The summer months are typically a little less exciting in the markets as liquidity dries up. However, the lower liquidity can make for more volatile trading as market participants find it harder to match bid and offers.

Overall, we managed to capture positive performance for the month, but as we can see from Exhibit 1 below, our Index Plus portfolios would have underperformed the broad market.

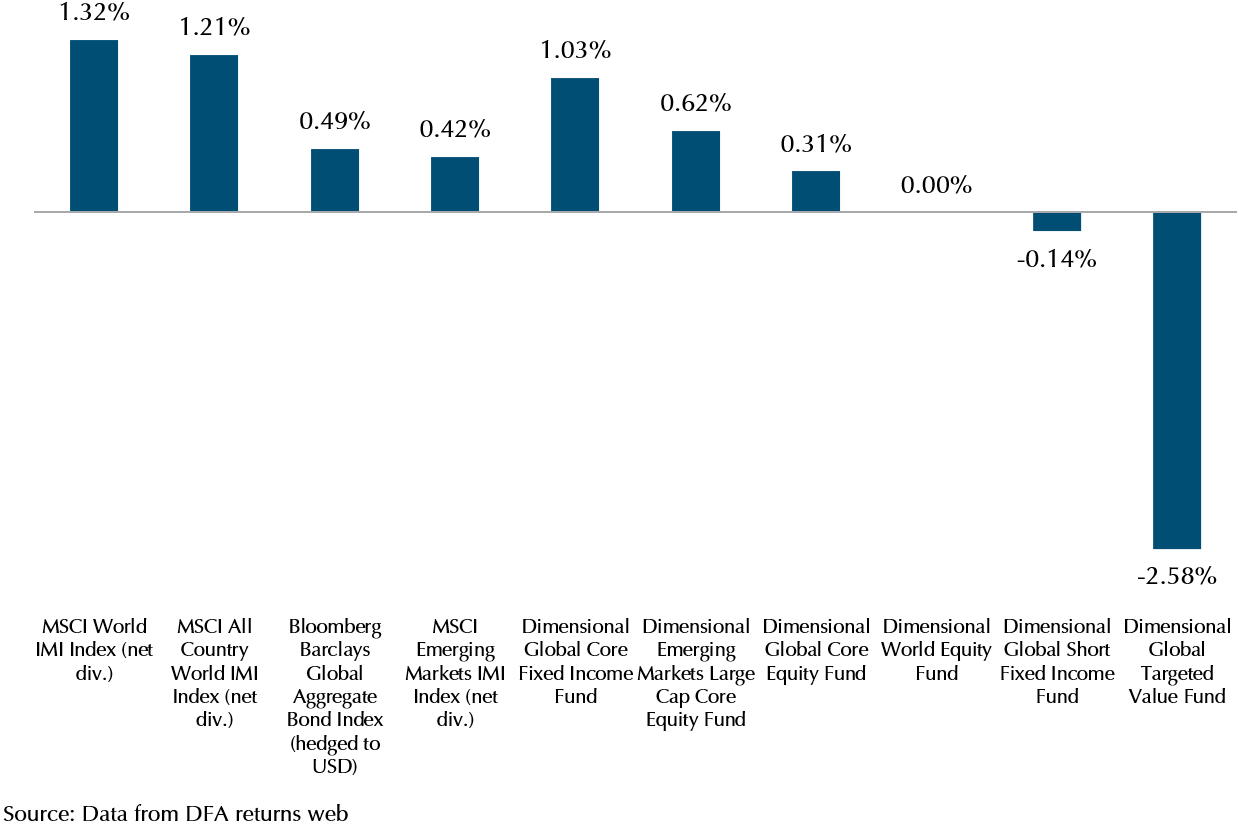

Exhibit 1: Returns in June – USD

Small caps and value stocks take a breather

After 6 months of outperformance, small caps and value took a back seat to large growth stocks over the month of June. The MSCI World IMI Index returned 1.32% far outperforming the DFA Global Core Equity Fund which returned 0.31%. The pure expression of small caps and value stocks that is the Targeted Value Fund fell 2.58% over June.

Ironically, the DFA Emerging Markets Large Cap Fund (+0.62%), which does not have small cap stocks in it, outperformed the MSCI EM IMI Index (+0.42%) which has small caps in it.

Intermediate bonds bounce back

The past 6 months have not been kind to fixed income, with inflation fears and higher than expected economic growth pushing the 10-year yield to a high of 1.75% at one point. June saw yields pull back and this has allowed the intermediate bonds to recover some ground. The DFA Global Core Fixed Income Fund has fallen 1.84% YTD, but June saw it return 1.03%, outperforming the Barclays Global Aggregate Index which returned 0.49%.

Forward looking markets

Economic growth is rebounding at high levels in the developed world, and inflation prints are all coming in higher as economies reopen more fully, so why is the 10-year yield suddenly falling? As of the timing of this note, the yield has fallen to 1.35%, quite far from the lofty heights of 1.75% in March.

We would like to highlight a few key points that might be reasons why the market is reassessing its economic optimism.

- Fiscal spending has slowed in the US. The earlier optimism came from the passing of the large Covid pandemic relief bill after the Democrats won both the House and the Senate. Since then, the Biden administration plans for the infrastructure bill have stalled somewhat, and negotiations are taking longer than previously expected. This has pared back the expectations that the economic rebound would be further fuelled by heavy fiscal spending, leading to even larger inflationary pressures.

- Easy monetary policy expectations are also pared back. At its latest meeting, the Fed signalled that it might start to raise rates in 2023, earlier than previously indicated. This has helped reign in the fears that the Fed would act too slow to control inflation or to cool an overheating economy, and thus the markets are also repricing their expectations on economic growth.

This provides a good example of how prices change as information changes, and how the markets are constantly trying to price in the new information that comes along. This is not to say that the markets are right, as information is imperfect. It just means that current prices reflect the best estimation for the value of an asset with the available information.

Avoid reacting to the short-term news

If the current market view is right, and that economic growth is slowing, it might also mean that value stocks and small stocks might once again not do so well. However, we would like to caution against reacting too pessimistically to the possibility.

We have just come off an almost 10-year period of underperformance for value (that ended in September last year). From the data, when the premium shows up again, it typically stays for a while.

Exhibit 2: Value minus growth, US markets

As the chart above, typically after a period of underperformance, if the premium returns it does appear it stays for a while. Of course, we have no way of knowing if this will be the case in our current situation, but it would be hasty to react to just a few recent data points.

After all, this could be just a short-term pause in rising yields and more data in the future will either show economic growth picking up and inflation rising leading to the market once again adjusting its expectations.

Remember how long-term returns are derived

Returns on financial assets do not appear out of thin air. They are the result of the economic contribution of businesses all around the world that continue to develop products and services demanded by consumers. As the economic recovery progresses across the world, companies will generate cashflow, delivering returns to their shareholders.

With this in mind, we can focus on staying invested long term even if the short-term news might not be as favourable.

Stay calm and keep invested

2021 has been exceptional so far as markets have started strong and not looked back. As we head into summer proper, lower liquidity might cause markets to be more volatile. Negative newsflow such as Covid-19 variants causing economic reopening setbacks or worse than expected data on the economic recovery might play a part in adding to volatility. On the flip side, we might also have another year similar to 2017 or 2019 where the market delivered strong returns over almost the entire year. In either scenario, we encourage clients to keep their long-term wealth goals in mind and make adjustments as required by the wealth plan and not market gyrations.

Stay safe and healthy as Singapore moves to get back to normal. Thank you for your continued trust and support.

Warmest Regards,

Investment Team

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current estate plan, investment portfolio, financial and/or retirement plan, make an appointment with us today.