The best musical composition, novel, or artwork is built on basic elements like notes, alphabets, or colour palettes. Similarly, to appreciate the elegance, depth and intricacy of portfolio returns, we should first start with understanding the building blocks of portfolio returns, which is the main purpose of this article. Important considerations of portfolio returns are added for the benefit of readers with insomnia.

This article focuses on an investor investing in a Unit Trust (“UT”) or Exchange Traded Funds (“ETF”) and will cover the following areas:

Two Building Blocks of Portfolios Returns

- Gross Return

a) Investment Return

b) Currency Return

- Expense

a) Fees

b) Taxes

Five Important Considerations

- Returns Drivers

- Currency Effect

a) Currency Hedging

b) Funding Currency

c) Transaction Currency

- Performance Measurement

- Absolute Versus Relative Return

- Real Return

Warning ☢

Brace yourself for an article of such excruciating dullness that filing a tax return is exhilarating by comparison. However, according to statistics which I have just made up, 88% of C-suite executives strongly agree that reading and doing boring things without getting bored is a distinctive competitive advantage that makes them successful.

Two Building Blocks of Portfolios Returns

Illustrative Waterfall Chart of Portfolio Returns:

Source: Author

1. Gross Return

a) Investment Return

This is the main driver of total portfolio returns. This is the return from the pure price movement of a security such as an Exchange Traded Fund (“ETF”) or an individual stock.

b) Currency Return

This refers to the gain or loss an investor experiences on their investment due solely to fluctuations in the exchange rate between the currency (say USD) they invested in and their base currency (say SGD).

2. Expenses

Real investments, unlike hypothetical benchmarks, have friction due to expenses incurred. There are broadly two types of expenses which reduce the net return of the Portfolio.

a) Fees

(i) Platform Fee

A platform fee refers to a fee charged by an online investment platform for accessing and using their services, which typically includes functions like account management and reporting. It is common for a platform to include a custody fee meant for asset safekeeping in their platform fee.

(ii) Total Expense Ratio

The total expense ratio (“TER”) is a measure of the total costs associated with managing and operating an investment fund such as a UT or ETF. These costs consist primarily of management fees and additional expenses, such as legal fees and auditor fees. The TER is expressed as a percentage of the fund’s total assets. Management fees are paid to the fund manager managing the fund. A portion of the management fee (typically called trailer fee) is paid to distributors to incentivise the marketing and sale of the funds.

Despite the naming, it is important to recognise that the TER does not capture all underlying costs such as transaction fees (e.g. commission, brokerage, exchange fees) and taxes. Investors should be mindful that an actively managed fund with high turnover of securities would incur high explicit transaction fees and implicit trading cost (from bid-ask spread) that will not show up in TER.

(iii) Sales Charge

This is a front-end fee charged by distributors for funds.

(iv) Advisory Fee

An advisory fee is a fee paid for professional advisory services relating to financial plan creation, portfolio management, and account maintenance.

Providend only uses funds with no sales charge and trailer fees to minimise cost and the risk of conflict of interest to our clients.

b) Taxes

The main tax considerations at the fund level are estate duty and withholding tax, especially from the U.S. given that it represents more than 70% of the MSCI World Index (for Equities) and more than 40% of Bloomberg Global Aggregate Bond Index. Capital gains tax (i.e. tax on investment profits) has lost popularity over the years and is only applicable to small investible countries like Brazil with generally insignificant impact to a globally diversified portfolio.

(i) Estate Duty

Non-residents of the U.S. are subject to estate tax on their U.S. assets which include real estate and certain intangible assets such as stocks of U.S. corporations. Assets exceeding the USD 60,000 threshold are subject to estate duty ranging from 18% to 40%. As a reference, the taxable amount of the Estate of USD100,001 to USD150,000 attracts a tax rate of 30%.

U.S. Citizens and U.S. Domiciliaries are also subject to estate taxation at a maximum rate of 40%, though the exemption is much higher at USD 10 million.

(ii) Withholding Tax

U.S. tax law requires the withholding of tax for non-US persons at a rate of 30% on payments of U.S. source stock dividends, short-term capital gain distributions, and substitute payments in lieu. Consequently, all dividends of U.S. listed securities are subject to a 30% dividend withholding tax.

Providend uses funds with efficient and legal tax structures. For example, we use funds that are under the Undertakings for the Collective Investment in Transferable Securities (“UCITS”) framework that are not considered U.S. assets and therefore not subject to U.S. estate tax.

Five Important Considerations

1. Return Drivers

Brinson, Hood and Beebower (“BHB”) published one of the most cited investment papers in 1986 in the Financial Analysts Journal called the “Determinants of Portfolio Performance.” The key insight drawn was that data from 91 large U.S. pension plans over the 1974-83 period indicate that investment policy (asset allocation) dominates investment strategy (market timing and security selection), explaining on average 93.6 percent of the variation in total plan returns. The original BHB paper sparked a wave of related research, and several critics have questioned the methodology, rigor, and assumptions of the BHB study.

David Larrabee gave a balanced view in his article titled “Setting the Record Straight for Asset Allocation” in 2012, which was published in the CFA Institute Enterprising Investor Blog. He concluded that the various studies collectively demonstrate the importance of (1) being in the market, and (2) doing a strategic asset allocation. However, the importance of asset allocation was likely overstated by BHB.

2. Currency Effects

a) Currency Hedging

Currency hedging is a strategy that aims to reduce the impact of currency fluctuations on investment returns. A simple example would be to hedge a USD exposure from an investment in Apple Stock with an FX forward contract (sell USD and buy SGD).

Currency itself has no intrinsic return profile and thus should have little impact on the portfolio’s total expected return over the long run. However, currency exposure increases volatility in the short run, which may not be ignored. A 2020 research (To Hedge or Not to Hedge?) by Dimensional Fund Advisors concluded that the impact of currency hedging on volatility depends mostly on the magnitude of asset volatility relative to currency volatility. Stocks tend to be more volatile than currencies and drive the overall volatility of a global equity portfolio. Currencies, however, are more volatile than bonds and dominate the overall volatility of a global bond portfolio. A 2024 research (How do Global Portfolio Investors Hedge Currency Risk?) by State Street Bank confirmed the often conjectured hypothesis that fixed-income investors hedge significantly more than equity investors.

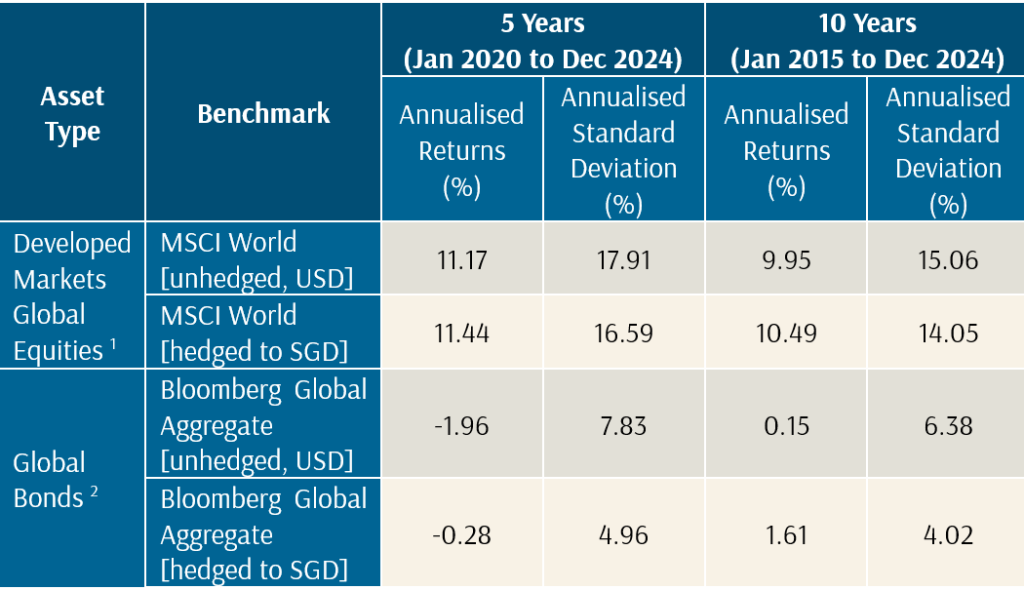

Given the above considerations, Providend recommends the use of unhedged Global Equity Portfolios and hedged Global Fixed Income Portfolios.

The annualised returns and standard deviation for developed markets global equities index and global bonds index on an unhedged (in USD terms) and hedged (to SGD) basis are shown below.

Source:

[1] MSCI

[2] Dimensional Funds Advisor Returns Web

b) Funding Currency

To avoid slippage, the funding currency should be the same as the currency denomination of the fund. Otherwise, FX conversion would be executed by the Platform Provider or the Fund Manager. For retail investors, the typical FX conversion rate is at the mid-rate (i.e., the middle point between the buying (bid) and selling (ask) rates), plus an additional spread of about 0.3%. Banks would generally charge a higher spread than Platform Providers and Fund Managers.

c) Transaction Currency

This is part of the overall trading cost. As an example, investing in a USD-denominated World Equity Fund by definition means investing in underlying securities that are not listed in the U.S. and settled in USD. The fund manager would need to convert the USD that was funded into the settlement currency (say SGD) of the security (say DBS Bank) to be invested. The fund manager’s Treasury Desk would do the FX conversion with great cost efficiency as the Treasury Desk would be able to do netting (across the whole organisation) and trade the net currency pairs in terms of pips at a small fraction of what retail investors will incur. A pip is the smallest whole unit price move that an exchange rate can make. The pip size of the USDSGD pair is 0.0001. If a platform allows for even smaller price movements, they are called “pipettes,” which represent fractions of a pip.

3. Performance Measurement

It is not common knowledge that there are different performance measurement methodologies. The two predominantly accepted ones are Money-Weighted Return and Time-Weighted Return. As astounding as it may sound, an investment could have positive returns using one method and negative returns using another method. Put simply, they represent different things and are suitable for different circumstances.

A good comparison is articulated by my colleague, Kyith, in this article in his personal investment blog.

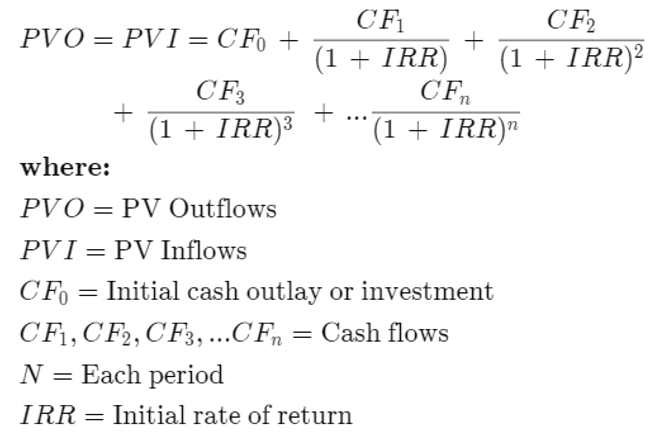

a) Money-Weighted Return (“MWR”)

Includes the impact of cash flows on a portfolio’s performance. MWR is a more personalised measure of an investor’s experience with an investment. It takes into account the size and timing of cash inflows and outflows, which are determined by the investor.

Formula:

Source: Investopedia

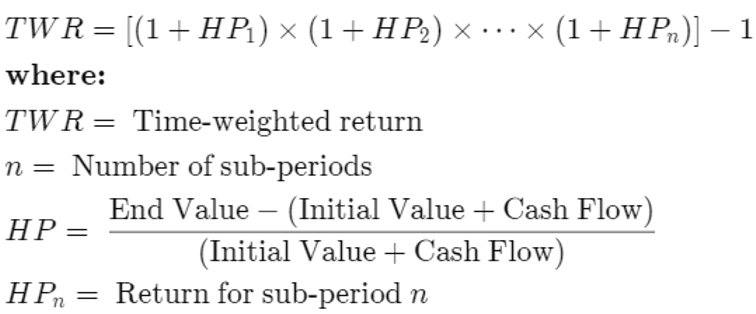

b) Time-Weighted Return (“TWR”)

Excludes the effect of cash flows in and out of the portfolio. TWR is more focused on the fund manager’s performance, excluding the influence of investor behaviour. TWR is calculated by dividing a period into sub-periods, calculating the percentage return for each sub-period, and then chain-linking the return percentages together.

Formula:

Source: Investopedia

4. Absolute Versus Relative Return

Absolute return is simply the portfolio return over a certain period of time. Relative return is the difference between the absolute return and the performance of the benchmark or index, such as the S&P 500. The most important factor in choosing a benchmark is to have one that mirrors the investible assets and risk level of the portfolio.

Seeking absolute return as a return objective is more common for hedge funds than for other investment vehicles.

5. Real Return

The returns mentioned above are all relating to nominal return. The primary goal of investing is to achieve real rates of return, which are nominal return adjusted for inflation. This is important because inflation can reduce the purchasing power of an investment over time. I personally find the use of the term “real” interesting. Does it imply that nominal return is “unreal” or “fake”?

Formula:

Glossary

- Closed-End Versus Open-End Funds

Closed-end funds have a fixed number of shares available for trading, and investors cannot redeem their shares with the fund administrator but must trade them on the secondary market. Open-end funds issue new shares, are frequently rebalanced, and allow investors to redeem shares through the fund administrator.

- Unit Trust

A UT is a collective investment scheme whereby multiple investors pool their money together, which is then managed by a fund manager who invests the money in a variety of assets like stocks and bonds, with each investor owning a portion of the fund represented by “units” they can buy and sell. UTs are open-ended funds, and the price of each unit (unit trust) is based on the net asset value (NAV) of the fund’s investment portfolio.

- Exchange Traded Fund

An ETF is a collection of securities such as stocks or bonds, which are grouped together based on a specific fund mandate and can be bought and sold like an individual stock. According to Investopedia, the first ETF was launched in Canada in 1990, which led to the introduction of the first U.S. ETF, the SPDR S&P 500 ETF Trust, in 1993. Technically, any securities could be bundled and offered as an ETF. ProShares Bitcoin Strategy ETF is the first cryptocurrency-linked ETF, which was launched in July 2021.

While most ETFs are passive ETFs, which are designed to track an index mechanically, there has been a growing trend of active ETFs in recent years, which attempt to beat the market through active fund management.

Final Thoughts

If you have come this far, congratulations. If it is daytime, you may need to get a life. If it is night-time, you must be feeling sleepy, and I have cured your insomnia (You are welcome!).

I hope my sharing of the basic building blocks will spark your interest in burrowing into the bottomless rabbit hole of investment and financial literacy.

As Steve Jobs once said (with a twist), “Stay hungry. Stay foolish. Stay boring.”

This is an original article written by Foo Jit Hwee, Associate Adviser at Providend, the first fee-only wealth advisory firm in Southeast Asia and a leading wealth advisory firm in Asia.

If you are interested in joining our Providend Associate Adviser Programme, kindly visit this link to find out more: https://providend.com/careers

For more related resources, check out:

1. A More Reliable Way to Get Enough Investment Returns

2. Investing in the S&P 500 Alone is Not the Silver Bullet

3. Stop Making New Year Resolutions Which Will Fail!

Download our Investment eBook titled “A More Reliable Way to Get Enough Investment Returns: Even During Times of Market Uncertainty” here.

Through deep conversations with our advisers, you will gain clarity on what matters most in life and what needs to be done to live a good life, both financially and non-financially. Learn more about our investment philosophy here.

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current investment portfolio, financial and/or retirement plan, make an appointment with us today.