July looks a little like a tale of 2 regions, with Global equities continuing their slow and steady climb to new records, while EM stocks had a tumble as changing regulations around Chinese education companies spooked international investors.

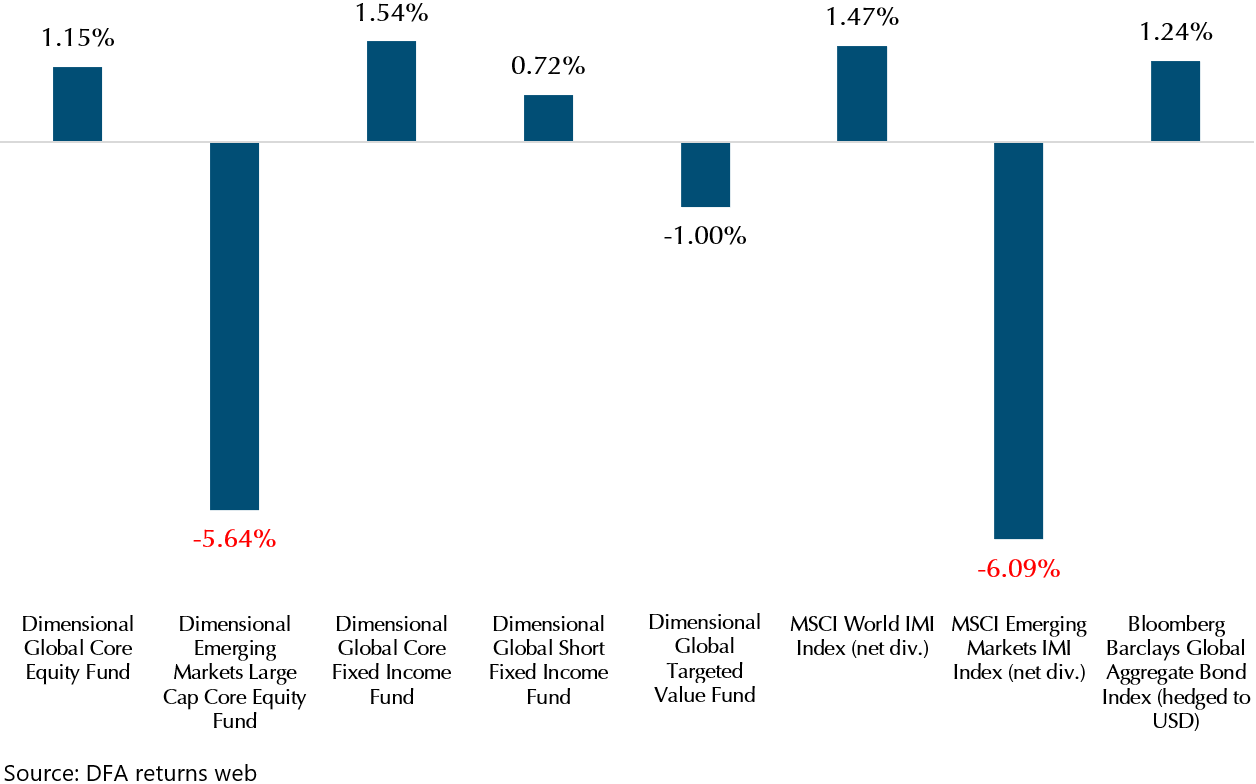

Exhibit 1: DFA funds and Providend’s reference indexes July 2021 performance in USD

Exhibit 1 highlights the stark difference between Global stocks which was up 1.47%, and Emerging Market stocks which fell 6.09%.

Small caps and value underperform

In between the two major indexes, we see that the DFA Global Targeted Value Fund fell 1%, reflecting the underperformance of smaller companies and value stocks in July. This can also be seen from the DFA Global Core Equity Fund’s slight underperformance against the MSCI World IMI.

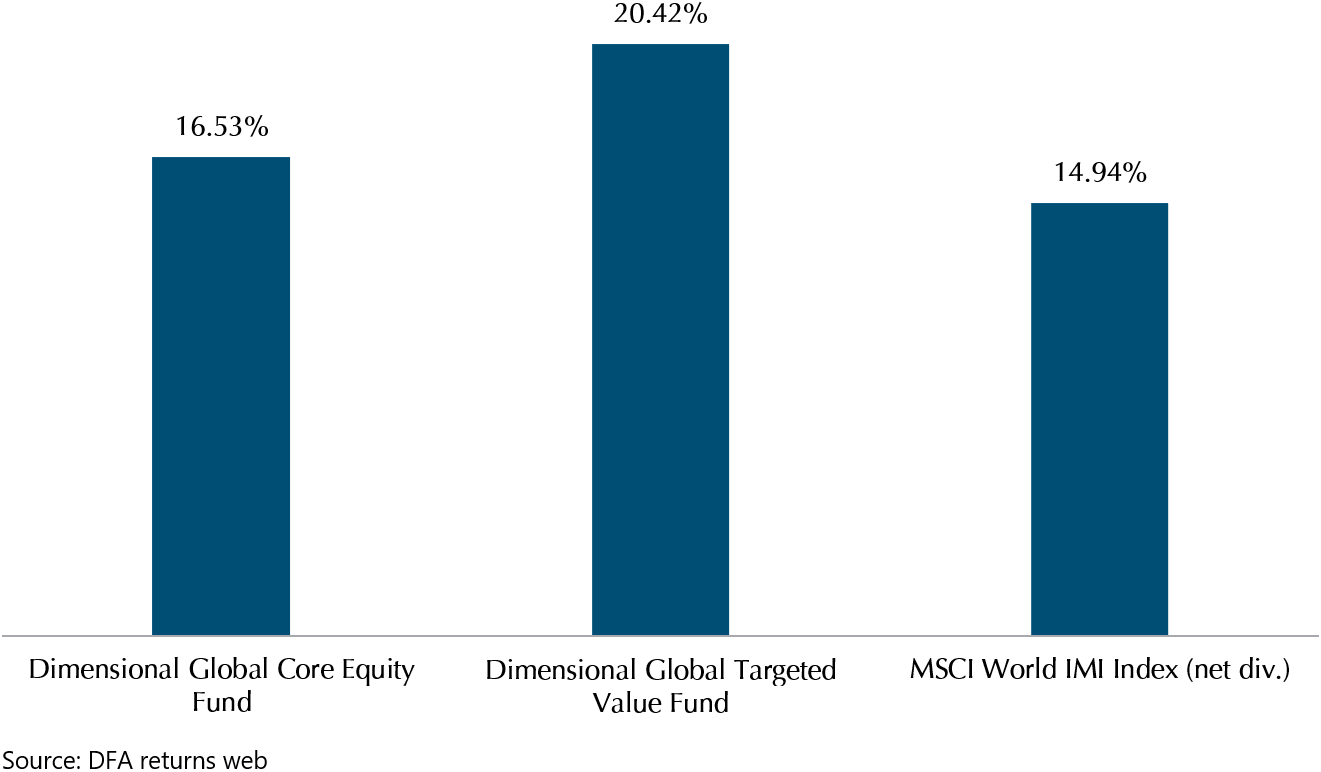

Having said that, we must understand that both returns and premiums are lumpy, and not linear. The above funds have delivered outperformance on a year-to-date basis. (See Exhibit 2)

Exhibit 2: DFA funds and MSCI World IMI YTD performance in USD

Bond yields fall

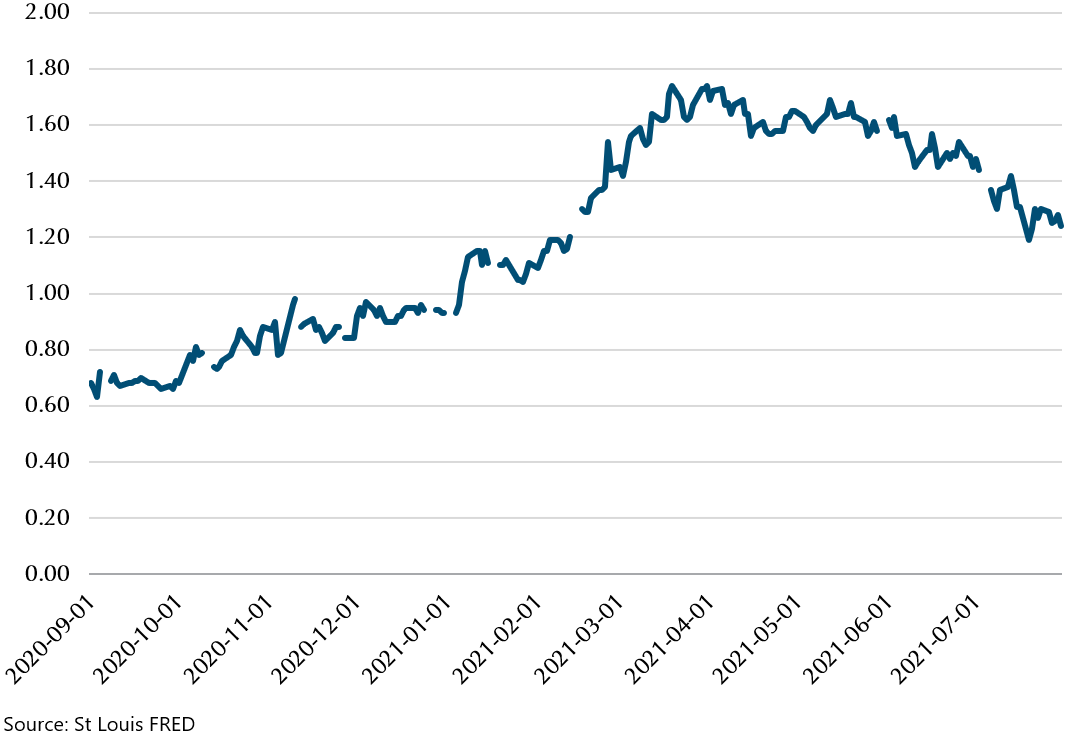

After hitting a recent peak of 1.74% in March, 10-year treasury yields have fallen to below 1.3%. This is signalling that investors are starting to expect economic growth to slow and no longer expect interest rates to rise as much as previously anticipated. (See Exhibit 3)

This has helped our intermediate fixed income allocation be the best performing in July, as the DFA Global Core Fixed Income Fund even outperformed Global stocks!

Is inflation temporary?

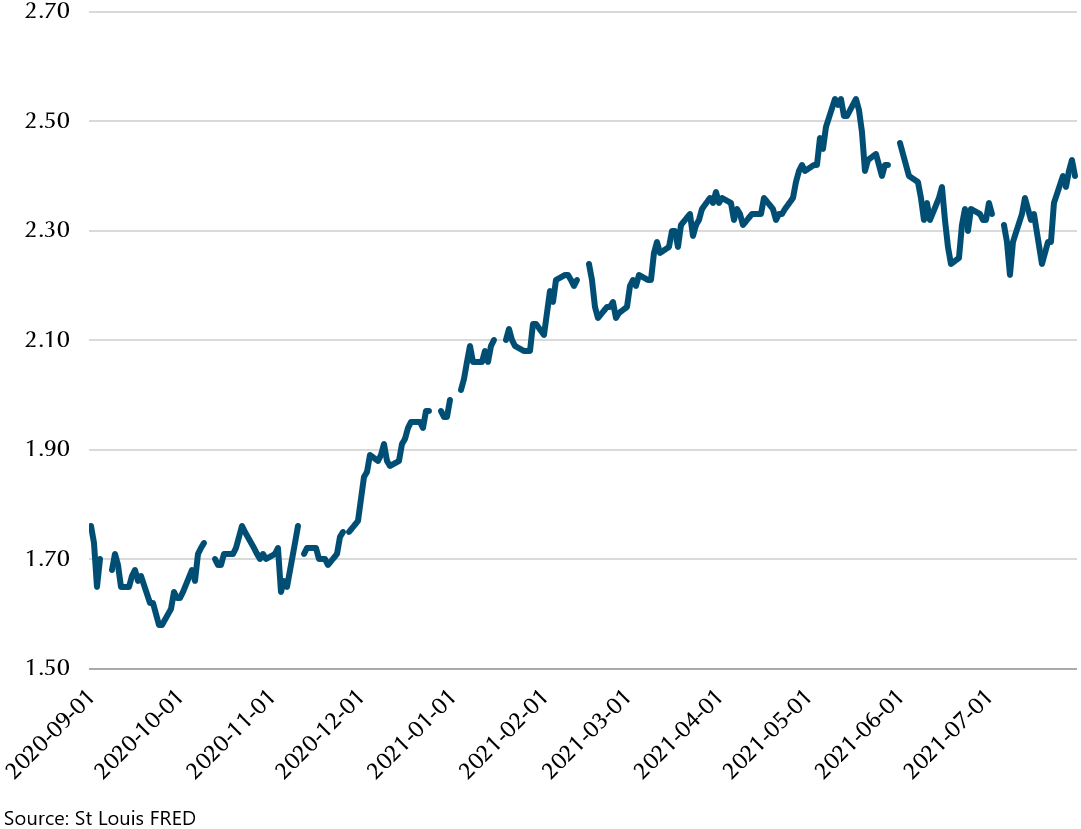

As expectations of economic growth have fallen, so have inflation expectations. The US 10-year breakeven, which is derived from the 10-year US treasury yield and the 10-year yield on US TIPS, gives an idea of what the market expects inflation to be in 10 years’ time. From hitting a high of 2.54% in May, the curve has flattened somewhat and now sits at 2.4%. (Exhibit 4) Instead of runaway inflation, the market is pricing in a slightly more muted outcome, and might be signalling that the price increases we are seeing are a temporary phenomenon as the world deals with the supply shortages due to the ongoing COVID-19 pandemic.

Exhibit 3: 10-Year US Treasury Yield, Constant Maturity

Exhibit 4: 10-Year Breakeven Inflation rate

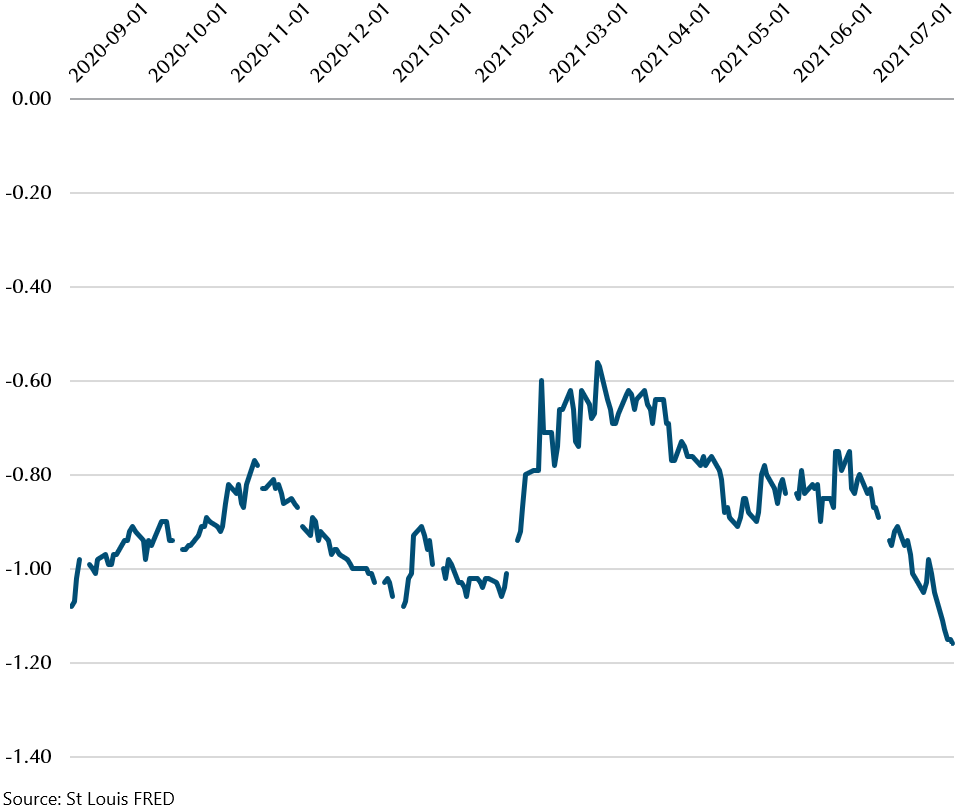

Real yields fall even more

With inflation expectations moderating, but not falling by much, and nominal yields falling sharply, we have a situation where real yields have fallen deeper into negative territory. At -1.16%, what it means is that if inflation expectations are accurate, the real (nominal – inflation) return on holding a 10-year treasury is -1.16%.

As we can see from Exhibit 5 below, the real yield has been negative for some time, but while the reason for it last year was low rates from monetary policy, earlier this year, the real rate fell as inflation expectations rose, but pulled back as nominal yields rose in tandem. This past month, we have seen inflation expectations stay constant while nominal yields fall, resulting in where we are now.

Exhibit 5: 10-Year Treasury Inflation-Indexed Security, Constant Maturity

Trying to make sense of it all

It appears that either inflation expectations are wrong, market expectations on growth are wrong, or maybe we might be going into a period of stagflation in the future. Typically, inflation in associated with economic growth, as increased demand for goods and services is constrained by limited supply of labour and raw materials, driving prices up. Or could the US economy be heading the way of Japan and getting stuck in a low growth and low rate environment for a long while? Although this would mean inflation expectations are very wrong as Japan has hardly had any inflation in a long time. Maybe the loose monetary policy has finally caught up with us and we are experiencing inflation due to excessive central bank asset purchases, alongside low growth (the stagflation scenario that was worried about a lot in the 2010’s but never happened).

Right now, it is far too early to tell what will happen. It is barely 6 months of data, and a lot of uncertainty alongside it. The path out of the pandemic is still not certain with the unknowns around the Delta variant of COVID-19, and a resurgence of the pandemic could derail economic growth. Or we could see economic growth power ahead with the US looking likely to pass an infrastructure spending bill, which would see further fiscal stimulus support the economy. It is not surprising then, that even market analysts and commentators are split on what is coming next, with some seeing inflation as temporary, and some seeing inflation here to stay as economic growth remains robust.

Markets are always adjusting to new information

The point we are trying to make is that information is changing constantly, and prices are moving when the market is trying to adjust and price in the new information. What serves us well is staying diversified and benefiting from investing in asset classes that deliver a long-term return. An inflationary environment will benefit value and small stocks, while slower growth is likely to benefit growth stocks (yes we have growth stocks in our portfolio too) and should yields fall further, our positions in bonds will benefit (as it happened this month). Instead of trying to figure out what might happen next, (as if we get it wrong, we will miss out on all the returns) our diversified portfolio allows us to participate in the returns from various scenarios.

A challenging period for EM

Emerging Market stocks got a shock late in July, when China’s regulators decided that tutoring companies could only conduct their core business on a non-profit basis. They also announced that education companies would not be able to use the VIE (Variable Interest Entity) structure that has been a way for international investors to invest in companies that are typically not able to sell shares to foreign investors.

Apart from the education firms, tech companies are also using this structure, and the uncertainty around it has led to many international investors selling down their positions in the tech firms also. This has an impact on the index as Tencent, Alibaba and Meituan make up 10.5% of the MSCI Emerging Markets IMI Index, and sharp falls in those stocks has pulled the MSCI EM Index down. China is the largest geographical allocation in the index, with a weight of 34.3%.

We expect further volatility for EM stocks ahead as the uncertainty around the situation resolves, but we continue to maintain our allocation to EM stocks inline with the reference MSCI All Country World IMI Index of about 10% of our portfolios.

Conclusion

Our portfolios still delivered a positive return for the month as fixed income and the overall return from Global equities helped to make up for the fall in EM stocks and small/value stocks. Do contact your adviser if you would like a more in-depth discussion about portfolio performance.

We look forward to some easing of restrictions in August as more people get vaccinated and hope to be able to meet face to face with our clients in the coming weeks. Stay healthy, and we would like to wish all our Singaporean clients a very Happy National Day!

Warmest Regards,

Investment Team

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current estate plan, investment portfolio, financial and/or retirement plan, make an appointment with us today.