After a terrible June, stock markets rebounded strongly in July as investors found some relief from earnings that were not as bad as expected and a Fed that did not pull any surprises with a 75-basis point (0.75%) rate hike.

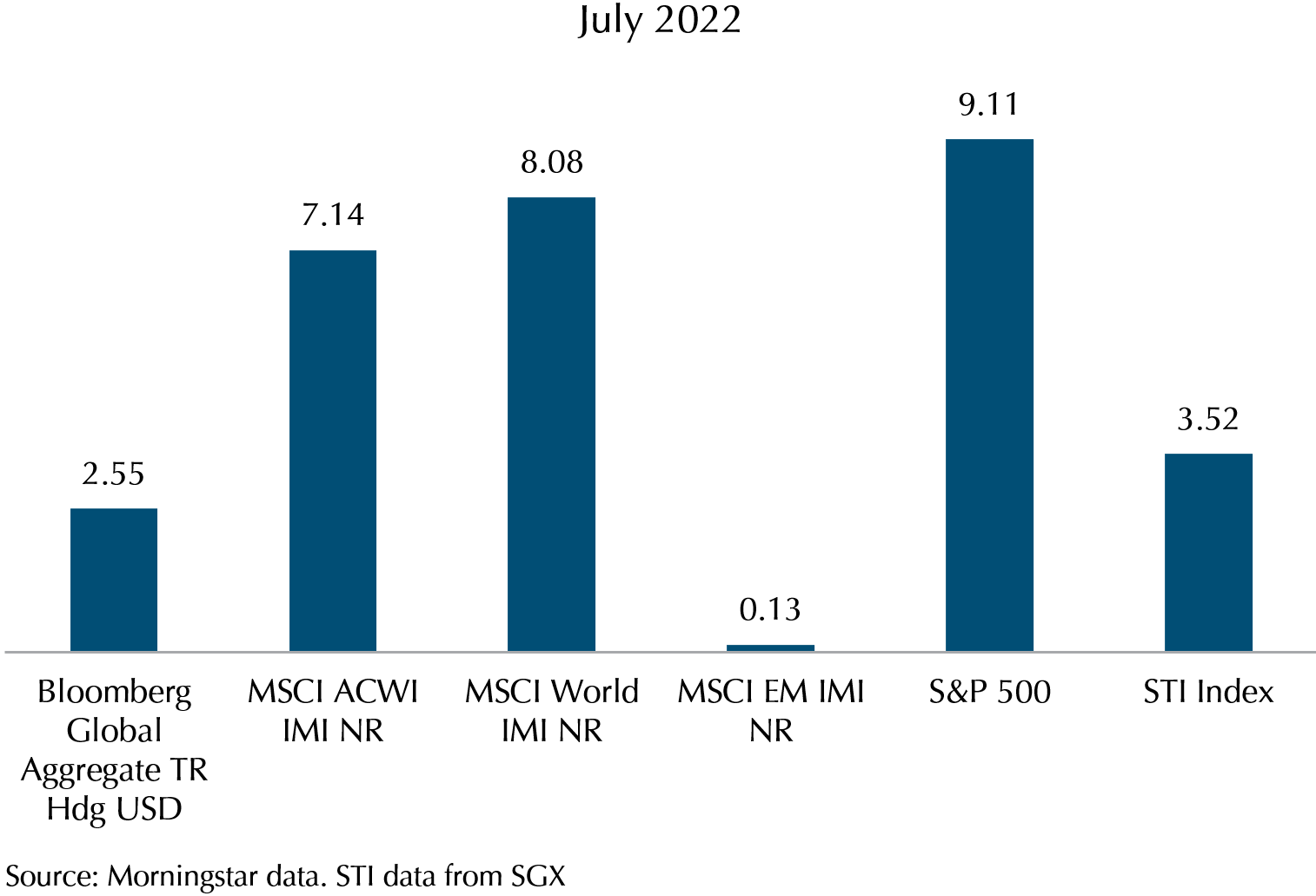

Looking at the data from Exhibit 1 below, we can see that developed markets had a strong month, led by US stocks with the S&P 500 up 9.11%. Emerging markets did not do so well (represented by the MSCI EM IMI) and are barely up 0.13%. This led to the composite MSCI AC World IMI which has both developed and emerging market stocks to underperform the S&P 500, up 7.14% for the month. Global bonds did well too, up 2.55% in the month. The STI index was up 3.52% (in SGD), a far more muted rally as compared to the developed market stocks.

Exhibit 1: Index performance in USD (SGD for STI index)

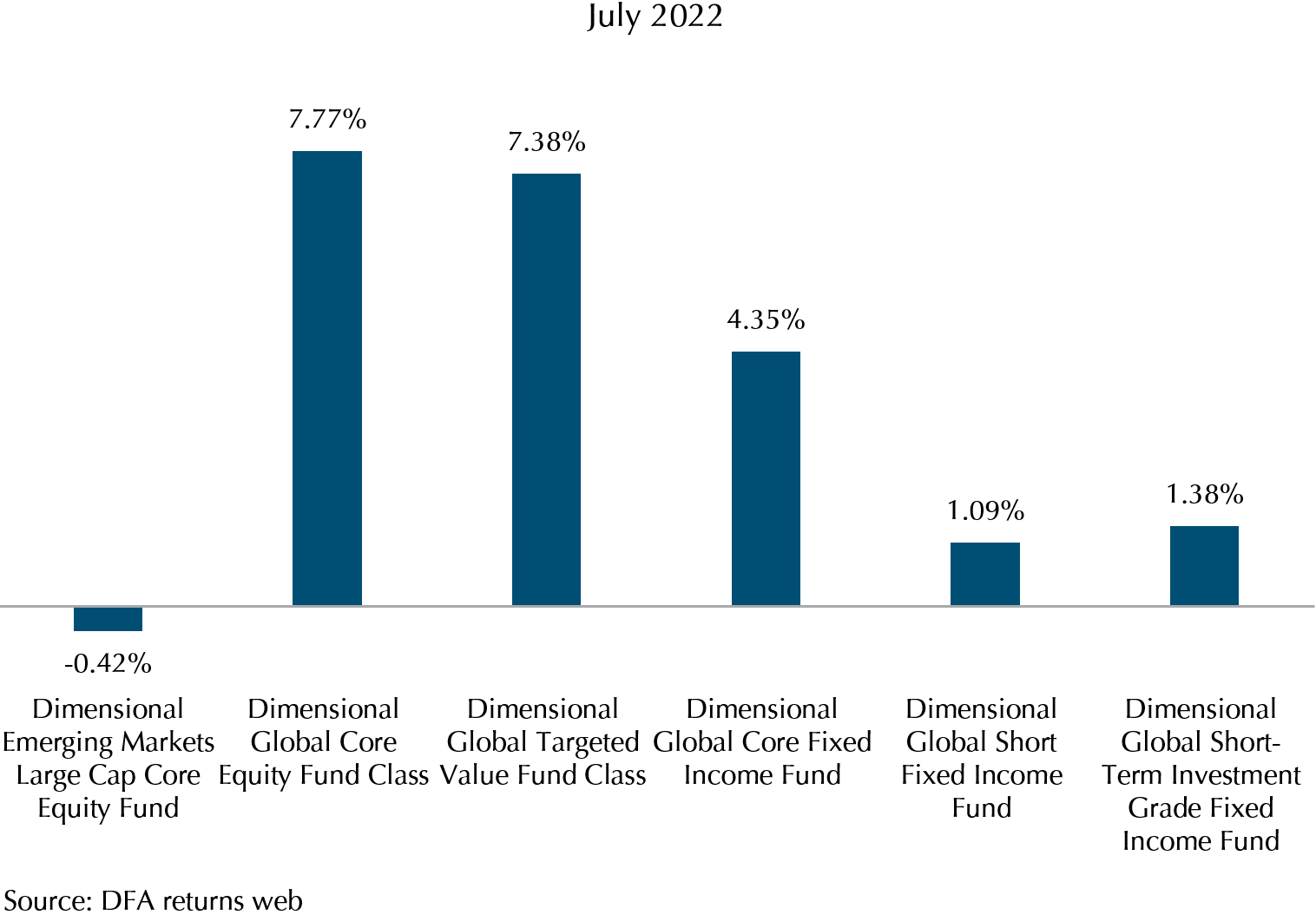

It is well and good for the indexes to be up, but what is of more importance to us is how the funds that we are invested in have done. The index funds track the index return (less cost) so we know they have done well this month, so we shift focus to the systematic funds from Dimensional.

Looking at the data in Exhibit 2, the funds from Dimensional have tracked the major indexes well. The Global Core Equity fund and the Targeted Value fund returned 7.77% and 7.38% respectively, which is close to the 8.08% return of the MSCI World IMI. Do note that the Dimensional funds have outperformed greatly over the past 6 months as value stocks have done well and are still capturing the return on the upside in July.

Exhibit 2: Fund returns in USD

Fixed income has also bounced back, with the Global Core Fixed Income fund up 4.35% in the month, and the short-term bond funds both up more than 1%.

We did not miss the good days

Despite the markets having the best month since November 2020, we can never be certain how the markets will move after July. We would like to highlight and remind clients that by staying invested in globally diversified funds, the portfolios have captured the returns from the rebound, which is critical for clients to achieve their long-term wealth goals. This can only happen if the client and adviser work together to keep the portfolio invested in the appropriate funds, and we would like to thank you for your continued trust in our advisers as they work with you through this difficult time.

Major Central Banks’ Conundrum – Inflation or Recession

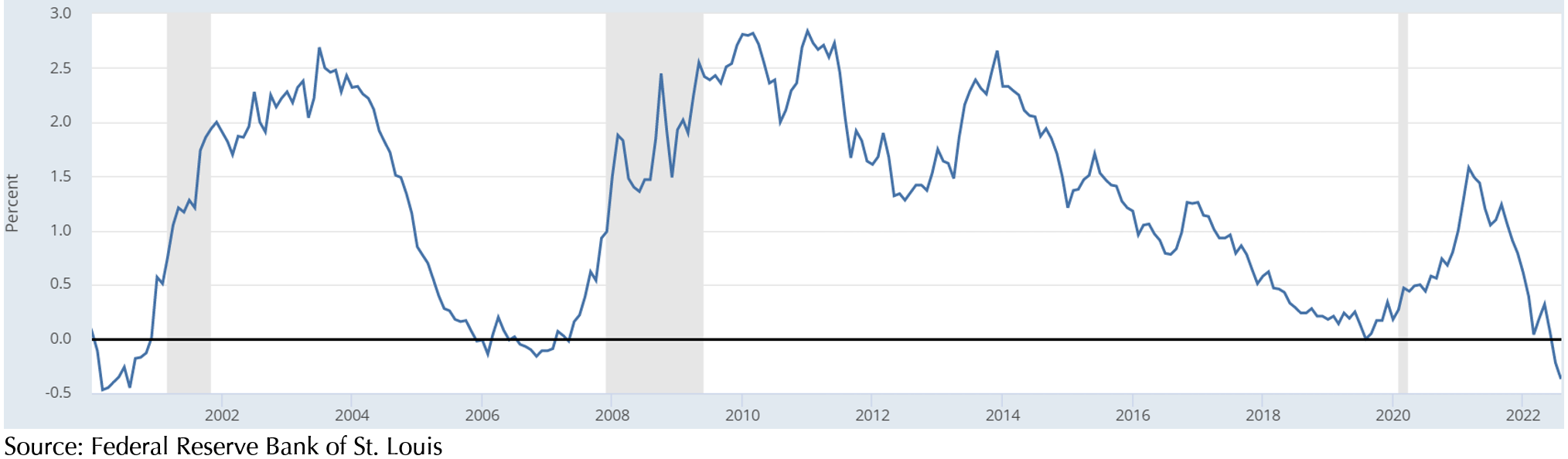

Looking at the current major economies, the central banks are in a conundrum between preventing a hard landing or hiking rate to curb inflation. The US economy contracts for a second consecutive quarter as real GDP growth rate fell by –0.9% in the first quarter followed by a –1.6% contraction in the second quarter. The markets continue to price in a recession as yield curve remains inverted. Exhibit 3 shows the 10 minus 2 Year Treasury at its lowest point since the dot com crash in March 2000. Despite the slowdown, the Fed is still tightening the buckle on demand to curb inflation as cumulative rate hike for June and July is now 150 basis points – the steepest since the early 1980s.

Exhibit 3 – 10-Year Treasury Constant Maturity Minus 2-Year Treasury Constant Maturity

In Europe, annual inflation in Germany rises to 8.5% in July as Europe’s largest economy impose further cuts to natural gas deliveries from Russia amidst record energy prices. The European Central Bank (ECB) hike rate for the first time in 11 years with 50-bps hike instead of the expected 25bps to deal with its rising prices as well and the ECB Bank deposit rate is now at 0%. Caught between rising debt in some of its economies and hot inflation, the ECB also introduced a Transmission Protection Instrument (TPI) which will be used to buy government bonds and possibly private bonds as well.

Eastwards, China’s conviction on its zero Covid policy has battered its economy and dampened manufacturing output. Lesser factory output and pent-up demand post Covid recovery pushed Producer Price Index to 6.1% and inflation to 2.5% in June, the highest in 2 years. While China’s monetary policy remain accommodative, it is uncertain how long this will last. The central bank of China, People’s Bank of China (PBoC), said on 14 July that it is watching monetary policy tightening abroad closely.

While Japan continues to retain its easy monetary policy with short-term rates at –0.1%, its inflation has been creeping upwards as well. Core consumer prices in June rose 2.2% on an annual basis, remaining above the Bank of Japan’s (BoJ) inflation target of 2% for a third straight month. In light of slowing global economy, the Japan government has also downgraded sharply its GDP forecast from 3.2% to 2% for its fiscal year ending in March 2023. Compared to other major central banks, the BoJ is still in a better position as inflation does not seem to be spiralling out of control. However, an easy monetary policy cannot be sustained if core CPI is constantly staying above its target.

The extent of each central banks’ monetary policy will nevertheless have an impact on the global demand and the markets. An aggressive rate hike by central banks may result in a global recession while an over accommodative monetary policy may cause inflation to become entrenched.

Bear rally or start of the next bull market?

Right now, the views are divided on the question, is this just a bear market rally or the start of the next bull? While it is interesting to discuss the possibilities, the truth is that there are still many unknowns. If inflation comes down and the central banks do not tighten policy as fast, it could be grounds for optimism. If central banks tighten beyond expectations and cause a deep recession, then the negative scenarios might happen. Regardless, we have seen that our portfolios are resilient when the markets come down (cushioned by the exposure to value stocks and fixed income (if it is part of the allocation) and are able to capture the returns when markets recover and go higher.

Thank you for staying invested, and for continuing to trust your adviser. Do reach out if you have any questions, and we would like to wish all clients a very Happy National Day!

Warmest Regards,

Investment Team

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current estate plan, investment portfolio, financial and/or retirement plan, make an appointment with us today.