In the previous article, I shared that by starting the conversation about finances and retirement planning with your other half allows both of you to think about your desired current and future lifestyle. More importantly, how you can balance your finances to enable you to achieve the lifestyle you want for your family.

As parents, we tend to be so caught up with the day-to-day activities at work and as well as family commitments such that retirement planning usually takes a backseat in our lives. Before we know it, years would have passed us by, without us taking any action, as we hustle through a series of financial life transitions – having another child, changing careers, starting your own business.

Part II: Thinking about retirement now allows you to take the appropriate actions early to secure your future.

“Without strategy, execution is aimless. Without execution, strategy is useless.”

— Morris Chang, CEO TMSC

It is most unfortunate that retirement planning often falls into “the important yet not urgent” list. But life is not a rehearsal. Delaying your retirement planning and saving effort essentially means that you must come up with a tremendous amount of additional money to catch up to a balance that you would have had if you started saving regularly earlier.

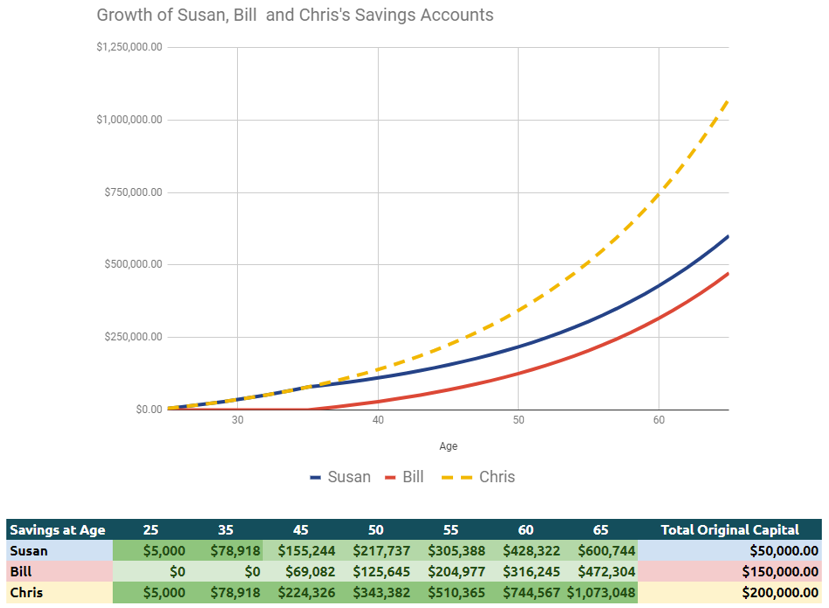

Let’s take a look at this example to see the importance of starting early. Susan, Bill and Chris all wanted to save for retirement. However, they all took different approaches to do it:

- Susan decided to start saving at age 25 but stopped at age 35. From 35 onwards, she decided to let the money she saved grew on its own

- Bill was late to the game. Unlike Susan, he only started saving from age 35 till 65, which was his retirement age

- Chris, on the other hand, did the same thing as Susan, only that he continued to contribute till age 65.

Each of them contributes $5,000 a year into their savings accounts according to their plan. Assuming their saving accounts grow at a rate of 7% per year, the chart below shows how much each of them would have accumulated at the age of 65.

We notice a few things:

- Susan saved up much more than Bill even though Susan’s capital put in was much less than Bill. Bill has put in 3 times more but ended up with lesser.

- If Susan and Bill had similar needs from age 25 to 65, Susan could afford to save less. She could lead to a better quality of life because she could devote more of her income to spend now rather than later and achieved the same result as Bill. Bill would have to continuously contribute $5000/year, an amount he could have put towards improving his family’s life.

- As Susan started early, she also had the opportunity to use a lower risk financial asset to grow her money. While the returns might be lower, she would have gained greater peace of mind and would be able to stick with the financial plan better. She could do that because of the savings she had built up in the first 10 years.

- To catch up with Susan, Bill would have to put in more money per year!

- Chris, by virtue of starting early, and had continued to contribute, built the most wealth. He is probably the only one who has decoded the magic of compounding and wealth-building!

At the end of the day, it is not just how much you save but it is when you start saving that truly matters. Again, life is not a rehearsal, I truly encourage you to take action now.

Do stay tuned for the next article where we will explore why your action now can benefit your children’s future greatly.

This is an original article contributed by Loh Yong Cheng, Client Adviser at Providend, Singapore’s Fee-only Wealth Advisory Firm.

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current investment portfolio, financial and/or retirement plan, make an appointment with us today.