Note: This article has been updated on 12 April 2024.

Mention what you could optimize about your CPF and the conversation will naturally shift to tips and tricks you could do to optimize your money with your CPF OA, CPF SA, and CPF Medisave accounts.

We don’t blame people for their focus on these 3 CPF accounts.

If these are the accounts in which your actions can lead to a better financial outcome for your family and yourself, you should see what you can do to optimize them as part of your overall financial plan.

However, the account that people know less about is your CPF Retirement Account (RA). This is a unique account that will be created for you at a later stage of your life.

We talk about it less because likely the larger majority are still in the accumulation stage of their lives.

Your CPF Retirement Account (RA) nevertheless is as important and needs to be managed properly.

In this article, I will share with you maybe some things you need to know about your CPF Retirement account and some optimizations that you may wish to consider concerning your CPF Retirement accounts.

1. What is the Purpose of Your CPF Retirement Account (RA)?

The money in your CPF Retirement Account is to set aside money for your retirement.

This enables you to enrol in the Retirement Sum Scheme or CPF LIFE so that you can receive monthly income payouts to pay for your expenses in retirement.

2. When will the CPF Retirement Account Be Created?

When you turn 55 years old, your CPF Retirement Account will be created for you.

3. When will CPF Automatically Transfer Money from your CPF OA and SA into CPF RA?

There will be two periods where the monies from our CPF OA and SA be automatically transferred to your CPF RA.

The first period is when the CPF RA is created at 55 years old.

An amount equivalent to the Full Retirement Sum (FRS) will be transferred from your CPF SA and CPF OA.

The second period is six months before you reached your payout eligibility age. Your payout eligibility age is currently 65 years old, and you may postpone to 70 years old.

CPF will write to you three months before the transfer is going to take place to explain to you the options.

Fun Fact: The transfer in the second period is for people who have not met their Full Retirement Sum but not on the Basic Retirement Sum scheme (meaning they did not pledge their property). This is to transfer the amount that is built up in both CPF SA and CPF RA from your employment contribution.

4. What is the Basis of Evaluation for Whether You Meet Your Full Retirement Sum, Basic Retirement Sum, and Enhanced Retirement Sum?

As I have said, the Full Retirement Sum, Basic Retirement sum, and Enhanced Retirement Sum are projected to rise annually.

CPF will measure whether the balances in your CPF RA hits the FRS, BRS, or ERS.

This balance excludes amounts such as:

- Interest earned

- Any government grants received

It includes:

- Monthly payouts

- Payout eligibility age lump sum withdrawal

- Retirement Sum Topping Up Amount (RSTU)

This equation comes into question if you are evaluating how much you can top up additionally into your CPF RA.

The interest earned in your CPF RA does not affect the ERS measurement. For example, suppose you have $192,000 in your CPF RA at age 57. At the start of 58 years old, your CPF RA will earn $8,000 in interest.

When you are 58 years old, the ERS is $200,000.

While you have $200,000 in your CPF RA due to the principal + interest, CPF measures how much you can top up based on $192,000 vs the $200,000 ERS limit.

This meant that you can further top-up.

5. Will there be People Exempted from the Automatic Transfer of Monies to Your CPF Retirement Account?

CPF Members under the Medical Grounds Scheme will not be affected by the transfer.

CPF Members who have an existing pension, or annuity policy bought using cash or CPF savings under the CPF investment scheme, will not be affected by the transfer as well.

6. Can you Transfer More Money into Your CPF Retirement Account after the Automatic Transfers?

Yes, you can.

If you transfer more money into your CPF RA, this will enable you to enrol in the Retirement Sum Scheme or CPF Life with greater monies, and allow you to receive a larger monthly income payout when you decide to start taking income after your payout eligibility age.

You can contribute up to the current Enhanced Retirement Sum (ERS) (that is, the ERS you see today). The Basic Retirement Sum, Full Retirement Sum, Enhanced Retirement Sum shifts up gradually over time.

You are allowed to contribute to the prevailing Enhanced Retirement Sum (not just the Enhanced Retirement Sum when you reach age 55)

This allows you to greatly enhance your CPF LIFE annuity payout.

You can top up using

- Cash

- CPF SA or CPF OA monies not affected by the automatic transfers

7. Can I limit the Amount of Money Transferred into CPF Retirement Account?

By default, the monies from your CPF SA and OA will be transferred to your CPF RA, to top it up to your applicable Full Retirement Sum in cash.

The applicable Full Retirement Sum (FRS) is the Full Retirement Sum when you turn 55.

If you have set aside the applicable FRS, then no automatic transfer will take place.

If you have met your retirement sum in cash and property pledge, you can opt to retain your property pledge.

A property pledge is created if you choose to withdraw money from your CPF Retirement Account in excess of the Basic Retirement Sum (which is half of the FRS) under the property pledge withdrawal rules.

When the pledged property is eventually sold, the amount of pledge is returned to the CPF account from the proceeds of the sale (You can re-use the CPF monies from this sale for subsequent housing purchases or draw it down if you have entered retirement).

8. Can I use the Monies in My CPF Retirement Account for My Property?

For some, you might still need to service mortgage with your CPF monies or use the sum to purchase a property.

You can tap upon the money in your CPF Retirement Account (RA) but that will depend on

- when you purchase your property

- the age of your property, relative to your own age

If you bought your property before 10 May 2019

You can use your Retirement Account (RA) savings (excluding interest earned, grants received from the Government, and top-ups made under the Retirement Sum Topping-up Scheme) minus your CPF Basic Retirement Sum (BRS) for the property.

As an example, if you turned 55 years old on 1 January 2016 and you have set aside $100,000 in your CPF RA.

The BRS applicable to you is $80,500.

You can use $100,000 – $80,500 = $19,500 to pay for your property.

If you bought your property after 10 May 2019

If the Remaining Lease of your Property Covers you till 95 years’ old

You can use your RA savings minus BRS for the property.

This is similar to the previous section.

If the Remaining Lease of your Property DOES NOT Cover you till 95 years’ old

Then you cannot use your Retirement Account (RA) savings for the property as the money needs to preserve for your needs.

It will not be prudent to commit more of funds meant for your retirement to a property that will not be around for the entire duration of your retirement.

NOTE: Monies Top-Up through Retirement Sum Topping-Up Scheme Cannot Be Used for Housing

The objective of such top-ups is to provide a member with a monthly income during retirement.

Therefore, such top-ups cannot be withdrawn in a lump sum or used for housing payments

9. Can You Withdraw Retirement Sum Topping-up (RSTU) Monies from Your CPF Retirement Account?

CPF Members can top up their own CPF SA before age 55 and CPF RA after age 55 under the Retirement Sum Topping-Up Scheme (RSTU).

Doing this can reduce their taxable income.

They can do the same under RSTU for their spouse and parents as well.

The money under RSTU is meant for your retirement and will be transferred into your CPF RA.

However, you cannot withdraw the RSTU monies in your CPF RA, even if you have pledged your property and have the equivalent of Basic Retirement Sum in your CPF RA.

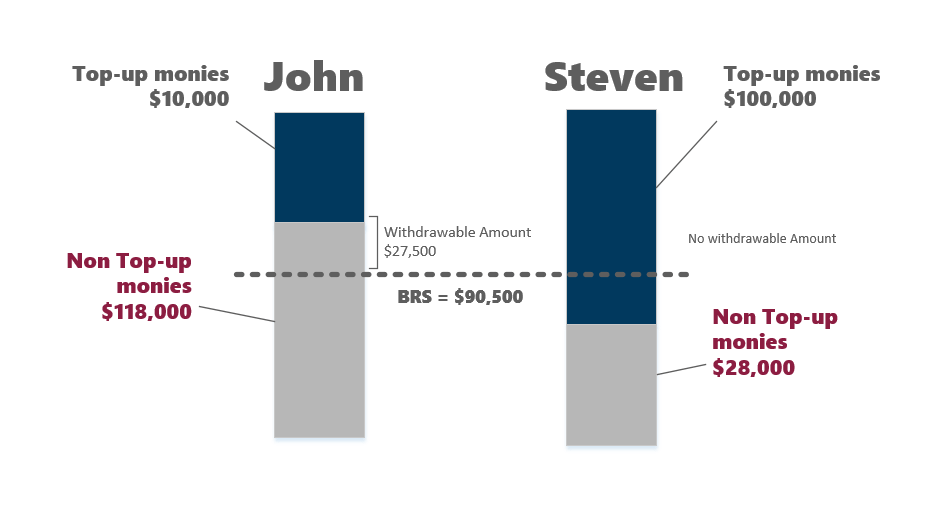

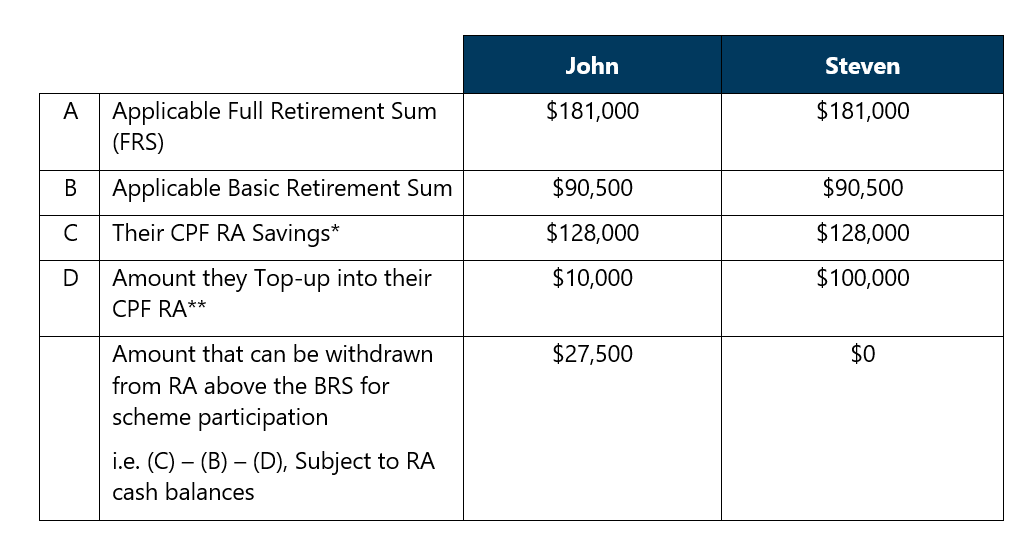

Here is an example to help illustrate.

John and Steven both have a similar amount in their CPF RA ($128,000). Both decided to pledge the property they own to CPF. Thus, they can withdraw from their CPF RA an amount net of the applicable Basic Retirement Sum which is $90,500.

The difference between John and Steven is that John has in the past topped up $10,000 in total into his CPF SA before it was transferred to his CPF RA. Steven has topped up $100,000 into his CPF SA before it was transferred to his CPF RA.

John can withdraw $27,500 after setting aside the BRS sum of $90,500 and $10,000 that he topped up.

Steven cannot withdraw anything because the BRS sum of $90,500 and $100,000 that he topped up exceeded what is in his CPF RA Savings.

The key thing to remember is that top-up monies, after being transferred to the CPF RA, cannot be withdrawn.

(This scenario is very possible if a parent decides to top-up his or her child’s CPF SA at a very young age till the child’s Full Retirement Sum)

* Refers to cash set aside in CPF RA (excluding amounts such as interest earned, any government grants received) plus amounts withdrawn such as monthly payouts and payout eligibility age lump-sum withdrawal. Includes Top-up monies as well.

** Includes top-up and accrual interest transferred from CPF SA to CPF RA when a member turns 55.

10. Can You Prevent Your CPF SA to be Transferred to Your CPF RA?

The SA Shield no longer applicable because the SA account will be closed for members age 55 and above from 2025 onwards.

CPF Retirement Account is an Integral Part of Your Sustainable Spending Plan

You may be less acquainted with your CPF Retirement Account now but eventually, the account will have an important role in your financial plan.

The monies in your CPF RA will eventually be used to purchase CPF LIFE, an annuity that provides recurring passive income as long as you are alive.

Currently, there is no private annuity plan with features and returns that could rival the CPF LIFE. From what we learn today, you can make a few strategic manoeuvres to enhance this lifelong annuity income.

You can incrementally top up your CPF RA as the ERS rises year on year.

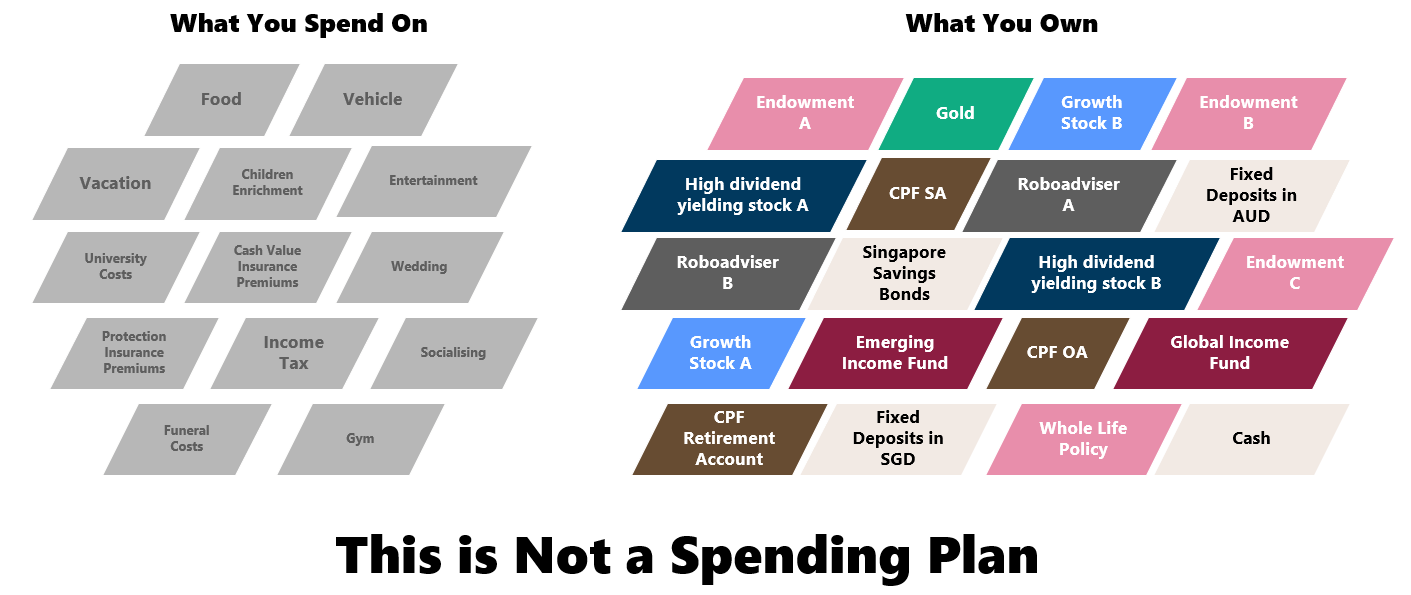

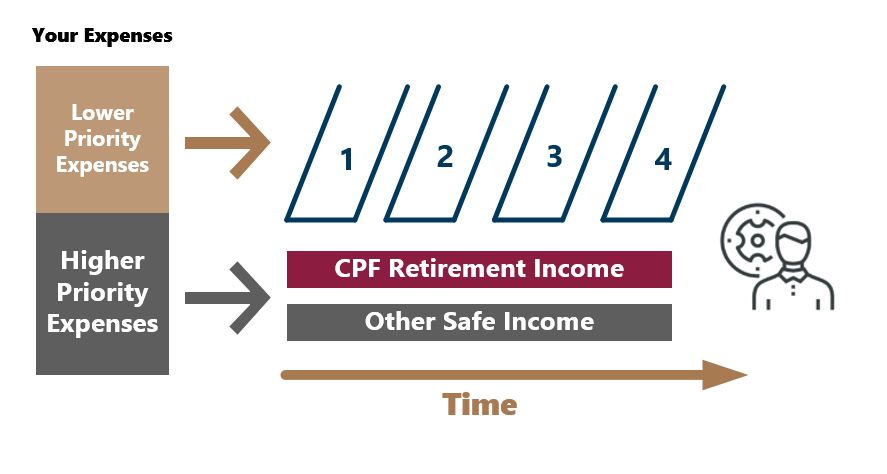

Despite how well crafted your CPF Retirement Account is, it is just a cog in your overall spending plan. A well-thought-out spending plan allows you to know from what age to what age, your income to pay for your expenses will come from which asset.

If you do not have a well-thought-out spending plan, you may not be adequately prepared for your financial independence.

While the CPF LIFE annuity scheme may provide income for life, by devoting all your capital to CPF retirement income, you might not have adequate assets to create an income stream that is more inflation-adjusted. You may lose too much purchasing power that your income does not keep up with inflation.

CPF LIFE annuity income, your insurance endowment plans, dividend income, rental income and manage investments are standalone tools.

Each has its strong points and area of weakness.

If you are able to put them together, you will have a plan.

At Providend, we believe that a rich retirement life should be supported by a sustainable spending plan. A sustainable spending plan is one where different income sources and assets come together to provide the adequate income you need for your lifestyle.

Let us know if you would like to find out more about how you can create a sustainable spending plan.

This is an original article written by Kyith Ng, Senior Solutions Specialist at Providend, Singapore’s Fee-only Wealth Advisory Firm.

For more related resources, check out:

1. Frequently Asked Questions About CPF

2. Assets That Cannot Be Distributed Via A Will | CPF Monies & Joint Accounts

3. Understanding CPF Part 5: Minimum Sum Scheme vs CPF LIFE Plans

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current investment portfolio, financial and/or retirement plan, make an appointment with us today.