The number one excuse I hear for not saving money is that everyone wants to wait until they have more. Well, with compound interest on your side, it is not a good enough reason.

Compound interest sounds incredibly boring but you don’t really need to understand the dull formulas behind it. You just need to know it can have a magical effect on your long-term savings and you don’t need to do anything to benefit from it. However, my Personal Finance Quiz demonstrated that it’s not well understood.

The Huge Impact Is Under-Estimated

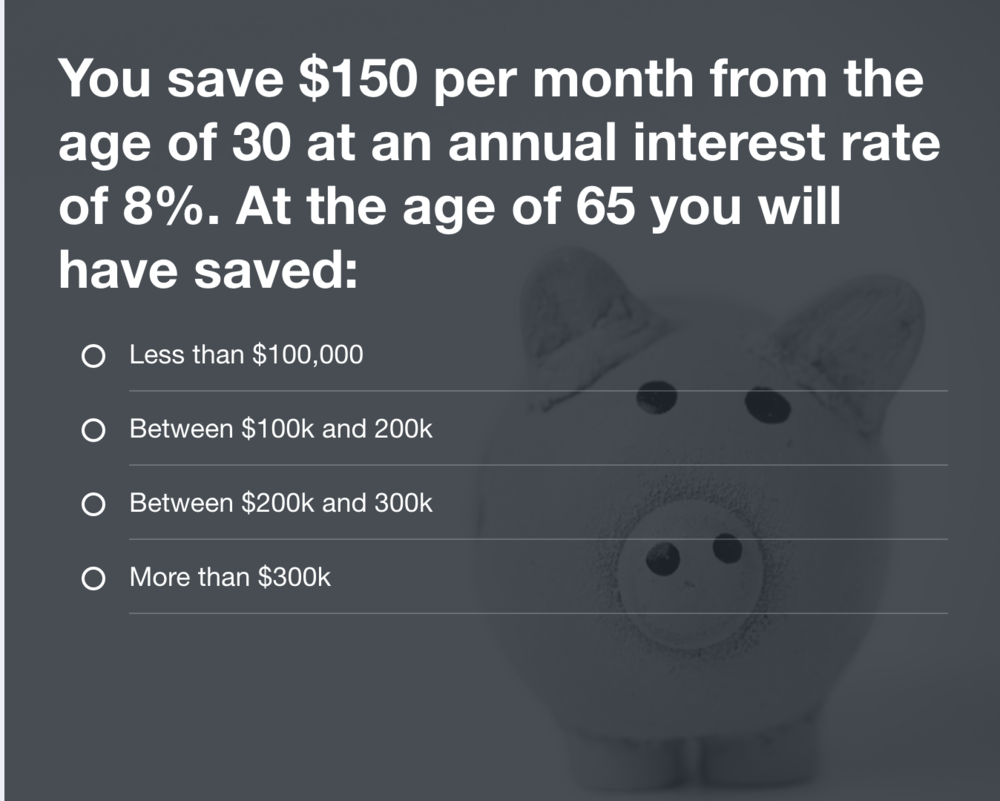

In my quiz, I asked:

Only 33% of people who answered got this right – it’s actually $327,670.74. You would have made $262,520.74 in interest from depositing just $63,150. This was, by far, the question with the highest number of incorrect answers.

So How Does Compound Interest Actually Work?

Just think of it as interest on interest.

Investopedia defines it as:

“Compound interest is interest calculated on the initial principal and also on the accumulated interest of previous periods of a deposit.”

It’s easier to understand visually so let’s walk through some pretty charts.

Understanding The Amazing Effects On Your Money

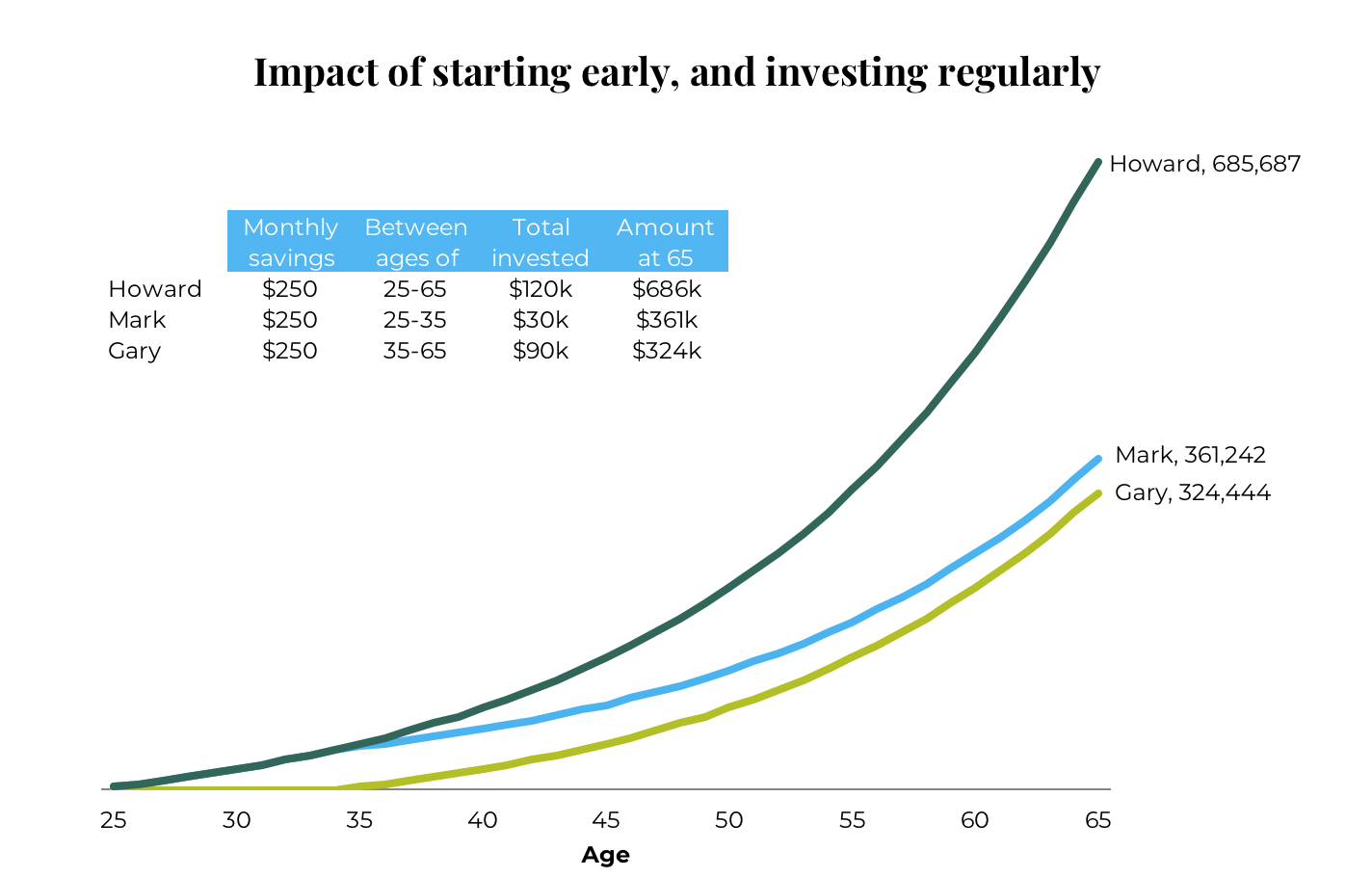

1. Get started early and benefit for longer

The earlier you get started, the more you earn even if you stop regularly adding to an investment. It’s much harder to catch up later. We can see this from the example below – Mark got off to an exemplary start in his savings life and put away $250 per month for 10 years from the age of 25 and then stopped. His total savings at 65 are worth almost $37k more than Gary who put away the same amount from the age of 35 for 30 years. Howard was well-behaved all his life and diligently put away $250 amount for all his working career from the age of 25 and his savings leave the other two for dust – he has more than $300k more than either of them.

Don’t wait until you earn more to start ‘seriously’ saving – this is just as true for 40-year-olds as it is for 22-year-olds. Put whatever you can away now.

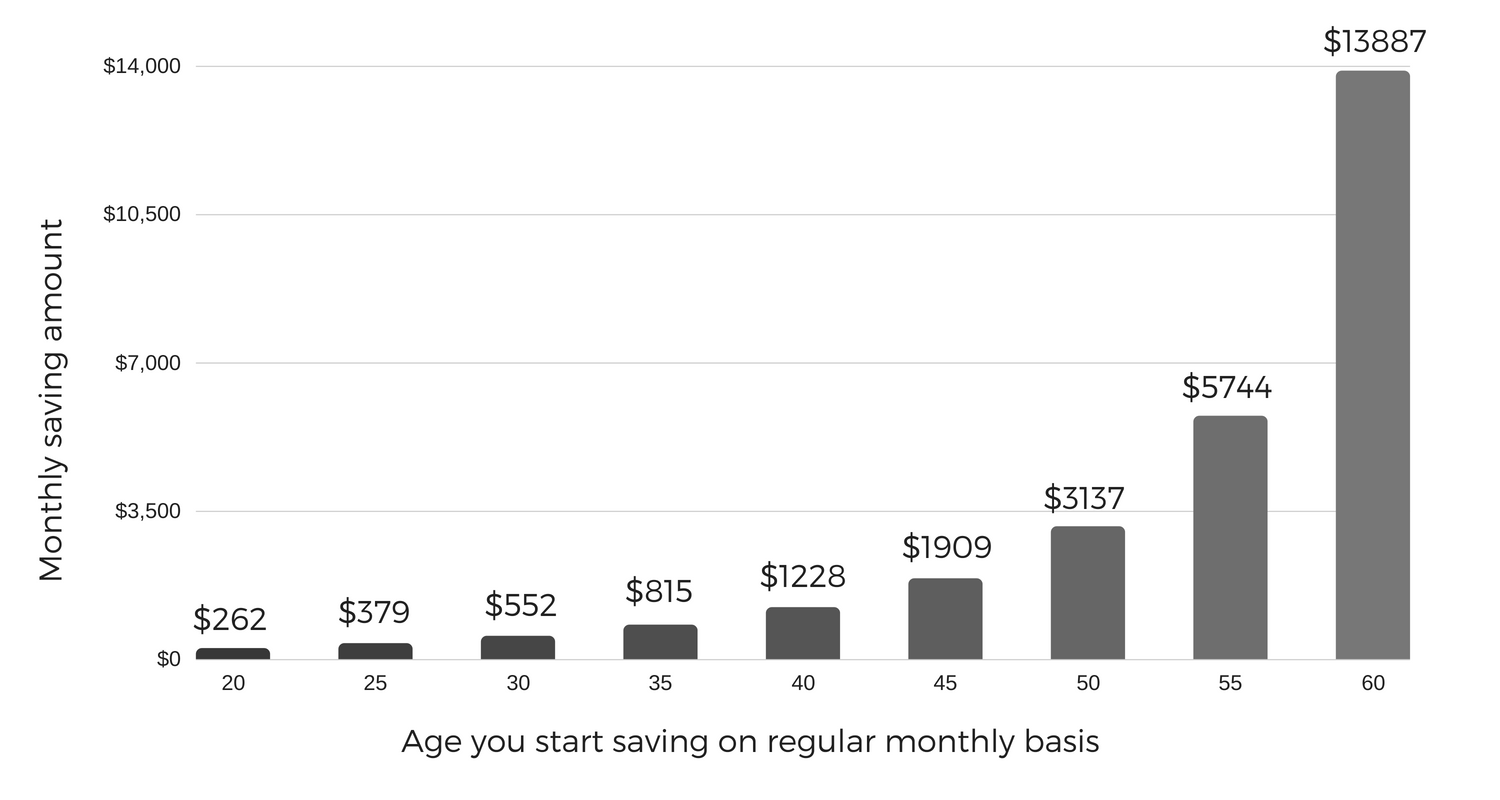

2. It can turn you into a millionaire if you get going early enough

It’s the chart you see all the time but it’s worth repeating. To have a million at 65, you don’t need to save as much per month when you are younger as you do when you are older. Right now, you probably wish you had started saving smaller amounts but it’s not too late. Yes, you might not be able to save $1000 per month to catch up but be serious about what you can save and start putting that away. As the old saying goes, you will never be as young as you are today.

Monthly savings required to have $1m at 65

3. Small percentage changes in interest rates have an enormous effect.

Let’s say you come into some money at 35 – $25k to be exact. You could have been lucky enough to have got a big bonus that year or it could be an inheritance from a long-lost aunt. You sensibly decide to put this away for 30 years. Take a look at the following pie charts – they show the impact of interest rates on your original $25k windfall.

Rather than leaving it floundering in a high-street savings account earning next to nothing, instead, you decided to put it into a low-cost index tracker earning you 7% interest per year. You made a wise choice – thanks to compound interest, your account balance is now $203k and the interest is responsible for 88% of that.

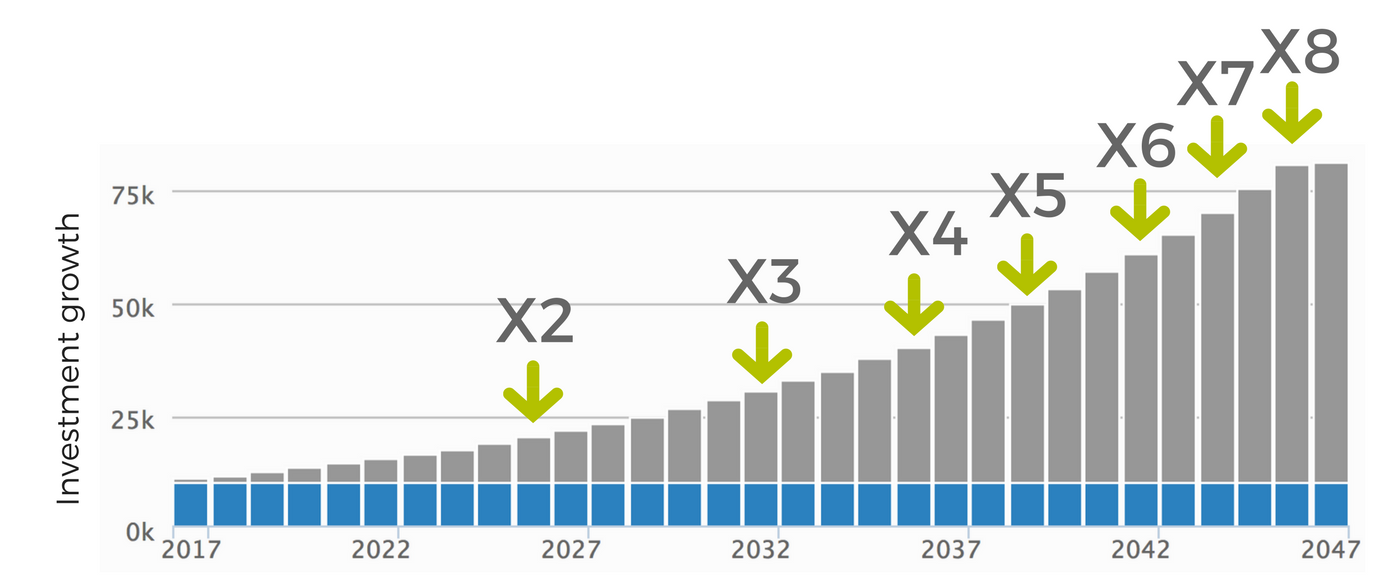

4. Your money starts doubling quicker and quicker over time

In this example, we look at $10,000 over a 30 year period earning 7% annual interest. By year 10, it has very nearly doubled, then it only takes another 6 years to be worth three times what you originally invested. You can see the numbers of years it takes for your money to multiply gets shorter and shorter as time goes on. The lesson here is just to put your money away and leave it alone.

Want To Know How To Work It Out?

If you want to get technical then this if the formula for how to work out annual compound interest:

A = P (1 + r/n) (nt)

Useful, eh? No, it’s not as you will never use this to work out compound interest. There are plenty of compound interest calculators online to do all the work for you.

If you like to impress people at dinner parties with your maths skills or do a lot of pub quizzes then you might be interested to know about ‘The rule of 72’.

The rule of 72 calculates the approximate time over which an investment will double at a particular interest rate. You can do this by dividing 72 by the interest rate.

For example, an investment that has a 7% annual rate of return will double in 10 years (as we saw in the chart above).

3 Rules Of Compound Interest

1. Start as early as you can: the more you can save in your 20s the better, as we have seen from the example above. Even if you are in your 30s or your 40s don’t leave it any longer- save what you can as soon as you can.

2. Keep investments for a long period: resist the urge to withdraw any money if you don’t have to. Make sure you have your rainy day savings that are easily accessible for emergencies.

3. Keep adding to your original investment: the more you put in, the more interest you will earn. Whenever you have a pay-rise, a work bonus or a mini-windfall, commit to putting part of it away in your long-term saving pot.

This is an original article written by Max Keeling, Client Adviser and Head of Expat Division at Providend, Singapore’s Fee-only Wealth Advisory Firm.

For more related resources, check out:

1. Know What You Can Control As An Investor

2. Do Low Cost Investments Give Investors Higher Returns

3. The Importance Of Building Wealth With A Purpose

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current investment portfolio, financial and/or retirement plan, make an appointment with us today.