Getting retrenched can feel like being punched in the gut. For some, it comes as a surprise; for others, they see the writing on the wall and have to deal with gut-wrenching uncertainty until notice is served. Either way, there is a lot to deal with emotionally in the form of shock, anxiety, anger and even grief.

The loss of income, or the uncertainty of it, commonly layers on more worry to this whole situation, especially if there are dependents to feed and bills to pay.

With so much going on, feelings of disorientation and loss of control can set in.

How can we quickly gain back our sense of agency and focus? Whilst a wealth plan is not the cure, having a solid one in place can help keep one grounded when everything else feels like it’s slipping away.

That said, no one should wait to plan only after retrenchment has happened. Through a simulated case study in this article, it is my hope that the reader can glean insights to be better prepared should retrenchment hit — and for those already dealing with retrenchment, that there are sufficient handles to soften the blow for themselves.

Case Study Scenario

Xiao Ming (fictitious) holds a rather senior position in a project management role and has just been notified that his department will be dissolved. While the news had caught him off-guard, he knows that the industry he is in has been undergoing much consolidation in recent years.

He has two months remaining before he is officially out of a job. His unvested stock options will be forfeited, but he is entitled to a severance pay roughly equal to three months of his current pay.

He is aged 44 this year and has two children in the primary-school-going age. Thankfully, his wife, Jane, has a stable career, but she earns around 40% less than him. Xiao Ming knows that he must continue looking for the next job to ensure that he can meet the needs of his future goals – the two most important ones being his children’s tertiary education needs and his own retirement plans.

Given that his industry is consolidating, he will likely need to find a smaller role in the same industry or switch to a different industry altogether. Both options would mean that he cannot expect his new job to pay him at his current levels. The bottom line is that he will most likely have less to spend and save.

He arranges a meeting with his wealth adviser to share 2 immediate worries:

- Will he be able to minimise the disruption to his family’s current lifestyle?

- Will he have enough for his future goals and needs?

Step 1: Deal With Immediate Needs First

Xiao Ming needs time to assess his situation and explore his options. His adviser first gets him to take stock of the available emergency buffers he currently has. He needs to assess how long he can maintain his current lifestyle without too much disruption to what Xiao Ming has been planning for. This will also set a basis for how much time he has to search and prepare for his new job.

Cash and cash equivalents, such as fixed deposits and short-term treasury bills, work out to around six months’ worth of expenses. Including his severance pay, he has roughly nine months of runway to get things in order and start a new career.

Step 2: Get a Lay of the Land

When in unfamiliar territory, begin by assessing the landscape. His adviser asks him to think about the options he has for his next job and the future income potential.

Xiao Ming has had various job offers in the past, and coupled with an initial online search, he estimates a potential income range that he could reasonably expect. On the lower scale, he could be looking at a drop of around 35% from his current income. The lower estimates are demoralising, but to be conservative, he decides to plan with less.

He sends the following information of his current household income versus his projected estimates to the adviser.

Step 3: Assess the Impact on the Short Term and the Long Term

With reference to their current plan, the adviser breaks down the potential impact on their current cashflow positions. They have consistently been saving around 30% of their income, so the adviser uses that as a basis.

Looking at the projected cashflows, Xiao Ming and Jane realise that they may have to make some difficult decisions. If they try to save at the same level as they currently do, they may have a tough time adjusting their lifestyle — but if they save too little, they may not be able to meet their goals.

The Short-Term Impact: Assess the Changes Needed to Expenditure

Whilst Xiao Ming feels an impulse to dramatically reduce expenses, Jane reminds him to be mindful of making lifestyle adjustments that could be detrimental to the development of their two young children.

Sensing an impending argument, their adviser gets both to list out their household expenses in greater detail and segregate them into fixed and variable categories before getting together for a discussion. Fixed expenses are typically constant and recurring expenses like their home mortgage instalments, car loans, school fees, and monthly subscriptions for internet or gym memberships. Variable expenses are any other expenditure that fluctuates. Examples could include petrol, groceries, dining out, shopping, etc.

Both categories will contain essential and discretionary items, but often, it may not be easy to discern because how essential an expenditure is can be very subjective. In Xiao Ming’s and Jane’s case, obvious items like club memberships were easy to cut, but one contentious item popped up during their discussions – that of enrichment classes. Xiao Ming was of the view that this was discretionary, but Jane disagreed.

She reminded him of one money value they have in common: the best way to give their children a head start in life is to equip them through education and skills.

They came to an agreement, and after estimating the reductions to other expense items, both were quite relieved to find out that it is still possible to reduce their expenses to somewhat match the new reduced number without sacrificing what was important to them.

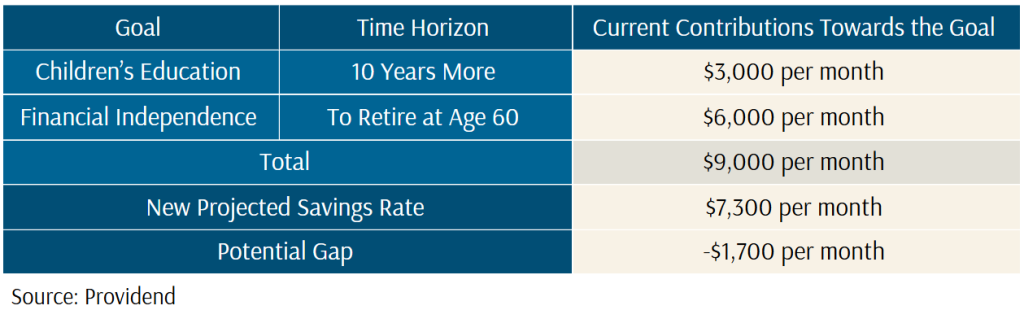

The Long-Term Impact: Assess the Ability to Meet Future Life Goals

Next, their adviser pulls out their planned goals and how much of their current savings go towards them.

Aligned with their values of prioritising education, both Xiao Ming and Jane easily agree to try and first maintain their savings contributions towards their children’s tertiary education goal and reduce their contributions to their retirement goal.

This is a trade-off that they willingly make after having that discussion about what is more important to them. They also feel that their retirement goal is more flexible because they have options. For example, they are prepared to work beyond their original target of retiring at age 60. If even that is not sufficient, they can consider either lowering their planned retirement expenses or downgrading from their current property to supplement their retirement needs.

As for their children’s education goal, they want to be fully prepared, should the opportunity ever arise for their children to pursue their preferred choice of study.

A Case Study Scenario Wrap-up

With greater clarity and knowing that his future is relatively secure even with a relatively large drop in earning potential, Xiao Ming’s sense of calm and confidence returns, allowing him to focus on getting his career back on track.

Conclusion: Your Wealth Plan Can Be Your Bedrock

Firstly, through this case study scenario, I hope to demonstrate how Xiao Ming’s wealth plan has kept him and Jane steady through the many distracting thoughts and emotions of this situation.

His plan also provides a structured approach to input different data he has gathered to make comparisons and weigh the trade-offs. There can be greater clarity over immediate needs versus longer-term needs. More importantly, having Jane involved from the beginning made it that much easier for discussions to flow constructively.

Secondly, I also hope to demonstrate that in such a critical situation, a good wealth plan and adviser focuses on areas that are within one’s control, such as checking in on cashflow positions, earnings and savings potential, and goal realignment. Financial products or instruments are really secondary and probably irrelevant as tools to provide constructive progress under such situations.

Finally, I hope that this case study showcases how a wealth plan is not only built upon goals, but also upon one’s money values and how both of these elements should be infused right from the start when formulating a plan.

At Providend, good financial planning isn’t just about the numbers — it’s about our clients, and in this case, Xiao Ming and Jane’s family. It is only through deep conversations with them over the years, that they are able to gain clarity on what matters most in their lives and what needs to be done to get there, both financially and non-financially, with our adviser guiding them through life’s unexpected situations.

Because when life throws a curveball — like a retrenchment — it’s not a fancy product or market return that gives you peace of mind. It’s having someone who understands your values, your needs, and your bigger picture, walking the journey with you.

This is an original article written by Ray Zheng, Client Adviser at Providend, the first fee-only wealth advisory firm in Southeast Asia and a leading wealth advisory firm in Asia.

For more related resources, check out:

1. Navigating Financial Challenges Post-Retrenchment

2. How to Know If You Are Financially Secure and Don’t Need a Job Anymore

3. How to Make Life Decisions

Download our Investment eBook titled “A More Reliable Way to Get Enough Investment Returns: Even During Times of Market Uncertainty” here.

Through deep conversations with our advisers, you will gain clarity on what matters most in life and what needs to be done to live a good life, both financially and non-financially. Learn more about our investment philosophy here.

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current investment portfolio, financial and/or retirement plan, make an appointment with us today.