Paul Merriman, the financial educator and adviser, believes that you can invest just $3,000 on behalf of your child, and turn it into $50m. If he’s right, this could be the most important article you ever read. If you have children – implement these steps. If you don’t have children, you might want to implement these steps on behalf of your nieces, nephews and god-children.

So, let’s see how you turn $3k into $50m! For ease, let’s assume your bundle of joy is called Jimmy.

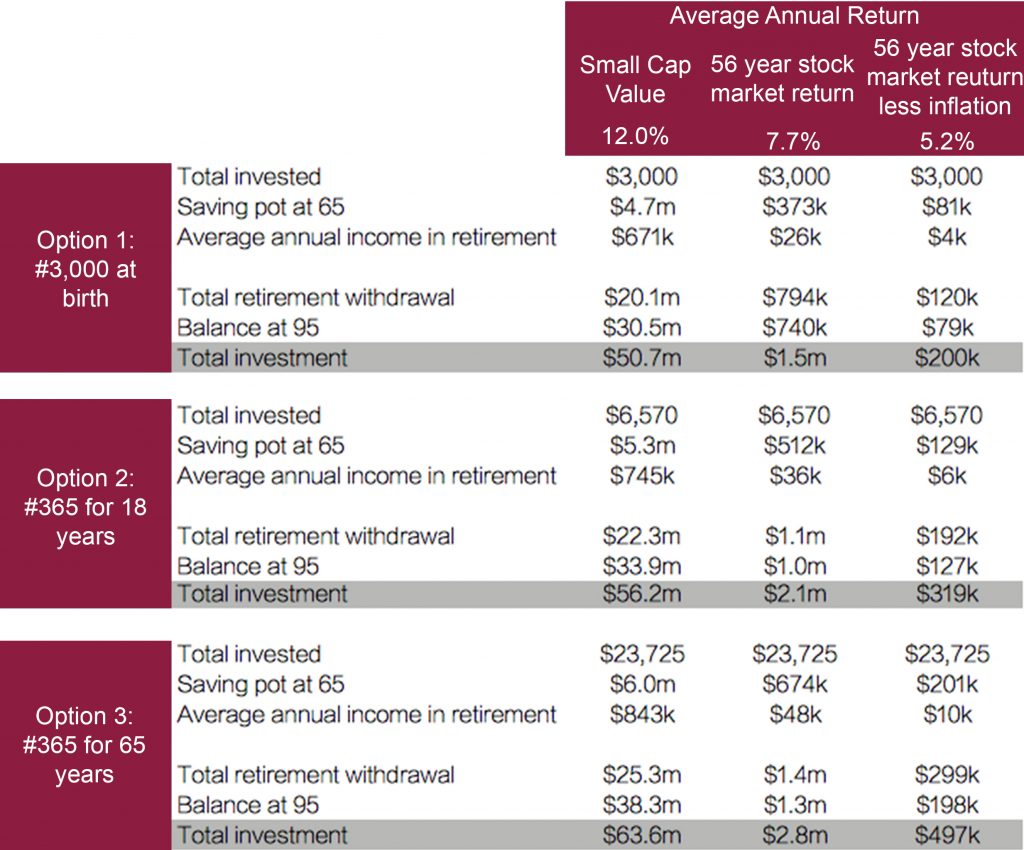

Option 1: $3k Lump Sum

First, you invest $3k at the birth of the child. You will put this in a tax-efficient wrapper in your country. For the UK, you could put it into a Junior stocks and shares ISA (2016/2017 limit is £4,080).

Next, you invest it in something that will return 12% – I’ll discuss if this is possible.

By the time Jimmy is 65, your $3k investment has grown to $4.7m!

It gets better. Your child now withdraws 5% of the pot each year for the next 30 years – which is an average of $671k a year! Sadly Jimmy dies at 95, but he had an amazing retirement. Your little Jimmy spent $20m in retirement, and still leaves a pot of $30m for the next generation (hence the $50m).

Option 2: $1 Per Day For 18 Years

An alternative is to put $1 aside every day for your child’s first 18 years. So the same process applies – put $365 a year in a tax-efficient wrapper, invest at 12%, and leave until 65.

Jimmy would have $5.3m at 65, can withdraw an average of $745k per year, and still leave $34m behind at 95!

Option 3: $1 Per Day For 65 Years

An even better option is that you pay $365 per year for the first 18 years, and then you somehow convince your child to continue putting in $365 every year until they are 65. It’s a financial education lesson they will be forever grateful for.

Jimmy would have $6m at 65, can withdraw an average of $843k per year during his retirement years, and still leave $38m behind at 95!

Is 12% Annual Return Possible?

The first hurdle is to find a long-term 12% return. Paul’s advice is to invest in small companies, and find ones that are value orientated – often referred to as ‘small-cap value’. In the US, this class of companies have returned 12% over a very long period, so it is not too much of a leap to assume the same for the future (listen to Paul’s podcast).

One stumbling block is that the US is more advanced than the rest of the world in terms of creating low-cost tracker funds that segregate the market to identify ‘small-cap value’. Therefore, those in the UK need to turn to actively managed funds. Normally, I prefer passive investments, but I’ve found one that is low-cost and fits Paul’s mandate.

It’s called Aberforth Smaller Companies Trust Plc (ASL) and its annual return over 26 years has been 13%, (annual fee is 0.79%).

What If I Get A Lower Return? Is It Still Worth Doing?

A more conservative route would be to buy a straight forward low-cost tracker fund.

The 2016 Equity Gilt study from Barclays indicates that the long term average stock market return (since 1961) has been 7.7%, and the real return after taking account of inflation of 2.5% is 5.2%.

You could buy the Vanguard FTSE UK All Share Index Trust to capture this return.

Here’s how the numbers change:

- Option 1: $3k Lump Sum: has turned into $1.5m at 7.7%

- Option 2: $1 Per Day For 18 Years ($6,570):has turned into $2.1m at 7.7%

- Option 3: $1 Per Day For 65 Years ($23,725): turns into $2.8m

If you take inflation into account, the equivalent amounts today would be $200k, $319k and $497 respectively.

Below is a summary of all the numbers:

Summary

So can you turn $3k into $50m? It is possible, and even with a more conservative approach of 7.7% return, you could still end up providing your child $1.5m-$2.8m. Even after inflation, that’s still $200k-$497k which is pretty amazing!

And the reason it works is through the power of compounding – investing small amounts over a long period of time.

Will your child live to 95? Will the stock market return 8% or 12%? No-one can tell you that, but you can focus on what you can control. The message here is clear – the earlier you start saving for your children, the more your money will earn.

Work through your budget and see how much you can spare to put away monthly or annually and start doing it today!

This is an original article written by Max Keeling, Head of Expat Division at Providend, Singapore’s Fee-only Wealth Advisory Firm.

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current investment portfolio, financial and/or retirement plan, make an appointment with us today.