Executive Summary

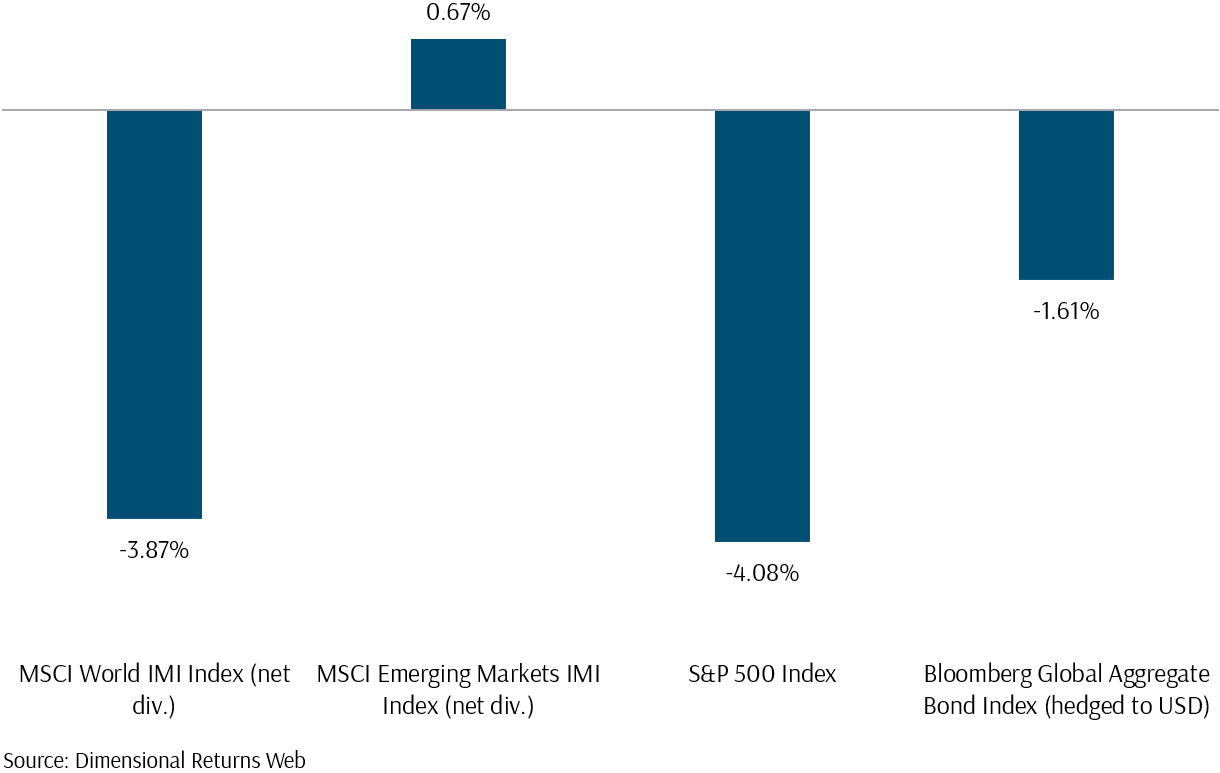

In April, the stock market rally paused as both equities and bonds saw significant declines amidst reports of persistent inflation in the US, which reduced the likelihood of Federal Reserve rate cuts. This unexpected inflation led to higher US yields and increased borrowing costs for companies, putting pressure on earnings and resulting in a 4.08% decrease in the S&P 500 Index and a 1.61% decline in the Bloomberg Global Aggregate Bond Index.

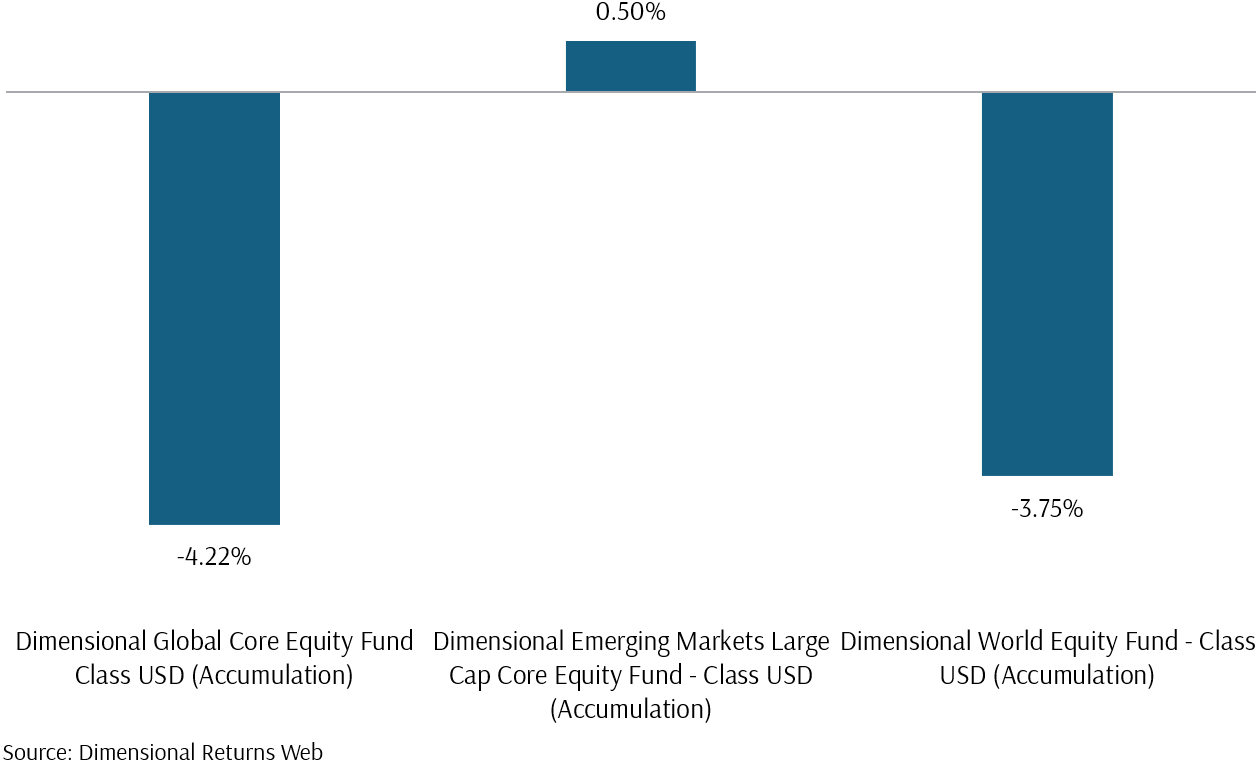

Dimensional Equity funds experienced even larger declines, primarily due to the underperformance of small-cap companies compared to large-cap counterparts, influenced by rising US yields. This susceptibility to increased borrowing expenses led to more pronounced share price declines for small-cap companies, resulting in negative returns for funds like the Dimensional Global Core Equity fund, the Dimensional Emerging Market Large Cap Core fund, and the Dimensional World Equity fund.

China’s stock market is influenced by various factors such as the economy, regulations, technology, and politics. However, encapsulating all these aspects within a single article is far too complex. Therefore, this article will focus on the most recent and significant event impacting China’s stock market: the real estate crisis.

Amid the challenges posed by the recent real estate crisis, it is essential to maintain long-term investment strategies in China. Short-term fluctuations in Chinese stocks should not overshadow the broader growth potential in the equity market. While banks and insurers face risks from bad loans and Local Government Financing Vehicles (LGFVs) debt, their impact remains manageable. The housing sector correction presents an opportunity to diversify China’s GDP growth away from real estate and into areas like green technology and innovation, enhancing long-term market resilience. Hence, despite the challenges posed by the real estate sectors, investing in China’s equity market offers potential benefits and growth opportunities over the long term.

April Performance

Equities and bonds fell sharply in April after reports of persistent inflation in the US reduced the probability of rate cuts by the Federal Reserve. The March US Consumer Price Index (CPI) showed goods and services rose 0.4% month-on-month (m-o-m) and year-over-year (y-o-y) at 3.5%, which is a 0.3% rise from February price levels. This is contrastingly higher than the expected inflation rate of 0.3% m-o-m and 3.4% y-o-y by economists from Dow Jones.

The higher-than-expected inflation rate raised the probability of interest rates staying higher for longer and lifted the US yields. The US 10-year yield, for example, rose 0.47% from 4.21% to 4.68%. This means higher borrowing costs for companies, which places pressure on companies’ earnings. Consequently, the S&P 500 Index fell by 4.08% and the Bloomberg Global Aggregate Bond Index fell by 1.61%.

In Europe, disappointing earnings drove down stock prices. Nestle fell 3.7% in April after missing first-quarter organic sales growth estimates, dragging the F&B sector down. The luxury sector also experienced a decline in April after Kering SA, the parent company of Gucci, reported a sharp drop in operating profits due to sluggish demand in China. This contributed to the STOXX Europe 600 Index falling about 1% in April.

In contrast, UK stocks were more optimistic. The FTSE 100 Index saw a rise of over 2%, primarily driven by the significant presence of energy and commodity firms. This increase coincided with crude oil prices hitting their highest point in over a year and commodity prices reaching record levels unseen in many years. UK energy giants Shell and BP saw remarkable gains of 9% and 5% respectively, while commodity giants Rio Tinto and Glencore experienced increases of over 7%.

Further East, Japanese equities gave up some of the gains that they had made over the first quarter. The Yen continued to depreciate in April as the rise in US yields made the US dollar more attractive, causing a selloff in the Yen. The depreciation raised concerns about higher inflation as Japan depends a lot on imports, which led to worries about weakening domestic demand. The Nikkei 225 Index fell 4.86% over the month.

Consequently, the MSCI World IMI Index, which tracks the developed markets, fell by 3.87%.

However, in the Emerging Markets, stocks are picking up momentum. The MSCI Emerging Markets IMI Index rose 0.67%, mainly buoyed by Chinese equities. The Hang Seng Index surged by over 7% in April following announcements by Chinese securities regulators regarding supportive measures aimed at facilitating listing procedures in Hong Kong. Additionally, China’s first-quarter GDP exceeded expectations, with the world’s second-largest economy expanding by 5.3% from the previous year. Official data revealed this growth rate comfortably surpassed analysts’ forecasts of 4.6% in a Reuters poll, marking an improvement from the 5.2% expansion seen in the previous quarter.

Exhibit 1 – Market Index Performance: April 2024 (USD)

How Did the Dimensional Funds Fare in April?

Moving on to the Dimensional Funds, the Dimensional Equity funds fell to a slightly larger extent compared to the indexes in April. This can be attributed to the underperformance of small-cap companies relative to large-cap counterparts, primarily influenced by the rising yields in the US.

Due to their greater susceptibility to increased borrowing expenses, which directly affects their future profitability, small-cap companies registered a more pronounced fall in their share prices.

As a result, the Dimensional Global Core Equity fund, the Dimensional Emerging Market Large Cap Core fund, and the Dimensional World Equity fund posted returns of -4.22%, 0.5%, and -3.75%, respectively.

Exhibit 2 – Dimensional Equity Funds Performance: April 2024 (USD)

Staying in Your Seats Through the Volatility

Market volatility is anticipated to persist as economic indicators illuminate inflationary trends across major developed markets. In response to these indicators, market participants will swiftly factor in the likelihood of central bank rate adjustments, influencing decisions to buy or sell in both stock and bond markets, creating a turbulent journey for long-term investors. Nevertheless, in the long term, economic fundamentals outweigh short-term fluctuations. Therefore, focusing on the long-term wealth plan and staying invested to achieve your wealth goals is the best course of action.

China’s Equity Landscape

As part of a series covering the equity landscape of major economies, this month we will be looking at China’s equity landscape.

The Importance of China’s Equity Landscape

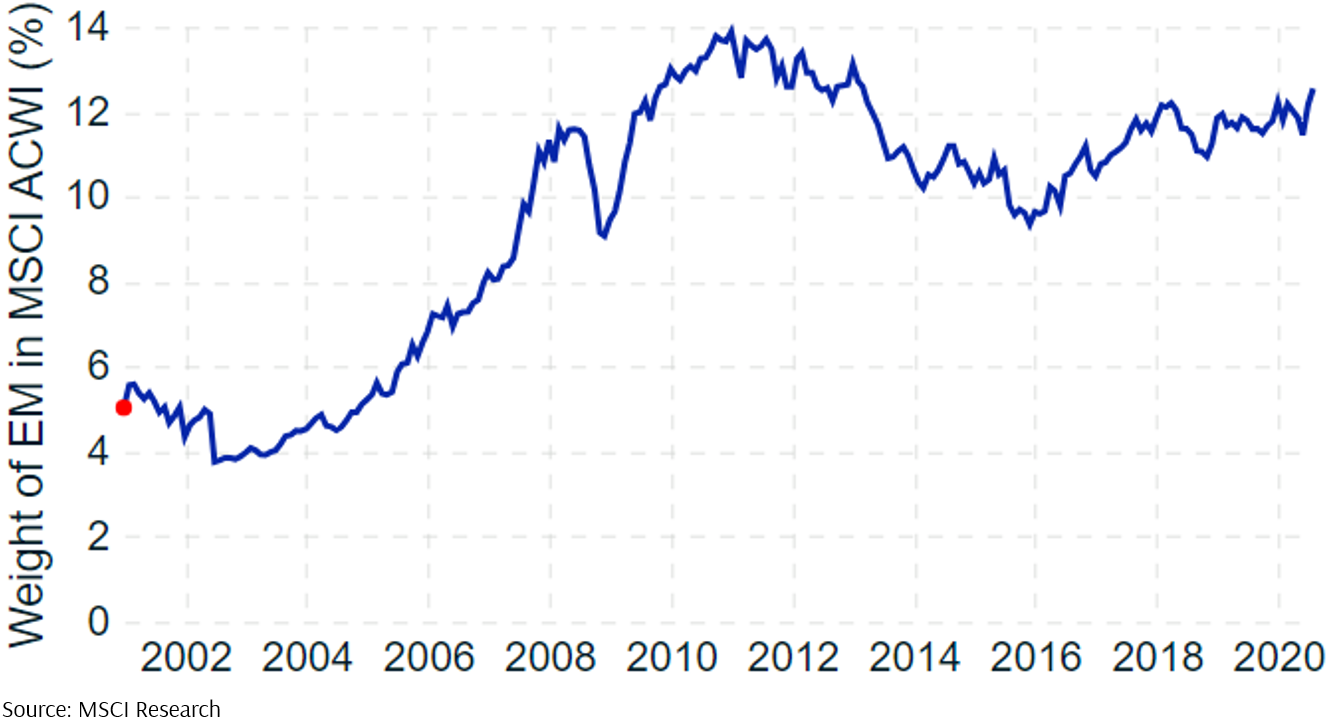

The MSCI All Country World Index (ACWI) captures large and mid-cap representation across 23 Developed Markets and 24 Emerging Markets countries. With 2,840 constituents, the index covers approximately 85% of the global investable equity opportunity set. From the start of 2001 to 2020, the Emerging Market weight in the MSCI ACWI has been growing from 5% to more than 12% as illustrated in Exhibit 3. During the same period, China’s weight has grown from the sixth largest country weight in the MSCI Emerging Market Index to the largest. Hence it is important, for investors who are invested in a globally diversified portfolio, to have a better understanding of China’s equity landscape.

Exhibit 3 – Weight of EM in MSCI ACWI (%)

China’s equity landscape is complex and dynamic, influenced by a variety of economic, regulatory, technological, and geopolitical factors. However, it is too complex to cover in just one article; therefore, this article will centre its attention on the latest event that has a direct impact on China’s equity landscape—the real estate crisis.

Since over 70% of Chinese firms within the MSCI ACWI are listed on the Hong Kong Stock Exchange, the Hang Seng China Enterprises Index, acting as a benchmark mirroring Mainland China’s securities performance in Hong Kong, will serve as a reference point in the subsequent discussion concerning China’s equity scene.

China’s Real Estate Crisis Impact on China’s Equity Stock Market

The downfall of Evergrande, once the global leader in real estate, sparked a crisis in China’s real estate sector. Before its downfall, the Chinese property market witnessed steep rises in housing prices and mounting debt among developers, prompting concerns of a potential housing bubble. According to data from the People’s Bank of China, nearly 90% of Chinese households possess homes, with a notable portion remaining unoccupied as per the China Household Finance Survey, indicating speculative rather than demand-based market dynamics.

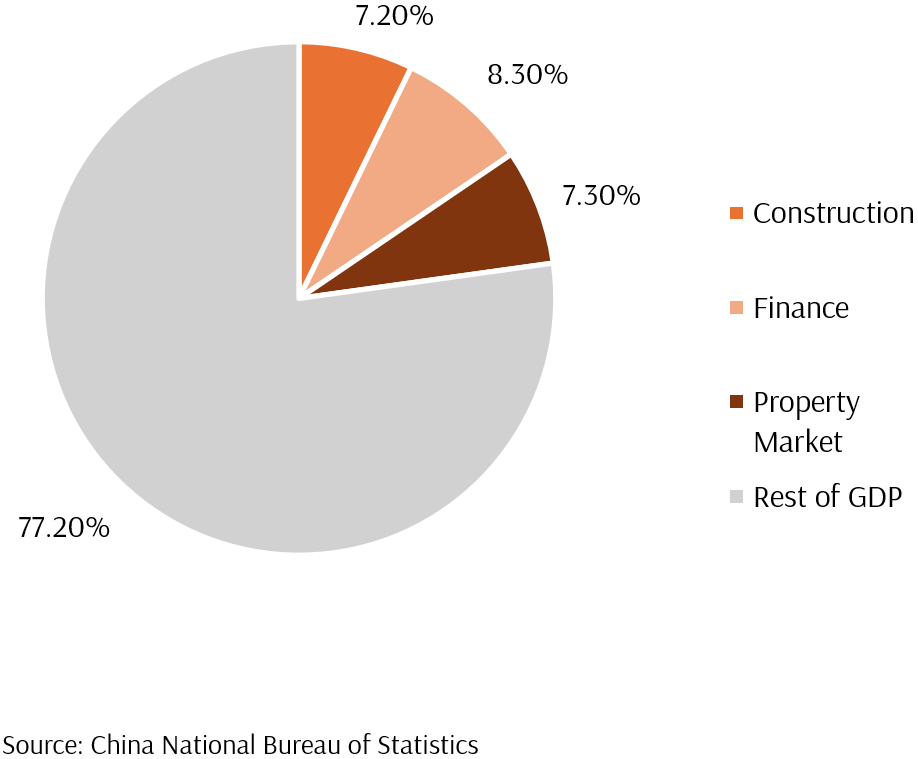

The real estate sector, along with its related industries such as finance and construction, represents more than 20% of China’s GDP as of 2020, as demonstrated in Exhibit 4 below. According to the China Household Wealth Survey, approximately 70% of family wealth is linked to property. A collapse in this sector could greatly jeopardise the stability of the financial system and have negative repercussions on the welfare of many Chinese individuals heavily invested in real estate.

In response, the Chinese government implemented the Three Red Lines Policy in August 2020, aiming to bolster the real estate sector’s financial robustness by curbing developers’ leverage, enhancing debt coverage, and boosting liquidity. Evergrande’s demise was expedited by its failure to adhere to policy restrictions, leading to a liquidity crunch and impeding its ability to repay bank loans and meet obligations to suppliers and contractors. Other prominent developers, such as Country Garden, encountered similar liquidity challenges, while Vanke experienced credit rating downgrades.

As a result, Evergrande was delisted from the Hang Seng China Enterprises Index in November 2021. During the period from the implementation of the Three Red Lines Policy until its removal from the index, the Hang Seng China Enterprises Index experienced a 40% decline, with a substantial portion attributable to the real estate crisis.

Exhibit 4 – Contribution of Property Market and Affiliate Industries to GDP in 2020

The Broad Impact of China’s Real Estate Crisis

The real estate crisis in China extends its impact beyond the real estate sector alone. As illustrated in Exhibit 4, financial sectors such as banks face exposure to the crisis due to their role as primary issuers of debt financing to real estate developers and buyers. Moreover, local governments in China are also grappling with the consequences of the crisis, as dwindling land sales translate to reduced income, exacerbating the debt burden of Local Government Financing Vehicles (LGFVs).

In the following section, “Assessing the Ripple Effect”, we delve into the cascading effects on China banks’ and LGFVs’ debt stemming from the real estate crisis and assess its potential ramifications on the China equity market going forward.

Furthermore, in the section “Potential Further Corrections in the Housing Market Landscape” we will explore a report by Kohlberg Kravis Roberts & Co. (KKR) that provides evidence suggesting that China’s real estate woes may not have concluded.

We will also examine how the decline in property prices resulting from the real estate crisis triggers a negative wealth effect, prompting reduced consumer activity, deflation, and sluggish economic growth in China.

Next, we explore macroeconomic indicators that show encouraging signs of increased Chinese consumption in recent months despite economic headwinds.

Lastly, we examine other sectors that could potentially bolster China’s GDP in the long term as the country moves away from over-dependence on real estate expansion.

Assessing the Ripple Effects

- Impact on China Banks

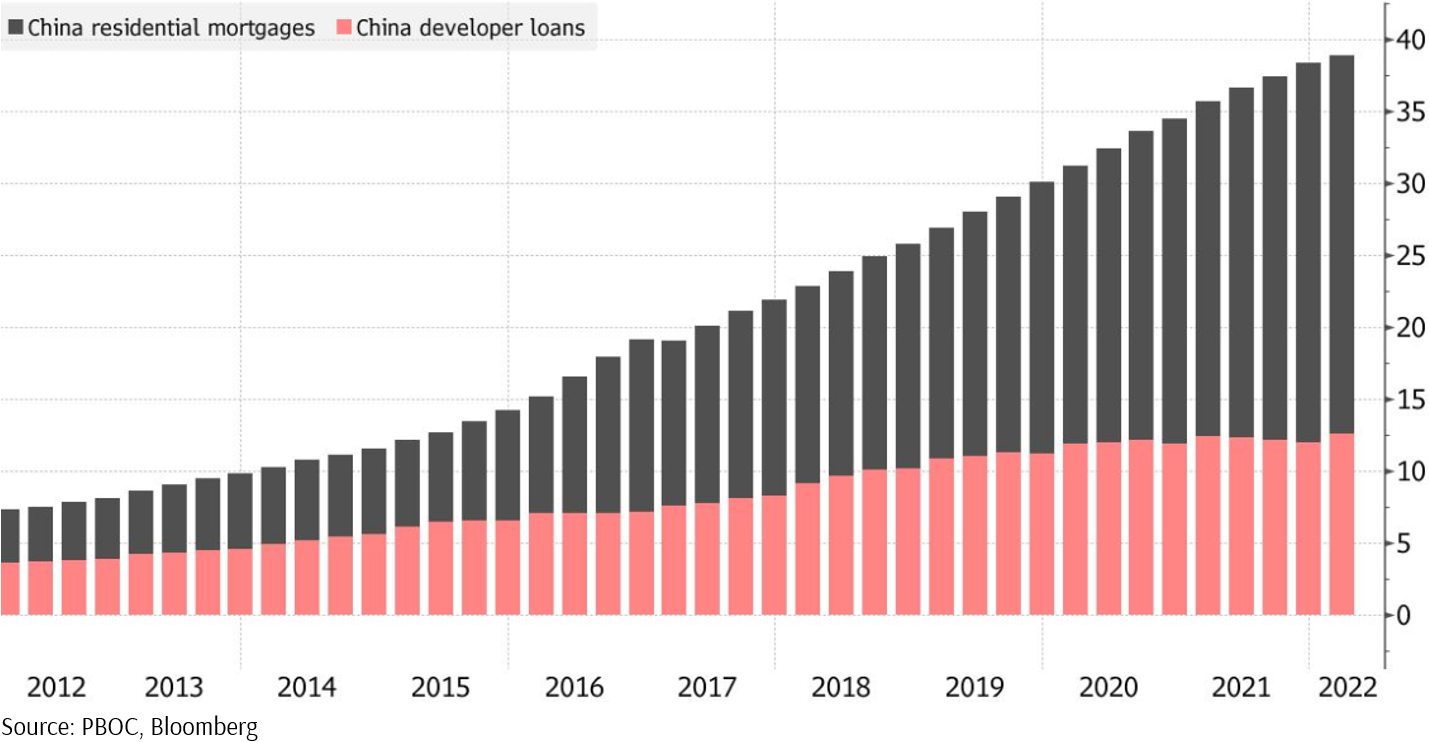

Over the years, bank loans to the property sector have increased, as shown in Exhibit 5 below. Hence, it is important to look at whether the real estate crisis has impacted the banking sector, especially since the top four banks in China have around a 20% weight in the Hang Seng China Enterprises Index.

From the implementation of the Three Red Lines Policy until the end of April 2024, the cumulative returns of the top four banks, namely the Industrial and Commercial Bank of China (ICBC), Bank of China (BOC), China Construction Bank (CCB), and Agricultural Bank of China (ABC), were -7.7%, 40.7%, -10.7% and 31.3%, respectively.

Exhibit 5 – China Property Loans 2011 – 2022 (In Trillions of Yuan)

In their 2023 annual reports, China’s top four banks, namely the Industrial and Commercial Bank of China (ICBC), Bank of China (BOC), China Construction Bank (CCB), and Agricultural Bank of China (ABC), collectively reported an increase in total bad loans, reaching 1.23 trillion yuan ($170 billion), up 10.4% from the previous year. Bad debts in the property sector surged, with bad loans to property developers rising to 183.9 billion yuan, and bad construction loans increasing by 38.38% to 33.5 billion yuan. Across the four state lenders, non-performing loans jumped more than 10% in 2023.

Despite this, the lenders assured that their bottom lines were not significantly affected due to ample provisions and reinforced risk controls. However, concerns over debt repayment have heightened, attributed to a slowing economy impacting job security and decreasing asset prices.

Despite declines in net interest margins, all banks reported increased net profits. Part of the reason is that the top four banks mentioned that they have set aside abundant provisions and have been ramping up risk controls in lending to property developers. Therefore, despite the challenges the banks faced due to the real estate crisis, it appears that the impact on them has not been significant so far.

Nevertheless, the lingering effects of the real estate crisis may continue to strain banks, as the complete ramifications of the crisis may not have been fully realised yet, which is a topic we will delve into in the subsequent section “Potential Further Corrections in the Housing Market Landscape”.

- The Impact on Local Government’s Debt on the Financial Sector

Local Government Financing Vehicles (LGFVs) were established to finance infrastructure projects. Due to their status as off-balance-sheet entities, the debt levels of LGFVs remain opaque. However, according to Pacific Investment Management Company (PIMCO), a global management firm known for its expertise in fixed income securities, they estimate that in 2023, LGFV’s debt amounts to approximately 55-60 trillion yuan. This is because many projects funded by LGFVs fail to generate adequate returns to cover debt obligations, often relying on refinancing or government support for survival.

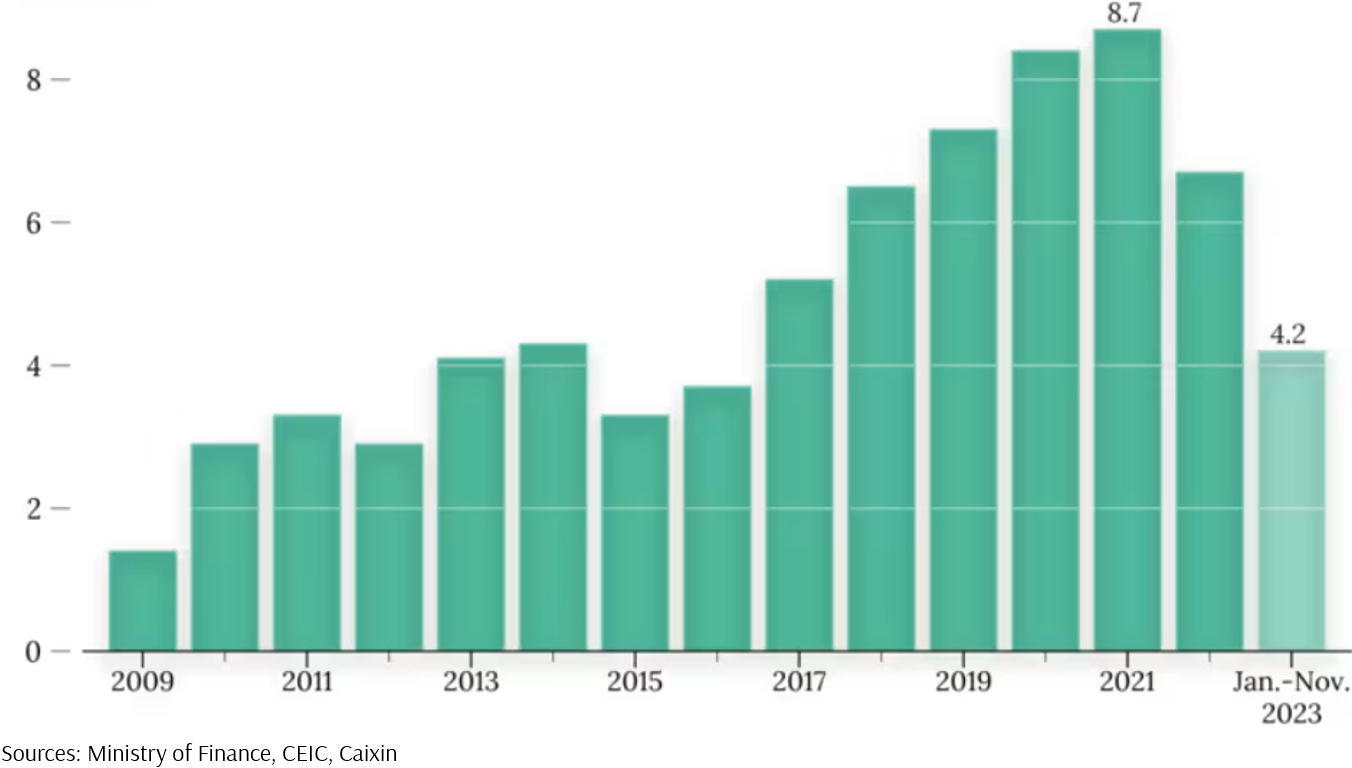

The real estate crisis exacerbated the strain on local governments, who are already burdened by escalating debts, as it reduced their revenue from land sales. Real estate developers, facing liquidity challenges due to the Three Red Lines Policy, reduced leverage and interest in acquiring new land, leading to a sharp decline in land sales demand. After peaking in 2021 at 8.7 trillion yuan, land sales plummeted by 23% to 6.7 trillion yuan in 2022. This was then followed by an 18% drop in the first 11 months of 2023 to around 4.2 trillion yuan, as depicted in Exhibit 6 below.

Insurance companies and banks are the primary holders of LGFV bonds, as they are significant lenders to these vehicles. Defaults in LGFVs could prompt holders to write down these assets, potentially affecting the share prices of these financial institutions.

While no LGFVs have defaulted thus far, the Chinese government has implemented measures to mitigate default risks. Since September 2023, the central government has restructured portions of LGFV debt with longer maturities and lower interest rates to ease repayment pressures on local authorities and LGFVs.

However, if LGFVs were to default, according to PIMCO’s stress test scenario, it could lead to volatility in China’s financial markets, widening credit spreads, and causing a flight-to-quality from corporate to government bonds.

Nonetheless, PIMCO believes that any impact would likely be short-term. In the worst-case scenario, a collapse of the LGFV bond market could reduce China’s GDP growth by approximately one percentage point over one year.

Exhibit 6 – Chinese Local Governments’ Land Sales (Trillion Yuan)

Potential Further Corrections in the Housing Market Landscape

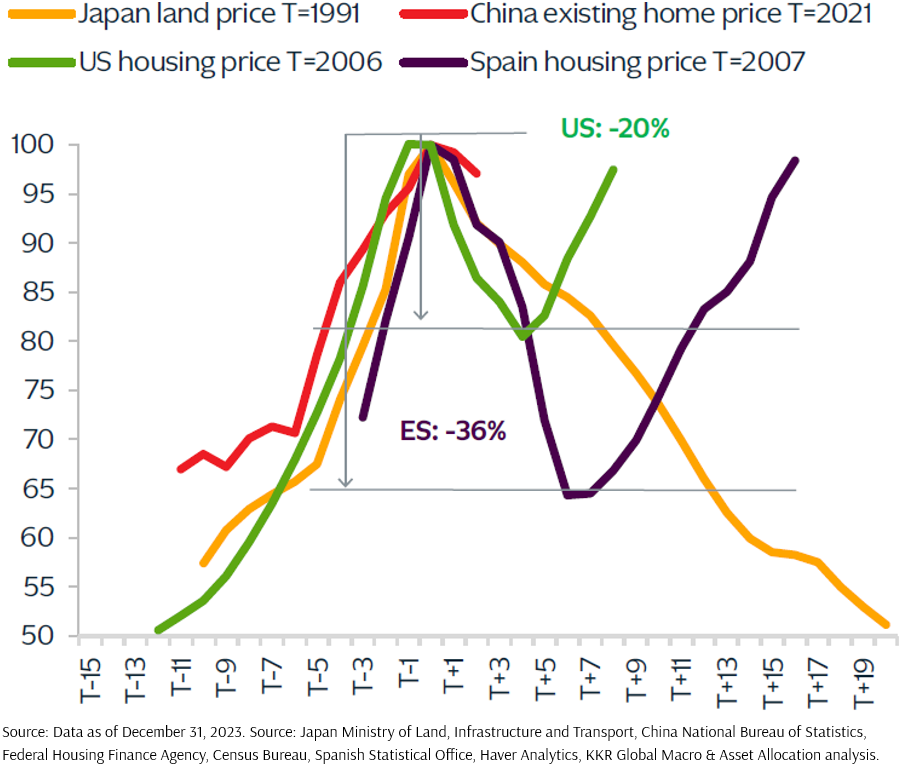

According to KKR, China’s housing market may only be halfway through its cycle. Drawing lessons from other countries’ experiences with housing-related bubble bursts, KKR highlights several key points:

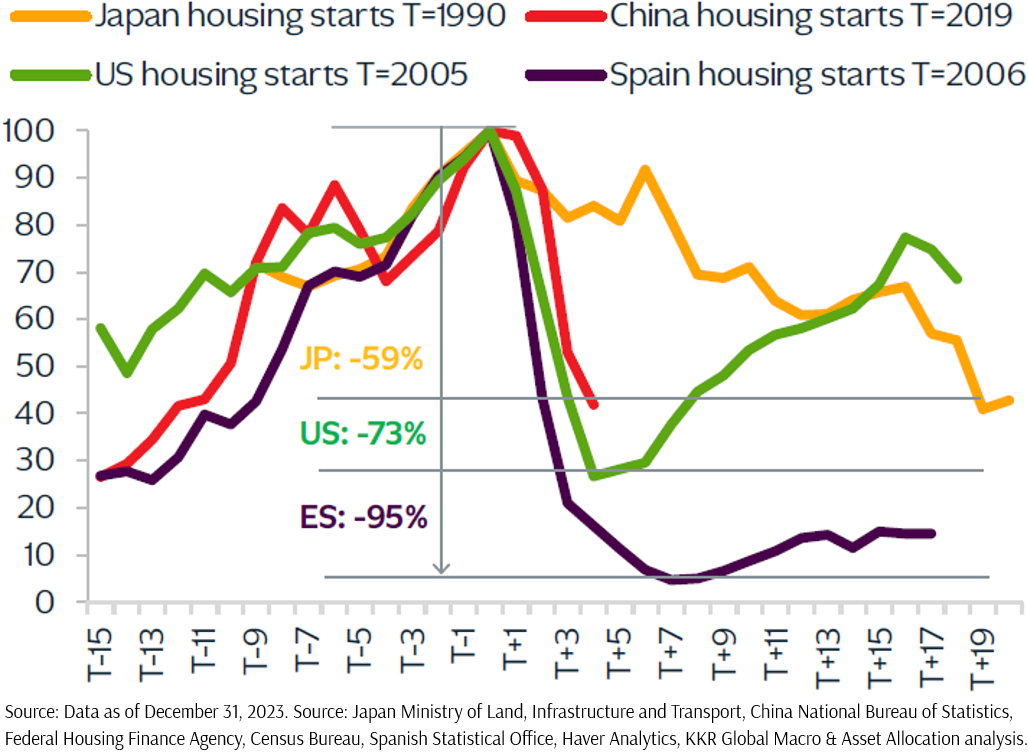

Housing starts: In China, a sharp decline in developers’ confidence has led to a nearly 60% drop in housing starts from their peak, comparable to past corrections in the US and Spain, as illustrated in Exhibit 7 below. “Housing starts” refer to the number of new residential construction projects that have begun during a specific period. A decline in “housing starts” suggests a slowdown in the housing market.

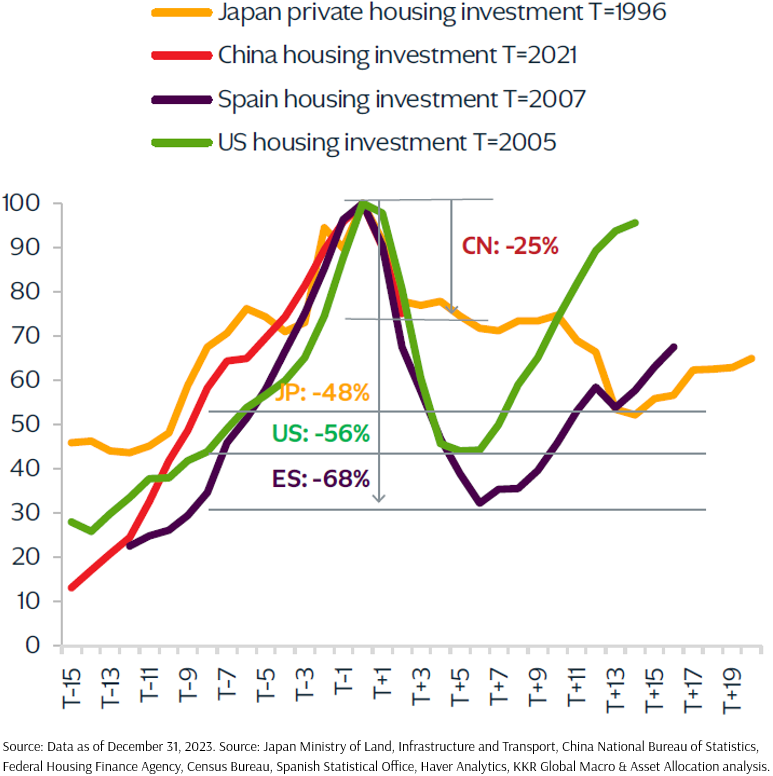

Housing investment: China’s housing investment has decreased by 25% from its peak, contrasting with steeper declines in the US and Spain. Japan’s decline occurred gradually over three decades as illustrated in Exhibit 8 below.

Housing prices: Despite reduced activity levels, China’s housing prices have seen minimal correction, likely due to statistical issues, regulatory constraints, and household reluctance to sell at lower prices. KKR anticipates further correction pressures as illustrated in Exhibit 9 below.

Housing inventory: By the end of 2023, China had amassed a substantial housing inventory, estimated at nearly 25 million units, surpassing annual household formation rates. KKR suggests that without additional government intervention to upgrade quality or write off assets, it will take significant time to absorb these inventories.

Exhibit 7 – Housing Starts

Exhibit 8 – Housing Investment

Exhibit 9 – Housing/Land Prices

KKR’s insights into China’s housing market have significant ramifications for both banks’ stock values, LGFVs’ debt and consumer confidence, exacerbated by a negative wealth effect that could worsen if housing prices continue to decline.

In terms of banks’ stock prices, a further deceleration in the housing sector could elevate default rates among property developers, resulting in a rise in nonperforming loans held by banks. This could undermine investor confidence, exerting downward pressure on banks’ stock prices.

Regarding LGFVs’ debt, the decrease in housing investment and the substantial surplus of housing inventory could perpetuate a dwindling interest in participations in land sales auctions. This reduced demand may negatively impact the revenue of local governments, potentially hindering their ability to meet debt obligations to LGFVs. This, in turn, might heighten the likelihood of default and compel financial institutions to devalue these assets, exerting downward pressure on the financial sector.

Finally, looking at China’s housing data presented by KKR in Exhibits 7,8 and 9, it appears that the full extent of the impact of the real estate crisis may not have materialised yet. For example, Exhibit 9 shows that China’s home prices have declined by less than 5% from their peak between 2021 and 2023, as depicted by the red line. In contrast, home prices in the US, Spain, and Japan fell by 20%, 36%, and 50% respectively over periods of five, seven, and 20 years. Moreover, Exhibits 7 and 8 continue to demonstrate a similar downward trend in housing starts and housing investments in China. Therefore, if we use these countries as benchmarks, China might experience a more prolonged and significant decline in home prices. If that is the case, Chinese consumers’ confidence may be further dampened by a negative wealth effect.

In the following section, we delve into the repercussions of the real estate crisis, which resulted in a negative wealth effect on Chinese consumers, contributing to a deflationary environment and sluggish economic growth in China.

The Negative Wealth Effect on the Equity Market

The negative wealth effect occurs when a decrease in household wealth leads to reduced consumer spending. With real estate often forming a significant portion of households’ wealth, declining property values can make homeowners feel less financially secure. This can prompt them to be more mindful of their expenditure, contributing to less consumer spending and potentially leading to a deflationary environment.

In such an environment, low consumer confidence discourages spending on goods and services, leading to lower sales for businesses, decreased production, and reduced investment. This economic slowdown can exacerbate deflationary pressures as businesses may lower prices to stimulate demand. Additionally, deflation can diminish household wealth, further dampening consumer confidence and spending, and perpetuating the deflationary cycle, placing pressure on companies’ earnings and growth.

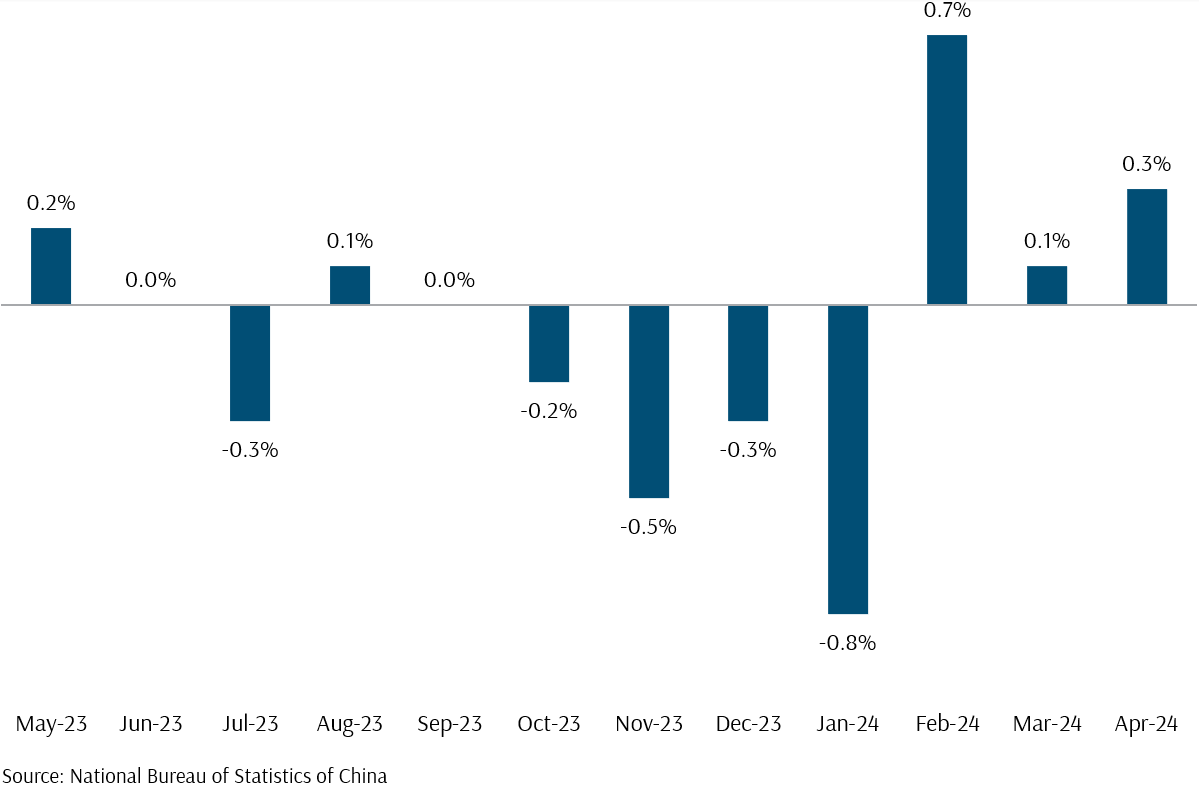

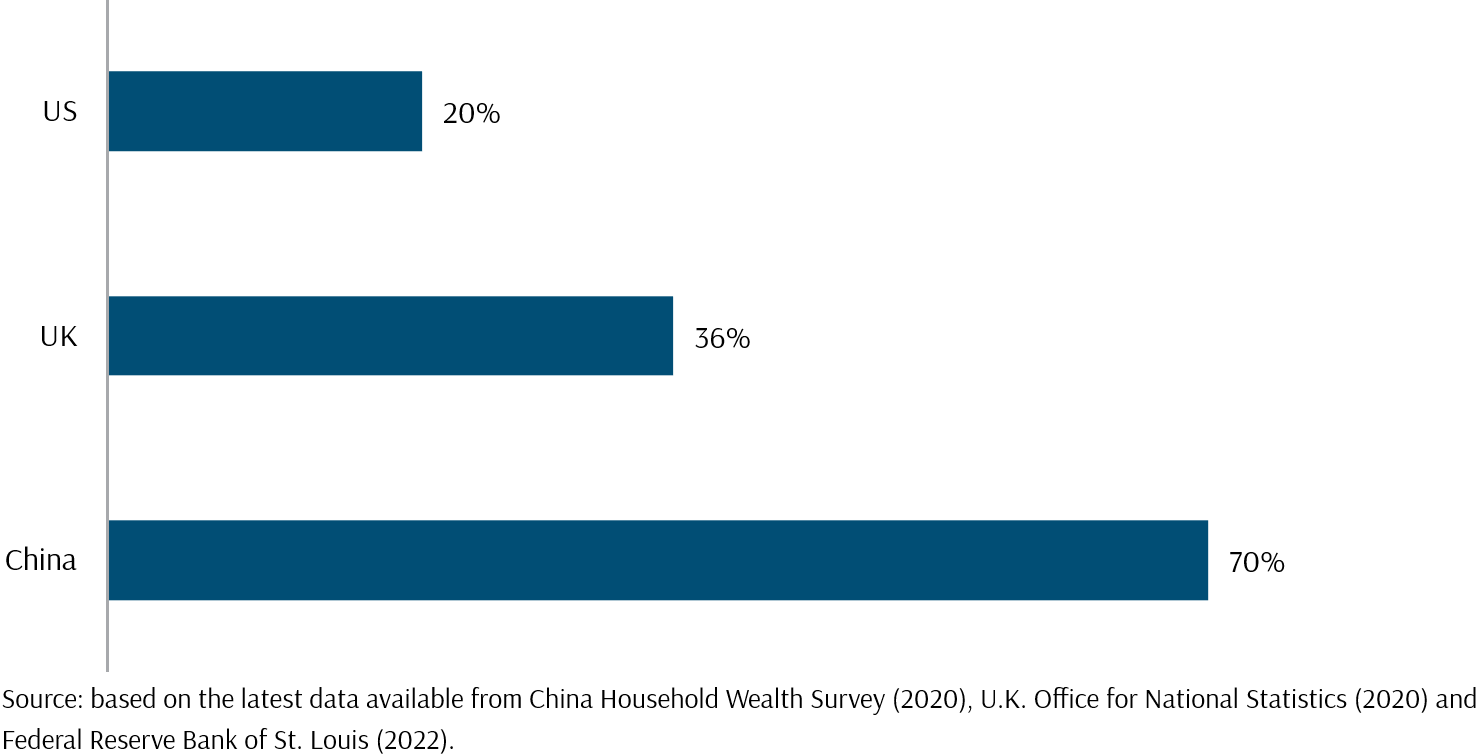

If we look at Exhibit 10 below, which depicts China’s inflation rate from May 2023 to Apr 2024, China has already witnessed deflation[1] in five out of the past 12 months since April 2024 and zero growth in price levels for two out of the past 12 months. Moreover, as depicted in Exhibit 11, China’s household wealth is more closely tied to real estate when compared to the UK and the US. This suggests that the negative wealth effect on consumer spending in China could be more significant and have a greater and more prolonged impact on its economy and the equity market landscape.

From June 2023, when China first entered a period of deflation, until January 2024, when deflation peaked at -0.8%, the Hang Seng China Enterprises Index experienced a decline of nearly 16%. This drop was largely influenced by a sell-off prompted by diminished investor confidence resulting from the deflationary conditions.

However, we also observe favourable inflationary trends post-January 2024 in Exhibit 10. In the following section, we examine various macroeconomic indicators alongside the recent performance of the Hang Seng China Enterprises Index.

Exhibit 10 – China Inflation Rate (%)

Exhibit 11 – Total Household Wealth Tied to Property

Positive Trends in Chinese Consumption Amid Economic Challenges

The initial months of 2024 present a picture of the Chinese economy navigating with significant positive momentum.

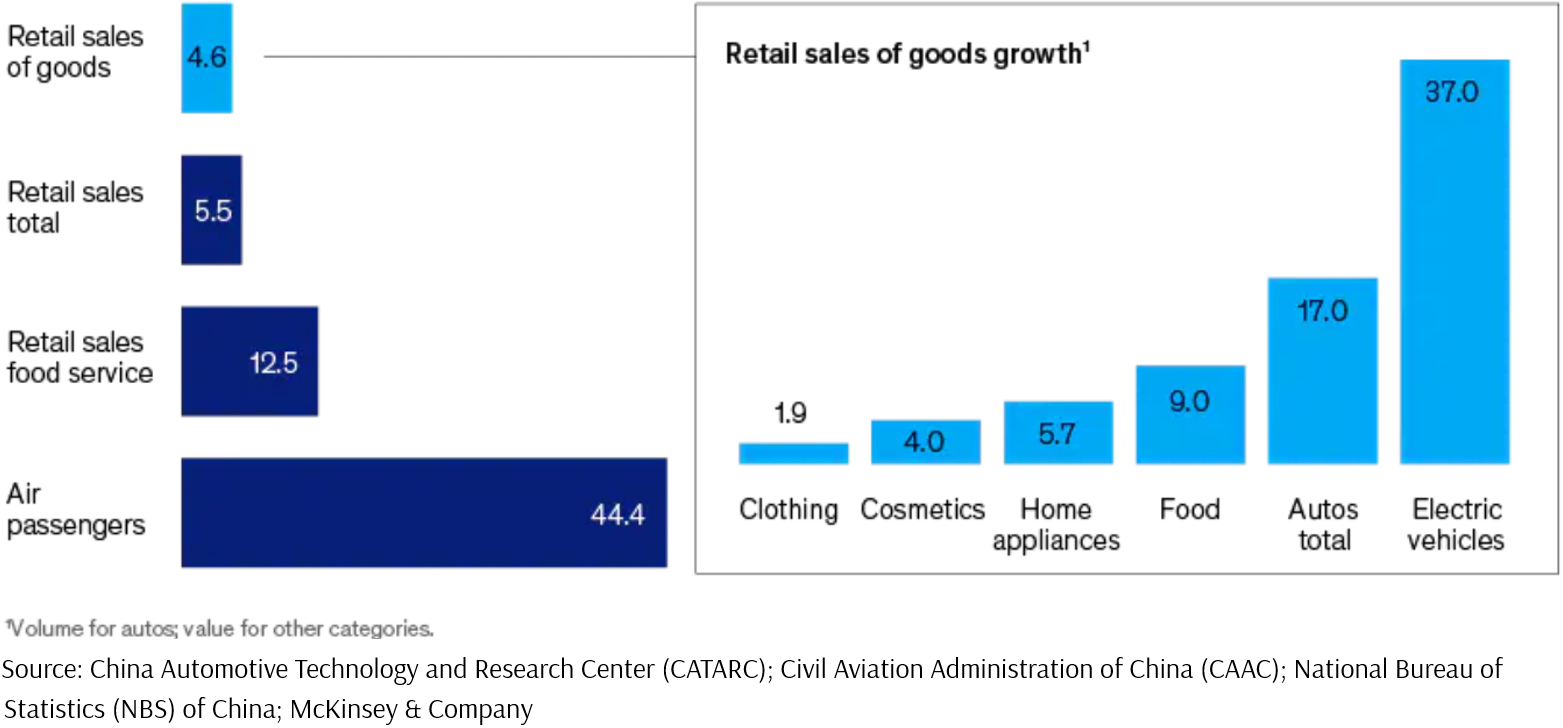

As illustrated in Exhibit 12 below, retail sales in the first two months of 2024 indicate a robust year-on-year increase of 5.5%, with goods contributing to a rise of 4.6%. Notably, food service sales surged by 12.5%, signalling a strong recovery in the hospitality sector. This was possibly fuelled by growing consumer confidence and the relaxation of pandemic restrictions.

Air passenger numbers witnessed an astonishing surge of 44.4%, reflecting renewed mobility and a resurgent appetite for travel and face-to-face business engagements. This suggests a rebound in air travel from the challenges of the pandemic era.

In the food sector, there was a notable 9% year-on-year growth. The moderate growth in cosmetics and clothing, at 4% and 1.9% respectively, may indicate a cautious approach by consumers towards discretionary spending in these segments. Home appliances experienced a moderate increase of 5.7%, potentially reflecting steady demand for home improvement.

The automotive sector emerges as another promising area of consumption growth. While overall auto sales grew by a healthy 17% in the first two months of the year, electric vehicles (EVs) surpassed this figure with an impressive surge of 37%, underscoring shifts in consumer preferences towards greener alternatives, supported by government incentives for EV adoption.

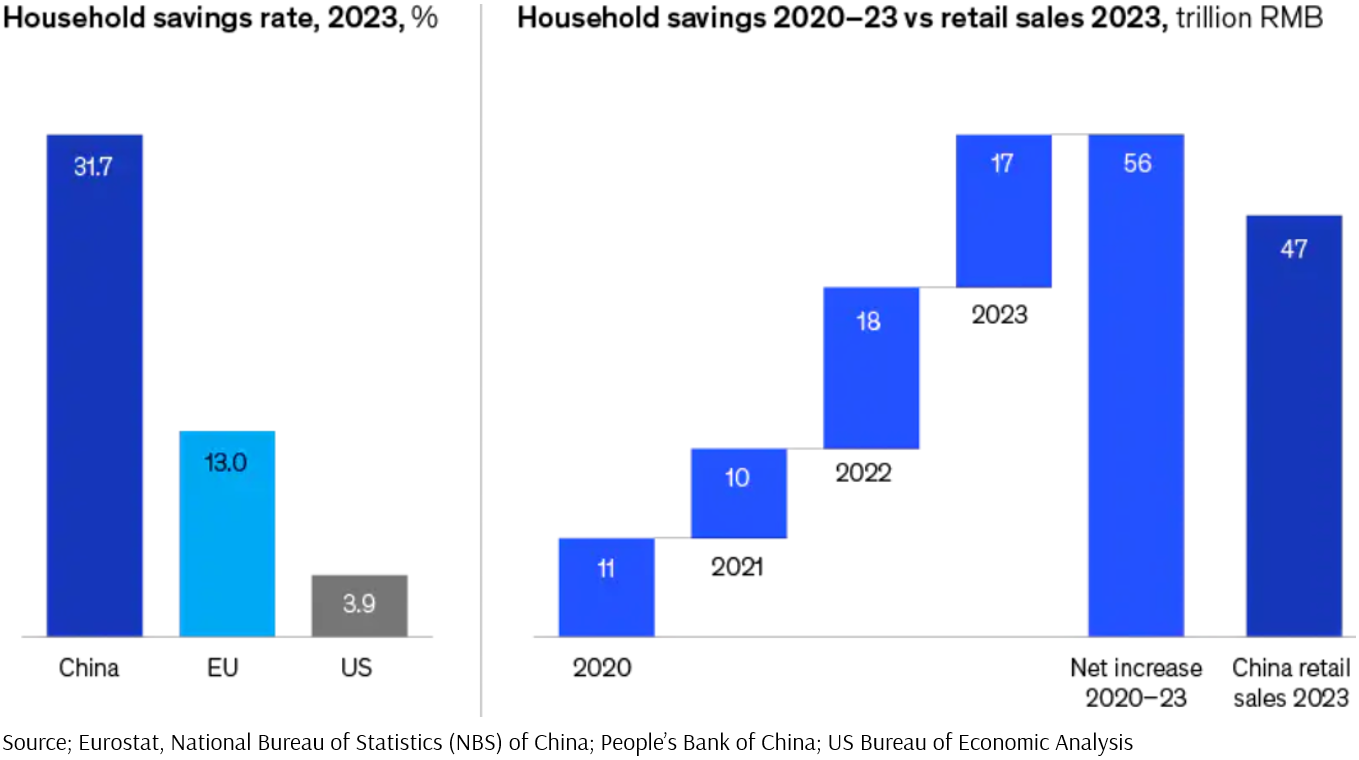

Complementing this economic activity, the savings rate in China reached 31.7% in 2023 from pre-COVID levels of around 29%, driving the nation’s total savings to record levels as illustrated in Exhibit 13 below. Chinese consumers accumulated 56 trillion Renminbi in new savings between 2020 and 2023, surpassing the 47 trillion Renminbi in retail sales for 2023. With such substantial savings amassed over recent years, consumer spending will likely rise significantly once confidence is fully restored, as excess savings come down back to the historical average.

Moreover, notwithstanding the geopolitical sanctions and tensions observed between China and the Western developed markets, particularly the US, China’s exports saw a 7% growth in the first two months of 2024 compared to the same period last year, with a notable 5% increase in exports to the US.

Exhibit 12 – China Retails Sales Growth From January to February 2024, % (Year Over Year vs 2023)

Exhibit 13 – China Household Savings Rate and Retail Sales From 2020-2023 (%)

While it is too early to accurately forecast how the remainder of the year will take shape, key consumption indicators are heading in the right direction.

Coupled with supportive measures towards the stock market from the China Securities Regulatory Commission (CSRC), China’s market watchdog, the encouraging macroeconomic indicators in China have helped to boost China’s stock market.

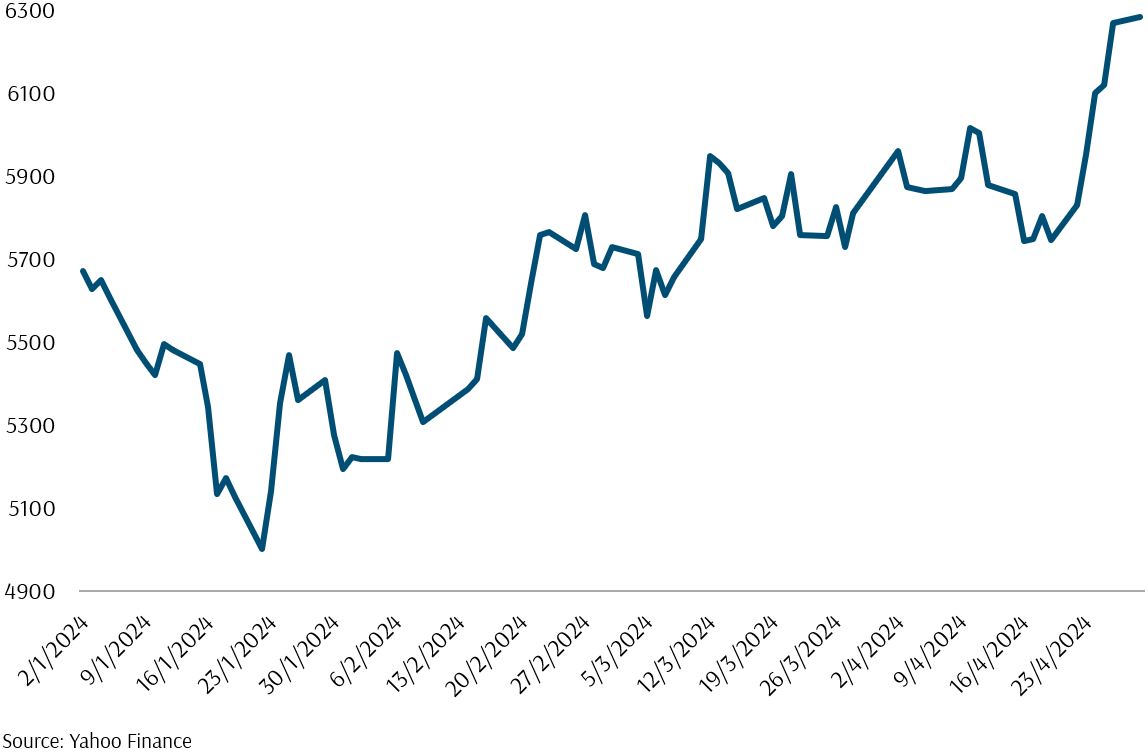

The Hang Seng China Enterprises Index from year-to-date until 30 April 2024, as depicted in Exhibit 14 below, reveals that since hitting a bottom on 22 January, the index has been on an upward trajectory, albeit with fluctuations, securing an 8.8% return.

In the final section on China’s equity landscape, we explore factors beyond the real estate sector and identify the potential major drivers of China’s economy.

Exhibit 14 – Hang Seng China Enterprises Index From YTD as of 30 April 2024

China’s Transition Towards Greener Pastures

China’s leadership is redirecting investments towards the clean energy sector, recognising that property-related activities, which previously fuelled a significant portion of the economy’s growth, began to impede expansion in 2022. Spearheading this transition are the “new three” growth engines (新三样 – xīn sān yàng): electric vehicles, batteries, and renewable energy.

This strategic shift has allowed China to avoid the recessions experienced by Japan in the 1990s and the US in 2008 following housing market collapses. In contrast to falling into recession, China, as the world’s second-largest economy, achieved a growth rate of approximately 5% in 2023.

A report by the Finland-registered Centre for Research on Energy and Clean Air (CREA) highlights that China’s clean energy sector contributed the most to the country’s economic growth in 2023, constituting 40% of its economic expansion.

Clean energy, spanning renewable energy sources, nuclear power, electricity grids, energy storage, electric vehicles (EVs), and railways, accounted for 9.0% of China’s GDP in 2023, up from 7.2% the previous year. This growth was mainly driven by advancements in the solar, EV, and energy storage sectors.

Furthermore, sectors such as information transmission, software, and information technology (IT) services saw robust growth, expanding by 11.9% year-on-year. As the real estate sector experiences stagnant or negative growth, other sectors with consistent growth trajectories will increasingly contribute to China’s overall GDP, reducing its dependence on real estate.

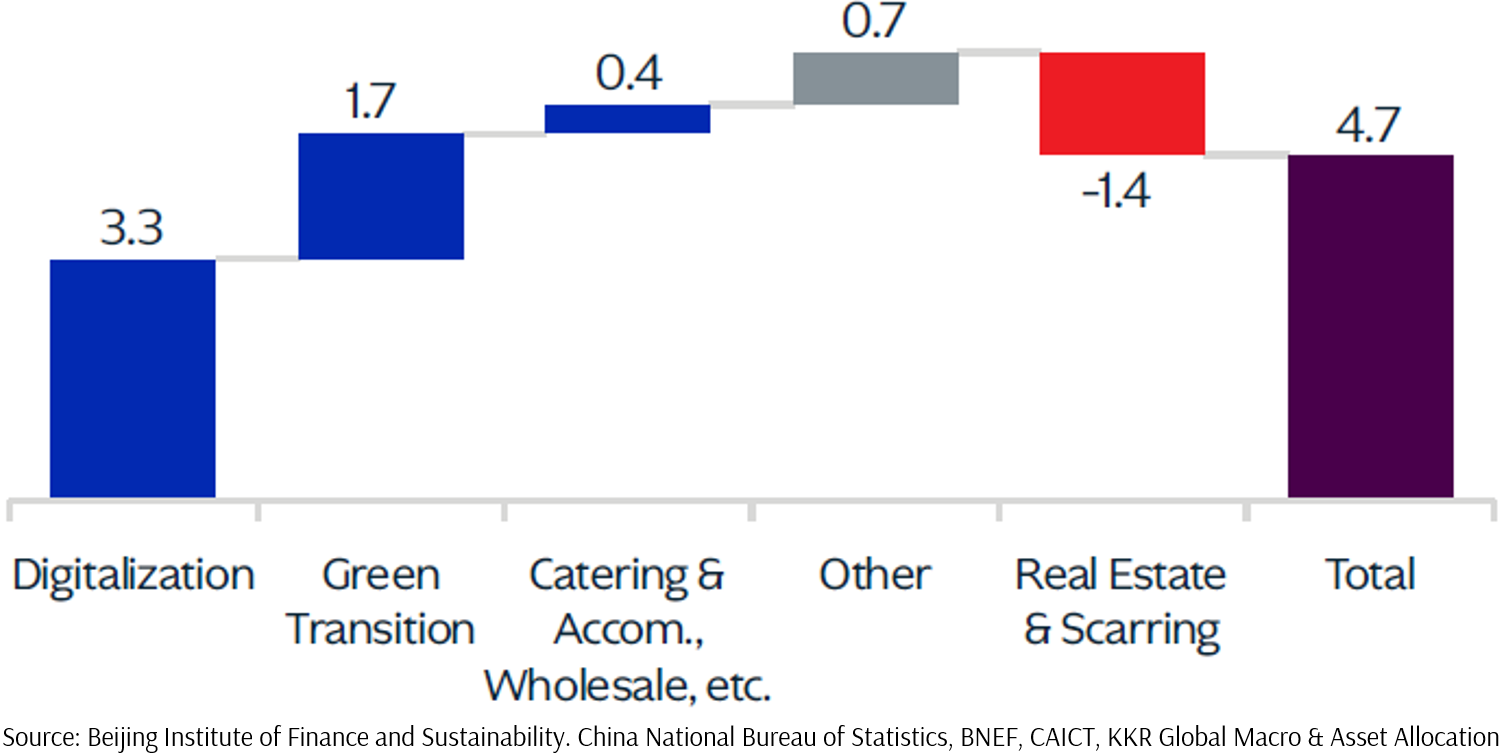

A recent report by KKR (Exhibit 15) suggests that despite challenges in the real estate sector and the scarring effects[2] of the COVID pandemic, growth in Digitalisation and the Green Transition are expected to offset these negatives, resulting in an estimated overall growth of 4.7% in 2024.

Prioritising sectors like technology, innovation, and sustainability can drive sustained economic growth by fostering innovation, research, and development. This strategic emphasis has the potential to enhance the competitiveness of China’s companies, attract foreign investments, and fortify China’s equity market in the long term.

Exhibit 15 – China’s 2024 GDP Breakdown (Estimates)

In Conclusion – Investing for the Long Term in China, the World’s Second-Largest Economy

Amid the recent challenges posed by the real estate crisis in China, it is crucial to uphold long-term investment strategies in the world’s second-largest economy. While the Hang Seng China Enterprises Index experienced notable fluctuations during the crisis, concentrating solely on short-term market movements may obscure the broader potential for growth and resilience within China’s equity market. Although banks and insurers are confronting risks stemming from the increase in bad loans and LGFV debt levels, their effects have not been significant thus far.

Moreover, the ongoing correction in the housing sector presents an opportunity to diminish China’s over-reliance on real estate for GDP growth, thereby promoting diversification into sectors such as green technology and innovation. These sectors provide avenues for sustained economic growth, innovation, and competitiveness, attracting both domestic and foreign investments and strengthening China’s equity market in the long term. Thus, despite existing challenges, maintaining investment positions in China’s equity market holds potential benefits and growth opportunities over the long haul.

In April, we witnessed favourable returns in Emerging Market stocks, primarily driven by China, which provided some degree of cushioning against the 4% decline in equities. However, it is essential to acknowledge that this is not an isolated incident. While it is true that developed markets have generally outperformed emerging markets over the past decade, this trend was not observed during the period from 2001 to 2010.

During this time, the MSCI All Country World Index, covering both developed and emerging markets, achieved an annualised return of 3.2%, with a substantial contribution from China, surpassing the 2.3% return of the MSCI World Index, which solely includes developed markets. Notably, the average inflation rate in the developed markets stood at 2.5% to 3% over the same period, resulting in a negative real return. Investing solely in developed markets would have led to the depreciation of an investor’s wealth. This underscores the significance of diversification in investment strategies to mitigate risks and optimise long-term returns.

Looking ahead, we will continue to explore the equity landscape of major economies as part of a series in our monthly market review. We trust you found this month’s market review insightful. Should you have any concerns, please do not hesitate to reach out to your Client Advisor. Thank you.

– Footnotes –

[1] This does not imply that the present deflationary condition is exclusively linked to the negative wealth effect triggered by the property price decline. Other factors, such as the decline in consumer confidence, are also at play, which arises from the persistent income uncertainties stemming from the strict and prolonged lockdowns implemented under Beijing’s zero-COVID policies.

[2] Note that “Scarring” refers to the scarring effect caused by COVID-19 which includes postponement of consumer upgrades and large expenditures, as well as an uptick in the youth unemployment rate, consumer confidence fell sharply over the past three years.

To learn more about our purpose-driven approach towards investment management, please visit this link.

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current estate plan, investment portfolio, financial and/or retirement plan, make an appointment with us today.