October was a prime example of the uncertainty facing investors in 2020. On one hand, we have improving economic data reviving hopes that a deep recession will be avoided, sending stocks higher initially. Yet a resurgence of the COVID-19 pandemic in Europe and the US led to fears that economies will be forced back into lockdown and sent stocks lower towards the end of the month.

Market Observations over the month of October

This month we would like to share some observations about risk premiums, to highlight how we focus on diversification in our portfolio construction, and to also help our clients better understand what drives the returns in their portfolios.

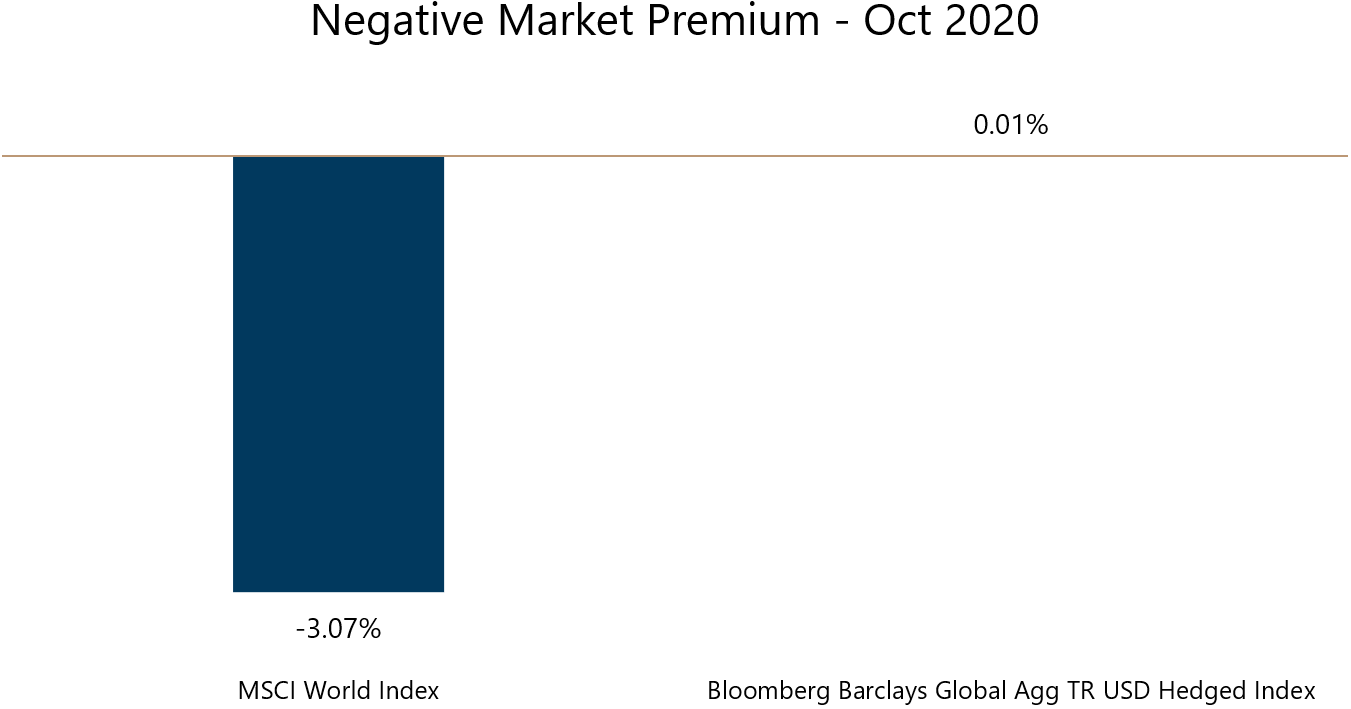

No Market Premium

Exhibit 1:

The Market or Equity Premium is the excess return of stocks over bonds. From Exhibit 1, we can see that MSCI World Index which represents Global developed world stocks, fell 3.07% in October, while the Bloomberg Barclays Global Aggregate Index which represents Global bonds, was up 0.01%. This is an outperformance of 3.08% for bonds vs stocks, which is a negative market premium as typically, stocks are expected to outperform bonds.

Of course, in the long term, the data shows that stocks do outperform bonds (because stocks are riskier, and therefore require a higher expected return), but there can be periods where stocks fall and bonds rise. This negative correlation is why we have allocations to bonds in portfolios that are designed to take less risk, for clients that are unwilling or unsuited to hold a portfolio of 100% equities. This diversification between bonds and stocks helps to reduce the volatility of portfolios that hold bonds as it reduces the drawdown in periods where stocks fall.

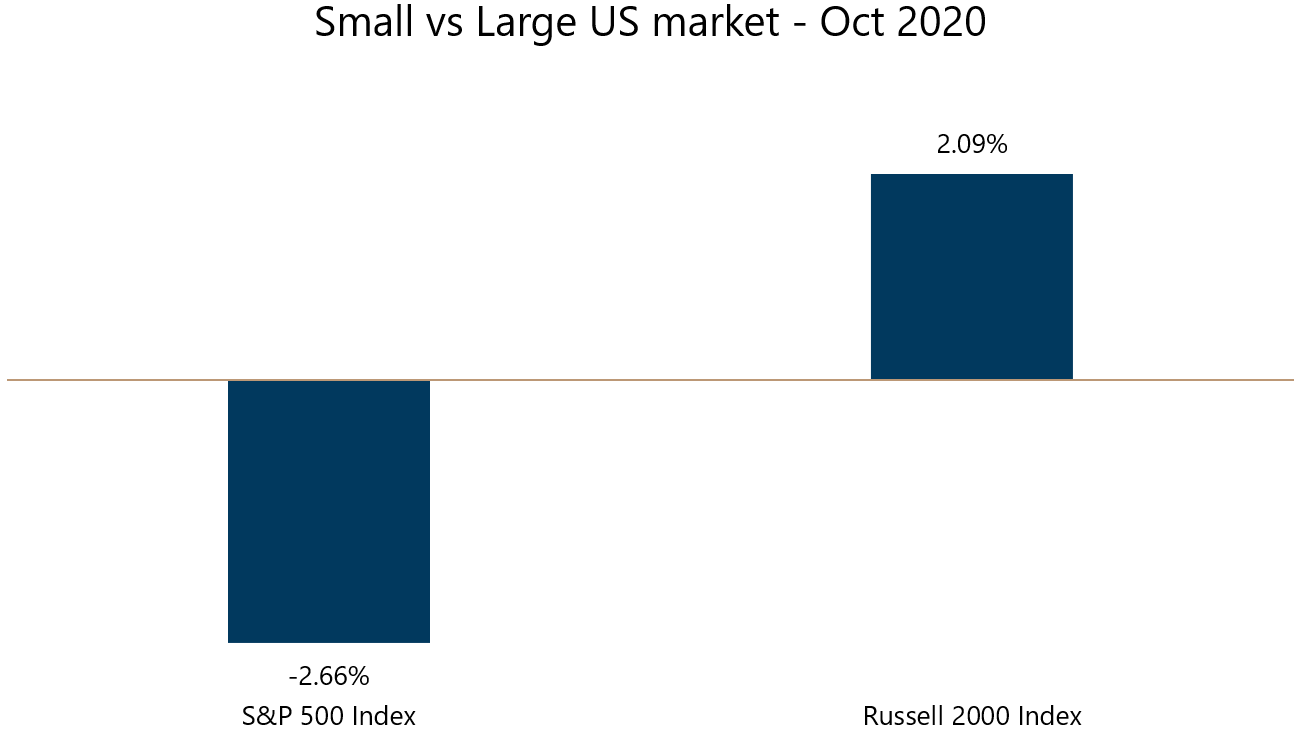

The US market had a small cap premium

Exhibit 2:

Smaller companies are riskier investments than larger companies. This is because there is less certainty around their business model, their cashflow and their cost of financing is higher. For the risk, investors would demand (expect) a higher return, so the expected return of smaller companies is higher than larger ones. This is the small cap premium.

The S&P 500 represents the largest 500 companies in the US market, while the Russell 2000 represents the smallest 2000 companies in the US market. In October, the improving economic outlook for the US (prior to the 2nd wave hitting) helped small companies outperform the large companies, capturing a 4.75% small cap premium.

Aside from diversification of asset classes, within an asset class, we also diversify the premiums we target in our portfolios. Implemented via Dimensional’s equity strategies, our portfolios captured the small cap premium this month to outperform the broader market.

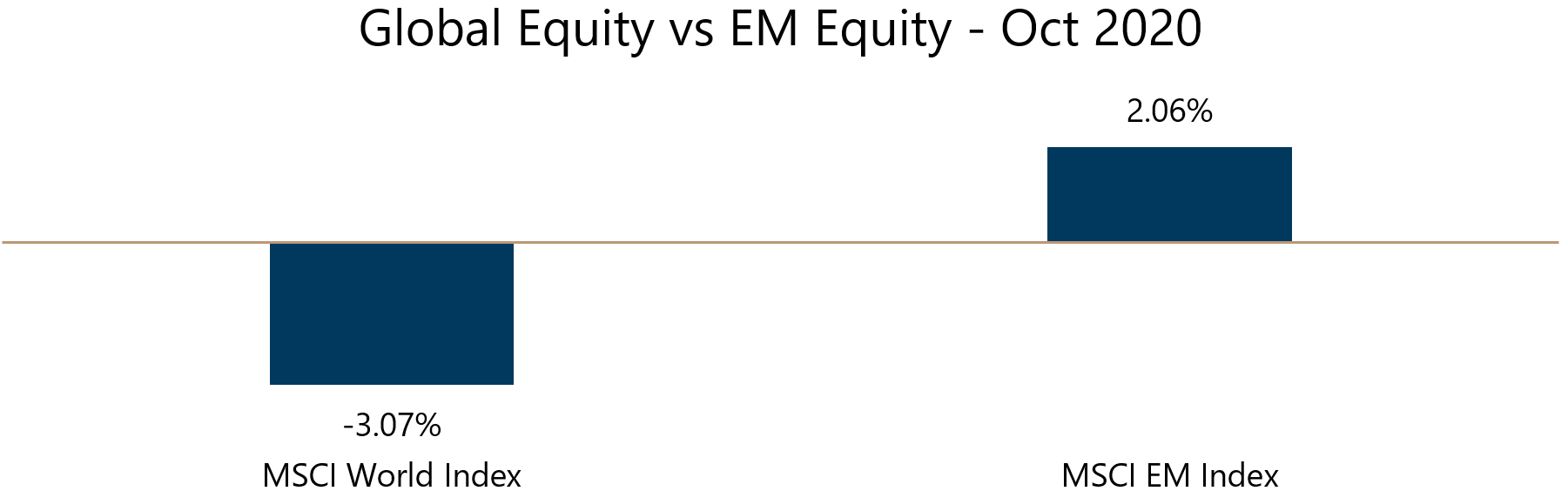

Emerging Markets outperform

Exhibit 3:

Emerging Market (EM) stocks in the past 10 years have returned much less than Global stocks, leading to many questioning asset allocation decisions that keep Emerging Markets in portfolios. While it is true that the past 10 years the performance has been lacklustre, the higher risk and lower liquidity (coupled with faster economic growth) do mean that expected returns from Emerging Markets are higher than from Global Equities. The risk is reflected in the higher standard deviation of the asset class.

We allocate to Emerging Markets prudently, keeping it at or below 12.5% of the equity weight in the portfolio to minimise the impact of the volatility on the portfolio. Yet there have been periods of strong EM equity outperformance such as in 2009 (+78%) and 2017 (+37%) that contribute to portfolio returns.

In this case, our allocation to Emerging Market stocks has helped to mitigate the fall in Global stocks this past month.

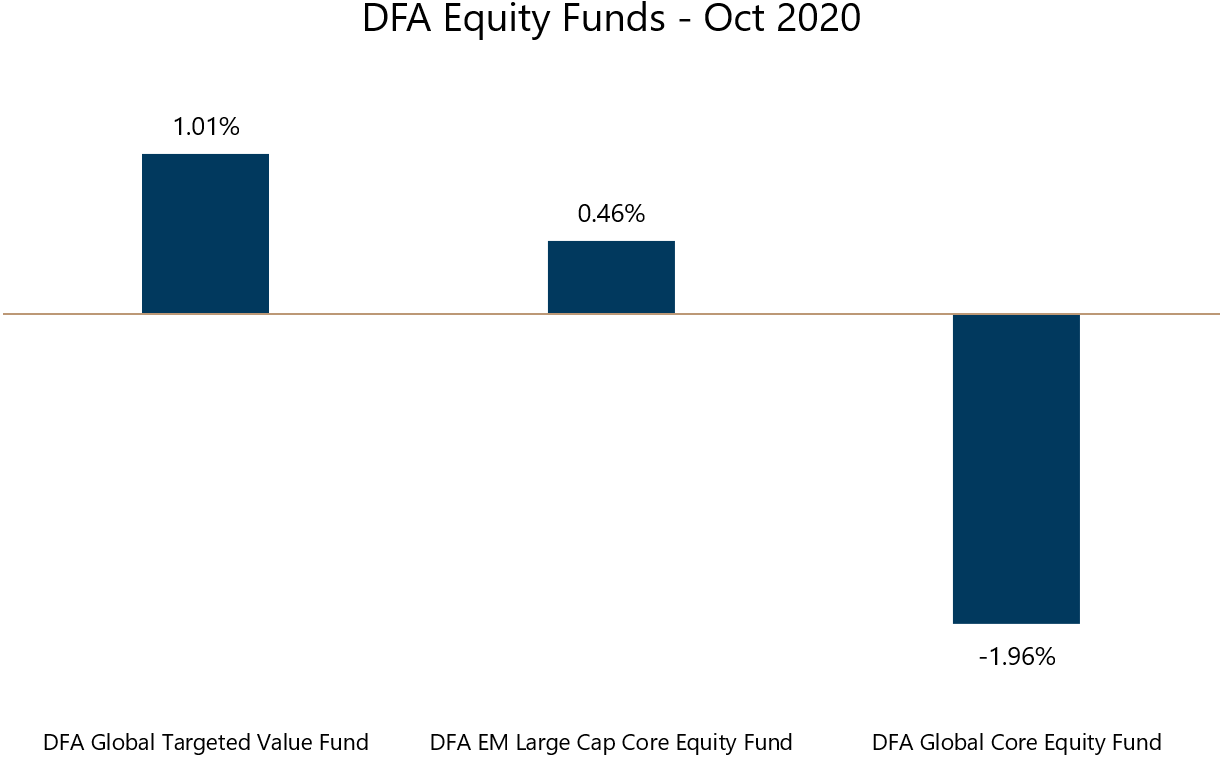

Dimensional Funds did better than the large growth indexes

Exhibit 4:

Targeting the Small Cap premium helped to mitigate the impact of the fall in Large Growth stocks over the month of October. Unfortunately, the Value premium is still not present, resulting in less than hoped for performance in the Targeted Value and EM fund. Despite that, the 2 funds had positive returns, and the Global Core Equity fund fell less than the MSCI World or the S&P 500.

Overall, this highlights how diversification in equities across various factors and geographies helps to diversify the return profile of the portfolio. Our portfolio returns don’t just come from developed world large growth stocks, but come from smaller companies, and also from Emerging Market stocks.

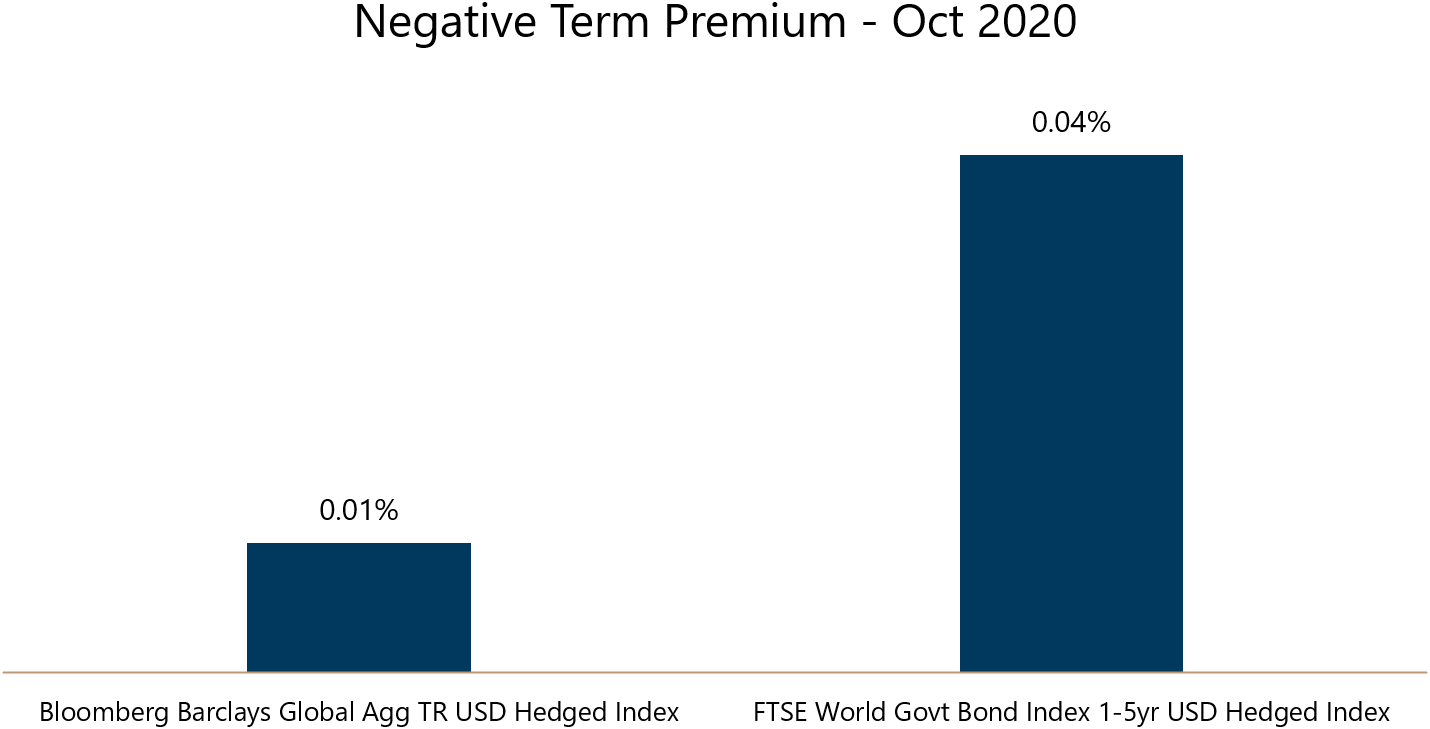

Short term bonds outperformed

Exhibit 5:

Bonds with longer duration should have higher expected returns. Extending a loan for a longer period results in more uncertainty around the borrower’s ability to repay, so the issuer will demand a higher return for the loan. This is the term premium. In October, we can see that intermediate bonds (5-15 yrs maturity) as represented by the Bloomberg Barclays Global Aggregate underperformed short term bonds (<5yrs maturity) as represented by the FTSE World Govt Bond Index. Rising 10-year yields caused bond prices to fall, while short term bonds were steadier for the month.

Our mix of intermediate and short-term bonds allowed the fixed income portion of the portfolios to stabilise the portfolio performance in Oct.

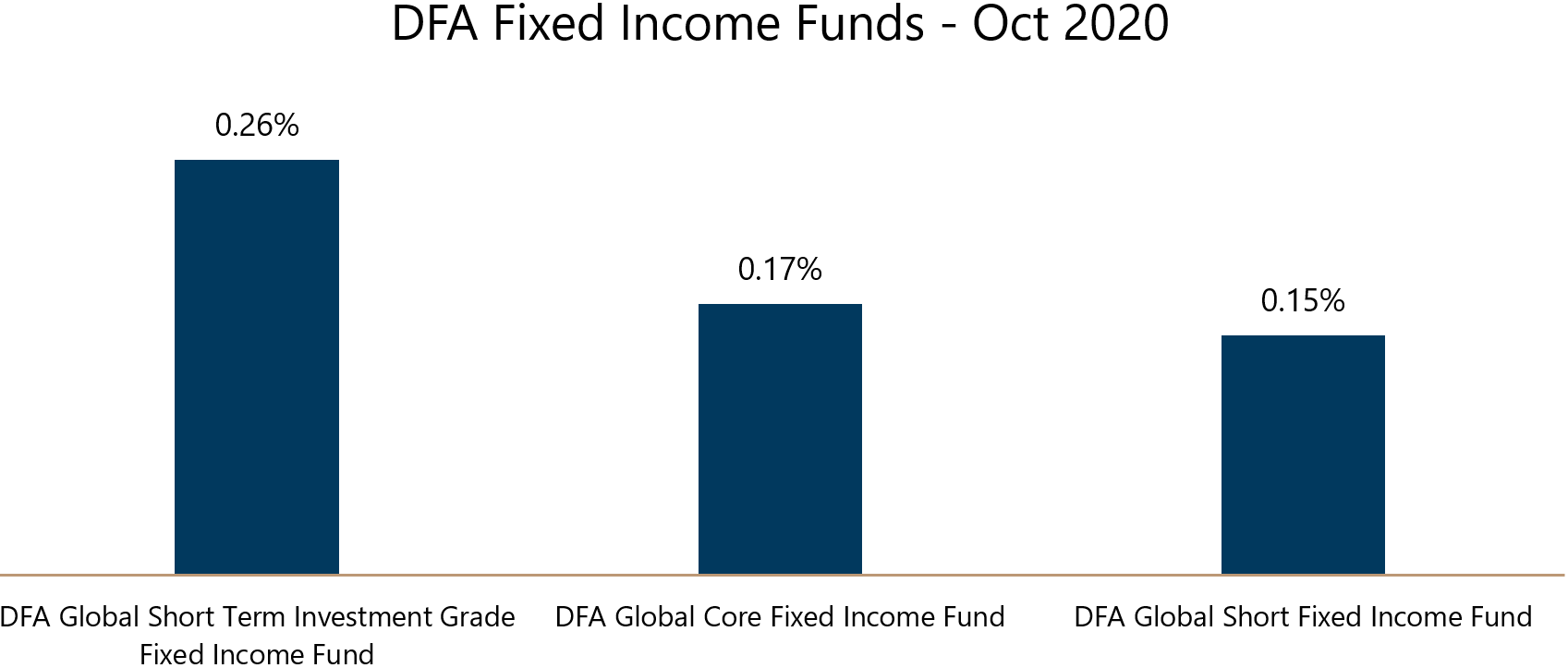

DFA fixed income outperformed because of the credit premium

Exhibit 6:

Fixed income is not just about the term premium though. The return for lending to a non risk-free borrower (Corporate or non-government) is the credit premium. In October, we can see that the credit premium delivered higher returns, as the DFA Global Short Term Investment Grade Fixed Income Fund, a fund that specifically targets the credit premium in short term bonds, outperformed both the Global Core Fixed Income Fund and the Global Short Fixed Income Fund.

The Global Core Fixed Income and the Global Short Fixed Income both outperformed their respective benchmarks (the Bloomberg Barclays Global Agg and the FTSE World Govt bond 1-5 respectively) as they also have some parts of their portfolios targeting the credit premium.

This diversification of fixed income premiums has allowed the fixed income portion of the portfolio to deliver a better than market return in October.

In the face of uncertainty, stay diversified!

Coming up to November, we are again looking at an extended period of uncertainty. There is one of the most important US Presidential elections in history that will take place on 3rd Nov, (nobody dares to predict the outcome after what happened the last round), where the outcome is uncertain. What we do know from history though, is that regardless of which party is in the White House, the stock markets have typically trended higher. (You can approach your Adviser for the data if you wish to see it).

We are also looking at a 2nd wave of the COVID-19 pandemic, with the major economies of Europe looking at lockdowns, and rising cases in the US likely to slow the economic rebound. While we cannot know the market reaction to the 2nd wave (before it happens), we can focus on the things that we do know.

Remember that you have a financial plan, meticulously planned out with your adviser and that you have defined your risk tolerances for investing. Focus on the fact that your portfolio is not 100% in stocks, (unless your risk tolerance allows for it), and that there is a fixed income allocation that preserves value and generates some return when stocks might be falling. We also hope that this article highlighting the diversification in your portfolio will help you realise that your portfolio is not just dependent on one asset class or geography or factor to deliver returns but is diversified across many different geographies and factors.

We hope you continue to stay healthy and safe as we head into the last 2 months of the year. Thank you for your continued trust and support.

Warmest Regards,

Investment Team

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current estate plan, investment portfolio, financial and/or retirement plan, make an appointment with us today.