In the past month, since Finance Minister and Prime Minister Lawrence Wong announced the launch of the Lifetime Retirement Investment Scheme (LRIS) in 2028, there has been considerable discussion about what LRIS is and whether CPF members should participate when the scheme is finally introduced.

In this article, I hope to provide clarity on LRIS but more importantly, to explain it within the broader context of Singapore’s CPF Retirement Scheme and how CPF helps Singaporeans plan for retirement, whether they are affluent or simply the common man in the street.

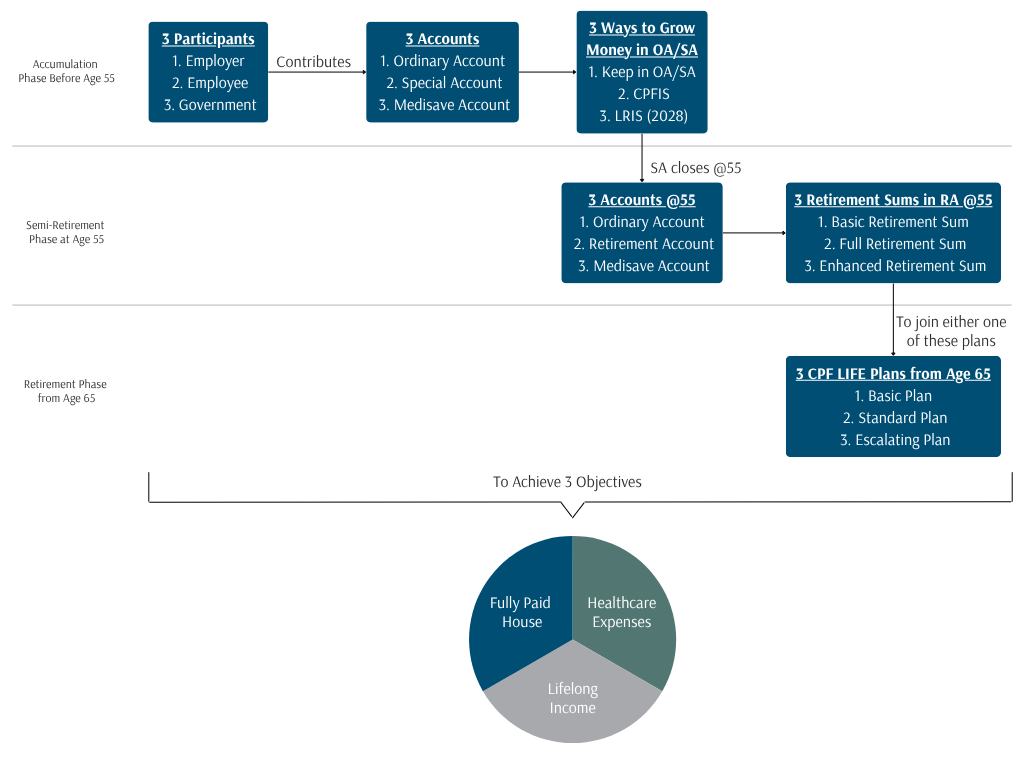

Many people do not realise that the CPF Retirement Scheme works almost like a framework built around sets of three in 3 life phases to achieve 3 objectives (see diagram).

Life Phase 1: The Accumulation Phase

First, there are three participants contributing to CPF:

- the employer,

- the employee, and

- the government, which contributes indirectly through the interest paid on CPF balances.

These contributions flow into three accounts:

- the Ordinary Account (OA)

- the Special Account (SA)

- the MediSave Account (MA)

Each account serves a distinct purpose. The Ordinary Account primarily helps Singaporeans pay for their housing mortgage so that they can eventually own a fully paid home. The excess after paying mortgage can form part of the retirement fund later. The Special Account is meant to accumulate funds for retirement. The MediSave Account helps to pay for healthcare expenses and insurance premiums such as MediShield Life, Integrated Shield Plans, ElderShield and CareShield Life.

For monies in the OA and SA, there are currently two ways to grow retirement savings. Members can simply leave their money in CPF and earn relatively high, near risk-free interest. Alternatively, they can invest through the CPF Investment Scheme (CPFIS) and from 2028, a third option will be introduced — the Lifetime Retirement Investment Scheme (LRIS). All of this takes place in what I call the first life phase: the accumulation phase.

Life Phase 2: The Semi-Retirement Phase

At age 55, CPF enters the next phase. Monies in the Special Account, up to the prevailing Full Retirement Sum (FRS), are transferred into a newly created Retirement Account (RA). Any excess in the SA is transferred to the OA and the SA is then closed. At this point, members effectively have three accounts again.

The Ordinary Account becomes relatively liquid. This allows members some flexibility and can support a gradual slowdown in work, what many may see as a semi-retirement phase. The Retirement Account holds the retirement sum and continues to grow until the member eventually joins the national annuity scheme, CPF LIFE, typically from age 65. The MediSave Account continues its role of supporting healthcare expenses and insurance premiums.

The retirement sum in the RA can be set at different levels:

- the Basic Retirement Sum (BRS)

- the Full Retirement Sum (FRS)

- the Enhanced Retirement Sum (ERS)

or any amount in between.

This stage of life represents a transition, a period where one may choose to slow down while preparing for full retirement.

Life Phase 3: The Retirement Phase

From age 65 onwards (up to age 70), CPF members join CPF LIFE, Singapore’s national annuity scheme. Members can choose among three CPF LIFE plans – Basic, Standard or Escalating Plan. CPF LIFE then provides income for as long as the member lives.

This marks the third life phase — retirement.

Across these three life phases, the CPF system is designed to help Singaporeans achieve three critical outcomes in life: a fully paid home, providing shelter and stability. Healthcare protection, supported by insurance and MediSave, and a lifelong income stream in retirement

What Is LRIS?

The Lifetime Retirement Investment Scheme (LRIS) was recommended by the CPF Advisory Panel (2014–2016), of which I was a member. At that time, the panel observed that many CPF members did not have a good investment experience when investing through the CPF Investment Scheme (CPFIS) due to two factors:

- First, many members lacked sufficient investment knowledge and experience.

- Second, investment costs were too high. Back then, it was not uncommon to see unit trusts with total expense ratios above 2 per cent a year. While fees have declined somewhat over time, they remain relatively high.

The purpose of LRIS is therefore to address these two issues — simplifying investment and lowering costs so that CPF members can potentially grow their retirement savings more effectively during their accumulation phase.

LRIS is expected to adopt a lifecycle investment approach, where younger members take on more equity exposure while the portfolio is automatically rebalanced to become more conservative as retirement approaches. But while LRIS may appear straightforward, implementing it is not necessarily easy. Lifecycle funds assume that younger investors can take more risk because they have more time to recover from market volatility. This may be true in terms of the ability to take risk, but it assumes that younger investors also have the willingness to take risk. In reality, willingness to take risk varies widely. It depends on factors such as investment literacy, past investment experience and personal life events that shape how comfortable someone feels with volatility.

Risk tolerance is far more complex than simply age.

At Providend, we have spent years refining how we assess our clients’ true risk tolerance. And the truth is, we need time to better understand their comfort with risk. It cannot be determined by a single factor at a single point in time.

Who Should Consider LRIS?

For high-net-worth and ultra-high-net-worth individuals, LRIS may not necessarily be the most optimal approach. When we design portfolios for clients, we look at their wealth holistically. CPF is simply one bucket of assets. It is also a bucket that provides relatively high, stable and low-risk returns. For some investors, it may therefore make sense to leave CPF untouched, while taking investment risk using other pools of capital.

For the common man in the street, LRIS can potentially be useful. But it is important to understand what it really means. Your CPF money will be invested in financial markets and privately managed. There is no government guarantee. Markets go up, but they can also go down.

Before investing, it is important to be educated. If you have a trusted adviser, you may wish to seek advice, though hopefully the advice is objective and not driven by incentives to sell CPF investments instead.

But for those who dislike volatility, do not really understand investments and have no interest in learning about them, there is nothing wrong with not investing your CPF savings.

I have often spoken about the 3Cs of financial security:

- Cashflow Management

- Coverage Management

- CPF Management

If you manage these three well, you may not accumulate as much as someone who invests successfully. But you will still have something very valuable – A fully paid home, Healthcare protection and an income that lasts as long as you live.

And when you reach the stage of life where work is no longer possible, when the paycheques stop and your energy slows, those three things may matter far more than whether your portfolio beat the market.

The writer, Christopher Tan, is Chief Executive Officer of Providend Ltd, Southeast Asia’s first fee-only comprehensive wealth advisory firm and author of the book “Money Wisdom: Simple Truths for Financial Wellness“. He is also a Certified Ikigai Tribe Coach.

The edited version of this article is published in The Business Times on 23 March 2026.

For more related resources, check out:

1. How To Make The Most Of CPF LIFE For Your Retirement

2. RetireWell™ Part 1: Drawing Down Retirement Money

3. Frequently Asked Questions About CPF

Providend promises to be a safe pair of hands and a second pair of eyes to help you avoid costly financial mistakes. You can find out more by reading our RetireWell™ eBook.

Being a trusted adviser to our affluent clients for over two decades, we know that our clients need the reliability and sufficiency of investment returns to meet their needs. You can learn more about our purpose-driven approach towards Wealth Management and Investment Management.

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current estate plan, investment portfolio, financial and/or retirement plan, make an appointment with us today.