2022 ended on a far more sombre note, and the 4th quarter rally in stocks fizzled out in December. Equity and bond indexes fell in December after central banks continued to remain committed to inflation-fighting and keeping rates high, the overriding theme that has driven market performance for the year. The S&P 500, MSCI World IMI, and MSCI Emerging Markets IMI fell 5.76%, 4.15%, and 1.36 respectively, while the Bloomberg Global Aggregate fell 1.18% for the month.

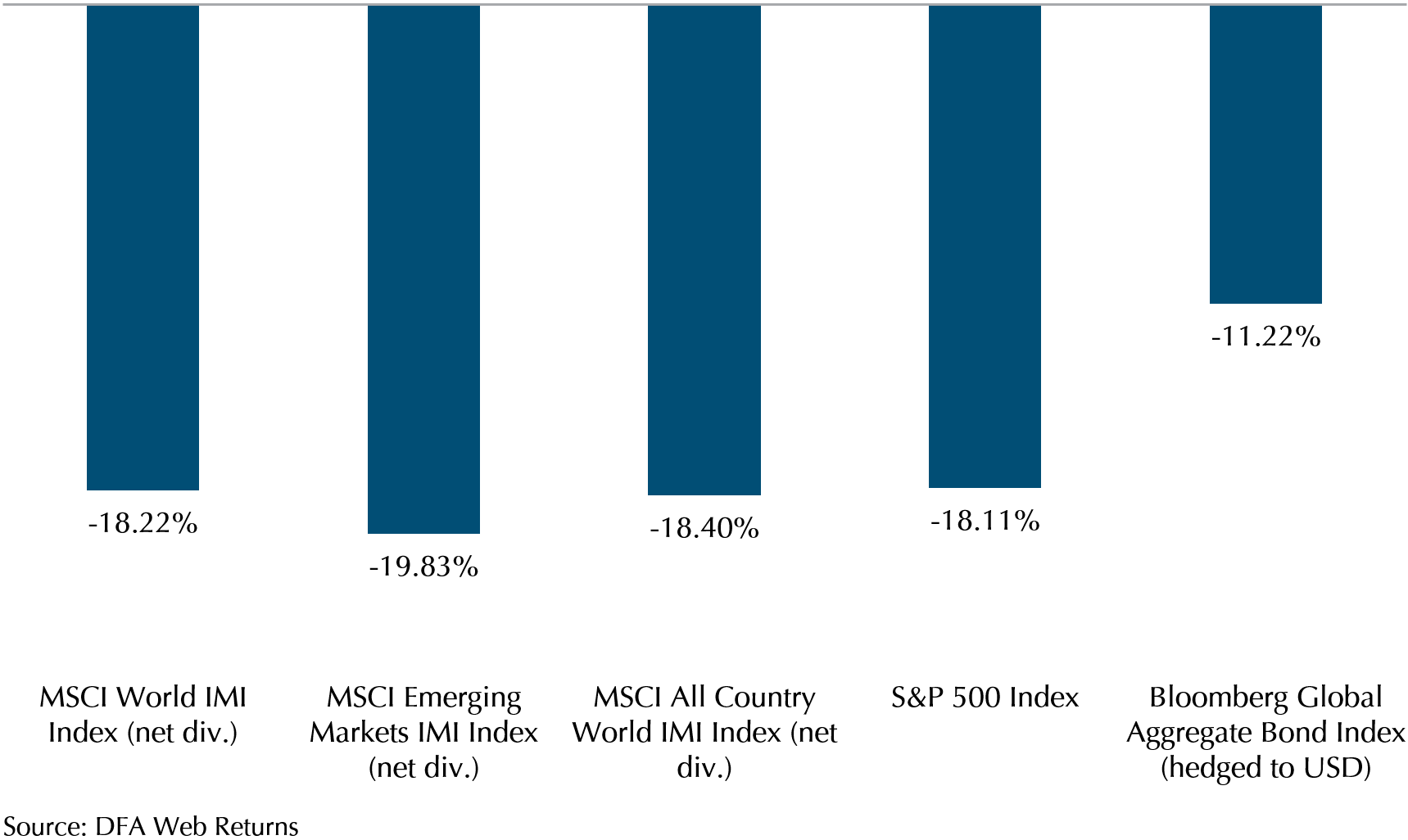

Zooming out to look back on the whole year, we see the impact of higher rates on financial asset prices. Global and EM stocks represented by the MSCI All Country World IMI Index fell by 18.4% while Global bonds represented by the Bloomberg Global Aggregate fell by 11.22% in 2022, its worst performance since the index was created in 1990 (Exhibit 1).

Exhibit 1: Index Performance 2022

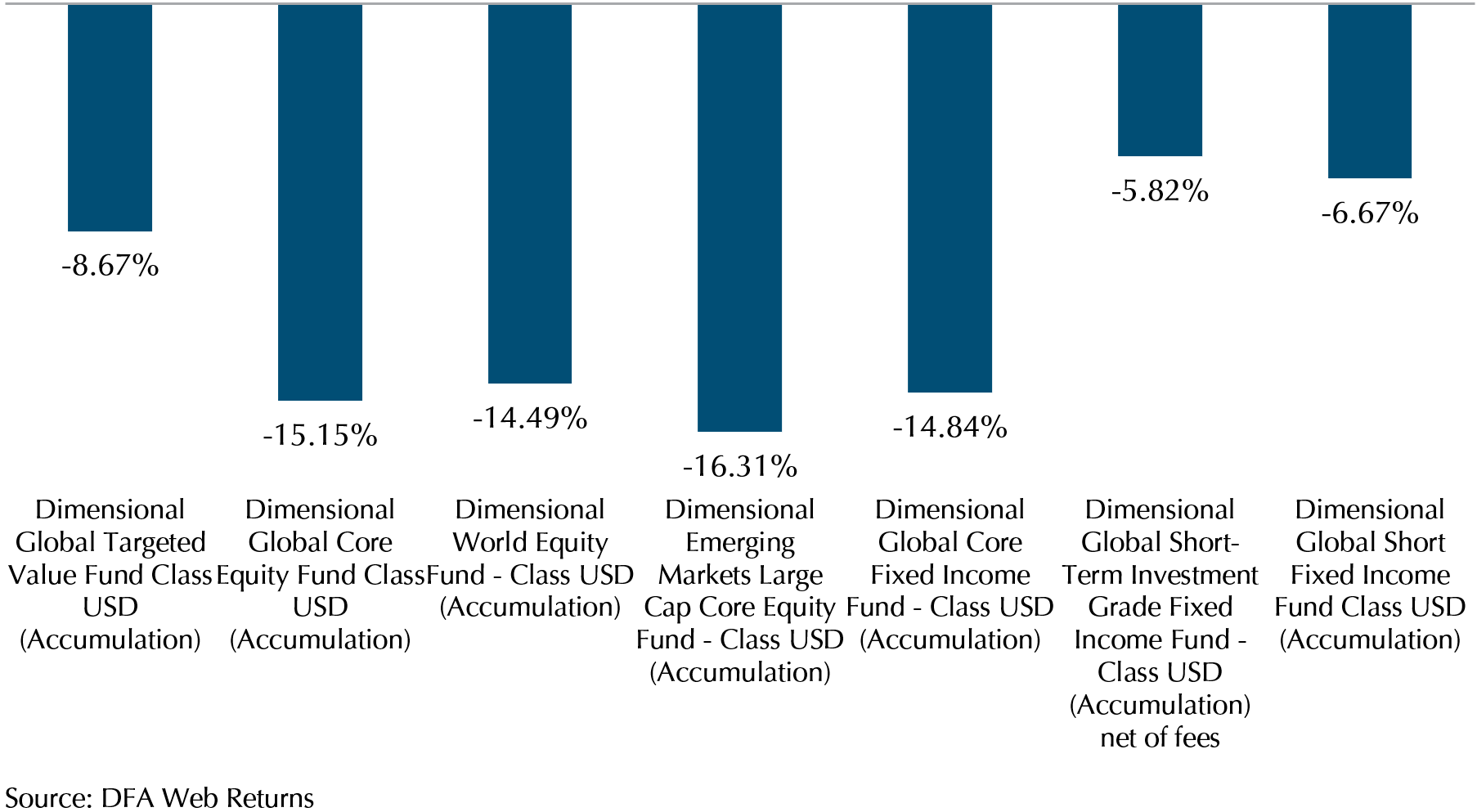

While it has been a challenging year for both stocks and bonds, one bright spot for Providend clients is that our tilts towards value stocks paid off handsomely this year, as value stocks continued to outperform growth stocks.

The DFA World Equity Fund, which holds both Global and EM stocks and is comparable to the MSCI ACWI IMI, fell 14.49% over 2022, which represents a 3.91% outperformance for the year. In fact, the fund with the strongest value tilt, the Global Targeted Value Fund, only fell 8.67%, a staggering 9.55% outperformance over the MSCI World IMI and 9.44% outperformance over the S&P 500 (Exhibit 2).

While performance across the board is negative in line with the markets, our portfolio positioning has at least mitigated some of the pain for client portfolios.

Exhibit 2: DFA Fund Performance 2022

A look back at 2022

As we usher in 2023, we review the major events of 2022 that were key drivers of market performance and their possible impact on markets in 2023.

1. The Russia-Ukraine War

Russia’s invasion of Ukraine on February 24 shattered a long period of peace in Europe and kicked off a period of heightened inflation for the world.

As a reaction to the aggression, the United States (US) and European Union (EU) imposed severe sanctions on Russia. A crude oil price cap was introduced to Russian oil and Germany froze the Nord Stream 2 project, a pipeline to transport natural gas from Russia to Germany. In addition, the EU announced a ban on Russian oil imports and cut back on importing Russian natural gas by two-thirds at end of 2022. Highly dependent on Russian natural gas for energy, this pushed EU inflation to some of the highest levels seen since World War II.

As a result, major central banks were pushed to deal with inflation with even more urgency as both food and energy prices spiked sharply after the start of the war.

2. Non-transitory Inflation

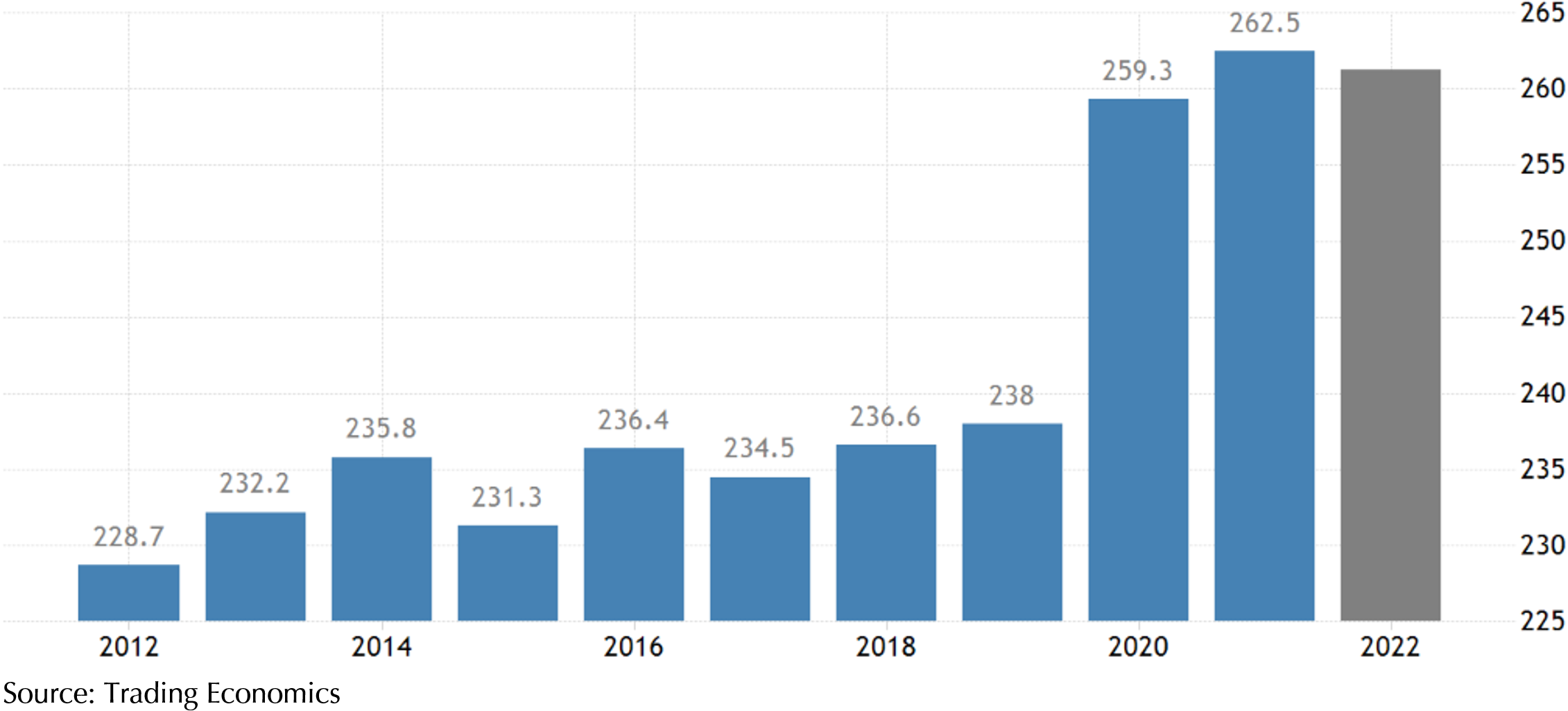

At the start of the Covid pandemic in 2020, the Fed, ECB, and BoJ started reacting to lockdowns with unprecedented quantitative easing to stimulate demand, using the old playbook for reviving an economy in recession. The Fed’s balance sheet ballooned from 4.3 trillion in March 2020 to a peak of almost 9 trillion in May 2022 (Exhibit 3). Japan’s Debt to GDP ratio also rose from 238% in 2019 to a peak of 262.5% in 2021 (Exhibit 4), the highest in the world.

Exhibit 3: Federal Reserve’s Total Assets (in millions of dollars)

Exhibit 4: Japan’s Debt to GDP

This unprecedented stimulus drove demand higher even as supply was affected by the pandemic restrictions and lockdowns even into 2021. However, the Federal Reserve characterised the rising inflation as “transitory” due to temporary supply and demand imbalances. The US central bank continued to maintain its low interest rates as well as quantitative easing throughout 2021, causing them to miss a key window to adjust monetary policy to deal with inflation.

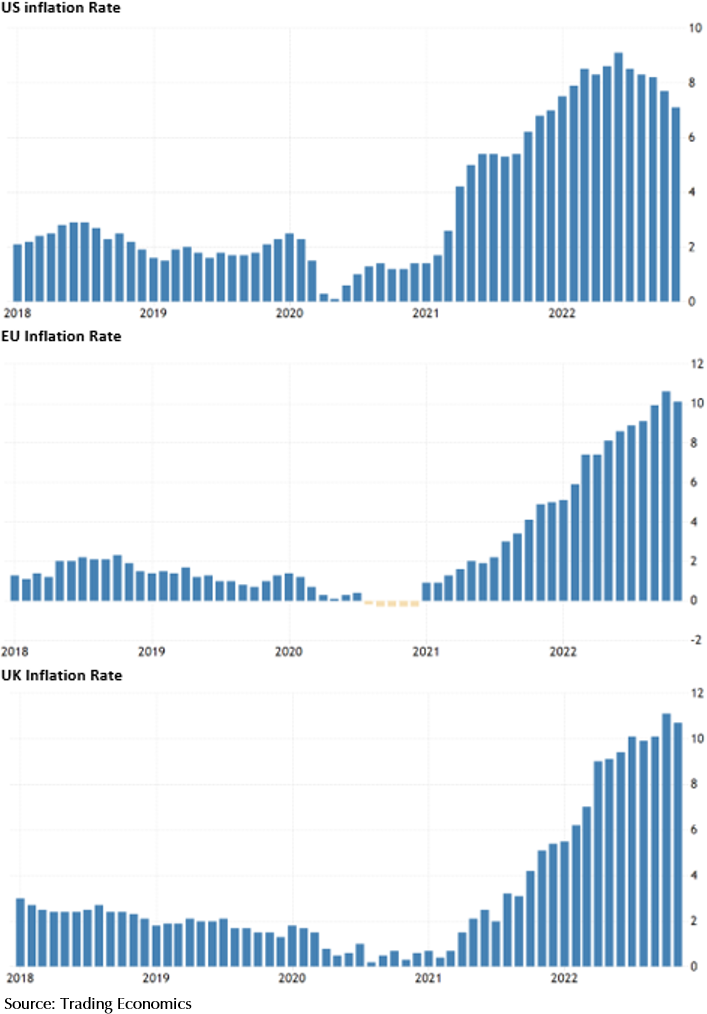

Entering 2022, the inflation rate in the US climbed to 7.5% in January and continued to climb to a peak of 9.1%, 10.6%, and 11.1% in the US, EU, and UK respectively (Exhibit 5). This time, in response to price levels rising at the fastest pace in 40 years, the Federal Reserve changed its stance and started signalling that it would raise interest rates and keep them higher to combat inflation.

Exhibit 5: US, UK, and EU Annual Inflation

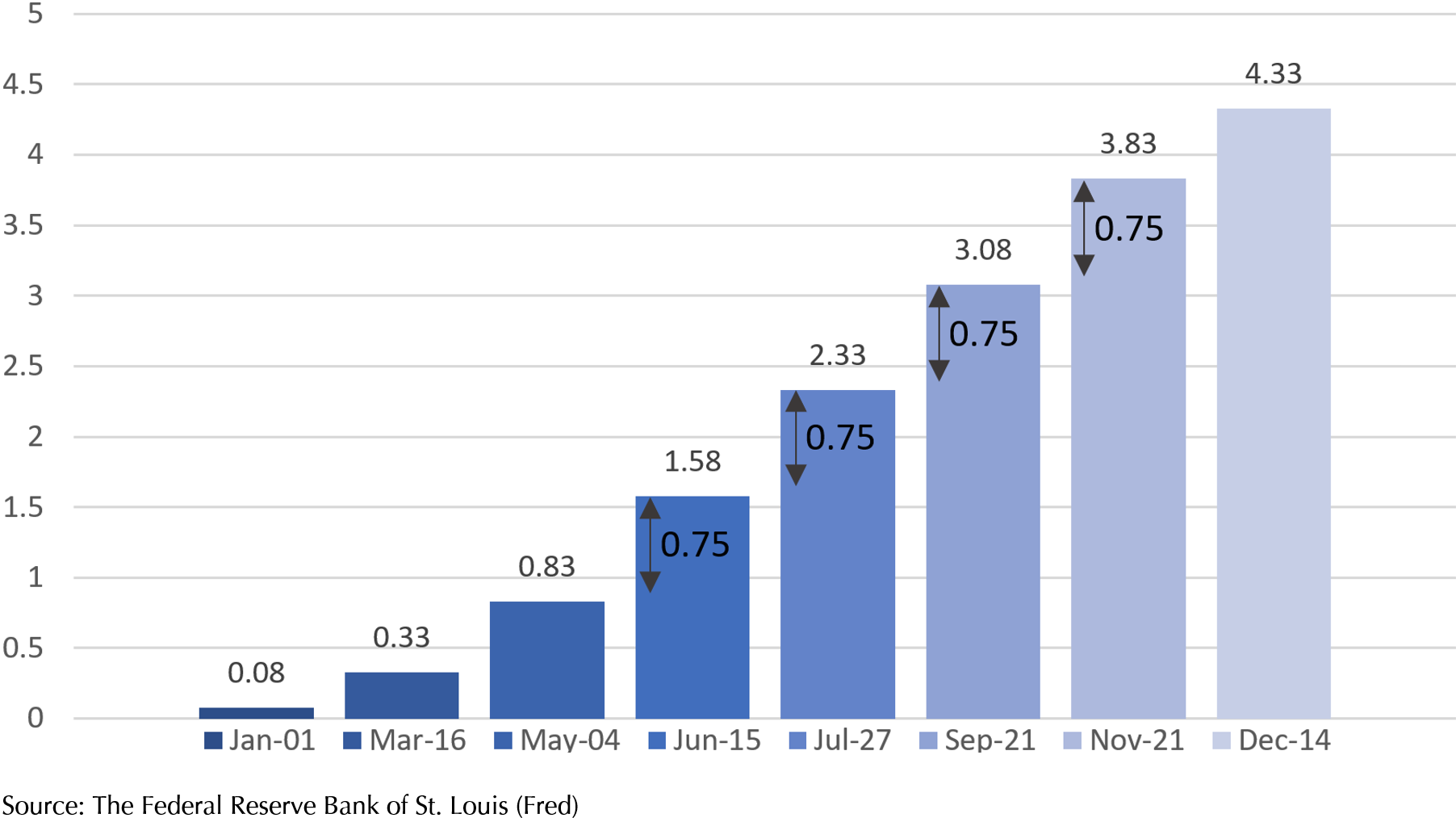

The Federal Reserve hiked rates 7 times over the course of the year and the effective Fed funds rate rose from 0.08% to 4.33% (Exhibit 6). The rise in interest rates caused yields to climb and bond prices to fall. The stock market also fell as a higher discount rate pushed down valuations. In addition, the uncertainty of the impact of higher rates on the economy has also led markets to price in a possible recession in 2023.

Exhibit 6: Effective Fed Funds Rate Change 2022

3. EM Debt Crisis

A stronger US dollar driven by the aggressive Fed rate hikes spilled over into Emerging Markets debt, as seen in the unfortunate Sri Lankan default in 2022.

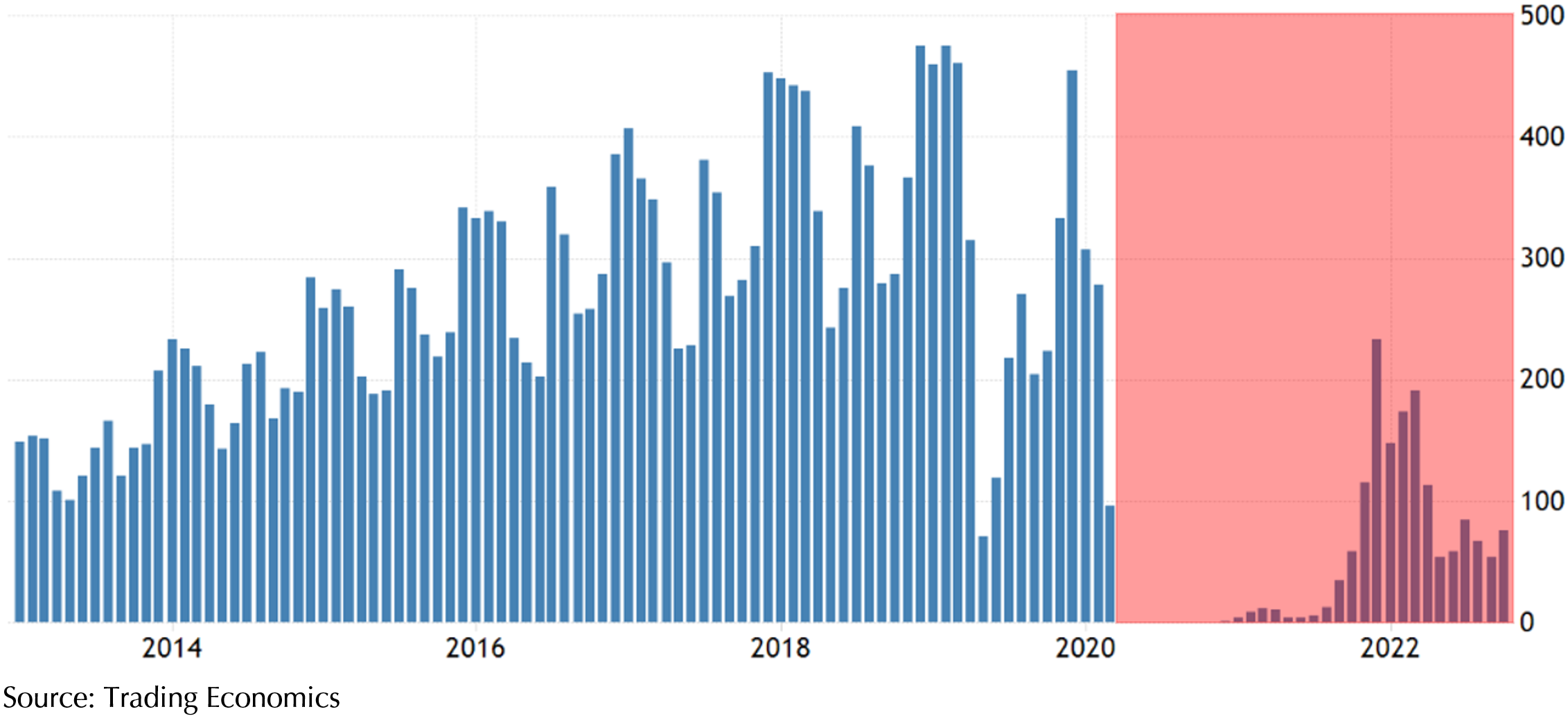

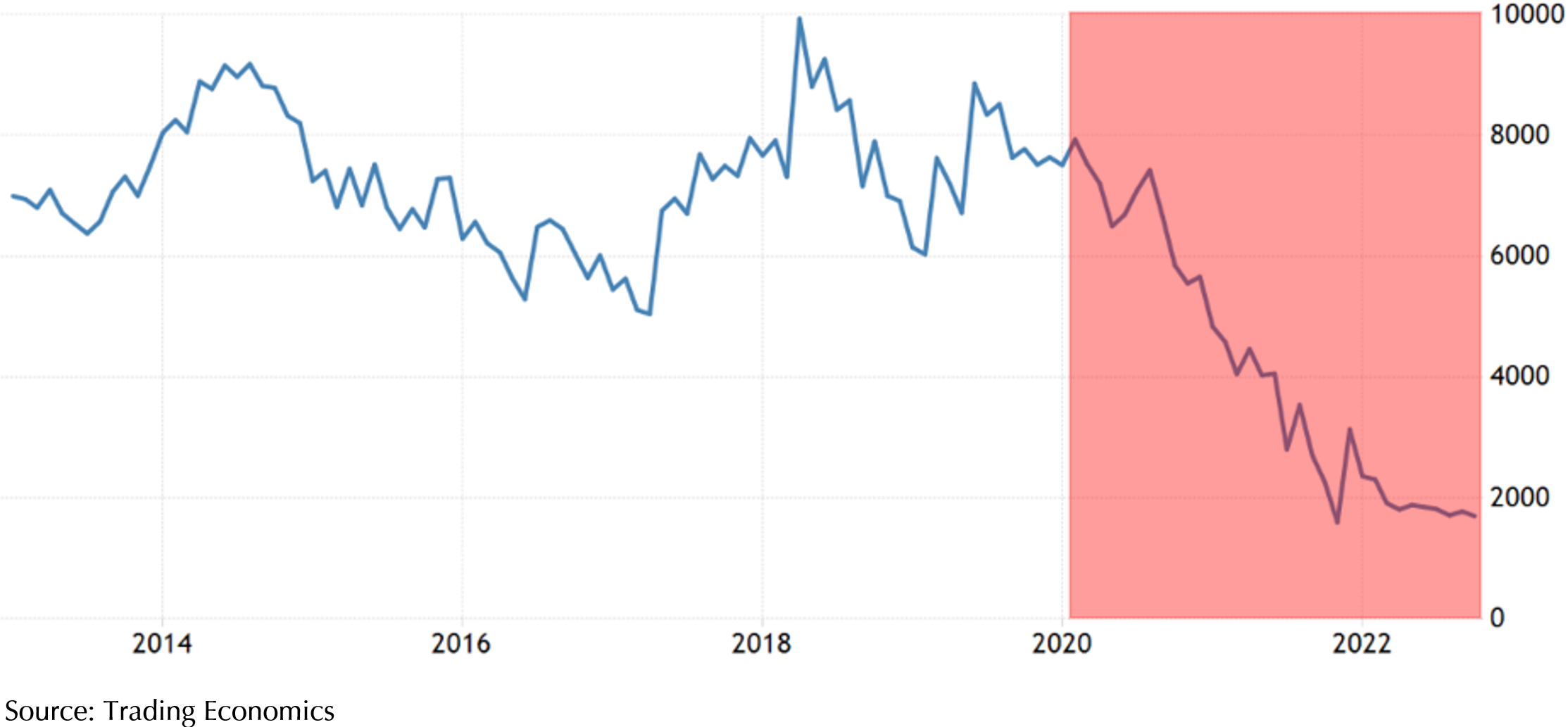

The Covid-19 pandemic hit Sri Lanka badly as 22% of its GDP was from the tourism sector. Revenues from tourism vanished after March 2020 (Exhibit 7) causing it to lose a key source of foreign income. At the same time, Sri Lanka is dependent on imports for necessities, especially food and energy – both of which were short in supply globally during 2022. The loss of foreign income from tourism and rising import costs led to a drastic fall in its foreign exchange reserves starting in 2020 (Exhibit 8). To make matters worse, Sir Lanka’s Prime Minister Gotabaya Rajapaksa in May ordered a halt to importing fertilisers and pesticides to reduce dependency on imports and turn the island’s agriculture sector to 100% organic. The decision led to declining crops and further shortage of food, forcing the nation to import more food instead.

Exhibit 7: Sri Lanka Tourism Revenues

Exhibit 8: Sri Lanka Foreign Exchange Reserves

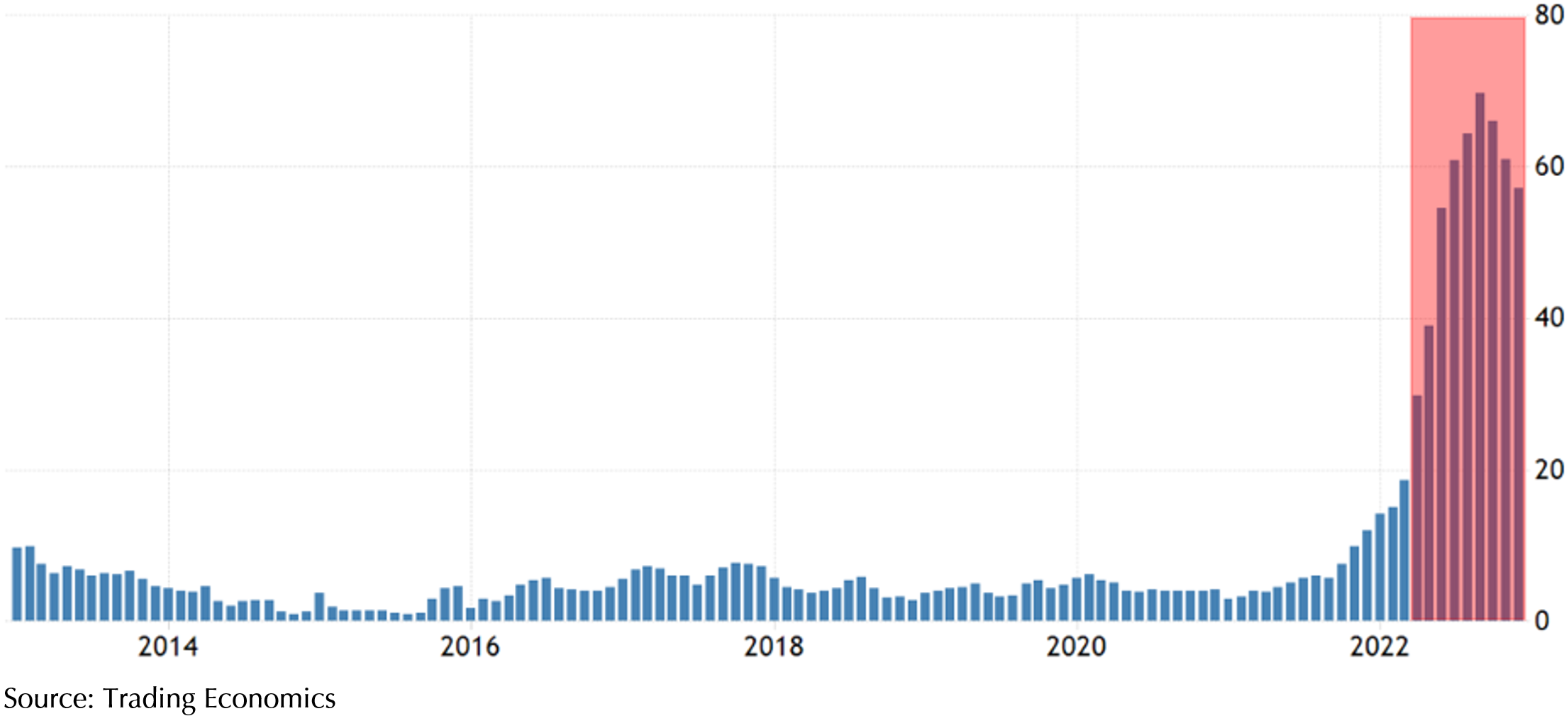

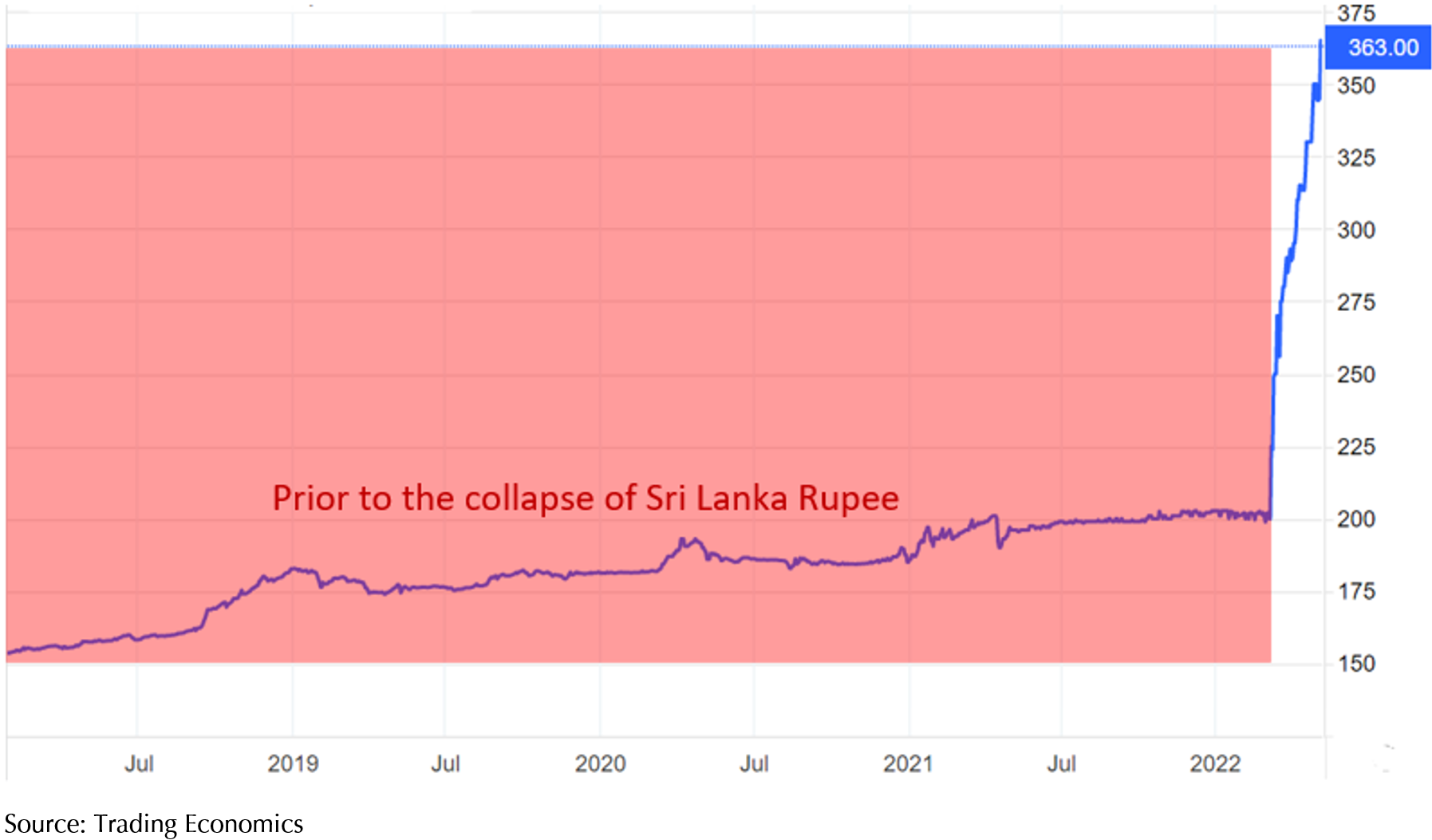

Struggling to service its growing external and domestic debt, the government resorted to money printing which caused the inflation rate to climb up to 70% per month in 2022 (Exhibit 9). The Sri Lankan government also kept its currency from depreciating against the USD (Exhibit 10) to prevent import costs from rising. By March 2022, Sri Lanka was left with only US$1.9 billion in its reserves against a debt obligation of US$8.6 billion. With no other options left, on April 12, 2022, Sri Lanka announced that it would suspend all foreign debt payments and triggering the first sovereign default in its history.

This has heightened concerns that other EM countries with weak fiscal positions will lose access to capital markets and trigger an unexpected wave of destabilising EM defaults in 2023.

Exhibit 9: Sri Lanka Inflation Rate

Exhibit 10: Sri Lanka Rupee Collapse

4. The End of Zero-Covid in China

Accounting for 30% of the world manufacturing output, China’s zero-Covid policy has exacerbated supply chain disruptions globally, particularly during the Shanghai lockdown in early 2022. Since then, supply chain pressures have eased, but the policy has affected domestic consumption and led to China reporting its weakest GDP growth since the 1980s.

The policy change in December to end the zero-Covid policy is very timely as it is likely to revive the Chinese economy and benefit the global economy in 2023 with increased tourism, commodity demand and consumption. However, this might also trigger some inflationary pressures, particularly in commodity prices if supply does not ramp up to meet the demand.

What’s next for markets in 2023?

Looking ahead, financial markets are likely to remain volatile in 2023 as uncertainty around inflation, interest rates and economic growth persist.

China’s reopening will be a bright spot for global growth. However, the US and EU are looking at a possible recession as higher interest rates continue to take their toll on demand. Even though demand for goods has fallen and supply caught up, economies are still seeing relatively high inflation numbers due to a shortage of labour, leading to inflationary price increases for services.

This means that central banks are unlikely to adjust their monetary policy in 2023, keeping interest rates at the highest levels since 2008. In fact, should inflation persist, the Fed might be forced to raise its interest rates higher than the 5.25% currently projected. One of the downside risks to this view is that rates end up going higher than expected, as investors have probably priced in rates going up to 5.25% and are valuing both stocks and bonds accordingly.

Another risk that has been less discussed is some form of EM debt crisis, as a stronger US dollar, coupled with higher borrowing costs put pressure on the fiscal position of some of the more indebted EM countries. Any event like that is likely to also trigger some downside risks to financial assets, particularly EM bonds.

However, should there be surprises with lower inflation or an end to the Ukraine war, we are likely to see markets surprise to the upside.

Please note that these are just some possible scenarios for 2023, and that Providend does not attempt to forecast the direction of stocks and bonds when implementing client portfolios.

What should an investor do in 2023?

If you are already invested, staying invested in a diversified global portfolio of stocks and bonds will help you capture the market returns. With bond yields much higher now than at the start of 2022, the expected returns of a 60/40 portfolio have improved. Sharp falls in equity prices over 2022 have also improved valuations and future returns for stocks, especially for Developed markets ex-US and EM. Staying diversified will give exposure to the best-performing stock markets or sectors in 2023.

Investors should also review their wealth goals in light of the higher interest rate environment we are in and have a discussion with their adviser on any new goals or plans that might require an adjustment to the risk parameters for their investment plan.

2022 was challenging in many different ways for investors, and 2023 looks like it will continue some of the themes that have gripped markets for the past year. Providend advisers stand ready to weather the storm with you, and to guide you to make the right investment decisions to make your wealth plan a success.

We look forward to continuing our journey with you in 2023 and would like to wish you a very Happy New Year!

Warmest Regards,

Investment Team

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current estate plan, investment portfolio, financial and/or retirement plan, make an appointment with us today.