Executive Summary

In July, global equity markets saw strong performance driven by weaker-than-expected inflation and employment data, increasing the likelihood of a Federal Reserve rate cut. This environment particularly benefited small-cap stocks, which outperformed their large-cap counterparts. Dimensional’s developed market equity funds, which are overweight small-cap stocks, significantly outperformed the market indexes.

The Global Targeted Value Fund, the Global Core Equity Fund, and the World Equity Fund posted impressive gains of 7.55%, 3.25%, and 3.28%, respectively, compared to the MSCI World IMI Index and the MSCI ACWI IMI Index, which rose 2.27% and 2.06%.

However, this positive momentum was abruptly halted at the beginning of August due to the unwinding of carry trades. This was triggered by significant developments, including a rate hike by the Bank of Japan, driving up Japan’s yield, and weaker US labour data, heightening fears of an economic slowdown, and caused US yields to fall. Consequently, there was a selloff in equities, leading to substantial month-to-date losses for both market indexes and Dimensional equity funds as of 5 August 2024.

These rapid changes highlight the inherent volatility and unpredictability in financial markets. Despite short-term fluctuations, a long-term investment strategy remains crucial. By focusing on long-term growth and diversification, investors can better navigate market uncertainties and capitalise on opportunities for sustained returns. The contrasting performances of July and August underscore the importance of maintaining a disciplined, long-term approach to investing in equities.

As part of our series covering major economies’ equity landscapes, we will focus on the US equity landscape in this final instalment.

July Performance

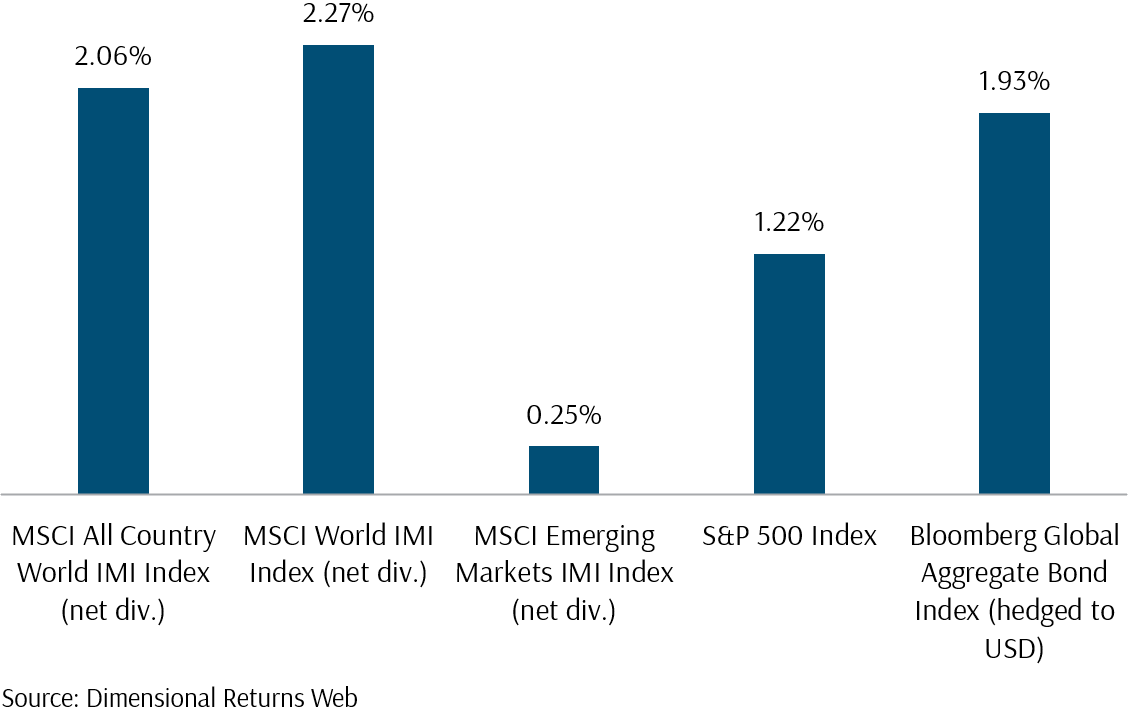

Small-cap and value stocks performed better in July. Weaker-than-expected CPI data released on 10 July 2024, combined with weak employment data, increased the probability of a rate cut in the Fed’s September FOMC meeting and drove US yields lower. Small-cap stocks rallied as the expectation of falling interest rates benefits small companies more due to their larger floating debt ratio, leading the Russell 2000 to rally about 10% in July. Expectations of falling rates also saw the Bloomberg Global Aggregate Bond Index rise by 1.93% as shown in Exhibit 1. In contrast, the S&P 500 Index, rose by 1.22% as large-cap companies underperformed compared to their small-cap counterparts.

One possible reason for these negative returns in large-cap stocks could be their expensive valuations, which have led investors to rotate out of large-cap and into small-cap stocks. Another reason is that after reporting results, investors are now questioning the return on investment for the massive Artificial Intelligence (AI) capital expenditures (CapEx) spend of the tech stocks. For example, Meta has committed to spending $37 to $40 billion in CapEx this year, and Microsoft has spent $55 billion the last fiscal year and is likely to spend a similar amount this year. This has investors questioning whether this CapEx spend for AI will be monetised effectively, and thus we have seen a pause in the tech-led rally. However, the rally extended to other sectors instead, with the equal-weight S&P 500 Index rising almost 11% in the month.

Overall, the MSCI World IMI Index, which tracks large, mid, and small-cap stocks in developed markets, rose by 2.27%. Meanwhile, the MSCI Emerging Market IMI Index climbed only 0.25%, dragged down by troubles in China’s real estate sector, which caused a spillover across the broader sectors, and ongoing concerns about weak inflation data signalling a lack of consumer confidence. Overall, July was still a strong month for stocks, as the MSCI All Country World IMI Index, which tracks market-cap-weighted developed and emerging markets, rose by 2.06%.

Exhibit 1 – Market Index Performance: July 2024 (USD)

Small-Cap Supercharged Dimensional’s Developed Market Equity Performance

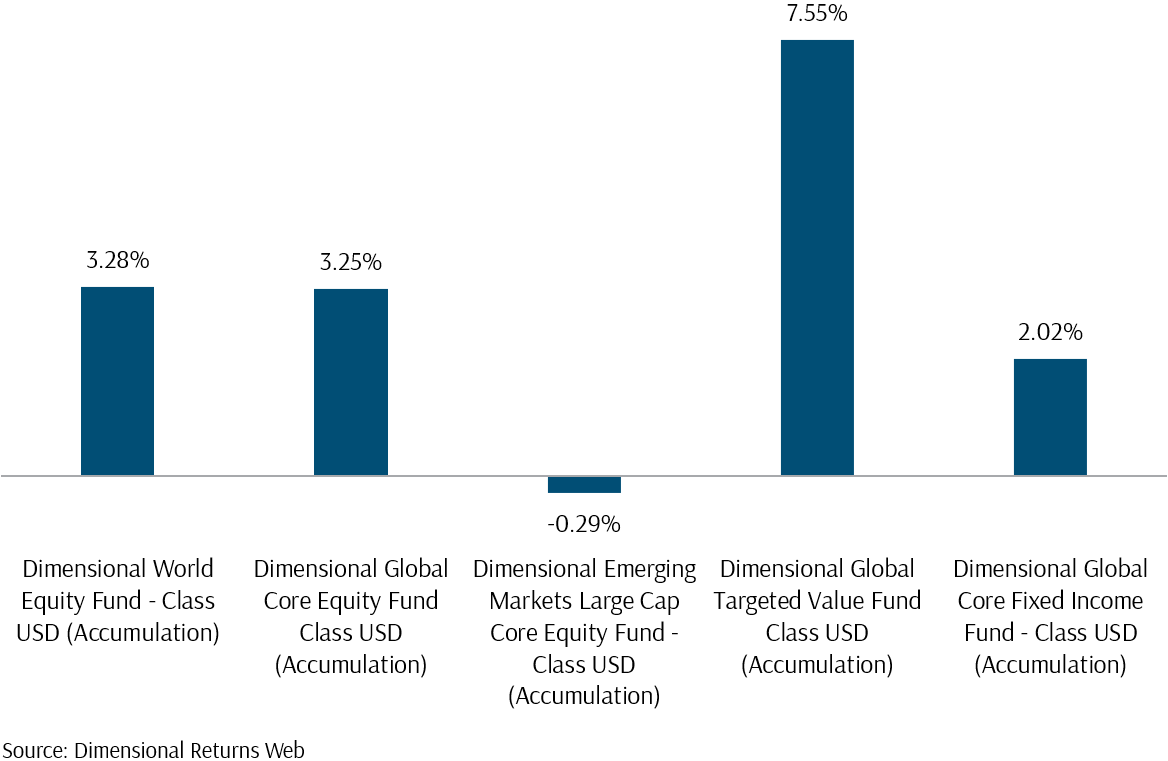

While the Dimensional Global Core Fixed Income and the Emerging Markets Large Cap Core Funds performed similarly to the Global Aggregate Bond Index and the MSCI Emerging Markets Index, with returns of 2.02% and -0.29% respectively (Exhibit 2), the Dimensional developed market equity funds significantly outperformed their market indexes. Most notably, the Global Targeted Value Fund, which holds only small value stocks, rose by 7.55%, more than three times the MSCI World IMI Index. Additionally, the Dimensional Global Core Equity Fund and the Dimensional World Equity Fund, both overweight in small value stocks compared to their respective indexes, the MSCI World IMI Index and the MSCI All Country World IMI Index, rose by 3.25% and 3.28% respectively.

Exhibit 2 – Dimensional Funds Performance: July 2024 (USD)

August Market Turmoil: Unwinding of Carry Trades Triggers Equity Selloff

Despite strong equity performance in July, the start of August has been devastating for the market.

As of 5 August 2024, equities have plummeted month-to-date. The primary driver of this downturn is the unwinding of carry trades, particularly due to significant developments in Japan and the US. The Bank of Japan’s (BOJ) chair, Ueda, raised interest rates, causing yields in Japan to rise. Simultaneously, in the US, softer labour data, including an increase in the unemployment rate from 4.1% in June to 4.3% in July and the addition of only 115,000 jobs compared to the expected 175,000, raised fears of a slowing economy.

This comes on the heels of the Federal Reserve’s decision to hold rates steady in late July, maintaining elevated borrowing costs until at least the next Federal Open Market Committee (FOMC) meeting in September. This scenario lowered US yields as the likelihood of a rate cut increased. The resulting unwinding of carry trades—a strategy where investors borrow in a low-interest-rate currency like the Japanese Yen (JPY) to invest in higher-yielding assets—led to a selloff in stocks. When Japanese yields rose and US yields fell, the value of collateral in USD fell, likely leading to margin calls which forced investors in the carry trade to sell off stocks and convert their investments back into JPY, which contributed to the sharp decline in equity markets.

The logic behind the unwinding of carry trades impacting equities, especially with the JPY/USD dynamic, works as follows: investors engage in carry trades by borrowing in a currency with low interest rates (such as the JPY) and investing in assets in a currency with higher interest rates (like the USD). When the interest rate differential between these currencies changes—due to events like the BOJ raising rates or US labour data signalling economic slowdown—the carry trade becomes less profitable. Investors then unwind their positions by selling off the higher-yielding assets (US equities in this case) and repaying their borrowings in the low-interest-rate currency (JPY). Another factor is that these trades are usually leveraged, so if the borrowing currency strengthens (like the JPY did), it reduces the value of the collateral, leading to margin calls. This unwinding process exerts downward pressure on the stock markets and can lead to significant equity selloffs.

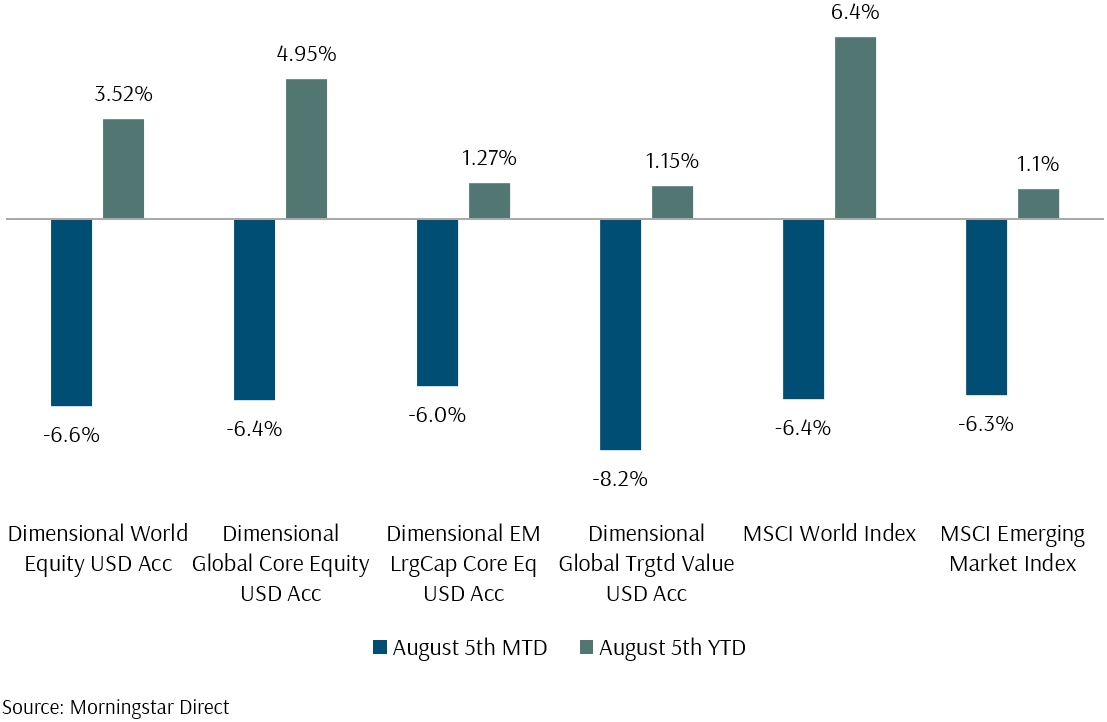

As of 5 August, month-to-date, the Dimensional equity funds fell by an average of 6.8% as shown in Exhibit 3. In market indexes, the MSCI World Index and the Emerging Market Index fell by 6.4% and 6.3%, respectively as of August month-to-date, bringing their year-to-date performance to approximately 6.7% and 1.7%, respectively.

Exhibit 3 – Dimensional Equity Funds as of 5 August 2024

Conclusion for July Market Review

July showcased a strong performance in global equity markets, driven by weaker-than-expected inflation and employment data that increased the probability of a rate cut by the Federal Reserve. This environment was particularly beneficial for interest rate-sensitive small-cap stocks, which outperformed their large-cap counterparts. Dimensional developed market equity funds, especially those focused on small-value stocks, significantly outperformed the market indexes.

However, the start of August has been marked by a sharp downturn. The primary catalyst for this decline has been the unwinding of carry trades, triggered by significant developments in Japan and the US. The Bank of Japan’s interest rate hike and weaker US labour data have heightened fears of an economic slowdown. As a result, investors have reversed their carry trade positions, leading to a selloff in equities. This has resulted in substantial month-to-date losses for both market indexes and Dimensional equity funds as of 5 August 2024.

These rapid and unpredictable market changes from July to August highlight the inherent volatility and uncertainty in the financial markets. While July’s positive momentum suggested a continued upward trajectory, August’s abrupt downturn underscores the difficulty of predicting short-term market movements. The events demonstrate that market conditions can shift rapidly due to a variety of factors, such as economic data releases, central bank decisions, and global financial strategies like carry trades.

In light of this unpredictability, it is crucial to emphasise the importance of investing for the long-term. By maintaining a long-term perspective, investors can capture market premiums that might be missed through short-term trading. Over time, the market tends to reward patience and consistency, allowing investors to benefit from the overall growth and compounding returns of diversified equity investments.

The contrasting performances of July and August serve as a reminder that while short-term market movements can be volatile, a long-term investment strategy remains the most effective way to achieve financial goals and capitalise on market opportunities.

The US Equity Landscape

As part of our monthly series on major economies’ equity landscapes, this month we focus on our final —though certainly not least —equity landscape: the US.

The Importance of the US Equity Landscape

On 19 July 2024, Jemma Wheeler reached Palma de Mallorca airport for what she expected would be a quick two-hour flight home after a five-night break with her family. However, she found herself standing in a queue for three hours, unable to proceed due to unexpected delays. The cause? A widespread IT disruption triggered by a system update from CrowdStrike[1].

Earlier that day, at 04:09 UTC, CrowdStrike had released a sensor configuration update to Windows systems as part of their ongoing operations. This update, intended to enhance the protection mechanisms of the Falcon platform, inadvertently caused a logic error. The result was a catastrophic system crash and blue screen (BSOD) on impacted systems across the globe, affecting a myriad of sectors and services.

Closer to home, Scoot, the low-cost subsidiary of Singapore Airlines, also faced significant issues due to the same global IT outage. The disruption affected their flight reservation system and check-in process, leading to flight delays. Scoot had to advise passengers departing from Changi Airport to arrive at least three hours before their flight to manage the operational challenges. Fortunately, services were eventually restored, and normal check-in procedures resumed[2].

These incidents underscore the profound and far-reaching impact of a single update error from a US company. The ripple effects of CrowdStrike’s configuration update were felt worldwide, highlighting the critical role US companies, particularly in the tech sector, play in global operations and the potential consequences of their technical mishaps.

To grasp the full scope of global equity investment, understanding the US equity landscape is crucial. The MSCI ACWI Investable Market Index (IMI), which encompasses 99% of global equity opportunities, highlights this importance. Within this index, US companies dominate, comprising 63% of the total weight, making the US the largest single-country component. In stark contrast, Japan holds the second-largest weight at only around 6%. This significant disparity emphasises the overwhelming influence and scale of US equities in the global market. Therefore, gaining insight into the US equity market is not just beneficial but essential for any comprehensive understanding of global investment opportunities.

Introduction

In this final segment of our US equity landscape coverage, we will revisit key events from recent years, starting with the COVID-19 lockdowns in 2020. Our focus will be on highlighting the following risks and its implication on the US equity landscape:

1. Inflationary risks

2. High interest rates and the US debt issue

3. US commercial real estate risks

We will explore how recent developments which include:

4. How the upcoming US election might influence these risks.

5. Examine whether the current high valuations in tech stocks resemble the dot-com bubble of 2000.

6. Finally, by providing two historical examples, we will demonstrate why US companies can still deliver strong returns despite these challenges.

Ultimately, this discussion will showcase the importance of staying invested in the market.

1. Inflationary Risks

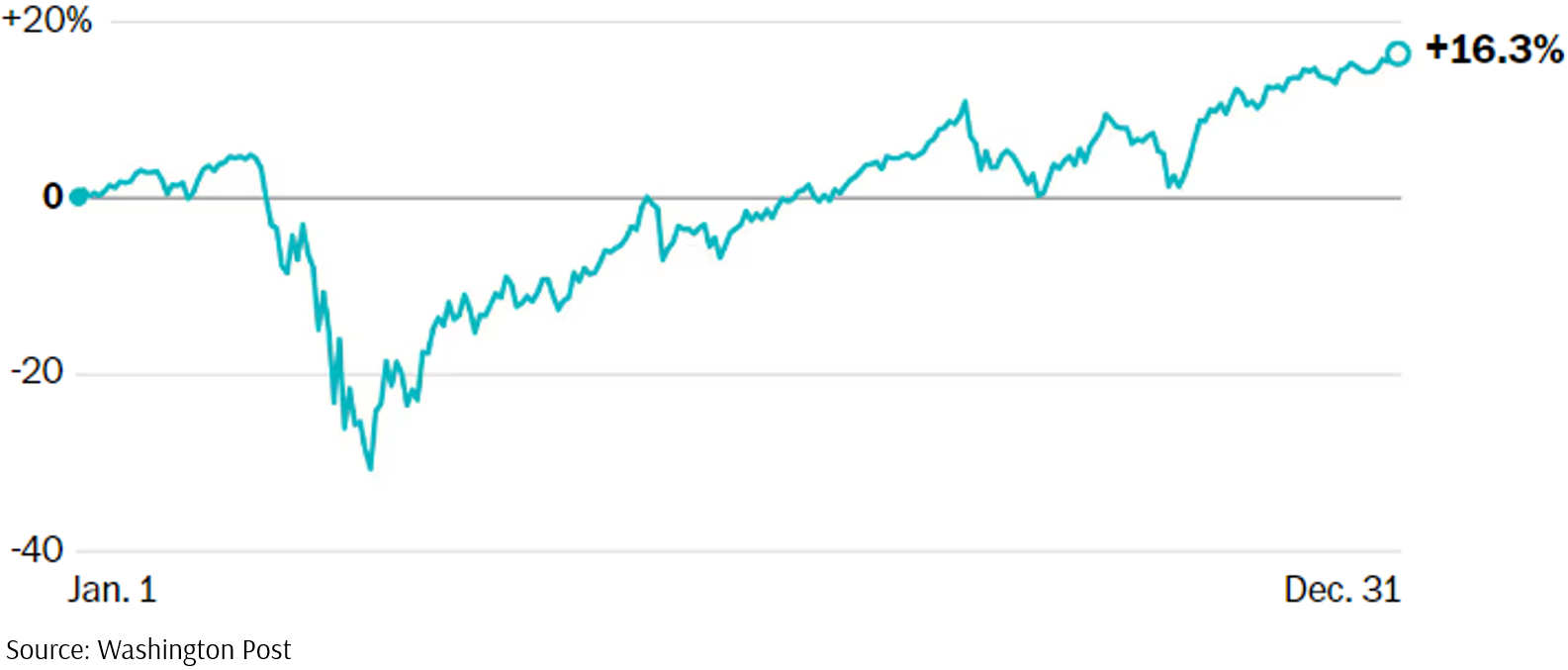

In March 2020, as the extent of the COVID-19 pandemic became clear, the stock market experienced a sharp decline, with stocks tumbling 34%. However, this downturn turned out to be the shortest in US history. Since the market bottomed on 23 March 2020, the S&P 500 has risen 68%, ending the year up 16.3% (Exhibit 4).

Exhibit 4 – The S&P 500 Performance in 2020

This rebound reflects market optimism about 2021 but also highlights the disconnect between the stock market’s success and the broader economic headlines. Several factors contributed to this recovery:

- Monetary Policy: Quantitative easing and near-zero interest rates boosted the stock market.

- Fiscal Stimulus: Significant fiscal stimulus towards US households increased consumption spending.

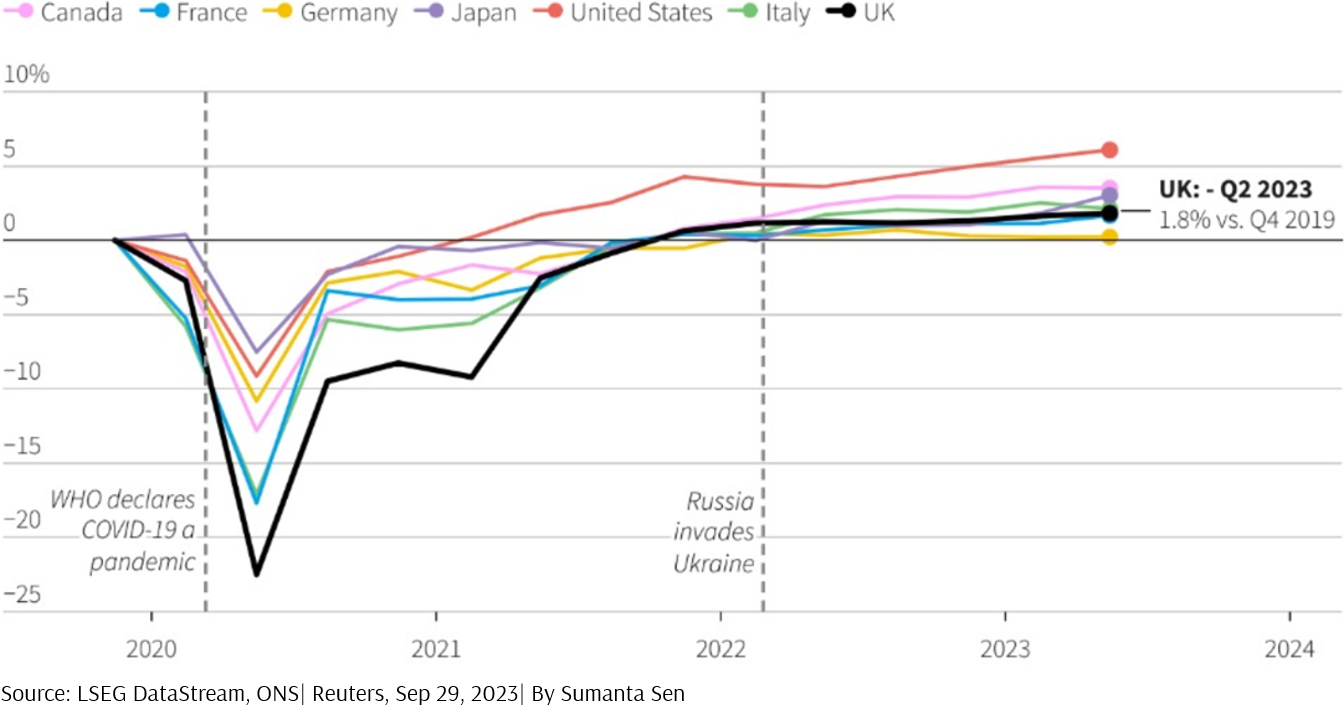

According to FactSet[3], 79% of the S&P 500 Index’s companies reported positive earnings surprises, marking the third highest percentage since FactSet began tracking this metric in 2008. The US economy remained strong going into 2021, rebounding most robustly among the Group of Seven (G7) countries (Exhibit 5).

Exhibit 5 – G7 Real GDP (Q4 2019 – Q2 2023)

However, inflation began to rise. From February 2021 to December 2021, headline inflation increased from 1.7% to 7%, primarily due to supply chain disruptions and strong demand. By June 2022, the Consumer Price Index (CPI) showed inflation peaking at 9.1%, exacerbated by the Russian invasion of Ukraine in March 2022, which impacted wheat, fertiliser, and energy prices.

Implications of Rising Inflation

Apart from potentially leading to rising interest rates, inflation can negatively impact equities in several ways:

1. Erosion of Purchasing Power: Inflation reduces the real value of money, decreasing consumer spending, and hurting company revenues and profitability.

2. Increased Costs: Higher costs for raw materials, labour, and other inputs can squeeze profit margins if companies cannot pass these costs onto consumers.

3. Reduced Investment Returns: Inflation can diminish real investment returns, making equities less attractive and reducing capital inflows in the stock market.

Although inflation has fallen to 3%[4] since its peak in June 2022, risks remain due to ongoing geopolitical tensions, such as the Ukraine-Russia war and the Israel-Palestine conflict. If these conflicts escalate, they could lead to higher shipping costs and import prices, exacerbating inflation and putting downward pressure on US equities.

Conclusion for Inflationary Risks

The persistent inflation from late 2020 to mid-2022, driven by factors like geopolitical tensions and supply chain disruptions, has significantly impacted the US equity markets. Inflation reduces purchasing power and increases costs for businesses, squeezing profit margins and potentially diminishing real investment returns. Although inflation has somewhat subsided, ongoing geopolitical conflicts pose a risk of renewed inflationary pressures, which could adversely affect consumer spending and corporate profitability, ultimately impacting equity markets.

In the next section, we will continue our recap by examining the impact of rising US interest rates on equities and the implications for the already high US debt.

2. High Interest Rates and the US Debt Issue

In response to the rising inflation rates, the US central bank hiked interest rates the most aggressively in 35 years[5] at the start of 2022. The rising interest rates spooked investors, who worried that higher borrowing costs could impact indebted companies, along with higher input costs caused by the ongoing Ukraine and Russia war and a shortage of labour supply.

Additionally, the US government estimated that its debt ceiling would be reached by the end of 2022. The closer the government gets to the debt ceiling, the more uncertainty it creates in the market. Investors tend to become cautious, leading to increased volatility.

A selloff ensues with the S&P 500 Index going down 4% on a single day on 13 September 2022, the worst day of the year. By the end of 2022, the S&P 500 Index had fallen 19% in 2022, marking one of the 10 worst-performing years for the stock index in at least 90 years.

Implication of the High Interest Rates and the US Debt Issue

The interplay between high interest rates and the US debt issue can have a complex and significant impact on US equity markets.

High Interest Rates

Reduced valuation multiples: Higher interest rates generally lead to lower valuations for stocks, especially growth stocks. This is because investors demand higher returns to compensate for the increased risk-free rate offered by bonds.

Increased borrowing costs: Companies with significant debt burdens may face higher interest expenses, reducing profitability and affecting stock prices.

Economic slowdown: Aggressive rate hikes can slow down economic growth, impacting corporate earnings and, consequently, stock prices. However, the Federal Reserve often aims for a “soft landing,” where growth slows enough to tame inflation without triggering a recession.

US Debt Issue

Investor sentiment: Concerns about the US government’s ability to manage its debt can erode investor confidence, leading to market volatility and potential selloffs.

Credit rating downgrades: A failure to address the debt ceiling or a significant increase in the debt-to-GDP ratio could lead to a downgrade of the US credit rating, impacting investor sentiment and increasing borrowing costs for the government and businesses.

Inflationary pressures: A rising debt burden can contribute to inflationary pressures, prompting the Federal Reserve to raise interest rates further, exacerbating the challenges for equity markets.

Conclusion for High Interest Rates and Debt Issue

The aggressive interest rate hikes by the US central bank, aimed at controlling inflation, have led to increased borrowing costs for companies and higher debt servicing costs for the government. These high rates can reduce stock valuations, particularly for growth stocks, and slow down economic growth, which in turn affects corporate earnings and stock prices. Additionally, concerns about the US debt ceiling and potential credit rating downgrades add to market volatility.

In the next section, we will be looking at the unexpected performance of US equities in 2023 despite the US Banking crisis. However, an additional risk is manifesting: the US commercial real estate.

3. US Commercial Real Estate Risk

In March 2023, aggressive interest rate hikes by the Federal Reserve led to a series of bank failures due to massive losses on government bond portfolios held by US banks. The SPDR S&P Regional Banking ETF, which tracks US regional banks, dropped over 40% from March to mid-May 2023. Despite this, the US stock market performed exceptionally well, with the S&P 500 index rising 24% in 2023.

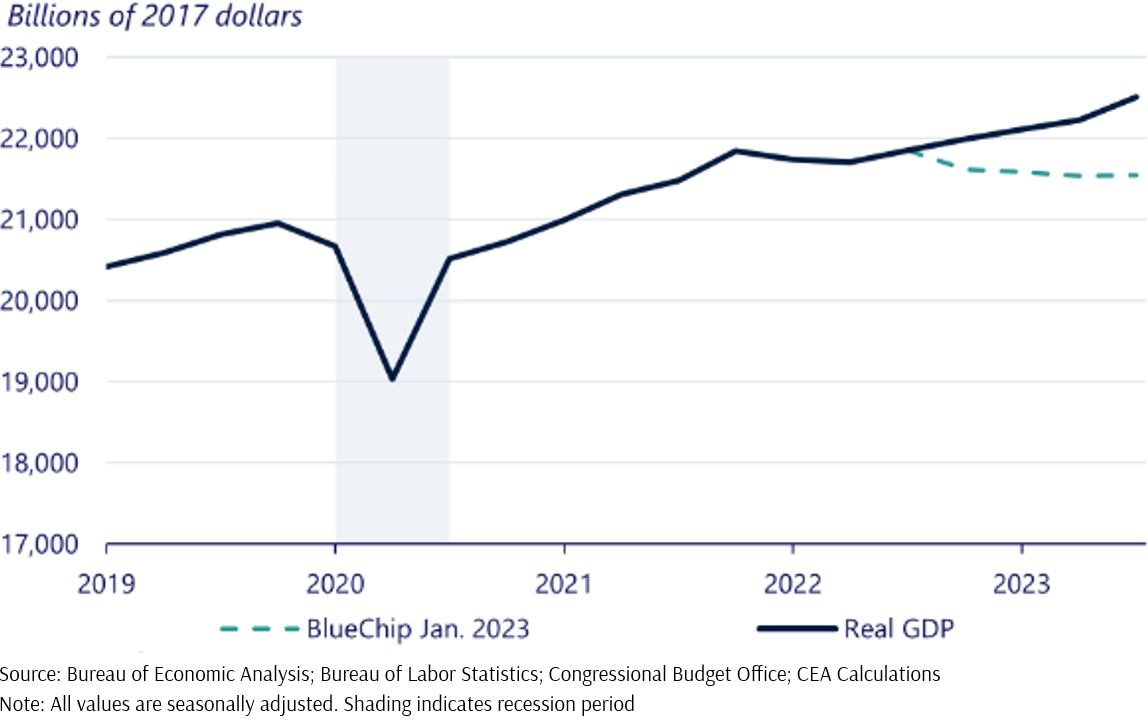

In October 2022, Bloomberg economists predicted a 100% chance of a US recession within a year, citing high interest rates, inflation, global unrest, supply chain issues, and an energy crisis. However, robust consumer spending helped the US economy grow significantly in 2023. The Blue Chip Economic Forecast had predicted -0.1% real economic growth for the year, but this was later revised to +2.6% (Exhibit 6), driven by consumer spending, a revival in manufacturing investment, and increased state and local government purchases.

Exhibit 6 – US Real GDP Growth: Actual vs Expected 2019 – 2023

However, US commercial real estate faced significant challenges. The shift to remote work resulted in less demand for office space, with about 50% of major global companies planning to reduce their office space within three years.

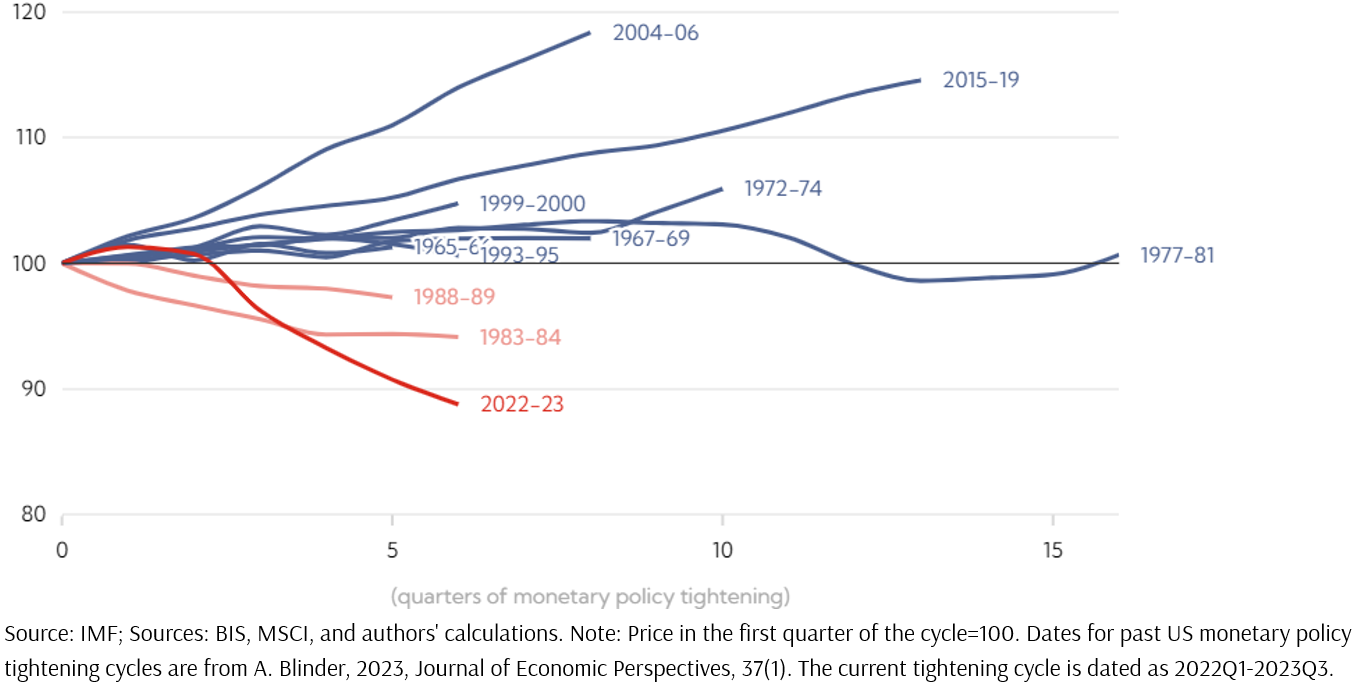

Knight Frank’s 2023 survey[6] of 347 companies indicated that firms with over 50,000 employees anticipated a 10%-20% reduction in office space. Historical data from the The International Monetary Fund (IMF) (Exhibit 7) showed that the 2022-2023 monetary policy tightening cycles led to the most significant plunge in US commercial real estate prices in recent history. This structural shift, exacerbated by the COVID-19 pandemic, has left American cities, especially San Francisco, highly vulnerable to vacant offices.

Exhibit 7 – US Real Commercial Real Estate Prices During Monetary Policy Tightening Cycles, Index

Implications of the US Commercial Real Estate Falling Prices

According to UBS[7] data and Visual Capitalist[8] charts, JPMorgan Chase, the largest US bank, has 12.6% of its loan portfolio in commercial real estate. Major banks like Wells Fargo are building larger cash reserves to buffer potential commercial property credit losses.

While major banks are somewhat insulated from commercial property shocks, averaging 11% exposure in their loan portfolios, smaller banks face greater risks, with about 21.6% exposure. For instance, just this month in August, a large office tower at 135 W. 50th St. in New York was auctioned off for $8.5 million, a significant decline from its $332 million purchase price in 2006[9]. New York Community Bancorp, a smaller regional bank with 57% of its total loans exposed to commercial property debt, reported a $2.7 billion loss in Q4 2023, leading Moody’s to downgrade its credit rating to “junk” status. The bank recently received a $1 billion capital infusion due to concerns over its commercial real estate loans.

Diminishing demand for office space is driving down property values and increasing vacancy rates, affecting the financial health of commercial property owners. This raises the risk of loan defaults, as the value of collateral depreciates. Consequently, banks could see a rise in non-performing loans, reduced profitability, and potential stock price declines. Investor confidence in these financial institutions may wane due to concerns over asset quality and loan loss provisions. Banks are likely to adopt a more cautious approach to commercial real estate lending, potentially restricting credit availability. A prolonged downturn in commercial real estate could lead to a broader economic slowdown, further challenging banks and impacting their stock performance.

Conclusion for US Commercial Real Estate Risk

The shift to remote work and subsequent reduced demand for office space have led to significant declines in commercial real estate values. Major banks with substantial exposure to commercial real estate loans are at risk of increased defaults, impacting their profitability and stock performance. Smaller banks are particularly vulnerable due to higher exposure levels. A prolonged downturn in commercial real estate could lead to broader economic challenges, further affecting the financial sector and overall market stability.

In the next section, we will explore how the upcoming US election could impact the risks we have discussed.

4. What does the Upcoming US Election Mean for These Risks?

Here are three scenarios: one where Democrats win the House and hold the majority in the Senate, another where Republicans win the House and hold the majority in the Senate, and a third where there is a bipartisan split with one party controlling the House and the other the Senate. For each scenario, we analyse the potential impact on the identified risks based on reports from research bodies[10], considering the policies that might be enacted.

Scenario 1: Kamala Harris Wins the House and Majority in Senate

Inflationary Risks and Impact on US Equity Markets

Policies: Increased government spending on social programs, infrastructure, and green energy initiatives.

Impact: Potentially higher inflation due to increased demand and government expenditure. However, these policies may also stimulate economic growth, supporting equity markets in sectors like renewable energy, infrastructure, and technology.

High Interest Rates and the US Debt Issue

Policies: Continuation of current fiscal policies, potentially leading to higher debt levels.

Impact: High interest rates could increase the cost of servicing national debt, leading to concerns about fiscal sustainability. Equity markets might face pressure due to higher borrowing costs for companies, particularly those with significant debt.

US Commercial Real Estate Risks

Policies: Support for urban development and green building initiatives.

Impact: While these policies may provide some support to the commercial real estate market, ongoing challenges such as reduced demand for office space could continue to weigh on property values. Banks’ exposure to commercial real estate could lead to increased defaults, impacting financial sector equities.

Scenario 2: Trump Wins the House and Majority in Senate

Inflationary Risks and Impact on US Equity Markets

Policies: Tax cuts, deregulation, and tariffs on imports.

Impact: Tax cuts may spur economic activity, potentially leading to higher inflation. Tariffs could increase costs for consumers and businesses, contributing to inflation. Equity markets may benefit in the short term from tax cuts but face long-term inflationary pressures.

High Interest Rates and the US Debt Issue

Policies: Policies to stimulate economic growth, potentially increasing national debt.

Impact: High interest rates could exacerbate the debt issue, leading to higher debt servicing costs. Equity markets may face volatility due to concerns over fiscal sustainability and higher borrowing costs for businesses.

US Commercial Real Estate Risks

Policies: Deregulation and tax incentives for real estate development.

Impact: While these policies may provide some relief to the commercial real estate sector, the ongoing shift towards remote work could continue to depress demand for office space. Banks with significant exposure to commercial real estate might face increased risks, affecting their stock performance.

Scenario 3: Bipartisan Government (One Party Controls the House, the Other the Senate)

Inflationary Risks and Impact on US Equity Markets

Policies: Compromise policies with limited aggressive spending or tax cuts.

Impact: Inflation risks may be moderate as extreme fiscal policies are less likely to pass. Equity markets might experience stability due to balanced fiscal approaches, although growth may be slower compared to a unified government scenario.

High Interest Rates and the US Debt Issue

Policies: Compromise on fiscal policies, leading to moderate debt accumulation.

Impact: Interest rates might rise gradually, leading to manageable debt servicing costs. Equity markets could benefit from a more predictable fiscal environment, although sectors sensitive to interest rates may still face challenges.

US Commercial Real Estate Risks

Policies: Mixed policies with potential targeted support for real estate.

Impact: Continued challenges in the commercial real estate market due to reduced demand. Banks’ exposure to commercial real estate could lead to cautious lending practices, impacting their profitability and stock performance. However, bipartisan support for certain initiatives could mitigate some risks.

Does It Matter?

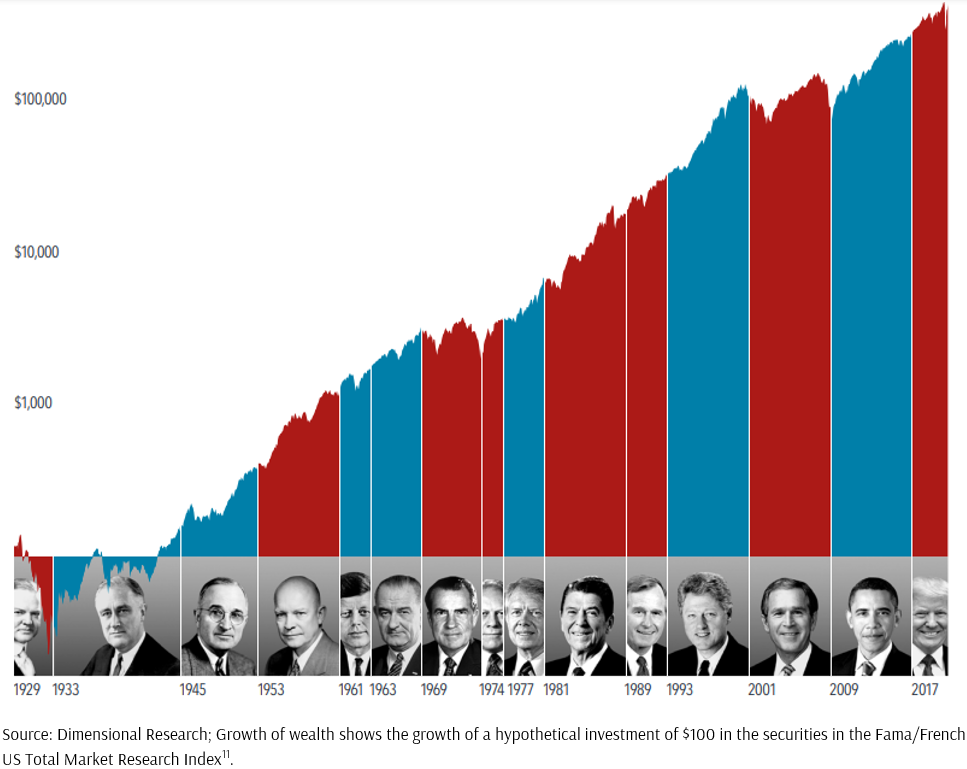

Investors often seek a link between the outcome of presidential elections and stock market performance. However, nearly a century of data shows that stocks have generally risen under administrations from both parties.

- Investors are buying into companies, not political parties. Companies focus on serving their customers and expanding their businesses, regardless of the occupant of the White House.

- While US presidents can influence market returns, many other factors also play a role, including the actions of foreign leaders, global pandemics, interest rate changes, fluctuations in oil prices, and technological advancements.

Stocks have consistently rewarded disciplined investors across Democratic and Republican presidencies (Exhibit 8). This underscores the importance of a long-term investment strategy.

In our next section, we examine concerns about the high valuations of US mega tech stocks fuelled by AI optimism. Could this be a precursor to a dot-com-like stock market crash?

Exhibit 8 – Growth of $100 in the US Stock Market (1929 – 2020)

5. Will the US Mega Tech Stocks Bring About a Dot Com Bubble Burst?

Dot-Com Bust Era (1995-2000)

During the dot-com bubble, many tech companies had little to no earnings growth. For example, Pets.com, one of the most notorious failures of the period, had no significant revenue or earnings growth before it went bankrupt. Amazon, one of the survivors, had negative cash flows and was far from profitability, with its stock price plummeting from around $100 to $7 after the bubble burst. Barron’s reported that 74% of Internet companies had negative cash flows and little realistic hope of profits in the near term. Most of the tech companies during this era had little to no fundamentals.

Earnings Growth of the Magnificent 7 (2019-2024 Q1)

The “Magnificent 7” refers to seven major US tech companies: Apple, Microsoft, Alphabet (Google), Amazon, Nvidia, Tesla, and Meta (Facebook). These companies have displayed robust earnings growth from 2019 to 2024, which contrasts sharply with the tech companies during the dot-com bubble.

1. Apple (AAPL): Apple’s earnings grew by approximately 9% annually between 2019 and 2024 Trailing Twelve Months (TTM). This growth has been fuelled by strong iPhone sales, expanding services revenue, and increasing margins on hardware.

2. Microsoft (MSFT): Microsoft reported earnings growth of about 14% annually during the same period. The company’s cloud computing division, Azure, and its enterprise software products have been key drivers of this growth.

3. Alphabet (GOOGL): Alphabet saw its earnings rise by roughly 14% annually from 2019 to 2024 (TTM). The company’s dominance in online advertising and the growth of its cloud services have underpinned this steady earnings increase.

4. Amazon (AMZN): Amazon’s earnings increased by about 21% over these years, driven by its e-commerce business and the rapid growth of Amazon Web Services (AWS), its cloud computing arm.

5. Nvidia (NVDA): Nvidia experienced an impressive earnings growth of approximately 62%[12] from 2019 to 2024 (TTM). This surge was driven by its leading position in graphics processing units (GPUs) for gaming, AI, and data centres.

6. Tesla (TSLA): Tesla’s earnings skyrocketed by 42% during this period. The company’s growth has been propelled by its electric vehicle sales, expansion into new markets, and advancements in battery technology.

7. Meta (META): Meta’s earnings grew by around 14% between 2019 and 2024 (TTM), despite facing challenges related to privacy changes and increased competition. The company’s investments in the metaverse and continued growth in its core social media platforms contributed to this performance.

Comparison and Justification

These growth figures reflect a fundamental difference between the current tech giants and the speculative companies of the dot-com era. The Magnificent 7 has posted strong and consistent earnings growth, supported by robust business models and leadership in high-growth areas like cloud computing, AI, and digital advertising. This substantial growth provides a solid foundation for their high valuations, unlike the tech companies of the late 1990s, which were often overvalued based on speculative potential rather than real earnings.

Conclusion for US Mega Tech Stocks Valuations

The comparison between the current valuations of mega tech stocks and the dot-com bubble era highlights key differences. Unlike the dot-com era, today’s leading tech companies generally have robust earnings growth and strong fundamentals.

6. Will US Equities Still Generate Returns for Investors?

The United States has consistently been a powerhouse of innovation, attracting top talent and groundbreaking ideas from across the globe. This enduring appeal stems from a unique blend of robust capitalism, a well-established ecosystem for research and development, and a culture that nurtures entrepreneurial spirit. These elements are key factors in determining whether US equities will continue to generate returns for investors.

The Case of Insulin Production: A Historical Perspective on Value Creation

In the early 1920s, a pivotal medical breakthrough took place at the University of Toronto when Professor Frederick Banting and Charles Best successfully extracted insulin from the pancreas, offering a new treatment for diabetes. Although the discovery was made in Canada, it was the American pharmaceutical giant Eli Lilly that first mass-produced insulin. This was no accident but rather a testament to the US’s superior infrastructure for commercialisation and its capitalistic drive, which remains a critical factor for equity investors.

Eli Lilly’s ability to swiftly mobilise resources, scale production, and navigate regulatory hurdles exemplifies how the US capitalist framework creates value. The company’s success in bringing insulin to the market rapidly demonstrates the efficiency of American capitalism in turning scientific discoveries into profitable ventures. For investors, this environment of robust financial support, competitive markets, and a willingness to embrace new technologies underpins the continued potential for returns in US equities.

Elon Musk’s Entrepreneurial Journey: A Modern Example of Growth Potential

Elon Musk, a South African-born entrepreneur, is a contemporary example of the US as fertile ground for innovation and, consequently, for equity growth. Musk’s ventures—including Tesla, PayPal, SpaceX, and OpenAI—have thrived in the US due to the country’s unparalleled opportunities within its capitalist ecosystem.

The US offers a unique combination of abundant venture capital, a culture that celebrates risk-taking and entrepreneurship, and a regulatory environment conducive to innovation. Tesla’s success, driven by access to substantial venture capital and government incentives for clean energy, highlights the growth potential for companies operating in the US market.

Similarly, SpaceX’s advancements in space exploration, supported by significant private and public investment, reflect the US government’s collaboration with private enterprises to push technological boundaries. For investors, these examples illustrate the continued capacity of US equities to generate strong returns, particularly in sectors at the forefront of innovation.

Conclusion: The Ongoing Promise of US Equities

The examples of Eli Lilly’s pioneering work in insulin production and Elon Musk’s entrepreneurial ventures underscore why the US remains an attractive market for equity investors. The American capitalist model, characterised by its financial resources, infrastructure, and supportive culture, continues to turn groundbreaking ideas into profitable realities.

As long as the US maintains its dynamic ecosystem that fosters innovation and supports entrepreneurial endeavours, US equities are likely to continue generating returns for investors. This enduring environment of innovation, risk-taking, and investment in new technologies ensures that the US will remain a leader in value creation, making its equity market a viable option for those seeking sustained returns.

An Overview Summary

The analysis of the US equity landscape reveals several key risks, including inflation, high interest rates, and challenges in commercial real estate. Persistent inflation reduces consumer purchasing power and increases business costs. Meanwhile, aggressive interest rate hikes aimed at controlling inflation have led to higher borrowing costs and market volatility. The commercial real estate sector faces significant risks due to the shift to remote work, resulting in decreased demand for office space and potential loan defaults, particularly affecting smaller banks.

Despite these challenges, the fundamentals of leading tech companies remain strong, although their high valuations raise concerns about potential market corrections reminiscent of the dot-com bubble. Historical trends suggest that US equities can still generate returns for investors, emphasising the importance of a long-term investment strategy.

Conclusion: The US Equity Landscape

Despite the array of risks and uncertainties within the US equity landscape, the market’s historical performance offers valuable lessons for investors. The unpredictable nature of the market underscores the importance of maintaining a long-term investment strategy. Empirical evidence, including the actual stock market returns in 2023 compared to economists’ forecasts, demonstrates that staying invested can yield substantial rewards over time. Furthermore, the resilience of the market through various political and economic cycles, including the influence of US presidential elections, reinforces the potential for continued returns.

Investors should recognise that while short-term volatility is inevitable, the US market’s robust capitalist framework, coupled with its culture of innovation and entrepreneurial spirit, provides a fertile ground for sustained equity growth. Therefore, maintaining a disciplined, long-term investment approach remains crucial for navigating the complexities of the US equity landscape and capitalising on its enduring promise for returns.

Do note that while we have covered the key themes that have driven the US markets in the past couple of years, the US landscape is complex, and we are unable to cover every scenario in exhaustive detail. However, we hope that what we have covered will provide our readers with a better understanding of the US equity market.

Thank you for taking the time to read the final segment of our monthly market review series, which focuses on the US equity landscape. Moving forward, our market review will return to discussing the monthly market performance.

We understand that recent market volatility can be unsettling. If you have any concerns or feel uneasy about the current market conditions, please do not hesitate to reach out to your Client Adviser.

Our team is here to provide guidance and support to help you navigate these times with confidence. We appreciate your trust in us and look forward to continuing to assist you in achieving your life goals.

– Footnotes –

[1] ‘Bedlam’ in UK as Air and Rail Travel Hit by Global It Outage

[2] As it happened: IT outage hits businesses worldwide, disruption triggered by CrowdStrike software update.

[4] As of June 2024, CPI data.

[5] Comparing the Speed of U.S. Interest Rate Hikes (1988-2022)

[6] Half of the biggest global companies plan to cut office space. US cities will suffer most.

[7] Commercial real estate exposure at US banks

[8] Major U.S. Banks With the Most Commercial Real Estate Exposure

[9] From US$332 million to US$8.5 million: Office block’s price plunge captures Manhattan’s shocking office collapse

[10] Oxford Economics: 2024 US Presidential Election

Allianz Global Investors: US elections monitor: looking back to look forward

[11] Fama/French Total US Market Research Index: This value-weighed US market index is constructed every month, using all issues listed on the NYSE, AMEX, or Nasdaq with available outstanding shares and valid prices for that month and the month before. Exclusions: American depositary receipts. Sources: CRSP for value-weighted US market return. Rebalancing: Monthly. Dividends: Reinvested in the paying company until the portfolio is rebalanced.

[12] The average EPS Growth Rate is determined by analysing the data from 2019 to 2024 (Trailing Twelve Months) provided in this link.

To learn more about our purpose-driven approach towards investment management, please visit this link.

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current estate plan, investment portfolio, financial and/or retirement plan, make an appointment with us today.