What an eventful year. Before we look ahead to 2021, let us take a look back at how stocks and bonds performed in 2020 and see what happened.

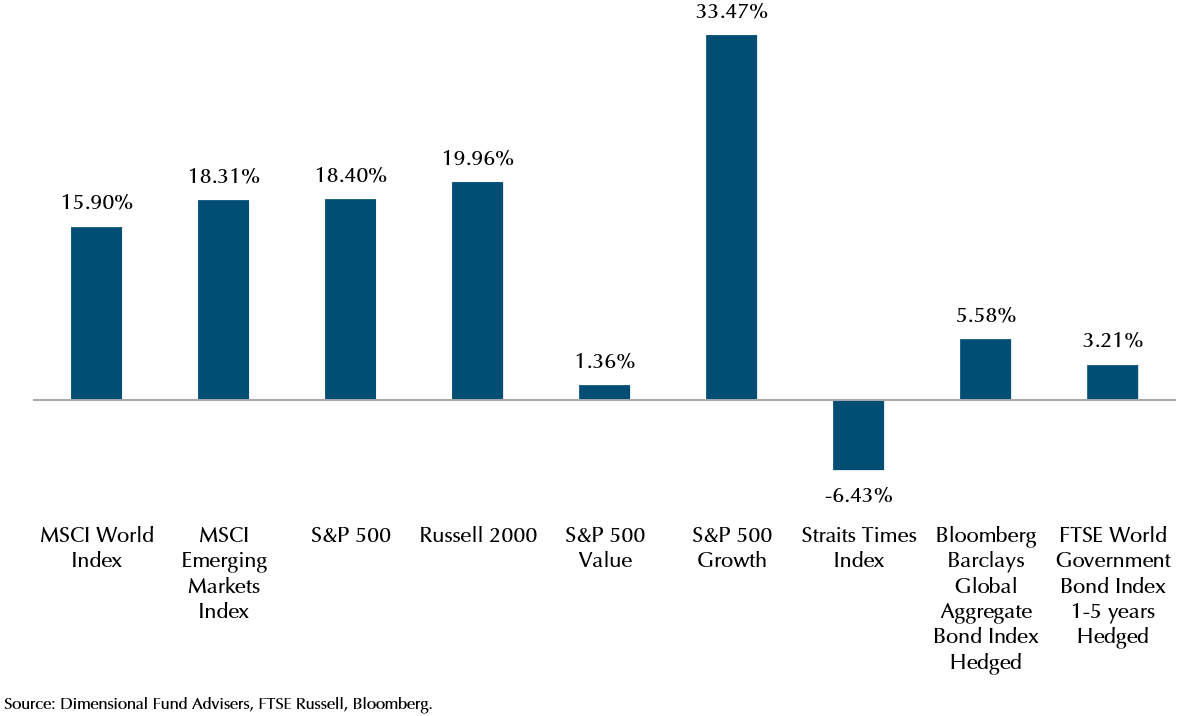

Exhibit 1: Performance of major indices 2020 (USD returns)

Some observations from the data above

Investing globally helps us capture the returns from diversification

The first thing that we would notice from the chart above is that unfortunately, our local index did not fare so well in 2020. Diversifying into a global Index such as the MSCI World (which captures 85% of the market cap of developed markets) or the MSCI Emerging Markets (which captures 85% of the market cap of emerging markets) would have given a very different investment outcome for 2020. It has been something we mention over and over again, but it is really something we focus on, as our portfolios are diversified not just across geography, but also risk premiums or factors which leads into our next observation.

Most risk premiums were present in 2020

We would expect intermediate term bonds (5-15years) to return higher than short term bonds, as they are riskier assets. That was indeed the case with the Bloomberg Barclays Global Aggregate Bond Index returning more than the FTSE World Government Bond Index 1-5 year.

We would expect stocks to return more than bonds as they are the riskier asset. That was indeed the case with Global stocks as represented by the MSCI World Index returning more than bonds.

We would expect that emerging market stocks return more than developed world stocks as they are the riskier asset. That was indeed the case this year as EM stocks returned 2.41% more than developed world stocks.

We would expect smaller companies to return more than larger companies as they are the riskier asset. That premium was also present this year especially in the US, with the Russell 2000 (which represents small companies in the US) returning 1.56% more than the large companies represented by the S&P 500. This premium was also present globally, with the MSCI AC World Small Cap outperforming the MSCI AC World slightly.

Unfortunately, there is one premium that did not show up, and that is the value premium. Over the year, the value premium underperformed the growth premium by a whopping 32.11% if we just look at the S&P 500 measures of value and growth. This was one of the worst years on record for the underperformance of the value premium, driven by the huge shift to digital solutions as the pandemic forced the world to adapt to working from home for months, and pushing up the valuations of the tech companies.

Thankfully, our portfolios are diversified across risk premiums. We do not just focus on value exclusively (although we do talk about it often). We own stocks, giving us exposure to the equity premium, we also have small companies, letting us benefit from the small cap premium and we have an allocation to emerging markets allowing us to benefit from the performance of this riskier asset class.

Premiums show up at different times

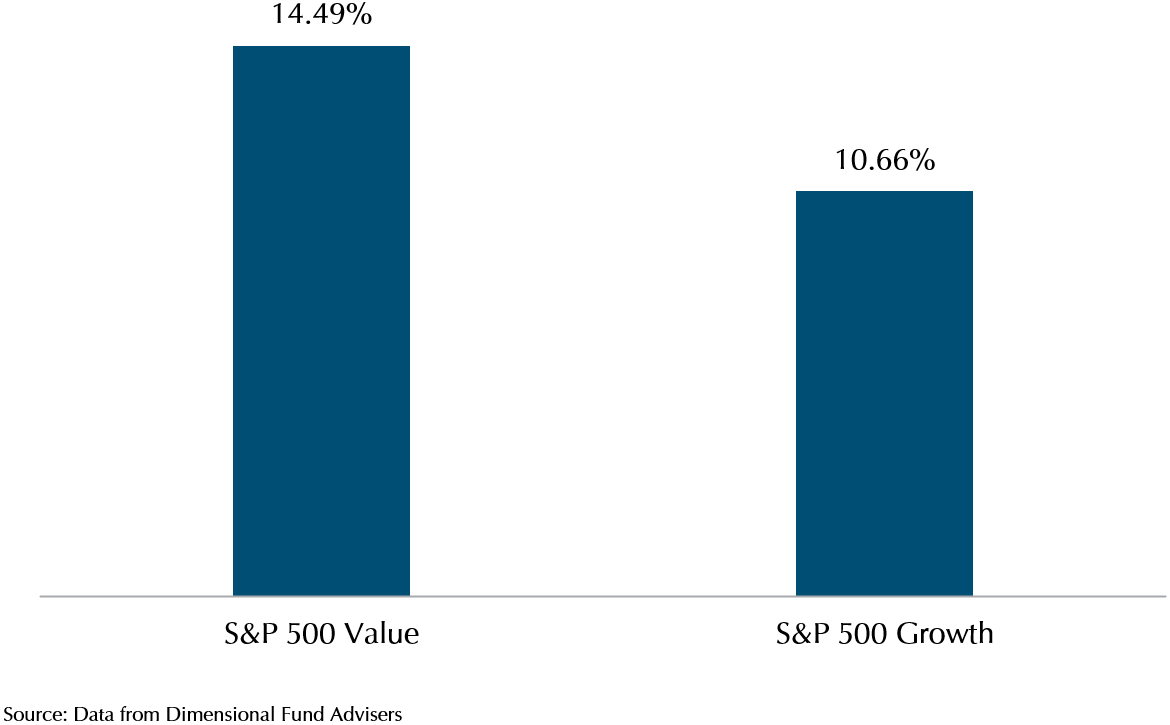

As for the value premium, it has not gone away. In the past 3 months, there has been a small resurgence in value stocks.

Exhibit 2: S&P 500 value vs growth 4Q 2020 (USD returns)

As we can see from the chart above, the last quarter of 2020 saw an almost 4% outperformance for value stocks. We have no way of knowing when premiums show up, so what we should focus on is to ensure that our portfolios are diversified across premiums so we are able to capture the returns when they do show up.

What lies ahead in 2021?

We must apologise for the slightly misleading title of this article. While we could give you a view of what lies ahead in 2021, the truth is that it would serve very little purpose, as it would not be very accurate.

Looking back at all the market outlooks for 2020, almost no one (except maybe Bill Gates) predicted that a global pandemic would upend life as we knew it, cause one of the deepest recessions since the 2nd World War, and in spite of that, stock markets would have one of the best years on record.

What we would like to do is to remind you of the few fundamentals that drive the markets.

1. Stocks are pricing in future cash flows, today.

Over the past year, some of you might have heard our Senior Advisor Dr Peng Chen speak, and he shared this basic equation on what drives the stock price (P).

![]()

This is the present value of future cashflows (CF), discounted by the discount rate (r). If CF increases, all else being equal, P will increase. If r decreases, all else equal, P will increase. While this is a basic 2 factor equation, it does highlight the relationship between future cashflow and the price of a stock.

For example, in March 2020, as markets expected lockdowns due to the pandemic, stocks fell as companies were expected to have lower cashflows. As the year progressed, and optimism returned, helped by the vaccine news, markets are expecting a better 2021 and stocks rose.

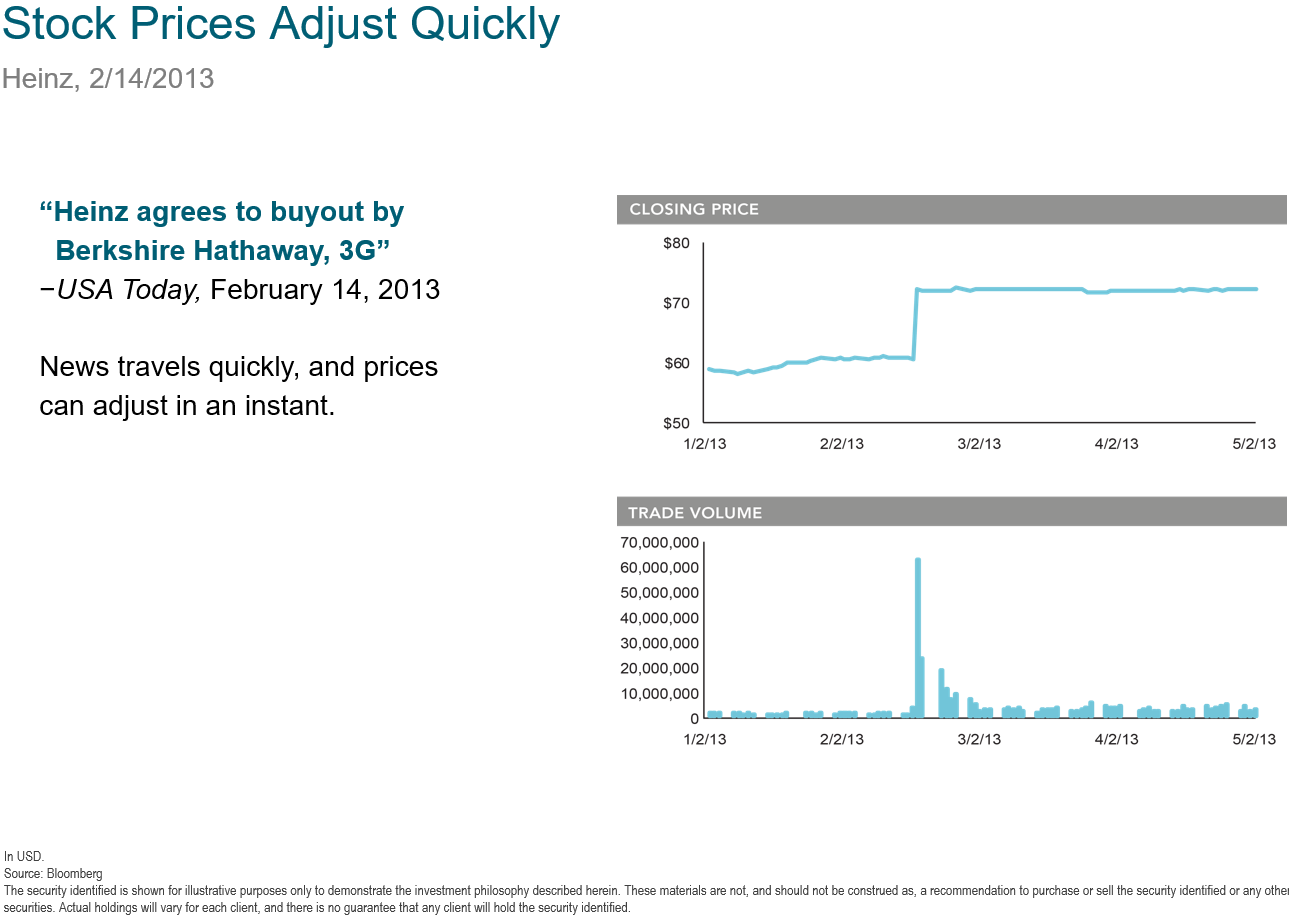

2. Markets are efficiently pricing in current information all the time

Stock prices move every day because the market is constantly pricing in all the new information that comes in, that might affect the future cashflow of a company. Analyst reports, financial updates from the company, news on external or internal influences that might affect the business outlook for a company, etc. All this information is constantly being factored into the price investors are willing to pay for a company every day. Stock prices going up from good news that improves a company cashflow or falling from bad news that reduces a company cashflow, are signs that the market is working efficiently.

Going back to March 2020 again, the fact that markets fell sharply was because it was pricing in an economic contraction from the lockdown of much of the global economy, an event that is truly unprecedented in peacetime during recent human history.

A more specific example below shows how a stock price instantly reacts to a private equity bid for a company.

Exhibit 3: Efficient markets price in new information quickly

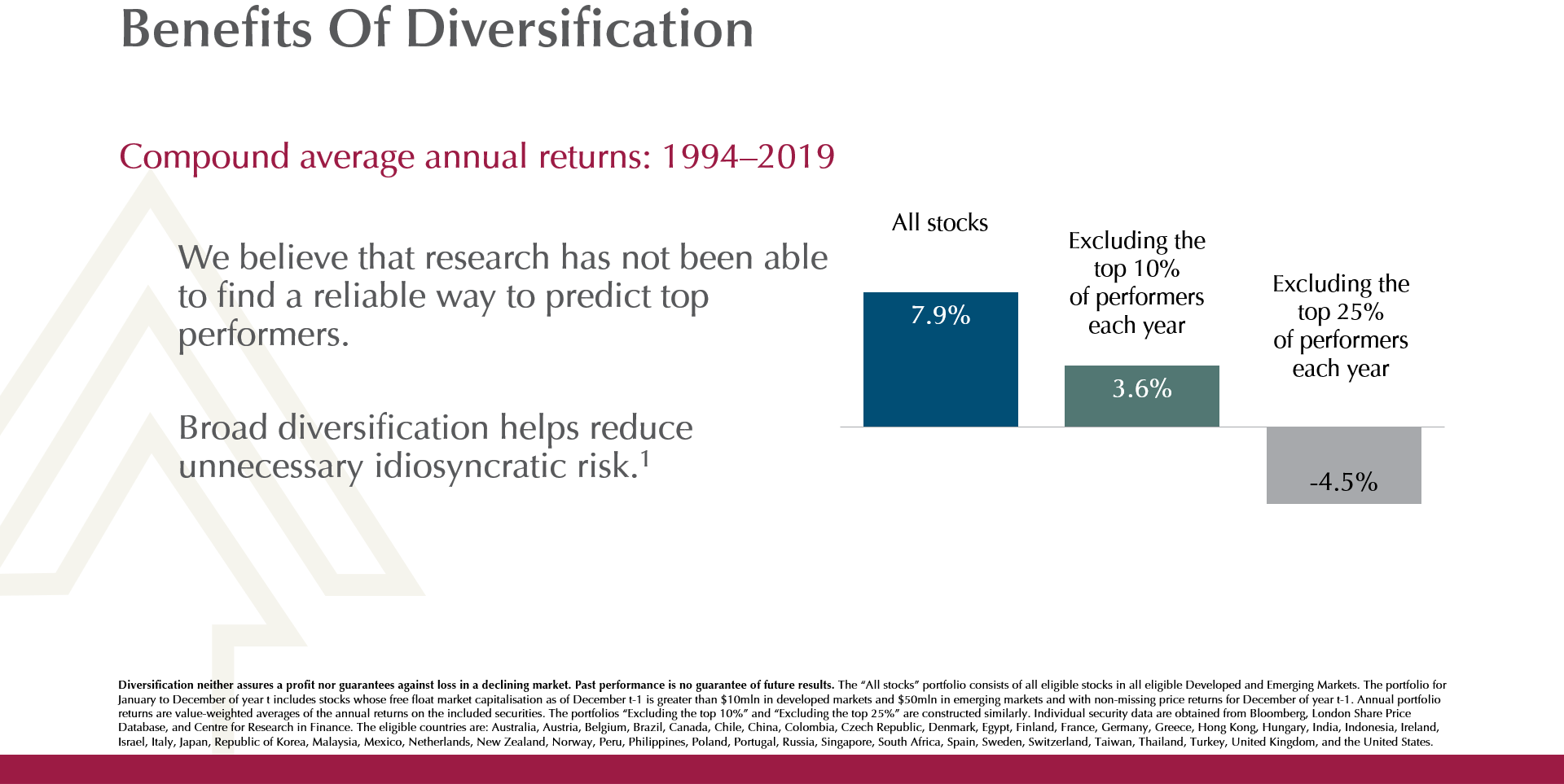

3. It is common for a few large stocks to drive market returns

It might seem like it is a new phenomenon that market returns are driven by a few large companies, yet it is actually quite a common occurrence as the data dating back to 1994 shows.

Exhibit 4: Stock returns without the top 10% of performers each year will be much lower

If you did not own the top 10% of performers, you would have a 4.3% annualised shortfall in your return from 1994 to 2019.

In fact, most stocks do not beat the market! Longboard Asset Management did a study called “The Capitalism Distribution” analysing the Russell 3000 Index from 1983 to 2006. This index follows the largest 3,000 stocks by market capitalisation in the US. The study found that while over this period, the index delivered an annualised return of 12.8% and cumulative return of 1,694% (not a typo), 39% of stocks lost money, 19% of the stocks lost 75% of their value, 64% of the stocks in the index underperformed the index, and 25% of the stocks were responsible for all the gains.

4. Expected returns are probabilistic not deterministic

While the evidence shows that risker assets are likely to deliver higher returns most of the time, it does not mean that riskier assets cannot underperform a less risky asset some of the time.

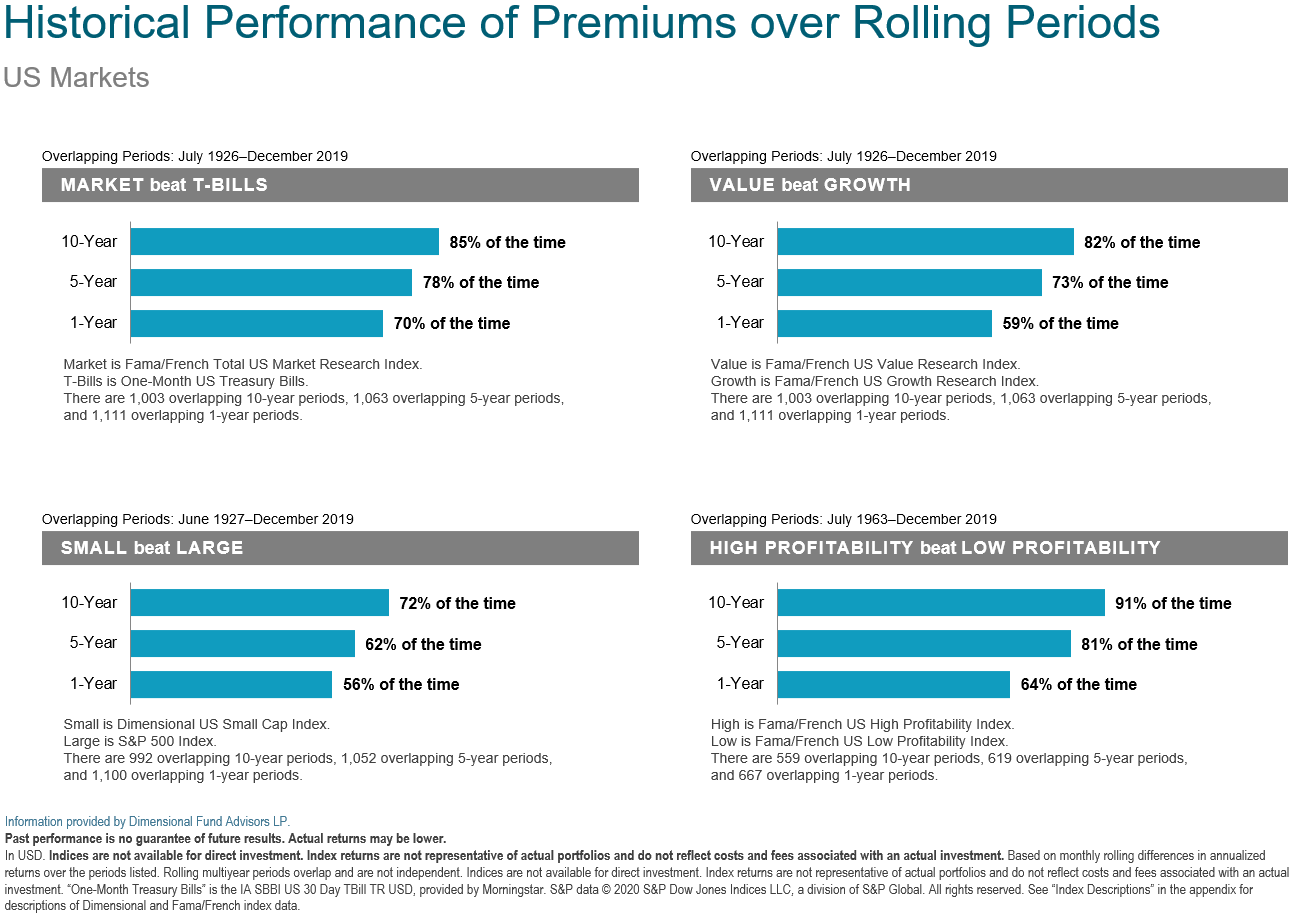

Exhibit 5: Premiums are there most, not all of the time

As we can see from the chart above, over 1-, 5- and 10-year rolling periods, risk premiums are present most, not all the time. While this data is for US stocks, stretching back to 1926, the data is similar for developed world ex US and emerging markets too.

So what should we do in 2021?

At least with regards to our investment portfolios, we would advise you to remember that you are diversified, so your portfolio is working hard to capture the risk premiums that present in the markets. You are holding as many stocks as possible, so you will have the current market leaders, and likely the future market leaders. Your portfolio has exposure to value stocks, small companies, emerging market companies to help your portfolio benefit from the various risk premiums. You are also holding an allocation to high quality fixed income to provide stability to your portfolio in times of market uncertainty.

When there is bad news and markets fall, do remember it is a natural function of price discovery in the market, and remember what is driving stock prices at the most basic level. Unless we expect cashflow to go to zero forever, we should pause and remember that after a shock, economies and businesses bounce back and adapt (just look at 2020 as an example!), and cashflows will recover.

It is also good to remember that market leaders deliver most of the returns, and that they change over different time periods, allowing a long-term investor to benefit from the changing drivers of economic growth in each time period.

Lastly, this is just one part of your wealth plan. At Providend we look at your finances beyond the investment portion and have worked out a detailed plan to help you achieve your financial goals. Do keep the plan in mind, and as always, your adviser is there for you should you have any questions or concerns.

Thank you for your continued support and trust. Wishing you a Happy New Year in 2021!

Warmest Regards,

Investment Team

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current estate plan, investment portfolio, financial and/or retirement plan, make an appointment with us today.