Yet eight of the eleven sectors finished the month in negative territory. The strong gains seen in benchmark indices against the backdrop of such a narrow market were noteworthy, and a source of consternation for many market observers.

The US dollar was modestly firmer, as the market continued to price in a prolonged Fed hold and receding expectations for near-term cuts. In commodities, the most notable move was in crude oil, which fell sharply as speculation around a US-Iran ceasefire and the reopening of the Strait of Hormuz gained traction.

Bond yields diverged across major sovereigns. US yields rose modestly on the back of above-target inflation prints and hawkish FOMC commentary. Japan was the outlier, with JGB yields rising as fiscal spending plans and reduced central bank purchases pushed long-end rates higher. In contrast, UK and Australian yields fell, reflecting weaker domestic growth data and weaker-than-expected inflation numbers.

In equity markets, the narrative was dominated by the AI and semiconductor trade. Earnings from major hyperscalers and memory chip manufacturers confirmed continued acceleration in AI-related capital expenditure, with data centre demand showing no signs of plateauing. Micron, a leading memory chip manufacturer, entered the trillion-dollar market capitalisation club during the month. The software sector, which had been under persistent selling pressure since late 2025, posted its strongest monthly performance in over a year, as the semiconductor and hardware rally took somewhat of a breather towards the end of the month.

Outside the US, Asia continued its run. The AI memory chip boom powered further gains across Korean and Taiwanese markets, while Japan rose on earnings growth and valuation expansion despite rising JGB yields. Greater China underperformed, as the economy remained bifurcated between strong exports and weak domestic demand. The Trump-Xi summit in Beijing in mid-May set the stage for a year of trade negotiations, though the two sides appeared focused on different priorities, with the US emphasising near-term purchases and the Strait of Hormuz, and China focused on the Taiwan question and reducing dependence on the US dollar.

Central banks turned more hawkish in response to energy-driven inflation. Markets began pricing in potential rate hikes from the ECB and the Bank of England, while several Asian central banks raised rates to defend their currencies against the oil shock. The Fed held rates steady in April but with its most divided vote since 1992, underscoring growing tension within the committee over the appropriate stance.

Equity Market Performance

US Equities

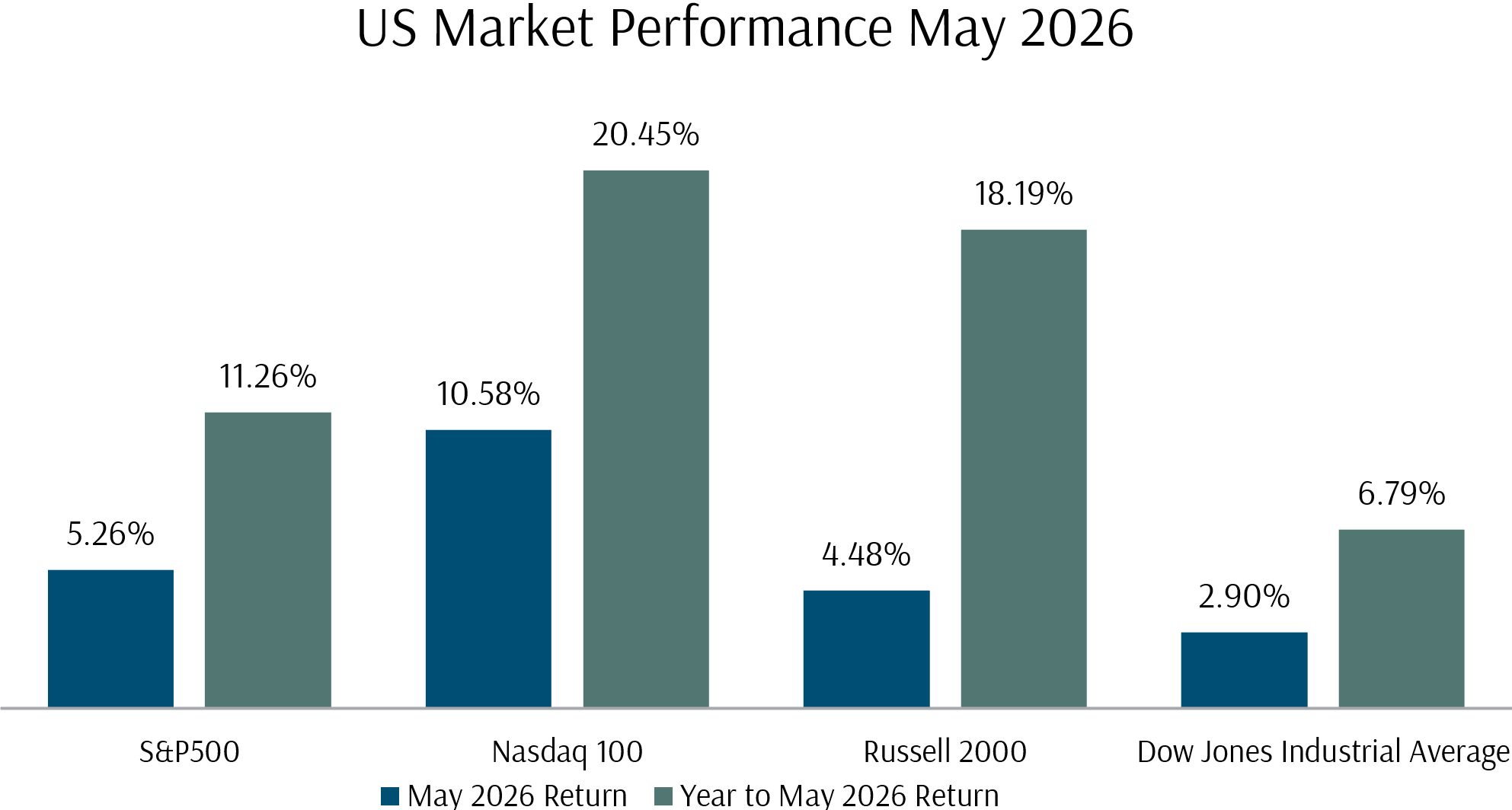

US equity markets were strong in May, with the S&P 500 rising 5.26% and the Nasdaq 100 up 10.58%. The S&P 500 reached a new all-time high of 7,580 on 29 May. Technology returned 19.76%, with the semiconductor ETF up 18.20% and software up 21.15%. Energy fell 5.63% and utilities declined 5.19%.

The Russell 2000 small cap index gained 4.48%, a solid return but below the large cap benchmarks as growth-oriented names outpaced value. Large cap growth outperformed large cap value by approximately 6% in the month.

US macroeconomic data was mixed. Headline CPI accelerated to 3.8% year-on-year in April, its highest level since May 2023, driven by a 17.9% jump in energy costs. Core CPI rose to 2.8%, also above expectations, though part of the increase reflected a statistical catch-up in shelter inflation following the October 2025 government shutdown. The labour market remained stable, with April nonfarm payrolls adding 115,000 jobs and the unemployment rate holding at 4.3%. However, real income growth turned negative, and the personal savings rate fell to 2.6%. The Federal Reserve held rates at 3.50% to 3.75% in April, with four dissents, the most since 1992, as three members advocated removing the easing bias and one favoured a cut. The next FOMC meeting is scheduled for 17 June.

Exhibit 1: Us Stock Market Performance May 2026 (USD)

International Equities

Elsewhere in the world, Asian markets saw another month of strong positive returns, as AI capital expenditure and semiconductor demand continued to drive gains, particularly in memory and advanced packaging segments.

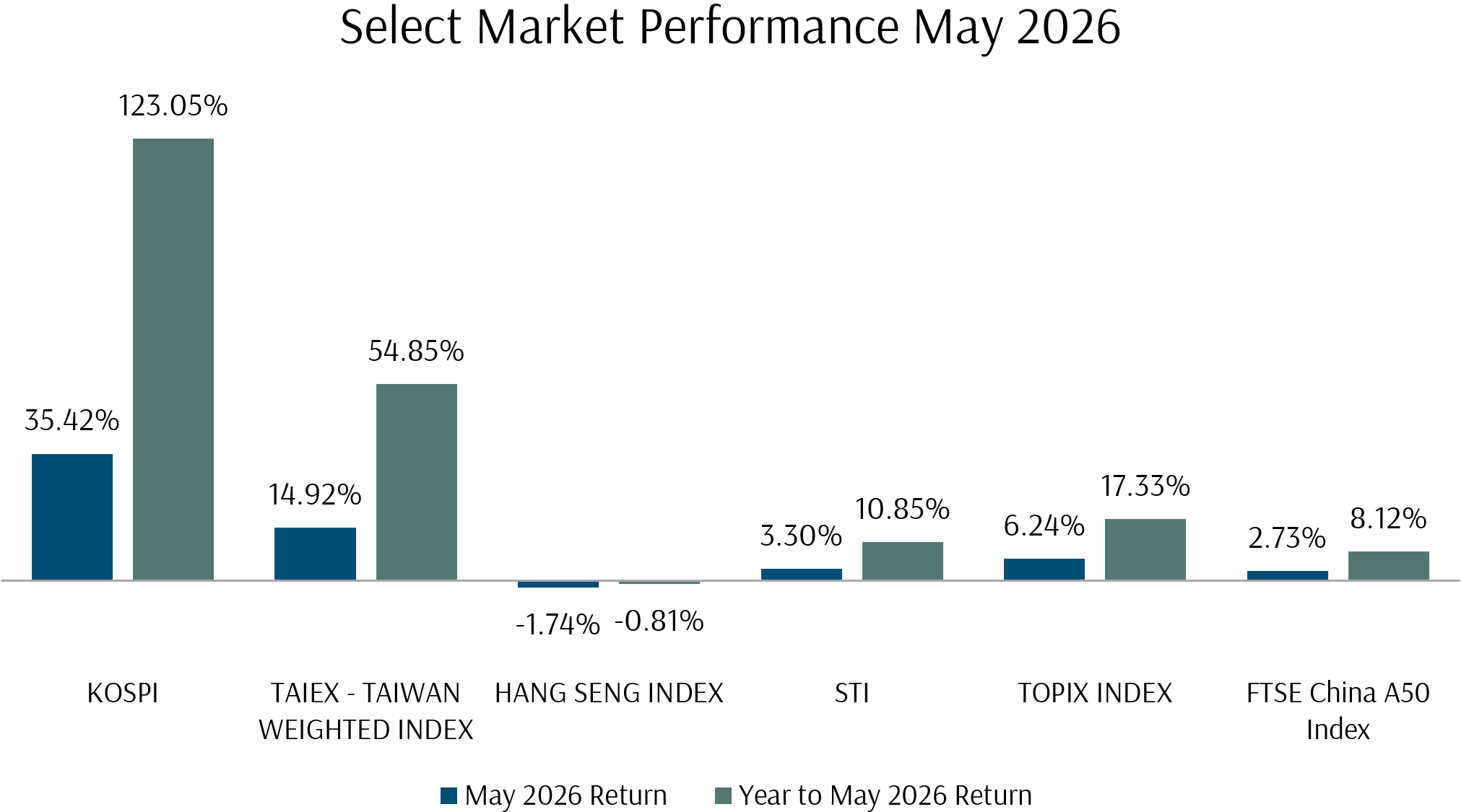

Korea’s KOSPI index was once again the standout, gaining 35.42% in the month, extending its year-to-date return to 123%. Taiwan’s TAIEX gained 14.92%, supported by strong earnings from semiconductor foundry and packaging names. Japan’s TOPIX rose 6.24%, though the JGB yield spike and fiscal concerns weighed on sentiment. Greater China was mixed, with the FTSE China A50 up 2.73% while the Hang Seng declined 1.74% due to weak domestic demand.

Locally, the STI index continued to perform well, rising 3.30% in May, supported by broad-based contributions from banks, industrials, and property names. Singapore’s position in the semiconductor supply chain and the data centre buildout provided additional support.

Exhibit 2: Select Market Performance May 2026 (Local Currency)

Global Summary

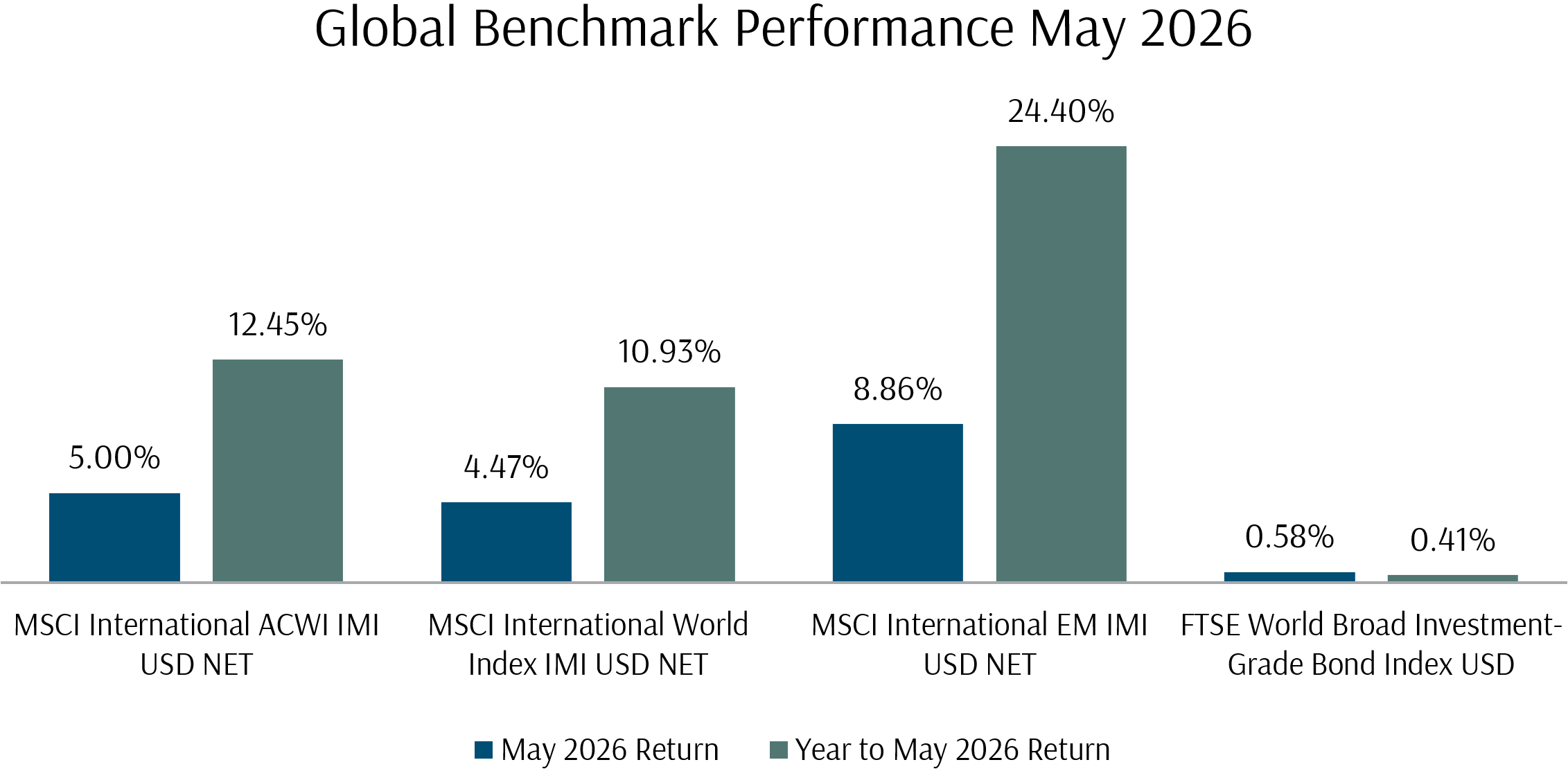

Globally, the combination of strong US technology performance and continued Asian outperformance drove global benchmarks higher. May was a strong month for global equity markets, with the broad MSCI All Country World IMI Index returning 5.00%.

Exhibit 3: Global Equity Benchmark Index Performance May 2026 (USD)

Cross-Asset Performance

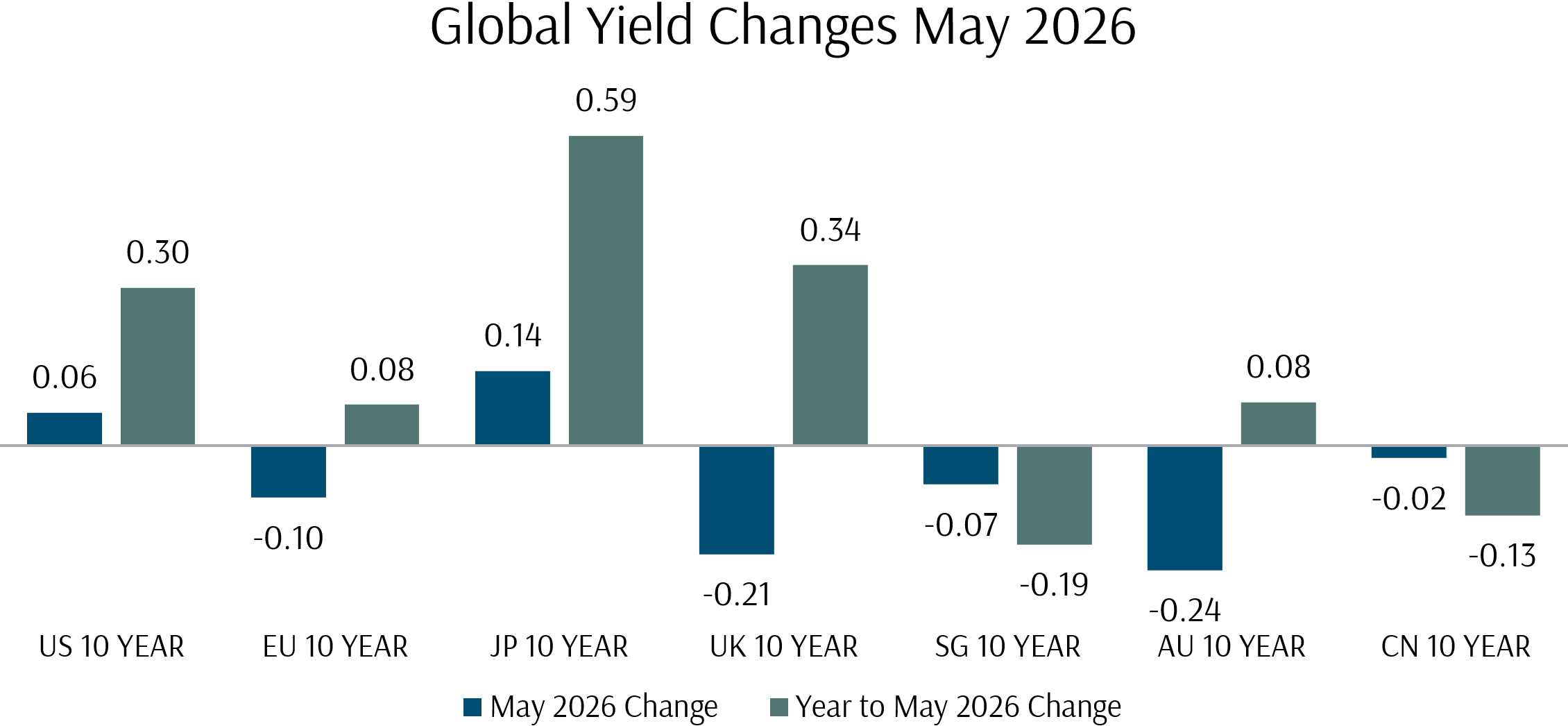

Fixed income markets were mixed in May. The US 10-year Treasury yield rose by 6 basis points to 4.45%, while Japan’s 10-year JGB yield rose by 14 basis points. UK 10-year yields fell by 21 basis points, Australian yields declined by 24 basis points, and EU 10-year yields fell by 10 basis points. Credit spreads remained tight, and the FTSE World Broad Investment-Grade Bond USD Index returned 0.58% for the month.

Exhibit 4: Global Yield Changes May 2026

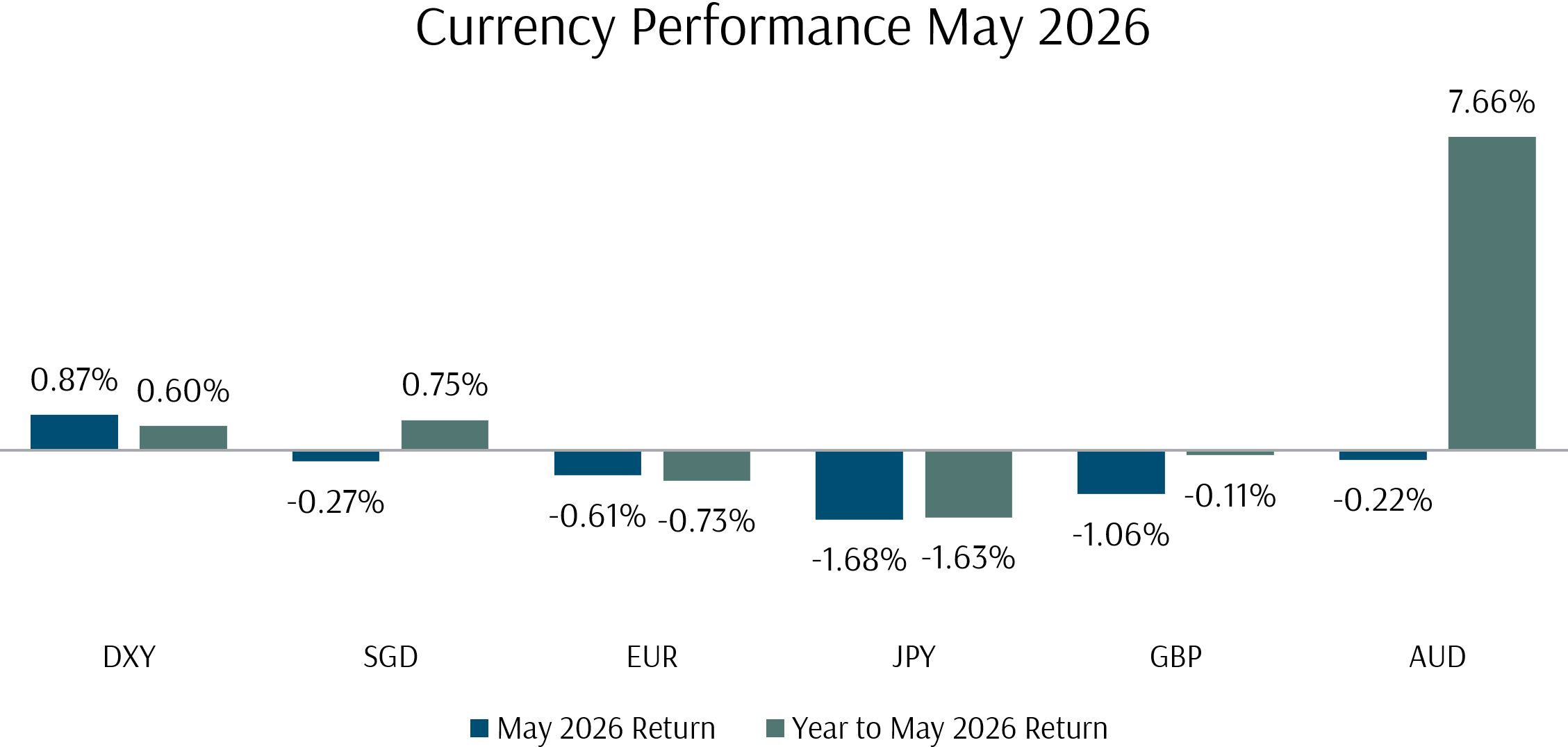

The US Dollar Index gained 0.87% over the month. The US dollar was roughly flat against the SGD, declining by 0.27%. The JPY weakened by 1.68% against the dollar as JGB volatility and policy uncertainty weighed on the currency. The EUR fell by 0.61%, the GBP declined by 1.06%, and the AUD was approximately flat.

Exhibit 5: Currency Performance May 2026

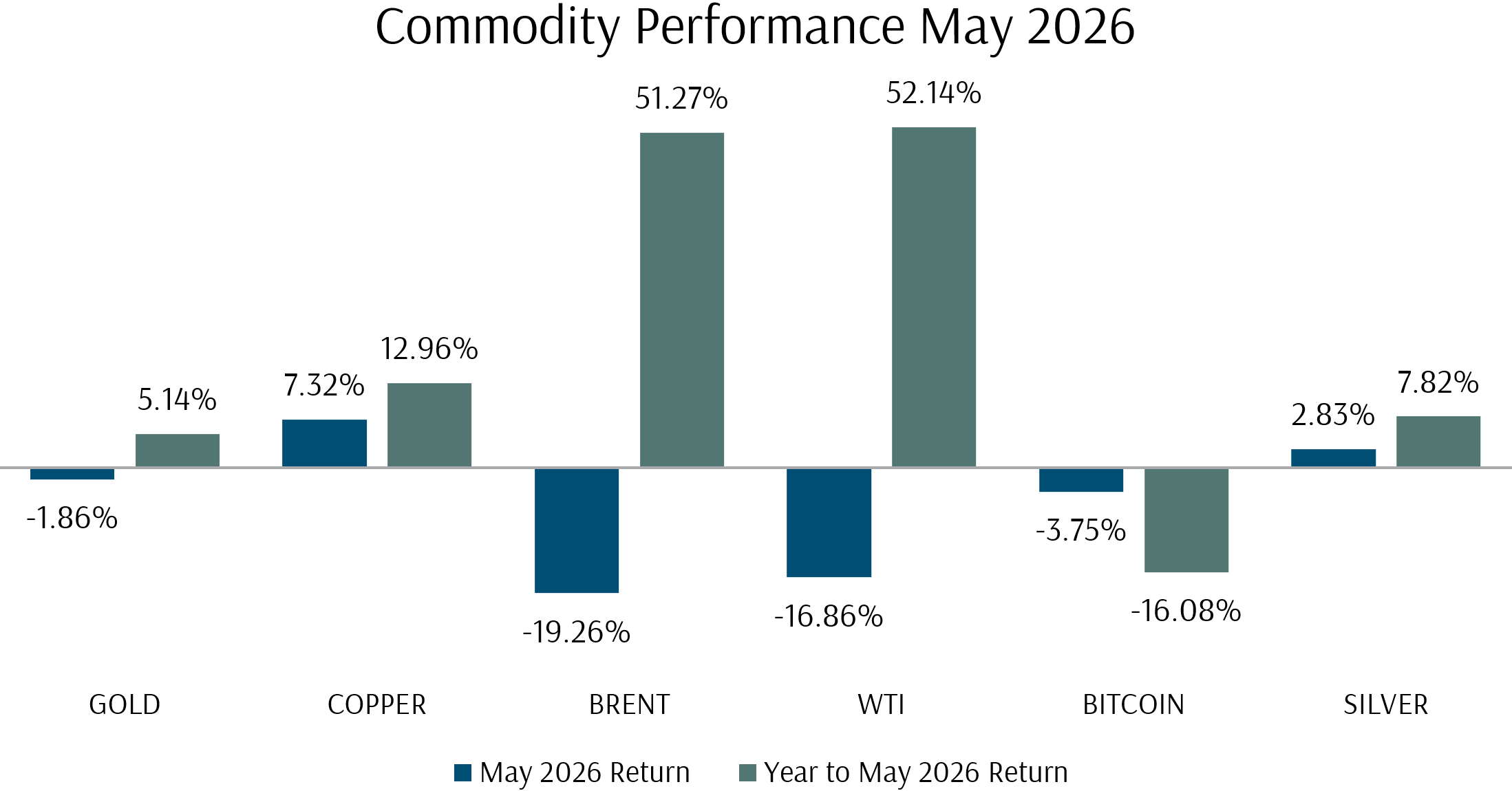

In commodity markets, Brent fell by 19.26% and WTI declined by 16.86% as speculation around a US-Iran ceasefire drove a sharp repricing of the geopolitical risk premium. Gold declined by 1.86%, as the safe-haven bid moderated alongside the improved geopolitical outlook and rising real yields. Silver gained by 2.83% on continued industrial demand, and copper rose by 7.32%, benefiting from AI-related data centre construction. Bitcoin fell by 3.75%, extending its year-to-date decline to 16.08%.

Exhibit 6: Commodity Performance May 2026

How Did Our Portfolio Funds Do in May?

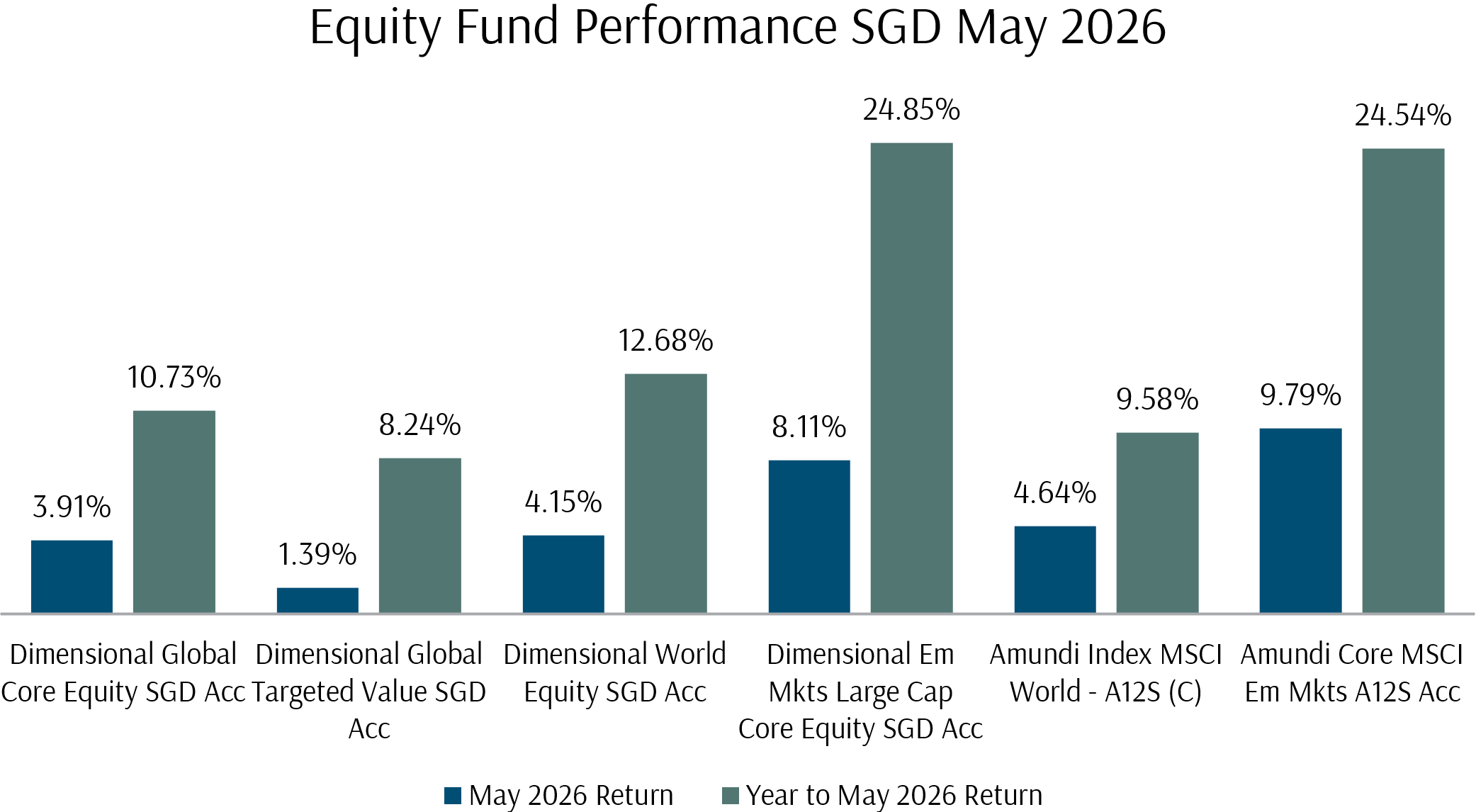

Exhibit 7: Equity Fund Performance May 2026 (SGD)

Portfolio fund performances were positive across the board. May was a month in which growth and large cap technology led, which meant value and small cap factor tilts did not add the same incremental outperformance as in preceding months.

DFA fund performances were solid. The DFA Global Core Equity Fund returned 3.91% in SGD terms, while the DFA Global Targeted Value Fund returned 1.39%, reflecting the month’s growth bias. The Amundi MSCI World Index Fund returned 4.64%, benefiting from its greater concentration in large cap growth names. The factor cycle is not linear, and months like May illustrate why diversification across both growth and value exposures remains important.

Emerging markets had the strongest returns, with the Amundi MSCI EM Fund gaining 9.79% and the DFA EM Large Cap Core Equity Fund gaining 8.11% in SGD terms respectively.

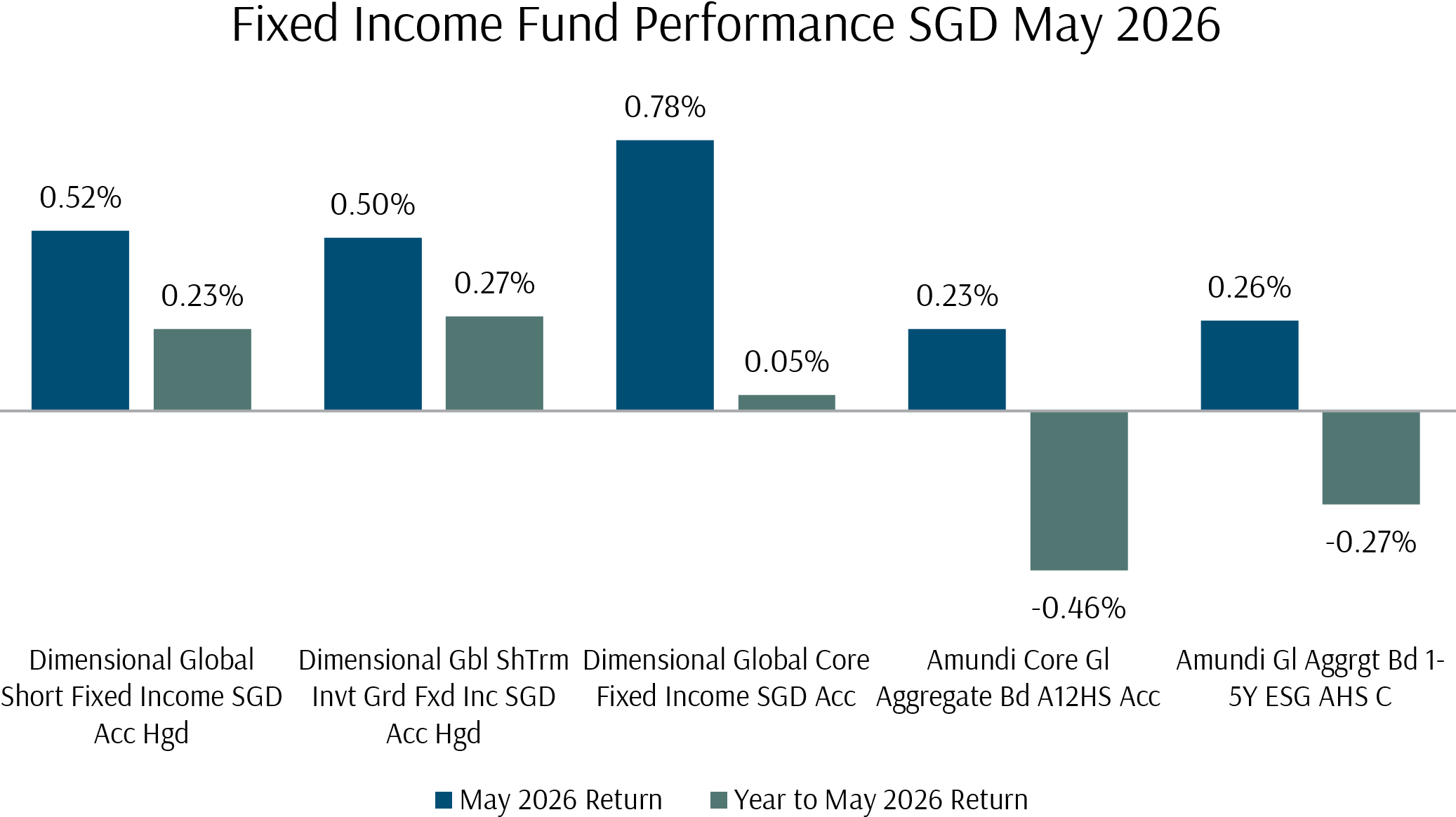

DFA fixed income funds delivered modest positive returns, with the DFA Global Core Fixed Income Fund gaining 0.78% in SGD terms and the shorter-duration funds returning 0.50% to 0.52%.

Exhibit 8: Fixed Income Fund Performance May 2026 (SGD)

Investment Questions: Resilient Markets Amid Conflicting Signals

Q1: Why do equity markets keep rising despite elevated oil prices and geopolitical risk?

The persistence of the equity rally, even as oil prices remain well above pre-conflict levels and the Iran conflict remains unresolved, has been one of the most discussed themes across research desks this year. Several factors explain the resilience.

First, the earnings cycle has remained strong. Q1 2026 reporting was positive, with US earnings growth tracking above expectations and global estimates revised upwards since the start of the year. AI-related companies in particular reported strong results, and the confirmation of continued capital expenditure commitments from major technology firms provided a powerful catalyst. Second, the AI investment boom has generated substantial positive growth spillovers for several economies, irrespective of the energy shock. The semiconductor supply chain across Korea, Taiwan, Japan, and Southeast Asia has been a direct beneficiary. Third, oil prices, while elevated, have not risen as much as initially feared. Pre-conflict inventories were higher than normal, demand destruction has been orderly (particularly in China, where the shift to electric vehicles and renewables has been substantial), and markets have maintained confidence that a policy response would prevent the most extreme price outcomes.

Q2: Should we be worried about rising interest rates and hawkish central banks?

The shift in central bank rhetoric has been one of the most notable developments of the past two months. The ECB is expected to deliver two 25 basis point hikes this year, the Bank of England may hike once, and several Asian central banks have tightened in response to the oil shock. The Fed is expected to remove its easing bias at the June meeting.

However, the inflationary impulse from oil is likely to prove temporary rather than structural. Research from multiple institutions shows that after previous oil price peaks, headline inflation falls quickly, typically within four months, while core inflation follows with a lag of approximately six months. In the US, consumer demand is softening, with real income growth turning negative and the savings rate at multi-year lows. Wage growth has decelerated to around 3.4% year-on-year, consistent with a labour market that is not generating sustained inflationary pressure. Alternative inflation metrics, such as trimmed-mean PCE, are running well below core PCE, suggesting that the headline figures are being distorted by a few volatile categories. The risk of rate hikes is present, but the underlying demand environment does not support a sustained re-acceleration in core inflation.

Q3: Is the AI rally sustainable, or is this a repeat of past technology manias?

The AI trade’s return to dominance in May was driven by concrete earnings delivery. Hyperscaler capital expenditure commitments, memory chip pricing, and data centre construction activity all confirmed that AI-related spending continues to accelerate. Analysts estimate that long-term earnings and dividends represent roughly 75% of fundamental equity value in the US market, and to the extent that AI improves productivity over time, the premium placed on AI-exposed names has a fundamental basis.

That being said, the concentration of returns is a legitimate concern. The rally has been driven by a narrow set of names, and positioning in US equities has become stretched. In the smaller-cap and speculative space, we are seeing signs of bubbly behaviour, such as massive volatility and outsized returns driven by very unsubstantiated catalysts.

Q4: How have Asian economies managed through the energy shock?

Asia’s resilience through the Strait of Hormuz disruption has exceeded expectations, for several reasons. Oil intensity has fallen across most Asian economies, and the capacity to adjust through electric vehicle adoption, remote work, and better urban transport is higher than in past cycles. The AI investment boom has generated direct positive spillovers for Korea, Taiwan, Singapore, Malaysia, and Vietnam. Asian policymakers have deployed substantial fiscal stimulus to cushion consumers and critical sectors. However, these buffers are being tested as the disruption extends, and vulnerable energy importers face tighter financial conditions. A prolonged oil shock would test these tailwinds.

Q5: What does this mean for our portfolios?

May was a month in which the pendulum swung back towards growth and technology. Our equity portfolios benefited from the broad market rally, with EM and Asia exposure adding the most value. Value and small cap tilts underperformed in May specifically, but year-to-date, these factors continue to outperform on a cumulative basis.

Factor performance will inevitably vary from month to month, and May’s growth dominance is a case in point. In periods like this, where market breadth has narrowed and a handful of AI-linked names account for the bulk of index returns, the importance of diversification across factors and geographies cannot be overstated. Concentrated rallies may prove to be fragile, and portfolios built on broad, evidence-based exposures will go some way towards mitigating downside risk.

Looking Forward to June 2026

Markets entered June near record highs, with the S&P 500 at 7,580 and the Nasdaq having delivered its strongest monthly return in years. The KOSPI and other Asian semiconductor-exposed indices continue to push higher. Oil prices remain elevated but off their peaks, with Brent at approximately $99 per barrel, as ceasefire negotiations continue.

The next risk event is the 17 June FOMC meeting, where the committee is widely expected to revise its inflation forecasts higher, shift its median dot to show no cuts in 2026, and potentially remove the easing bias language from its statement. However, the incoming data present a more nuanced picture than the hawkish pricing suggests. Real incomes are declining, the savings rate is at historic lows, and several leading indicators point to further softening in the labour market. The combination of lower oil prices (if ceasefire talks progress), softer jobs data, and dovish messaging from Chair Warsh could see markets begin to price out rate hikes later in the year.

On the AI front, there are emerging signs that the cycle’s most explosive growth phase may be moderating. Application download data for major AI products, including Claude, appears to have peaked, and the reception to the latest model releases, including Claude 4.7 and Claude 4.8, has been mixed relative to earlier generations. This does not invalidate the AI investment thesis, which is underpinned by capital expenditure commitments that span multiple years, but it introduces a question about whether the pace of end-user adoption will match the infrastructure buildout.

The Iran situation remains fluid. Reports suggest that a 60-day ceasefire and Strait reopening are under discussion, and market pricing has moved in favour of a resolution. A confirmed ceasefire would likely trigger a sharp decline in oil prices towards $80 per barrel and a broad relief rally in energy-importing equities. Conversely, a breakdown in talks would reverse the recent oil decline and reintroduce the supply shock dynamic.

For our portfolios, the combination of record equity prices, narrowing market breadth, and an unresolved geopolitical backdrop warrants a measured outlook. The underlying fundamentals, namely earnings growth, AI capital expenditure, and eventual monetary easing, remain constructive. However, the path from here is unlikely to be as smooth as the past two months have suggested. Staying invested and grounded through periods of both volatility and exuberance continues to be the most reliable approach.

With a comprehensive plan already in place with your Client Adviser, covering near-term spending needs while allocating capital at a level of risk suitable for your longer-term goals, you can have the peace of mind to navigate market volatility and stay invested for the long term, allowing your wealth to compound and fulfil your ikigai. If you have any questions, please do not hesitate to reach out to your Client Adviser.

The writer of this market review, Glenn Tan, is Senior Portfolio Manager at Providend Ltd, Southeast Asia’s first fee-only comprehensive wealth advisory firm. He is also a CFA Charterholder and a Certified Financial Risk Manager (FRM).

For more related resources, check out:

1. Active Investing That Adds Value to the Client

2. Staying the Course: Investing With Confidence in Uncertain Times

3. Here’s Why We Charge a Higher Fee Than Robos

Download our Investment eBook titled “A More Reliable Way to Get Enough Investment Returns: Even During Times of Market Uncertainty” here.

With a minefield of financial misinformation out there, we promise to be a safe pair of hands and a second pair of eyes to help you avoid costly financial mistakes. Learn more about our investment philosophy here.

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current estate plan, investment portfolio, financial and/or retirement plan, make an appointment with us today.