Executive Summary

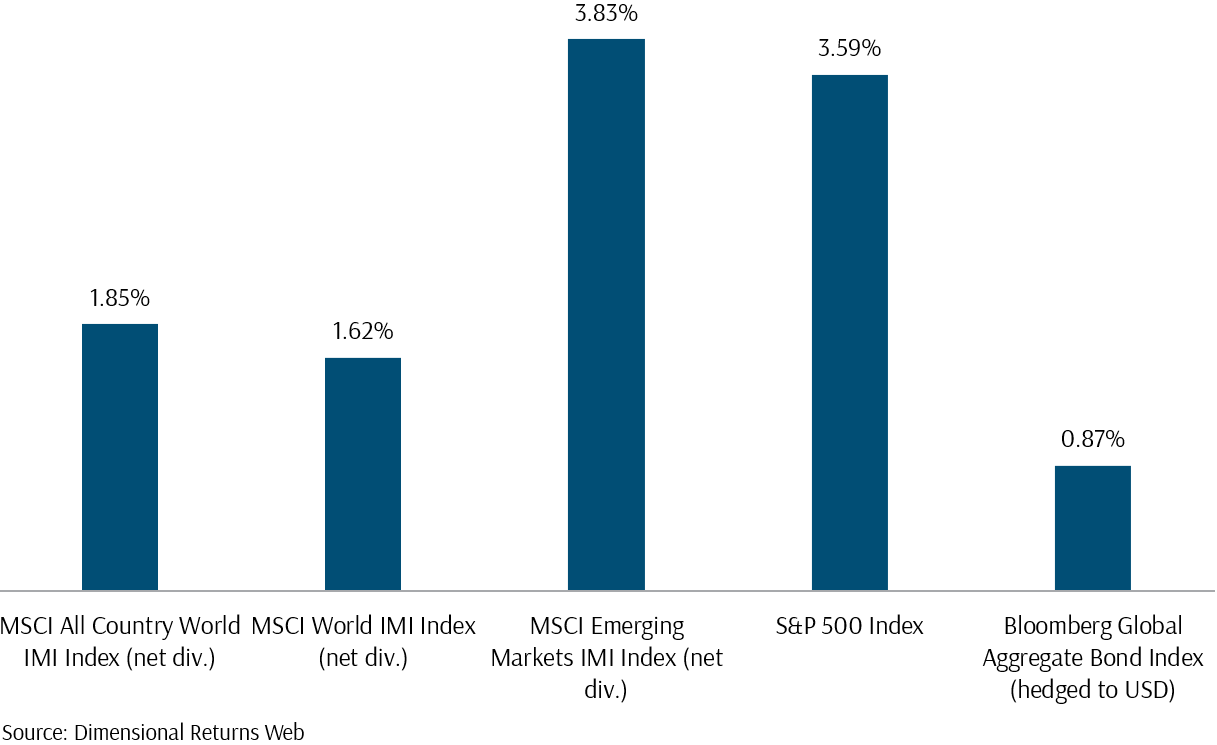

In June, the global equity markets experienced a significant rally, largely driven by large-cap growth stocks in the technology sector. The MSCI All Country World IMI Index rose by 1.85%, with major contributions from semiconductor companies. In the US, tech giants like Nvidia and Broadcom saw substantial gains, increasing by 12.7% and 21.2%, respectively, contributing to the S&P 500’s rise of 3.6%. Emerging markets also saw noteworthy performance, with Asia’s leading semiconductor manufacturers and India’s stock market driving the MSCI Emerging Markets IMI Index up by 3.8%.

Despite these gains, Dimensional equity funds faced challenges due to the underperformance of small-cap stocks in the US and Europe. The Russell 2000 Index fell by 1%, while the Russell 1000 Index rose by 3.31%. European small caps were particularly affected by political uncertainties.

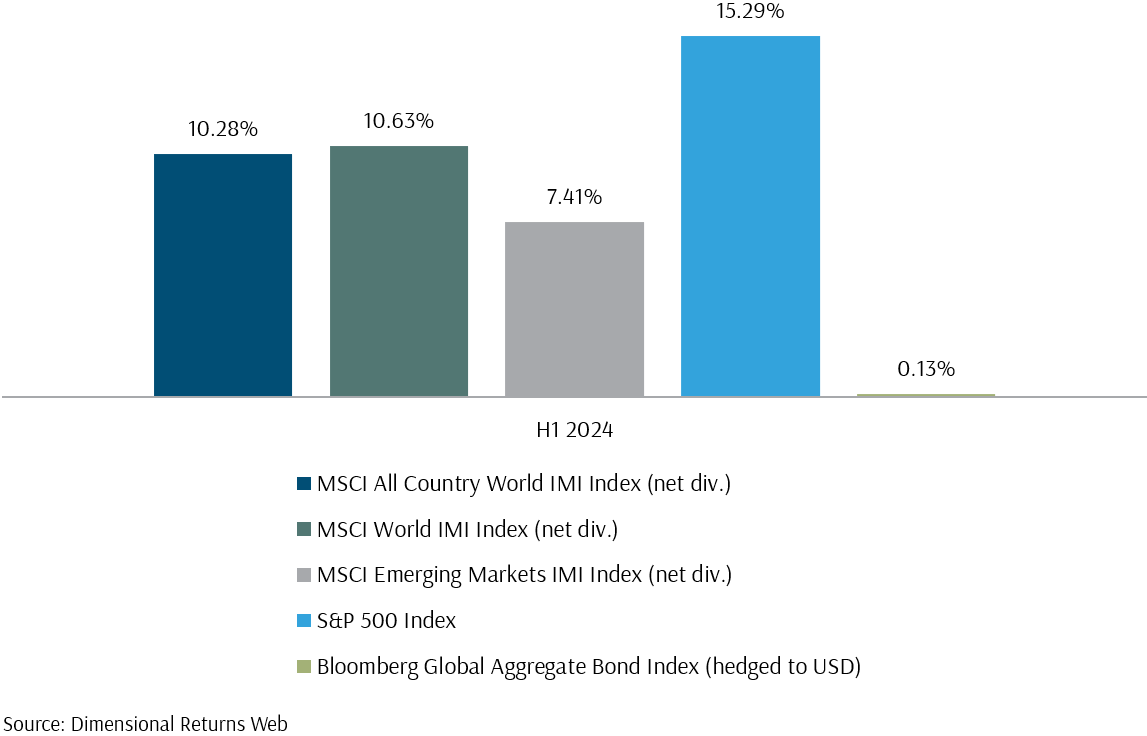

Looking at the first half of 2024, the semiconductor industry’s boom, driven by optimism around artificial intelligence, was a significant highlight. Nvidia surged by 150% and Broadcom by 45%. Major market indexes also showed strong performance, with the MSCI All Country World IMI up by 10.28%, MSCI World IMI by 10.63%, MSCI Emerging Markets IMI by 7.41%, and S&P 500 by 15.29%. The bond market saw minimal changes, with the US 10-year yield rising slightly. This increase negatively impacted bond prices, but the effect was offset by income from coupons. The Global Aggregate Bond Index returned 0.13% in the first half of 2024.

Looking ahead, valuation concerns arise as large-cap tech stocks hold high P/E ratios, suggesting that value and small-cap stocks may offer compelling opportunities.

As part of our special series on major economies’ equity landscapes, this month we will focus on Europe’s equity market.

June Performance

Overall, equities performed well in June, driven by the large-cap tech sector, particularly semiconductor companies, with the MSCI All Country World IMI Index rising by 1.85%.

In the US, semiconductor giant Nvidia continued its upward momentum, surging by 12.7%, while Broadcom Inc. climbed 21.2%. Additionally, a drop in US price levels, as measured by the Consumer Price Index, which fell from 3.4% in April to 3.3% in May, caused the US 10-year yield to decline in June.

This decline provided relief to global equities, which have benefited from the falling US 10-year yield as it has lowered borrowing costs from April’s peak.

Consequently, the MSCI World IMI Index rose by 1.62%, the S&P 500 by 3.6%, and the Bloomberg Global Aggregate Index by 0.87%.

In the emerging markets, Asia’s largest semiconductor manufacturers—TSMC, Samsung Electronics, and SK Hynix—saw gains of 18.1%, 10.9%, and 25% respectively.

India’s stock market also performed exceptionally well post-election, with the Nifty 50 climbing over 7%. Consequently, the MSCI Emerging Markets IMI Index performed exceptionally, rising by 3.8%.

Exhibit 1 – Market Index Performance: June 2024 (USD)

Small Cap Performance: A Drag on Dimensional’s Equity Performance

Dimensional equity funds underperformed indexes in June due to weakness in small-cap stocks in the US and Europe.

In the US, the Russell 2000 Index, which tracks the smallest 2000 companies, fell by 1%, while the Russell 1000 Index, which tracks the largest 1000 companies, rose by 3.31%. Prolonged elevated interest rates have weighed on US small-cap companies, which typically have higher debt compared to large-cap companies.

In Europe, political uncertainty in the UK and EU increased market risks, with more voters seeking change from incumbent parties. The CAC 40 Index, which tracks the largest French stocks, dropped over 5% after President Macron’s party faced setbacks in legislative elections. Small-cap companies, heavily reliant on Macron’s pro-business policies, were particularly affected. The STOXX Europe Small 200 Index, tracking the smallest European companies, fell by 4.91%, while the STOXX Europe 50, tracking the largest companies, fell by only 1.12%.

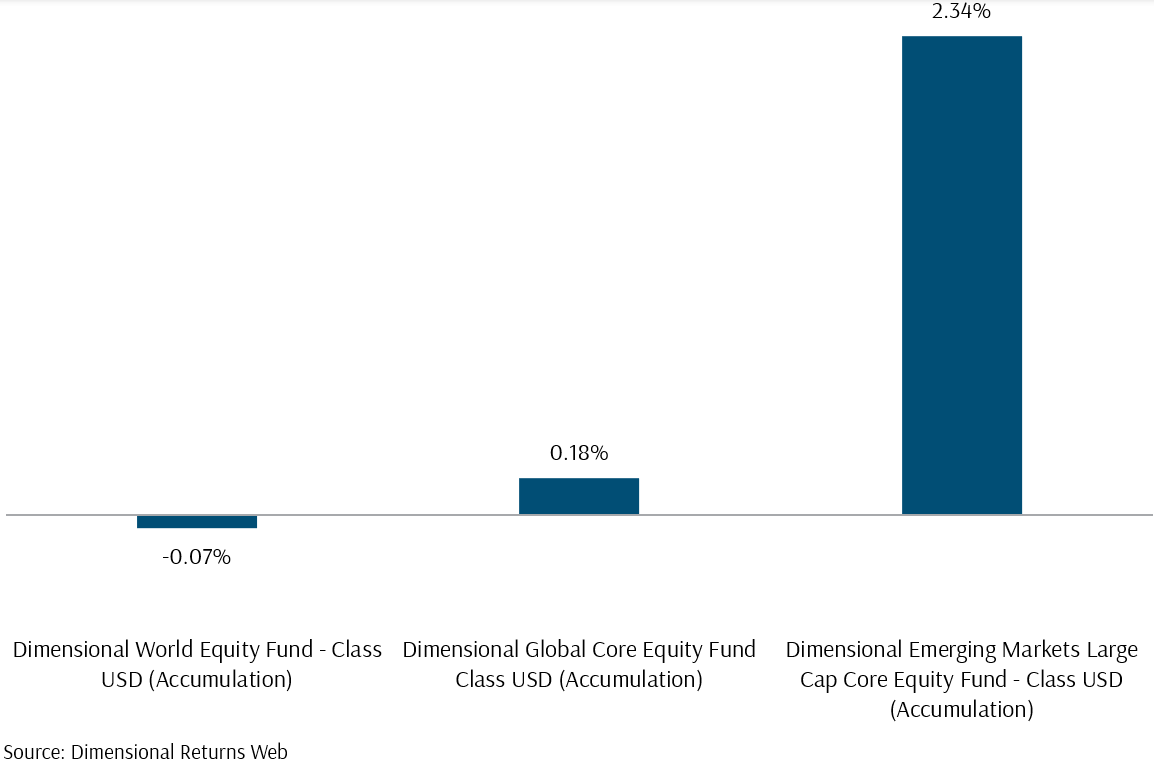

Due to the underperformance of small caps in the US and Europe, the Dimensional World Equity and the Dimensional Global Core Equity funds returned -0.07% and 0.18%, respectively, compared to the MSCI All Country World IMI Index and the MSCI World IMI Index, which rose by 1.85% and 1.62%, respectively as shown in Exhibit 2.

In emerging markets, large growth companies were also the main drivers in June. Consequently, the Emerging Markets Large Cap Core Equity fund, with a higher weight in value companies compared to the MSCI Emerging Markets IMI Index, increased by 2.34% while the MSCI Emerging Markets IMI Index rose by 3.83%.

Exhibit 2 – Dimensional Equity Funds Performance: June 2024 (USD)

Our look back at markets in June highlights strong performance in global equities, driven predominantly by large-cap growth in the technology sector, particularly semiconductor companies.

The MSCI All Country World IMI Index rose by 1.85%, with significant contributions from major US and Asian semiconductor firms. The US markets saw gains in large-cap stocks, with the S&P 500 rising by 3.6%, buoyed by companies like Nvidia and Broadcom. A decline in the US Consumer Price Index and the 10-year yield provided further relief to equities by lowering borrowing costs.

Emerging markets also performed well, marked by significant gains in Asia’s largest semiconductor manufacturers and a strong post-election performance in India’s stock market, contributing to a 3.8% increase in the MSCI Emerging Markets IMI Index.

However, small-cap stocks in the US and Europe underperformed, negatively impacting Dimensional equity funds. The Russell 2000 Index fell by 1%, while the Russell 1000 Index rose by 3.31%. In Europe, political uncertainty led to declines in the CAC 40 and STOXX Europe Small 200 Index, with small-cap companies particularly affected. As a result, both Dimensional World Equity and Dimensional Global Core Equity funds underperformed their benchmarks.

Market Index Highlights 1H 2024

The first half of 2024 witnessed significant trends in global equity and bond markets (Exhibit 3), driven by technological advancements and inflation rates influencing major central banks’ decisions on interest rates.

A major factor in market performance was ongoing optimism around Artificial Intelligence (AI), particularly benefiting the tech sector. The semiconductor industry was a primary beneficiary of the AI wave. For instance, chip giants like Nvidia and Broadcom saw substantial gains, rising by 150% and 45%, respectively.

Emerging market semiconductor companies also benefited from the AI wave, albeit to a lesser extent. TSMC, the world’s largest semiconductor manufacturer and the company with the largest weight in the MSCI Emerging Market IMI Index, rose by 64%.

Despite political uncertainties in India and Europe, equities in these regions still delivered strong returns. The Nifty 50 Index, tracking India’s 50 largest companies, and the Stoxx Europe 600, tracking Europe’s 600 largest listed companies, rose by 11.5% and 10.5%, respectively.

Overall, both developed and emerging markets delivered strong returns in the first half of 2024.

Year-to-date, the MSCI All Country World IMI, the MSCI World IMI, the MSCI Emerging Markets IMI, and the S&P 500 rose by 10.28%, 10.63%, 7.41%, and 15.29%, respectively.

In the bond market, yield fluctuations caused volatility in longer-term bond prices. As of 30 June 2024, the US 10-year yield rose slightly from 3.86% to 4.19%. However, income from bond coupons offset the slight decrease in price returns, resulting in the Global Aggregate Bond Index performance standing at 0.13% year-to-date.

Exhibit 3 – Market Index Performance: January to June Performance 2024 (USD)

Dimensional Funds Performance in 1H 2024

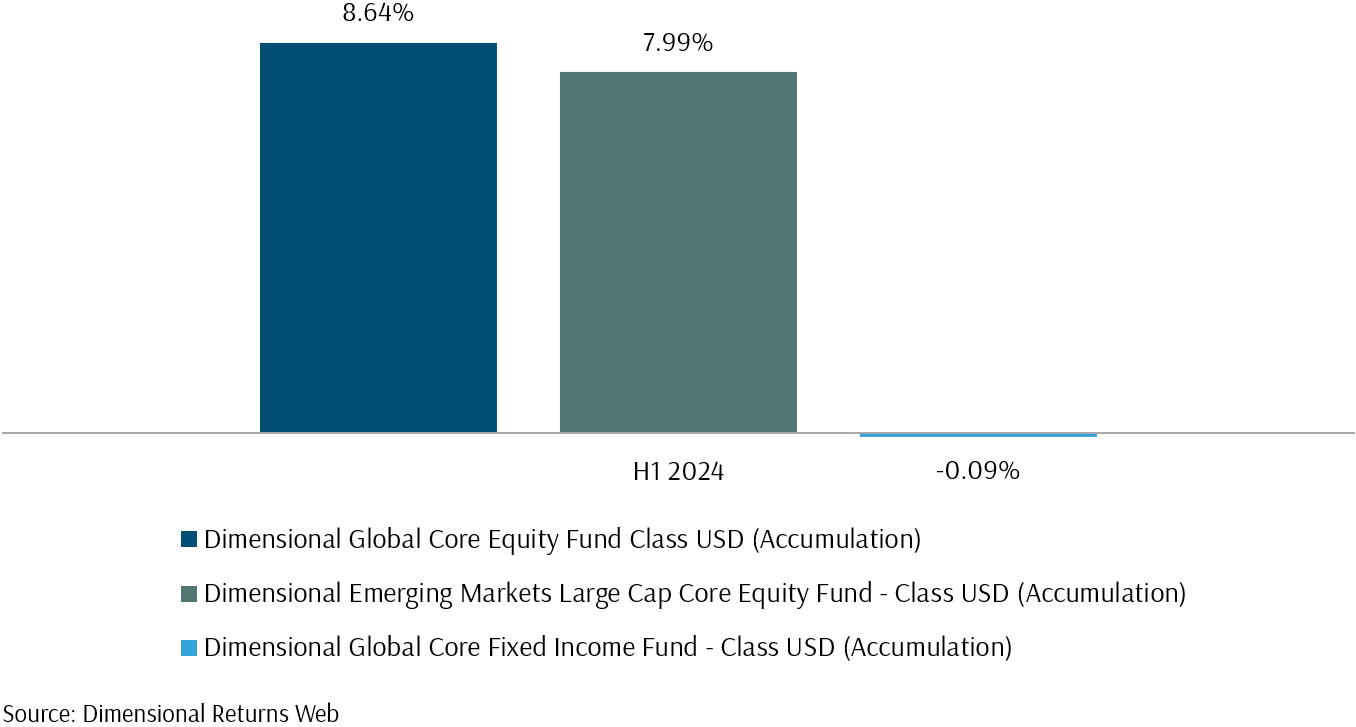

Dimensional equity funds experienced varied performance relative to their market indexes in developed and emerging markets. The Global Core Equity fund, which has a higher allocation to small-cap and value stocks and tracks developed markets’ equities, underperformed the MSCI World IMI Index. This underperformance was largely due to the strong performance of large-cap tech growth stocks within the index.

Prolonged elevated interest rates have put pressure on US regional banks, which are predominantly small-value stocks with significant exposure to struggling commercial real estate through property loans. Additionally, small-cap companies, which typically have higher debt ratios than large-cap companies, faced increased pressure on earnings, contributing to their underperformance. Political uncertainties in Europe also negatively impacted small-cap stocks, particularly evident in June when these stocks struggled, affecting the Global Core Equity fund’s performance. As a result, the Global Core Equity fund returned 8.64%, compared to a 10.63% rise in the MSCI World IMI Index.

In contrast, emerging markets displayed a different trend. The Emerging Markets Large Cap Core Equity fund increased by 7.99%, outperforming the MSCI Emerging Market IMI Index by nearly 0.6%. This was driven by the stronger performance of emerging market small caps compared to large caps. For example, the MSCI India Small-Cap ETF, which tracks Indian small-cap companies, surged by 19.3% year-to-date as of June. Meanwhile, the Nifty 50 Index, which tracks India’s 50 largest companies, rose by 11.5%. The small-cap companies, more reliant on domestic growth, benefited disproportionately from India’s robust economic growth, unlike large-cap companies with a more international presence.

In fixed income, the performance of the Dimensional Global Core Fixed Income fund was nearly flat, with a return of -0.09% year-to-date, similar to the Global Aggregate Bond Index as the slight rise in yields was offset by the income from coupons.

In conclusion, Dimensional equity funds showed mixed performance across different markets in 2024. The Global Core Equity fund, with its focus on small-cap and value stocks in developed markets, underperformed due to the strong performance of large-cap tech stocks and pressures on small-cap companies from higher interest rates and political uncertainties in Europe. Conversely, the Emerging Markets Large Cap Core Equity fund outperformed, buoyed by the robust growth of small-cap stocks, particularly in India. The fixed income segment, represented by the Dimensional Global Core Fixed Income fund, remained relatively flat, mirroring the Global Aggregate Bond Index.

Exhibit 4 – Dimensional Funds Performance: January to June 2024 (USD)

Looking ahead, valuation concerns are becoming more prominent in today’s investment environment. While large-cap tech stocks like Nvidia and Microsoft have experienced substantial valuation expansions, it is crucial to highlight that value and small-cap stocks currently offer compelling opportunities due to their comparatively lower valuations. In the upcoming section, we discuss these valuation dynamics within the equity markets.

The Value of Persistence: Not All P/E Ratios Are High

Concerns about market overvaluation are understandable, particularly with high P/E ratios in the tech sector. Nvidia, for instance, has a P/E ratio of 75x, and Microsoft 40x, indicating high valuations. However, these are exceptions. Many other sectors, like the US financial and energy sectors, which are generally considered value stocks, have P/E ratios of 16.8x and 13.6x respectively, reflecting more grounded valuations.

Globally, valuations vary. Japan’s stock market P/E ratio is 16.7x, while Germany’s is 13.6x, suggesting reasonably valued markets.

Attempting to time the market often leads to missed opportunities. Historically, markets have shown resilience and growth even with high valuations. For example, during the mid-1980s, the market had relatively high P/E ratios but continued to grow steadily, delivering significant returns for long-term investors.

Staying invested allows for the benefits of compounding returns and overall market growth. Instead of exiting the market, a more prudent approach involves diversifying holdings, gaining exposure to small-cap and value premiums, and staying invested. This strategy reduces risks associated with high P/E sectors and positions the portfolio to benefit from long-term market growth.

Investing is a marathon, not a sprint, emphasising the importance of staying invested through market cycles to achieve your long-term wealth goals.

Europe’s Equity Landscape

As part of our series covering the equity landscape of major economies, the next section will delve into the equity landscape of Europe.

1. Importance of Europe’s Equity Landscape

Understanding Europe’s equity landscape is crucial for investors with globally diversified portfolios. Europe holds the second largest weight in the MSCI All Country World IMI Index at approximately 13.3%, and 9.3% if we only consider the European Union (EU), following the United States at 63.2%. This index covers 99% of the global investable equity market.

Post-Brexit, many aspects of the EU’s economic and financial landscape are distinct from the UK’s. Focusing on the EU allows us to address these specific dynamics without the added layer of UK considerations. However, many widely referred Europe indexes, such as the STOXX 600, include UK stocks. This could make it challenging to isolate EU-specific data and comparisons. Moreover, accounting for almost one-third of Europe’s equity weight in the MSCI All Country World IMI Index, excluding the UK would not provide a comprehensive view of the European equity market.

Therefore, to maintain a manageable length and complexity while ensuring thorough coverage, this review will primarily focus on the EU markets, with the UK’s influence on European markets discussed to a lesser extent.

2. Overview

In this series on Europe’s equity landscape, we will begin by examining the diversification advantages of holding European equities, which are currently valued cheaper compared to US equity markets.

We will then explore the factors contributing to this valuation difference, including comparing estimates of European equities forward earning growth estimates versus the US.

Next, we will look at the short-term challenges Europe has faced in recent years that may have contributed to its larger discount compared to US equities. This analysis will delve into the events that unfolded in recent years that placed pressure on or created uncertainty in Europe companies’ earnings, leading to a discounted share price in European equities. These include the:

A. Ukraine-Russia War – We examine the impact of the Ukraine-Russia war on investor sentiment and European market valuations. We analyse how the conflict has influenced risk perceptions and economic uncertainties, driving down equity market valuations in Europe compared to the US.

B. Energy Crisis and Future Supply Uncertainty – We look into the energy crisis and its impact on future supply uncertainty in Europe. We explore how the crisis has influenced investor sentiment and stock valuations, highlighting the broader economic implications for European equities.

C. Political Changes in the UK, France, and Germany – We examine the political changes in the UK, France, and Germany, and their impact on equity valuations. We explore how significant political shifts in these major European countries have created an environment of uncertainty and cautiousness among investors.

Lastly, we will evaluate the long-term outlook that may have also led to a higher discount of the European equities market against the US.

D. Dependency on China’s Economy – The EU’s economic relationship with China plays a significant role in shaping its equity market landscape. This dependency brings both substantial opportunities and considerable risks, influencing market dynamics and investor sentiment.

E. Demographic Challenges and Healthcare Sector Opportunities – Europe’s ageing population is exerting a profound influence on its equity markets, impacting corporate earnings and valuations. This demographic shift presents both challenges and opportunities, particularly within the healthcare sector, which is poised to benefit from the increased demand for age-related healthcare services.

F. Higher Saving Rates and Increase Fiscal Spending – Europe’s higher savings rate and lower debt-to-GDP ratio compared to the US position it uniquely in the global economic landscape. These financial dynamics offer significant benefits and potential growth opportunities for European companies, setting the stage for sustainable economic expansion.

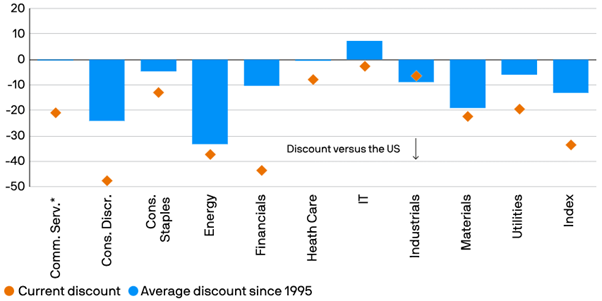

3. The Diversification Advantage of the European Market

Europe provides significant diversification benefits to the US market. Its valuations are currently discounted across nearly all sectors compared to the US market (Exhibit 5).

Exhibit 5 – MSCI Europe Sectors Forward P/E Ratio Discount Versus the S&P 500 (%)

4. Factors Contributing to Lower Valuation of Europe Equities Compared to US Equities

The PE ratio is a key valuation metric used to justify why European equities are perceived as trading at a lower, or cheaper, valuation. It assesses a company’s worth by dividing its current share price by its earnings per share (EPS), indicating how much investors pay per dollar of earnings.

If a US company and a European company have equivalent earnings but the US company commands a higher valuation, two reasons may explain this:

- Firstly, the US company might offer greater potential for earnings growth.

- Secondly, specific risks unique to the European company’s operations may create

uncertainty about its future earnings. In scenarios where these risks do not materialise and assuming similar earnings growth rates between the European and US companies, investors could potentially realise higher returns from the European company.

Considering the broader European equities market, it is crucial to evaluate the earnings growth potential and identify any unique risks within Europe that contribute to its lower valuation.

5. Comparison of EPS Growth: US vs. Europe Equity Markets

When comparing the earnings per share (EPS) growth of companies in the US and European equity markets, a clear distinction emerges between their historical performance and future expectations.

Historical Performance

The US equity market, represented by the S&P 500 Index, has historically shown strong EPS growth, averaging around 8.72% annually. However, in 2023, the S&P 500 saw a slight decline, with EPS dropping from $48.41 in Q1 2023 to $47.37 in Q1 2024[1], marking a year-over-year decrease of approximately 2.15%. In contrast, the European equity market, represented by the STOXX Europe 600 Index, experienced a more significant decline in EPS growth, with an estimated fall of 4.1% from Q1 2023 to Q1 2024[2].

Future Expectations

Looking ahead, forecasts indicate differing growth trajectories for the two markets. According to Factset[3], the S&P 500 is expected to see EPS growth of 8.8% in Q2 2024, 8.1% in Q3 2024, 17.3% in Q4 2024, and 15.2% in Q1 2025. Conversely, Lipper Alpha[4] estimates that the STOXX 600 will have earnings growth rates of 2.8% in Q2 2024, 9.4% in Q3 2024, 12.8% in Q4 2024, and 13.2% in Q1 2025.

Sectoral Insights:

While EPS growth in the US market is primarily driven by the technology sector, with some contribution from healthcare, the EU’s growth prospects appear more diversified. In the EU, sectors such as basic materials, real estate, cyclical and non-cyclical consumer goods, and technology are all expected to contribute to forward EPS growth.

Additionally, within the largest developed markets, the information technology sector’s weight in the most referenced index[5] is 30% for the US, 51% for Japan, and 7% for Europe. This diversification away from the information technology sector in terms of EPS growth rates and sector weights offers a potential buffer for investors.

For instance, if the anticipated AI boom in the US fails to meet expectations, it could significantly impact the future earnings growth of US equities. However, the broader sectoral base in Europe might provide a cushion for globally diversified investors.

Conclusion for Comparison of EPS Growth

In summary, while the US equity market has historically outperformed Europe in terms of EPS growth, future prospects suggest a more balanced outlook. Europe’s diversified sectoral growth and proactive fiscal policies provide a promising landscape for investors, despite the inherent risks. As such, a well-diversified portfolio including both US and European equities could offer a robust strategy for navigating the global market’s uncertainties.

Despite promising forward EPS growth, European equities continue to be valued lower than their US counterparts. This discrepancy is likely due to higher perceived risks and uncertainties in the EU region, which create a more unpredictable environment for future earnings.

In the following section, we will explore the possible challenges in the short run that may have led to the market pricing a higher premium (or lower valuation) for the potential risk in Europe’s equity market.

6. Potential Factors Impacting Europe’s Valuation

Short-Term Challenges

6A. Impact of Ukraine-Russia War on Investor Sentiment and European Market Valuations

The ongoing conflict between Ukraine and Russia continues to cast a shadow over investor sentiment in Europe, contributing to lower equity market valuations compared to the US. The war has intensified economic uncertainties, leading investors to demand higher risk premiums for holding European equities, thus driving down their valuations.

Investor Sentiment and Market Impact

Heightened Risk Aversion:

Recent data from S&P Global Commodity Insights[6] highlights the severe disruption in energy supplies due to the conflict. For instance, the European Union’s gas and liquefied natural gas (LNG) imports from Russia drastically decreased from 155 billion cubic meters (Bcm) in 2021 to just 43 Bcm in 2023. This shift has forced Europe to rely heavily on alternative suppliers, such as Norway, Algeria, and Azerbaijan, to meet its energy demands.

The instability and unpredictability brought about by the war have heightened investors’ risk perceptions. These heightened risks are reflected in the increased volatility and lower valuations of European markets, as investors demand higher risk premiums for holding European equities.

Sanctions and Market Disruption:

Sanctions imposed on Russia have had widespread economic repercussions. They have not only affected Russian companies but also those in Europe with significant exposure to the region. Accenture’s 2024[7] analysis points out that these sanctions have led to operational risks and supply chain disruptions, increasing the overall uncertainty in European markets.

By examining these factors, the Ukraine-Russia war may negatively impact investor sentiment, leading to lower valuations in European equity markets compared to their US counterparts. This ongoing uncertainty and the associated economic risks underscore the challenges facing European markets in the near term.

6B. Energy Crisis and Future Supply Uncertainty

Europe’s energy crisis, driven by the fallout from Russia’s invasion of Ukraine, has significantly impacted the valuation of European equities. The crisis has led to increased uncertainty about future energy supply and elevated energy costs, which have in turn affected investor sentiment and stock valuations.

The disruption of Russian natural gas supplies forced Europe to pivot quickly towards liquefied natural gas (LNG) imports, increasing its dependency on global LNG markets. In 2022, Europe LNG imports surged by almost 60%[8], with LNG making up 53% of the region’s total gas supply, compared to an average of 20% between 2000 and 2019. This increased demand for LNG also led to higher energy prices[9], peaking at €207/MWh in August 2022, significantly higher than the average of €11/MWh observed between 2011 and 2020.

The high energy costs have had a pronounced negative effect on European firms’ equity returns. Research[10] indicates that a one standard deviation increase in energy exposure is associated with a 0.9 percentage point reduction in European firms’ returns, whereas in the US, the same increase is linked to a 0.7 percentage point rise in returns. This differential highlights the competitive disadvantage[11] faced by European firms due to higher energy costs and supply uncertainty.

Additionally, the European Union’s efforts to stabilise energy supplies have involved significant financial outlays[12]. Between September 2021 and January 2023, EU countries spent over €650 billion on measures to mitigate the crisis, including energy tax abatements, price ceilings, and fiscal transfers. Germany alone accounted for about €158 billion of this total.

These factors combined have led to discounted valuations for European equities as investors reassess the region’s economic prospects amidst ongoing energy challenges. This situation underscores the critical impact of energy security and the cost on corporate performance.

War and rising costs have frequently led to voter dissatisfaction. As European voters grow increasingly polarised, they share a common goal: seeking change from the incumbent party. In the following section, we will explore how this dynamic has also affected equity valuations.

6C. Political Changes in the UK, France, and Germany

In 2024, Europe’s political landscape experienced significant shifts, leading to increased uncertainty and negatively impacting equity valuations. The major elections in France, the UK, and the broader European Parliament saw substantial gains for both right-wing and left-wing factions, creating a fragmented and polarised political environment.

France

In France, the legislative elections[13] saw the far-right National Rally (RN) led by Marine Le Pen winning 142 seats, marking a significant gain from their previous standing. The leftist coalition New Popular Front (NFP) won the largest number of seats with 188, followed by President Macron’s centrist Ensemble coalition with 161 seats. No group has won the required majority seats of 289 to govern. This division raised concerns about policy continuity and potential political gridlock, affecting investor confidence and contributing to market volatility.

United Kingdom

The UK experienced a political shift with the victory of the left-wing party in the general elections, resulting in a new Prime Minister from the Labour Party. This change came amid economic challenges and uncertainties surrounding Brexit trade deals and domestic economic policies, leading to cautious sentiment among investors.

Germany

Although Germany did not hold national elections in 2024, the right-wing Alternative for Germany (AfD) continued to gain support, reflecting a broader trend of rising right-wing populism across Europe. This rise in right-wing sentiment added to the political uncertainty, particularly in the context of EU policymaking and cohesion[14].

Impact on Equity Valuations

The political turmoil and the resulting uncertainty have led to a discounted valuation of European equities. For example, the STOXX Europe 600 Index saw a decline of around 1.3% in June, reflecting investor concerns over the fragmented political landscape and its implications for economic stability and growth prospects.

Overall, the 2024 elections underscored the deepening political divides within Europe, which have created an environment of uncertainty and caution among investors, thereby impacting equity valuations across the continent.

Conclusion for Short-Term Challenges

In conclusion, European equity markets are facing significant short-term challenges due to a combination of geopolitical, economic, and political factors. The ongoing Ukraine-Russia war has dampened investor sentiment, leading to lower market valuations and increased risk aversion, particularly evident in energy supply disruptions and higher risk premiums.

The European energy crisis, exacerbated by reduced Russian gas supplies, has resulted in higher energy costs and further market uncertainty, negatively impacting corporate performance and equity returns. Additionally, political changes and electoral shifts in key European countries have contributed to market volatility and discounted valuations due to concerns over policy continuity and economic stability. Together, these factors underscore the heightened uncertainty and challenges currently affecting European markets.

Long-Term Outlook

6D. The EU’s Dependency on China – A Double-Edged Sword

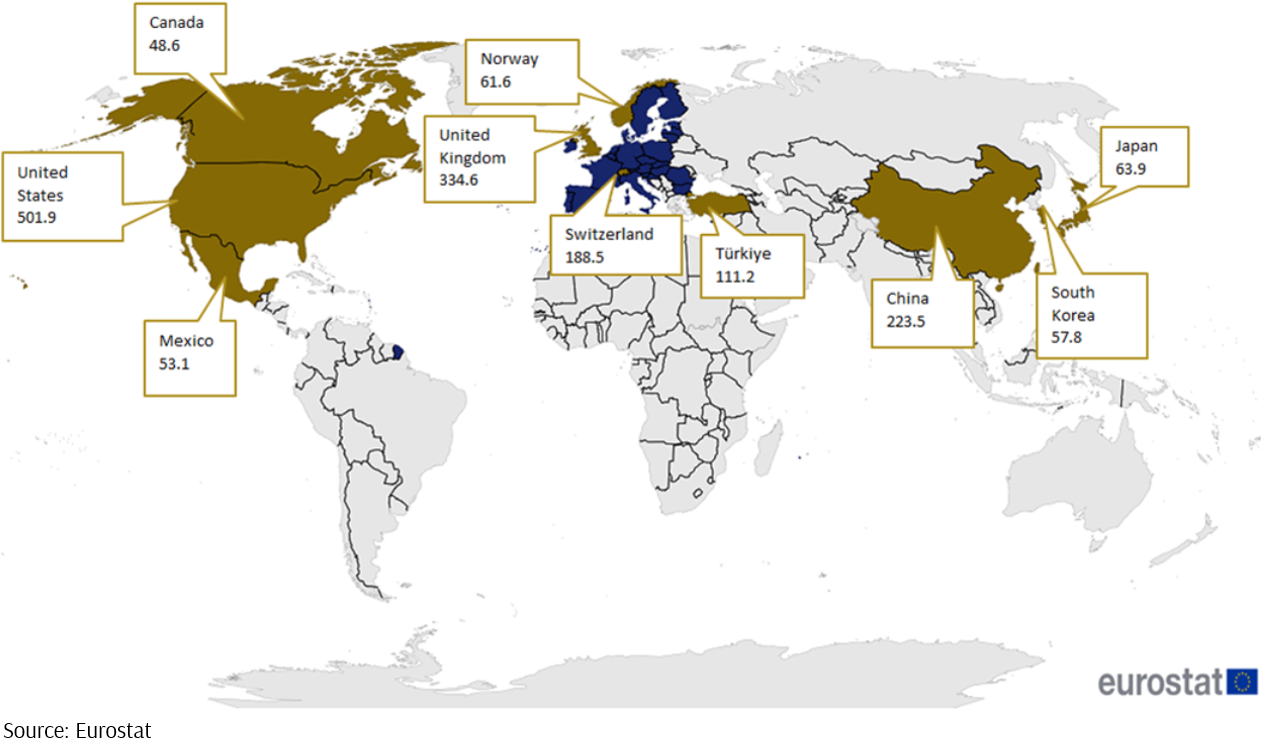

According to Eurostat, China was the EU’s third-largest trading partner in 2023 (Exhibit 6), with an export value of 244 billion USD (223.5 billion Euro), compared to 147.8 billion USD for the US. In 2019, MERICS[15] took a sample of 25 listed EU companies from different member states and industries to gauge European corporate dependence on China. They found that, on average, these companies generated 11.2% of their revenue in 2019 in the People’s Republic of China.

Exhibit 6 – Principal Partners for EU Exports of Goods, 2023 (Billion Euros)

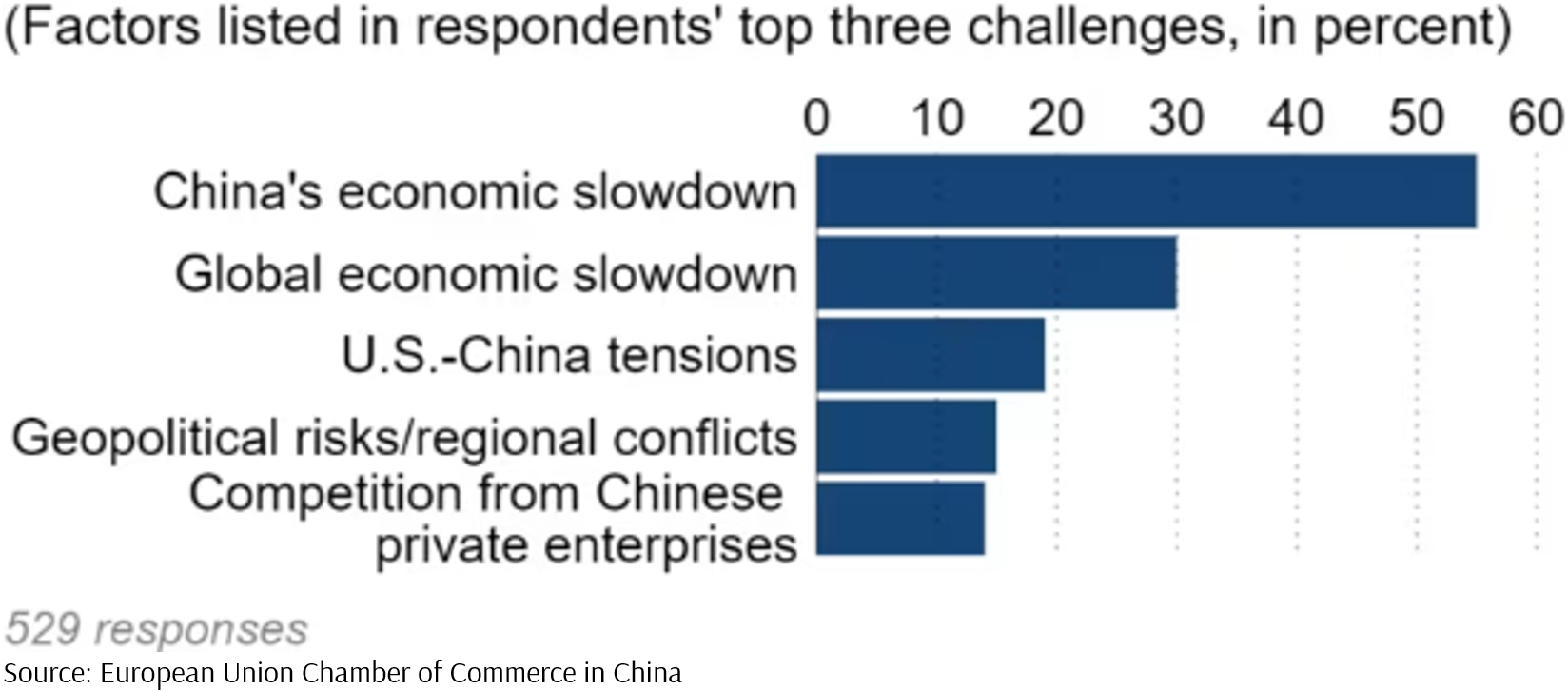

In the European Chamber of Commerce’s annual business confidence survey conducted in early 2024 on 529 EU companies, 55% of respondents ranked the slowing Chinese economy as a top-three challenge, compared with 36% the previous year (Exhibit 7).

Exhibit 7 – Major Challenges in China for European Companies

As China’s weak consumption demand persists, it is expected to impact EU equity markets. Nevertheless, the EU’s economic ties with China offer both opportunities and risks. As China potentially rebounds and consumption demand strengthens, EU companies could experience increased export opportunities.

Conclusion of the EU’s Dependency on China

In summary, while the slowdown in China poses risks to EU equity markets, a potential economic recovery there could stimulate EU export growth and overall economic expansion.

6E. The Impact of Europe’s Ageing Demographics on Equities Valuations

Evidence of Europe’s Ageing Population

Europe is experiencing significant demographic changes characterised by an ageing population. Over the past two decades, the share of people aged 80 and over in the EU has risen from 3.7% in 2003 to 6.0% in 2023[16]. Additionally, the share of individuals aged 65 and over increased from 16.2% to 21.3% in the same period. This shift is expected to continue, with the median age of the population projected to increase from 44.5 years in 2023 to 48.2 years by 2050. Similarly in the UK, we are also witnessing a fast pace of increasing proportion of the ageing population[17].

Impact on Companies’ Earnings and Valuations

The ageing population in Europe impacts companies’ earnings and valuations in several ways:

- Labour Market Constraints: With fewer young people entering the workforce, there is a smaller pool of talent to hire from. This labour shortage drives up hiring costs and can lead to decreased productivity.

- Increased Wage Pressure: As the working-age population shrinks relative to retirees, companies may face increased wage pressure to attract and retain employees.

- Changing Consumer Demand: Older populations typically spend less on certain goods and services, shifting consumer demand patterns that companies must adapt to.

In 2023, the old-age dependency ratio[18] was 33.4%, meaning there were just over three working-age individuals for every person aged 65 and over. This ratio is projected to rise, further straining economic resources.

Healthcare Sector: A Beneficiary of Ageing Demographics

Performance of Healthcare Giants

Despite the demographic challenges posed by an ageing population, the healthcare sector, which holds the highest weighting in the Stoxx Europe 600 at 15.9%, is poised to gain significant advantages. Companies like AstraZeneca and Novo Nordisk B have seen significant stock performance improvements over the past decade, driven by the increasing demand for healthcare services and products.

AstraZeneca

Over the past ten years, AstraZeneca’s stock has risen significantly, fuelled by successful drug developments and acquisitions. For instance, its oncology portfolio and respiratory treatments have driven robust earnings growth.

From 2014 to 2023, AstraZeneca saw significant growth in its oncology and respiratory segments. Oncology revenue grew from $2.9 billion[19] in 2014 to $17.15 billion in 2023, driven by successful drugs like Tagrisso and Imfinzi. Their respiratory segment also experienced growth, with revenues rising from $4.3 billion in 2014 to $6.1 billion in 2023, supported by strong sales of Symbicort and Fasenra.

AstraZeneca’s share price grew 183% from 2014 to 2023, reflecting the company’s strong performance and strategic initiatives.

Novo Nordisk

Novo Nordisk, known for its diabetes care products, has also performed exceptionally well. The company’s focus on diabetes and obesity treatments has resulted in a substantial increase in its market value.

Novo Nordisk’s share price increased 608% from 2013 to 2014, driven by its innovative products and expanding global reach.

Profiting from Demographic Shifts

The healthcare sector benefits from the ageing population through the increased prevalence of age-related diseases such as cancer, diabetes, and cardiovascular conditions. AstraZeneca and Novo Nordisk have capitalised on this by developing and marketing drugs that address these conditions.

For example:

- AstraZeneca’s blockbuster cancer drug, Tagrisso, has become a significant revenue driver.

- Novo Nordisk’s diabetes treatment, Ozempic, and obesity drug, Wegovy, have seen substantial market success.

Conclusion of the Impact of Europe’s Ageing Demographics

While Europe’s ageing demographics pose challenges to equity valuations, the healthcare sector remains a bright spot. Companies like AstraZeneca and Novo Nordisk are well-positioned to benefit from the increased demand for healthcare services. As more developed economies face similar demographic shifts, the growth potential for these healthcare giants extends beyond Europe, indicating a promising future despite the broader economic challenges.

6F. The Impact of Europe’s Higher Savings Rate on European Companies and Lower Debt-To-GDP versus the US

Higher Savings Rate in Europe Compared to the US

Europe traditionally exhibits a higher savings rate compared to the US. This trend can be illustrated by the European Union’s gross household saving rate, which has consistently been higher than that of the US. According to data from Trading Economics, the savings rate in the European Union[20] was 13.7% as of Q4 2023, while the UK[21] was 10.2%, significantly higher than the US[22] savings rate of 4%.

Benefits of Higher Savings Rates for European Companies

Increased savings rates can positively impact European companies in several ways:

- Increased Investment Capacity: Higher savings rates can translate to increased investment capacity among individuals and institutions. This can lead to more capital being available for investment in businesses, infrastructure, and innovation. Companies in sectors like banking, real estate, and technology stand to benefit significantly from this increased availability of capital.

- Consumer Spending Potential: While high savings rates can indicate a cautious approach to spending, they also suggest a potential for future spending booms. As savings accumulate, consumers may eventually increase their expenditure, benefiting retail, automotive, and luxury goods sectors. For instance, luxury brands like LVMH and retail giants like Carrefour could see heigthened sales as accumulated savings are converted into increased consumption.

Debt-To-GDP Comparison and Fiscal Policy

Europe’s Debt-to-GDP vs. the US

The debt-to-GDP ratio is a critical indicator of a country’s fiscal health. As of the latest data, the European Union’s debt-to-GDP ratio is lower compared to the US. As of 2023, the EU and UK debt-to-GDP ratios stand at around 88%[23] and 97.6%[24] respectively, while the US ratio is approximately 122.3%[25]. This relatively lower debt level suggests that European governments have more room to manoeuvre fiscally.

Shift from Fiscal Austerity to Fiscal Spending

In recent years, Europe has shifted from fiscal austerity to increased fiscal spending. For instance, the NextGenerationEU[26] initiative is a major recovery plan aimed at boosting investment across the EU, focusing on green and digital transitions. In the UK, the Labour Party has pledged to increase spending on healthcare, education, and infrastructure, signalling a move towards more expansive fiscal policies.

Impact on European Companies

Increased fiscal spending can significantly benefit European companies in several ways:

- Boosting Demand: Government spending can stimulate economic activity, increasing demand for goods and services. Sectors such as construction, technology, and green energy are likely to benefit from public investments.

- Supporting Innovation: Investments in infrastructure and technology can foster innovation and competitiveness. Companies involved in renewable energy, digital services, and advanced manufacturing could see substantial gains.

Conclusion: The Impact of Europe’s Higher Savings Rate on European Companies and Lower Debt-To-GDP Versus the US

Europe’s higher savings rates and relatively lower debt-to-GDP ratio provide a robust foundation for future economic growth. The shift from fiscal austerity to increased fiscal spending, as evidenced by initiatives like NextGenerationEU and policy shifts in the UK, can further bolster this growth. European companies, particularly those in investment-heavy and consumer-driven sectors, stand to benefit significantly from these dynamics. Thus, while the US has historically exhibited a higher consumption propensity, Europe’s strategic fiscal management and high savings rates may pave the way for sustainable and balanced economic expansion.

Conclusion: Europe’s Equity Landscape

In conclusion, the European equity landscape offers significant diversification benefits and opportunities despite the challenges it faces. The region’s equities are currently valued cheaper compared to the US, influenced by factors such as the Ukraine-Russia war, energy crisis, and political changes. These events have created uncertainty and pressured earnings, contributing to discounted valuations.

Despite these challenges, European equities have promising mid to long-term growth prospects. The region’s dependency on China’s economy, while posing risks, also presents opportunities for export growth. Additionally, Europe’s ageing population drives demand in the healthcare sector, benefiting companies like AstraZeneca and Novo Nordisk.

Moreover, Europe’s higher savings rate and lower debt-to-GDP ratio compared to the US provide a unique financial dynamic that supports economic stability and growth. These factors highlight the potential of European equities as part of a well-diversified investment portfolio, offering a balanced outlook amidst global market uncertainties.

The Europe Fox: Balancing the Savanna with Diversified Strength (A Metaphor)

In a vast savannah where the lion, known as the king of the jungle, dominates the landscape, the lion represents the US market, particularly the S&P 500. Just like the lion, the US market is strong and commands a high valuation (PE ratio), drawing significant attention and investment. A notable portion of this lion’s strength comes from its tech-savvy mane, which constitutes 35% of its territory.

However, as majestic as the lion is, the savannah is home to a variety of other creatures that contribute to the ecosystem’s balance. Enter the Europe fox, representing the Europe market. Unlike the lion, the fox is more understated and diversified in its habitat. With a PE ratio much lower than the lion’s, the fox lives in a less crowded and less competitive environment. Moreover, only 8% of the fox’s diet relies on the tech sector, allowing it to thrive on a more varied diet that includes different sectors and industries.

When the savannah faces challenges, such as a drought that might impact the US lion’s tech-dominated territory, the Europe fox’s diversified diet allows it to adapt and survive better. Similarly, when high-valuation stocks, particularly within the tech sector, are under pressure in the US market, the European market, with its broader and less tech-heavy composition, offers a refuge.

By investing in both the lion and the fox, you ensure that your portfolio is not overly dependent on one type of food source or environment. This diversification within the savannah’s ecosystem provides a more stable and resilient investment strategy, capable of weathering various market conditions.

In essence, the Europe fox brings balance to the savannah, offering diversification benefits that protect against the risks associated with high-valuation stocks in the tech-heavy US market, represented by the lion.

Reflections on 1H 2024

As we reflect on the first half of 2024, it is evident that large-cap tech stocks led the rally, and challenges persisted in small-cap and value sectors. Looking ahead, maintaining a diversified approach remains key to navigating market uncertainties and achieving your wealth goals.

For example, the European equity market, with its current lower valuations and sectoral diversification, offers significant benefits to investors against developed markets that have a proportionately concentrated technology sector. This highlights the importance of maintaining a well-diversified portfolio to mitigate risks and capitalise on varied market opportunities, reinforcing the strategic advantage of diversification in achieving long-term investment goals.

We hope you found this piece on Europe’s equity landscape informative, and we thank you for staying informed and committed to your wealth journey with us. Should you have any concerns, please do not hesitate to reach out to your Client Adviser. Thank you.

– Footnotes –

[1] YCHARTS: S&P 500 Earnings Per Share.

[2] LSEG: STOXX 600 EARNINGS OUTLOOK.

[3] FACTSET: EARNINGS INSIGHT.

[4] LSEG: STOXX 600 EARNINGS OUTLOOK.

[5] The S&P 500, the Stoxx Europe 600 and the Nikkei 225.

[6] S&P GLOBAL: After two years of war, Europe emerging from shadow of Russian gas.

[7] Accenture Risk Study: 2024 Edition.

[8] CEPR: The European energy crisis and the consequences for the global natural gas market.

[9] CEPR: The Ukraine invasion and the energy crisis: Comparative advantages in equity valuations.

[10] CEPR: The Ukraine invasion and the energy crisis: Comparative advantages in equity valuations.

[11] ECONPAPERS: The invasion of Ukraine and the energy crisis: Comparative advantages in equity valuations.

[12] CEPR: The European energy crisis and the consequences for the global natural gas market.

[13] POLITICO: How France voted: Charts and maps.

[14] Reuters: Explainer: Turning back the clock: Germany’s AfD and the economy.

[15] MERICS: Mapping and recalibrating Europe’s economic interdependence with China.

[16] Eurostat: Population structure indicators at national level.

[17] Centre for Ageing Better: Our Ageing Population | The State of Ageing 2023-24.

[18] The number of people aged 65+ compared to those aged 15-64.

[19] AstraZeneca PLC: FOURTH QUARTER AND FULL YEAR RESULTS 2014.

[20] Trading Economics: European Union Gross Household Saving Rate

[21] Trading Economics: United Kingdom Household Saving Ratio.

[22] Trading Economics: United States Personal Savings Rate.

[23] Eurostat: Government debt down to 88.6% of GDP in euro area.

[24] Trading Economics: United Kingdom Public Sector Net Debt to GDP.

[25] Trading Economics: United States Gross Federal Debt to GDP.

To learn more about our purpose-driven approach towards investment management, please visit this link.

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current estate plan, investment portfolio, financial and/or retirement plan, make an appointment with us today.