If you have been reading the financial news headlines you would think that stock markets had a terrible time in February. The headlines were not wrong as the typical barometers for stock market performance, the broad indexes such as the S&P 500 fell sharply in late Feb. Despite this though, the S&P 500 Index finished the month of February up 2.76%.

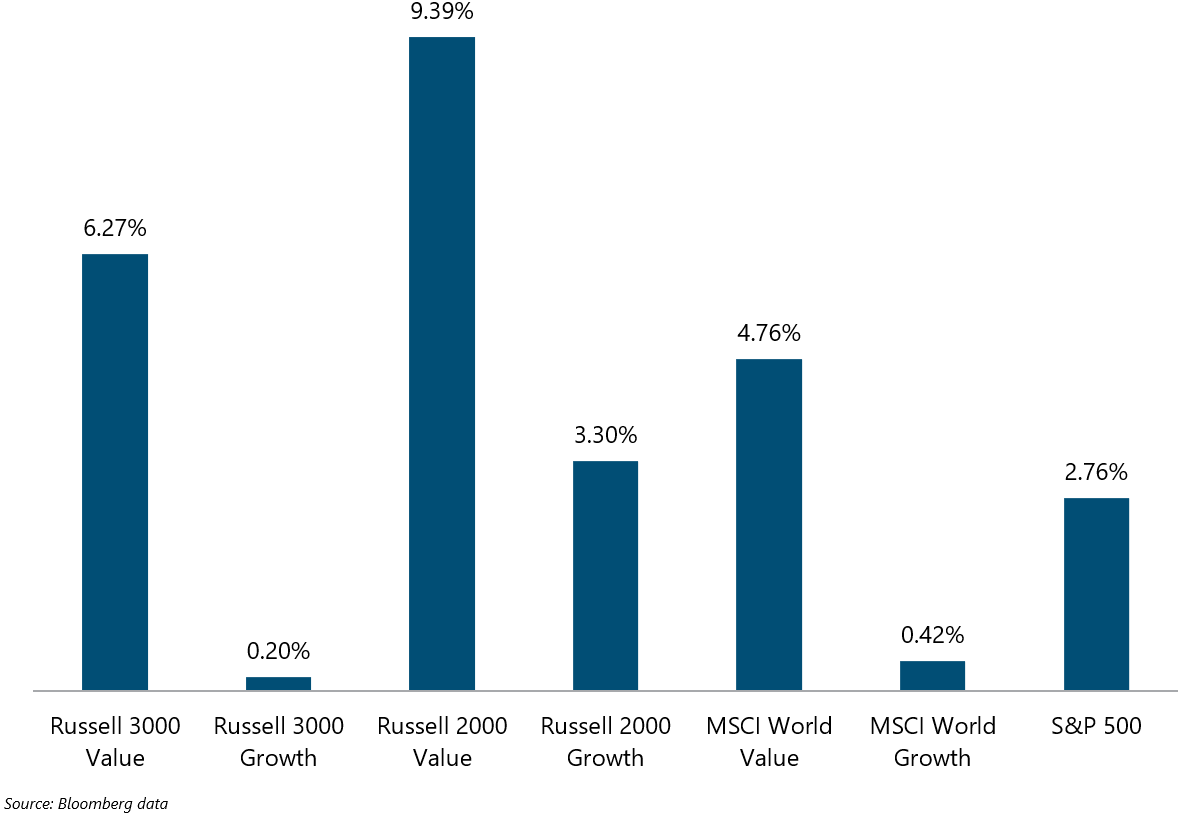

Exhibit 1: Value vs Growth vs S&P 500 Feb 2021 performance. (Total returns in USD)

The more interesting thing that happened in February is that value stocks had an excellent month vs growth stocks. If you look at the chart above, you can see that for Total market US stocks (Russell 3000), US small caps (Russell 2000) and Large global stocks (MSCI World) the value premium showed up overwhelmingly, and value stocks outperformed growth stocks by a huge margin.

This of course is not actually interesting if you look at the long-term historical context, as value stocks tend to outperform growth stocks about 80% of the time, and by around 3-4% on average. Unfortunately, value stocks had such a difficult period in the past 3 years, particularly last year, that the recovery of the value premium is something worth nothing. Along with the recovery in value, the outperformance of smaller companies continues to drive returns. The chart above also shows how much better small companies outperformed as represented by the Russell 2000 Index.

Suffice to say, our portfolios that have tilts to value and small companies would have outperformed the broad indexes in the past month.

Yields are rising, bonds are falling

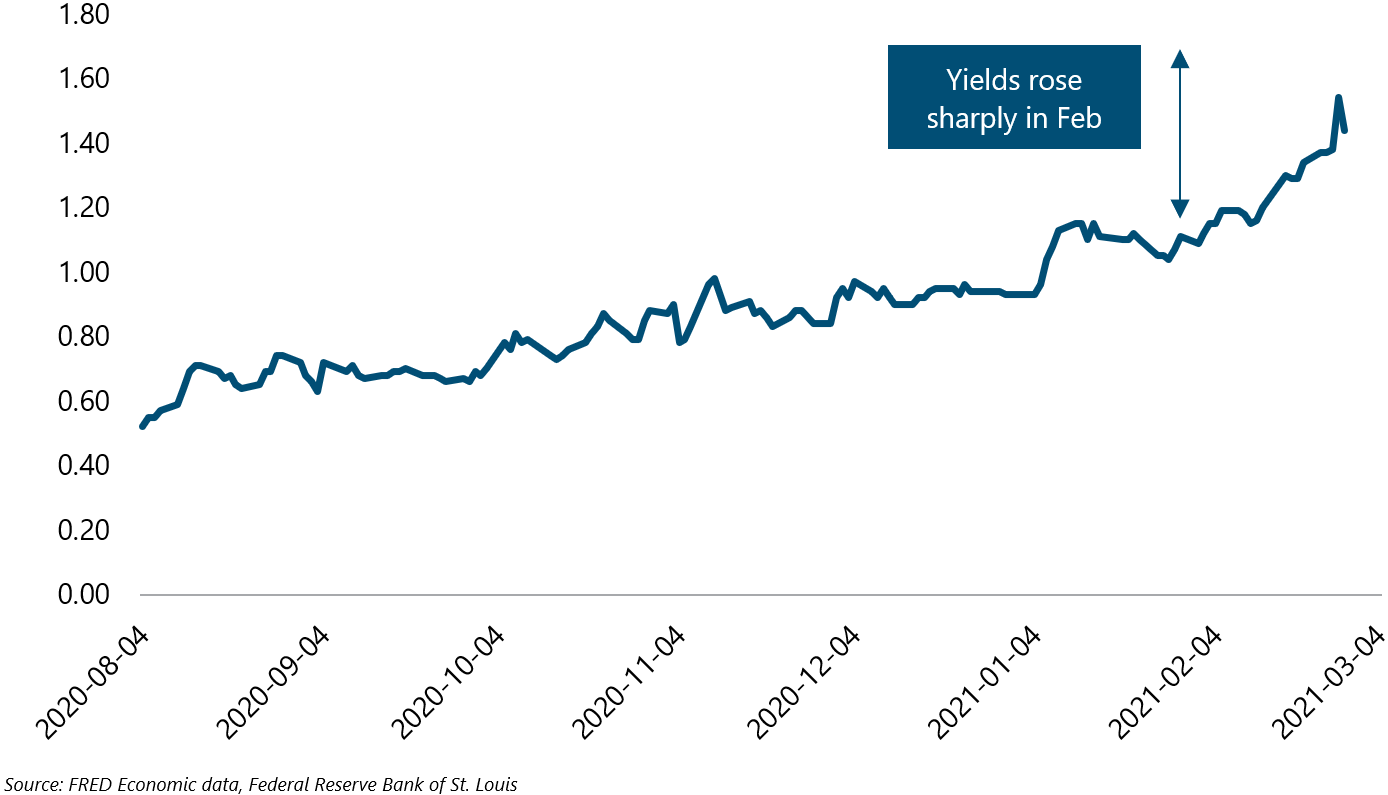

Bond yields (which move inversely to bond price) have risen sharply since the start of the year, particularly in February.

Exhibit 2: 10-year US Treasury yields

Let’s look at this in terms of how it might impact the price of a 10-year Treasury. Modified duration is the impact on a bond price for a 1% move in yield. So a duration of 9.48 (the Modified duration of the current 10-year Treasury as calculated by Bloomberg) means that for an increase/decrease in interest rates of 1%, the bond value will move 9.48% in the opposite direction. The yield went up 33bps (basis points or a hundredth of a percentage point) in Feb from 1.11 to 1.44, so the price of the 10-year Treasury would have fallen about 3.12%, which is a huge move for a risk-free bond in such a short period of time.

IEF, an ETF that tracks 7-10 year treasury returns, has fallen 3.48% so far this year, highlighting the pain for bonds so far.

Mark to market matters

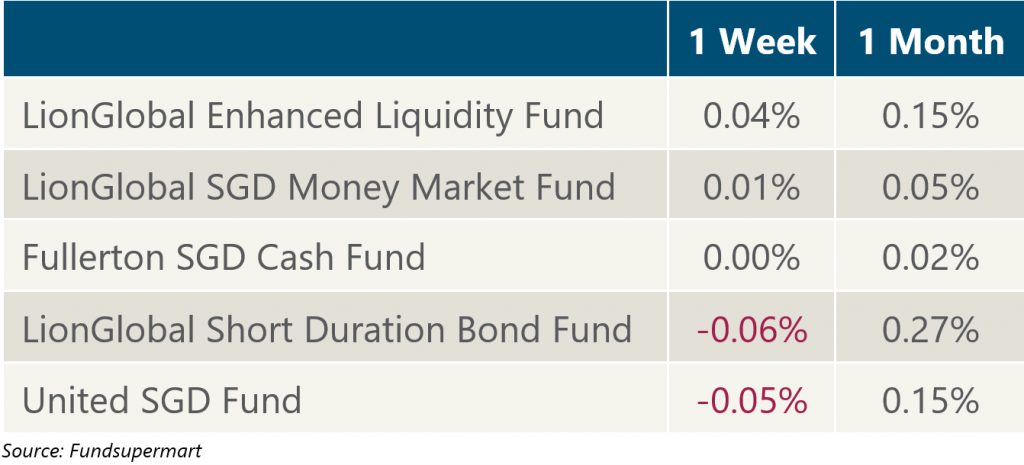

Referencing the choices we made for our cash management portfolio, we are glad to say that they made it through the last week of Feb without any drawdowns, as expected by the different way they mark their portfolios.

Exhibit 3: Cash management funds vs short-duration bond funds as of Feb 26th 2021

From the table above, you can see that even the short duration bond funds experienced mark to market losses in the last week of Feb as short bond yields also rose, while the funds we selected for our cash management portfolio did not show mark to market losses as they amortise the value of the bonds to maturity. Of course, with less risk comes lower returns, and as expected, the short-duration bond funds on average had higher returns over the month.

What do rising yields have to do with stocks?

Going back to our familiar valuation equation ![]() , where r represents the discount rate, can help us understand why growth stocks took a hit in late Feb. The price of a stock is affected by both future cashflows and the discount rate. Especially for growth companies, much of their valuation is derived from cashflows in the future, as they are expected to grow, so the P is sensitive to any increase in the discount rate or in this case the r. When the r rises so quickly as it did in late Feb, then the P has to fall. Markets were simply adjusting the prices to reflect the higher discount rate, which is a sign that the markets are working to price in the latest available information.

, where r represents the discount rate, can help us understand why growth stocks took a hit in late Feb. The price of a stock is affected by both future cashflows and the discount rate. Especially for growth companies, much of their valuation is derived from cashflows in the future, as they are expected to grow, so the P is sensitive to any increase in the discount rate or in this case the r. When the r rises so quickly as it did in late Feb, then the P has to fall. Markets were simply adjusting the prices to reflect the higher discount rate, which is a sign that the markets are working to price in the latest available information.

The good news for our portfolios is that value stocks tend to do better in such an environment as less of their valuation is dependent on high future cashflows typically, and they start off with a lower P in the first place.

There is always volatility so having a plan is important

Heading into March, we expect volatility to continue to be present, as prices continue to adjust to the changing situation around the economy. Do remember the importance of having a wealth plan and portfolios that consider the volatility around short-term market returns (such as Dec 2018 and Mar 2020). If you have any questions or concerns, please feel free to reach out to our advisers, and have a chat about recent market moves or update your wealth plan if required. Thank you for your continued trust and support.

Warmest Regards,

Investment Team

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current estate plan, investment portfolio, financial and/or retirement plan, make an appointment with us today.