Executive Summary

- March was a challenging month for global markets, as the escalating US-Israel conflict with Iran and the near-total shutdown of oil flows through the Strait of Hormuz sent reverberations across all major asset classes. Equities declined sharply, while bond yields surged, as markets repriced the inflation and monetary policy outlook from rate cuts to rate holds and potential hikes. Crude oil was the dominant story, with Brent surging 63.29% and WTI gaining 51.27%, while Gold and silver fell despite the geopolitical turmoil, as margin calls, forced liquidation and some central bank selling overwhelmed safe-haven demand.

- The evolving oil supply crisis and its implications for inflation, monetary policy, and the global growth outlook are the focus of this month’s discussion. We address the state of Strait of Hormuz disruptions, the scenarios for oil price normalisation, the impact on Asia and emerging markets, and what a potential US withdrawal without a deal could mean for supply.

- April has opened with oil prices continuing to rise, with physical Brent Crude Oil spot prices hitting $141 per barrel, its highest since 2008. However, the final week of March brought an important inflection point, with Fed Chair Powell’s comments at Harvard signalling that the Fed is inclined to “look through” the oil price shock, pushing hike odds from above 50% to near zero, providing significant relief for bond markets. Value and small cap factors have continued to hold up well relative to large cap growth, and the structural supports for diversified portfolios remain intact even in this period of elevated stress.

March Market Summary

In March, what began as a sharp but initially orderly market reaction to the late-February strikes on Iran escalated as the Strait of Hormuz effectively shut down, global energy supplies tightened at a frenetic pace, and the entire framework for monetary policy in 2026 was upended in the space of a few weeks.

The first week set the tone. Iran’s retaliation against tanker traffic and regional oil infrastructure sent crude oil surging past $80 within days, its highest level since mid-2024, and the Dow briefly plunged over 1,100 points in a single session before partially recovering. Airlines, industrials, and consumer-facing companies led the sell-off as markets began pricing in the second-order effects of an energy shock.

As the month progressed, the supply shock deepened. Flows through the Strait of Hormuz collapsed to approximately 6% of normal levels. Iran struck tankers, refineries, and petrochemical facilities across the Gulf, knocking significant refining capacity offline. Asian governments began implementing emergency measures: Indonesia introduced fuel rationing, the Philippines declared a national energy emergency, Sri Lanka ordered a four-day work week, and South Korea expanded vehicle restrictions to conserve fuel.

The bond market’s reversal was also significant. February’s substantial rally, which had sent the US 10-year yield down 28 basis points, was completely erased and reversed, as yields surged 35 basis points higher in March. At the start of the year, markets had been anticipating multiple rate cuts from the Fed, the ECB, and the Bank of England. By mid-March, those expectations had been replaced by fears of potential rate hikes, as inflation expectations moved sharply higher and central banks signalled they would wait and watch rather than ease. Major central banks largely held rates steady, with officials striking a cautious tone. Economic forecasters removed their rate cut forecasts for the year almost entirely.

In equities, the damage was broad with a few exceptions. Energy was the sole bright spot in the US, surging over 10% as oil prices spiked. All other major sectors declined. The Magnificent Seven mega-cap stocks fell 5.56%, extending their multi-month slide. Industrials, consumer staples, and healthcare all suffered steeper declines, as investors grappled with the growth implications of sustained high energy prices.

Outside the US, markets that had led the world earlier in the year fell victim to aggressive profit-taking. Korea, Taiwan, Japan, and Hong Kong all declined sharply. Greater China was the relative outperformer, with the FTSE China A50 down less than 1%, as its strategic oil reserves and direct negotiations with Iran for safe shipping passage provided a degree of insulation in the minds of market participants.

The month ended with a few somewhat positive turning points. On 30 March, Fed Chair Powell, speaking at Harvard University, signalled that the Fed is inclined to “look through” the oil price shock rather than tighten policy in response, arguing that rate hikes work with long lags and would weigh on the economy well after the energy shock has passed. The reaction was immediate, with market-implied probabilities of a rate hike collapsing from above 50% to near zero. Treasury yields fell 10 basis points across the curve, and the dollar also softened, highlighting the importance of monetary policy in financial markets, despite the geopolitical impact observed throughout the month.

Equity Market Performance

US Equities

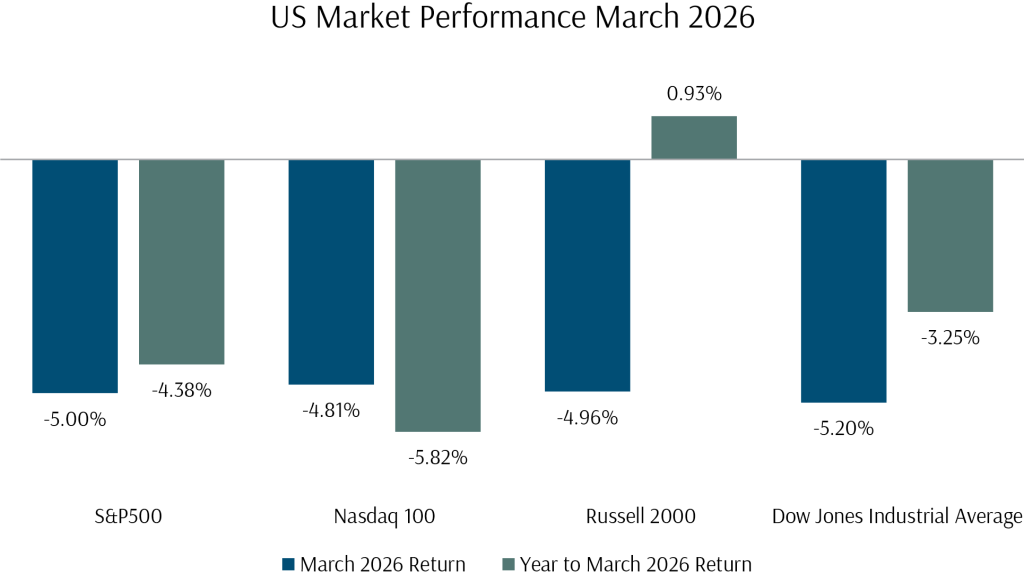

US equity markets were sharply lower in March, with the S&P 500 falling 5.00% and the Nasdaq 100 declining 4.81%. The Dow Jones Industrial Average lost 5.20%. The sell-off was broad-based, with only the energy sector posting positive returns. Technology sector weakness continued, impacted by a large rise in bond yields, although it was no longer the primary driver of market declines.

The Russell 2000 small cap stock index fell 4.96%, tracking the broader market’s decline but continuing to outperform on a year-to-date basis, with small caps up 0.93% for the year compared to the S&P 500’s 4.38% decline. Value-tilted indices continued to outperform, with large cap value beating large cap growth by 0.74 percentage points in the month alone and by a cumulative 7.03 percentage points year-to-date.

US macro-economic data painted a mixed picture. The ISM Manufacturing Index rose to 52.7 in March from 52.4 in February, marking a third consecutive month in expansion territory. The Federal Reserve held rates steady at 3.50% to 3.75% at its March meeting, in an 11-1 vote with the lone dissent in favour of a cut. The Fed raised its inflation forecast for 2026 to 2.7% on both headline and core PCE. During his post-meeting press conference, Powell acknowledged that the progress on inflation had been slower than hoped and that the implications of the Middle East conflict were uncertain.

Exhibit 1: US Stock Market Performance March 2026 (USD)

International Equities

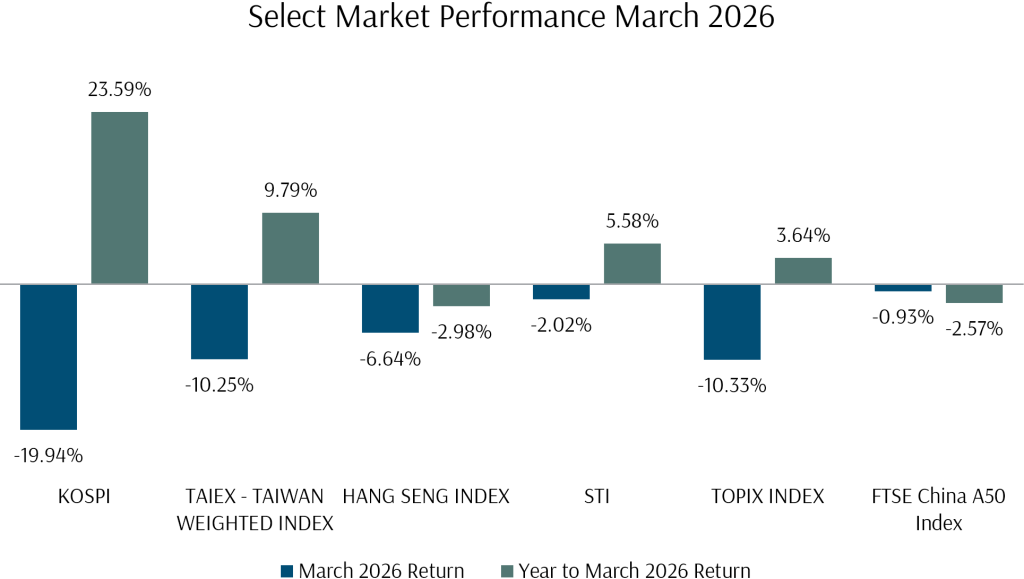

Elsewhere in the world, Asian markets saw sharp declines, reversing much of their extraordinary January and February gains as the oil shock hit energy-importing economies disproportionately hard.

Korea’s KOSPI fell 19.94%, effectively giving back its entire 20.73% February gain, as the memory semiconductor rally retraced amidst the broader risk-off environment, a sharp drop in memory prices in China, and concerns about the impact of higher energy costs on the Korean economy. Taiwan’s TAIEX declined 10.25%, while Japan’s TOPIX fell 10.33%, hit by both higher energy costs and yen weakness. Greater China fared better, with the FTSE China A50 down just 0.93% and the Hang Seng losing 6.64%, as China’s strategic oil reserves and its negotiations with Iran for safe passage through the Strait provided a degree of insulation.

Locally, the STI index was relatively resilient, declining 2.02%, with its banking and finance sector once again acting as a relative bastion of safety throughout the declines in global tech and cyclical sectors.

Exhibit 2: Select Market Performance March 2026 (Local Currency)

Global Summary

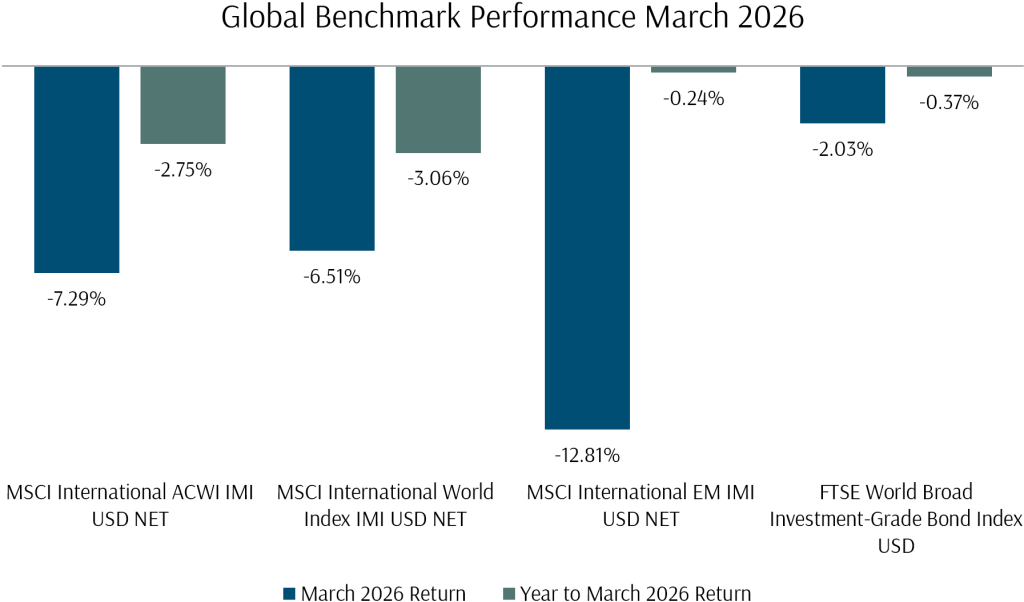

Globally, there were few hiding spots in March, with all major regions declining. The MSCI All Country World IMI fell 7.29%, its worst monthly performance in over a year. Emerging markets were hit hardest, with the MSCI EM IMI down 12.81%, while developed markets ex-US declined broadly as well. For diversified investors, the rotation into value and small cap factors that had been in progress since late 2025 provided some relative cushion, but the magnitude of the oil shock meant that March was generally a difficult month for investor in a majority of markets.

Exhibit 3: Global Equity Benchmark Index Performance March 2026 (USD)

Cross Asset Performance

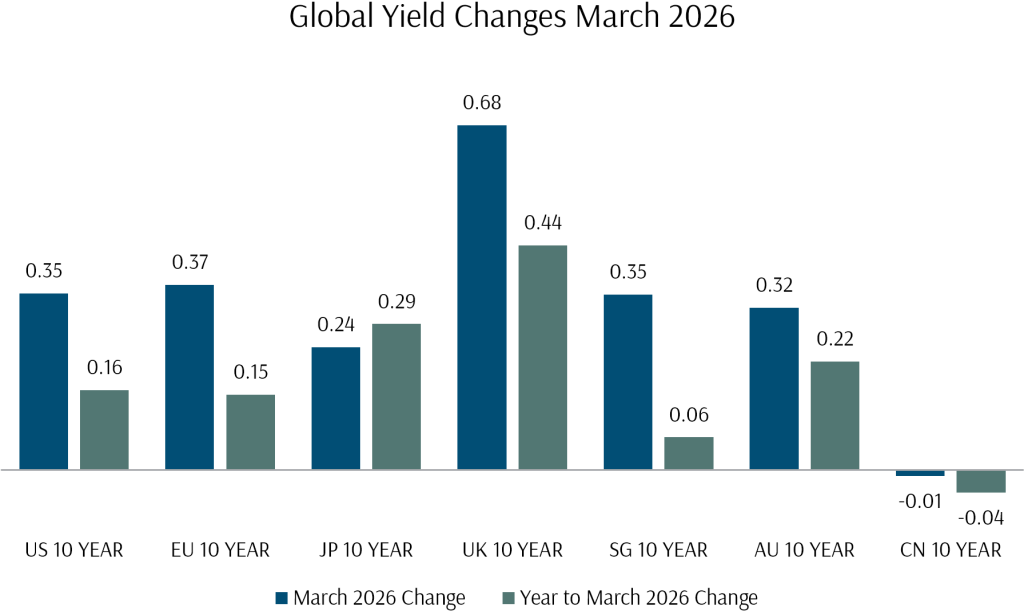

Fixed income markets suffered a sharp reversal in March, as surging oil prices and the associated repricing of inflation expectations sent bond yields markedly higher. The US 10-year Treasury yield rose 35 basis points, reversing February’s decline. UK gilt yields were hit even harder, with the 10-year rising 68 basis points as the market priced in potential rate hikes from the Bank of England. EU yields rose 37 basis points, while Singapore’s 10-year yield climbed 35 basis points.

The bond sell-off reflected a fundamental shift in the monetary policy outlook, as markets moved from pricing in rate cuts across all major central banks to pricing in holds, and in Europe and Australia, potential hikes. The ECB and Bank of England both held rates steady in March, with officials signalling a “wait and see” approach. Major research houses removed their expectations for rate cuts in 2026 entirely and noted that while they do not expect central banks to raise rates, the risk of hikes cannot be entirely dismissed if inflation expectations de-anchor.

Overall, the FTSE World Broad Investment-Grade Bond USD Index returned -2.03% for the month.

Exhibit 4: Global Yield Changes March 2026

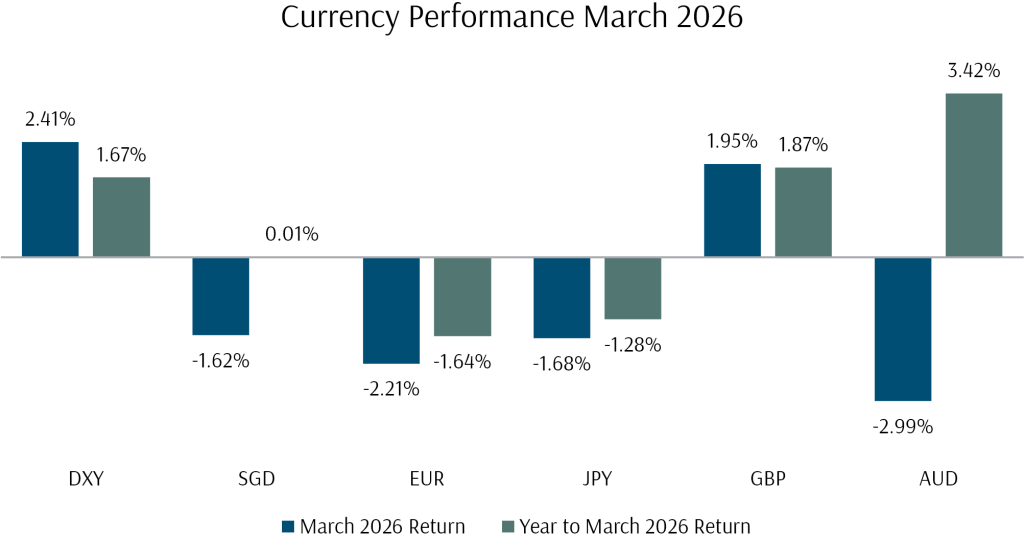

In other macro markets, the US Dollar Index gained 2.41% over the month, driven by safe-haven demand and the repricing of rate expectations. The dollar gained 1.62% against the SGD. The euro weakened 2.21% and the Australian dollar fell 2.99%, reflecting their economies’ greater sensitivity to the energy shock and the sell-off in EM. Sterling was the notable outlier, rising 1.95%, supported by the move higher in UK yields. Among emerging market currencies, energy importers came under particular pressure.

Exhibit 5: Currency Performance March 2026

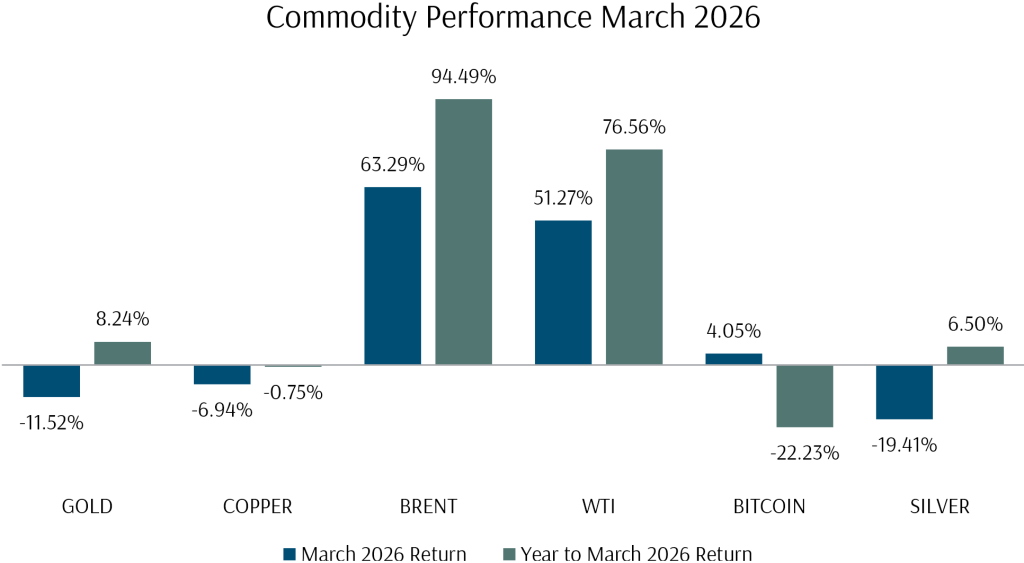

In commodity markets, crude oil was the main story. Brent surged 63.29 in the month, its largest monthly gain in recent history, as flows through the Strait of Hormuz fell to approximately 6% of normal levels. WTI gained 51.27%. Research houses estimated the net hit to global commercial oil stocks at approximately 10 to 11 million barrels per day, an extreme pace of supply tightening. Multiple governments responded with coordinated strategic petroleum reserve releases, fuel rationing, and export bans on refined products.

Gold fell 11.52% despite the geopolitical backdrop, as forced liquidation from margin calls across leveraged portfolios overwhelmed safe-haven demand, with reported selling by some central banks getting ahead of liquidity demands through an energy crisis. Silver fell 19.41%, compounding the reversal from February’s extraordinary gains. Copper declined 6.94% on growth concerns. Bitcoin edged up 4.05%.

Exhibit 6: Commodity Performance March 2026

How Did Our Portfolio Funds Fare in March?

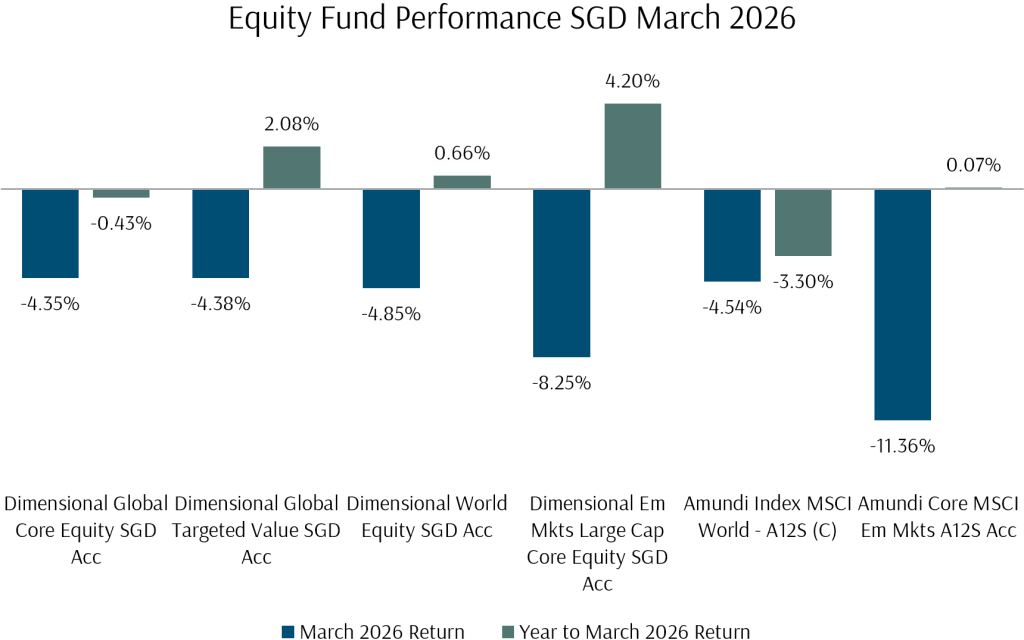

Exhibit 7: Equity Fund Performance March 2026 (SGD)

Portfolio fund performances reflected the challenging environment, with declines across equity and fixed income funds. However, relative to broad benchmarks, diversification and factor tilts continued to provide resilience.

DFA equity funds held up well relative to their benchmarks, continuing the trend over the past six months. The DFA Global Core Equity Fund returned -4.35% in SGD terms, ahead of the Amundi MSCI World Index Fund which returned -4.54%. Despite a -4.38% fall, DFA Global Targeted Value Fund remains up 2.42% year-to-date, well ahead of both the Amundi MSCI World (-2.44%) and the S&P 500 (-4.38%).

Emerging markets had the largest declines, with the Amundi MSCI EM fund losing 11.36% and the DFA EM Large Cap Core Equity Fund falling 8.25% in SGD terms, with the DFA fund outperforming meaningfully.

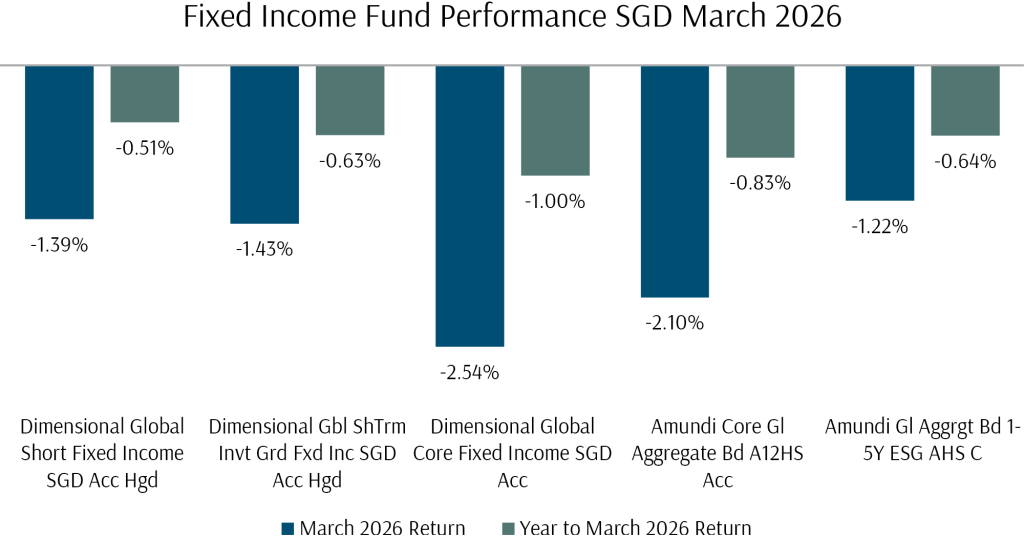

DFA fixed income funds were impacted by the sharp rise in bond yields, with the DFA Global Core Fixed Income Fund returning -2.54% in SGD terms, while the shorter-duration DFA Global Short Fixed Income Fund returned -1.39% and the DFA Global Short Term Investment Grade Fixed Income Fund returned -1.43%. The shorter-duration positioning in our fixed income allocation added value in March, as shorter-term bonds were significantly less impacted by the surge in yields. As a result of the rise in the US dollar in March, SGD-hedged currency fund classes underperformed USD peers.

Exhibit 8: Fixed Income Fund Performance March 2026 (SGD)

March Investment Questions: The Ongoing Oil Shock and Implications On Markets

Q1: How severe is the disruption to oil markets?

The supply situation has deteriorated significantly since February. In our last review, we noted that Strait of Hormuz flows had fallen sharply and that the key question for markets was how long the disruption would persist. Since then, flows have remained at approximately 6% of normal levels, with an estimated net hit to global commercial oil stocks of around 10 to 11 million barrels per day. Global visible oil inventories have declined by approximately 162 million barrels since the conflict began, depleting over a third of 2025’s visible inventory builds. Pipeline workarounds through Saudi Arabia and the UAE have been operating near capacity and have been able to redirect approximately a quarter of normal flows.

The physical oil market has correspondingly tightened drastically The price of physical Brent crude oil, surged to $141 per barrel in early April, its highest since 2008. The crude oil futures curve saw extreme backwardation, which was a somewhat positive signal, as markets continued to price in a high probability that the disruption will be short-lived, even as spot shortages grow in the meantime.

Q2: What are the scenarios for oil prices from here?

Research houses have outlined several scenarios. In a base case where flows through the Strait remain very low for approximately six weeks before beginning to normalise, Brent is expected to average above $100 in March, peak around $115 in April, and then fall back towards $80 by year-end as shipping resumes and demand adjusts. In an adverse scenario where disruptions persist for 10 weeks, prices could reach $140 per barrel. In a severely adverse scenario involving 10 weeks of disruption plus lasting damage to production infrastructure, prices could peak near $160.

On the other hand, if a broader deal is reached that restores transit through the Strait, oil prices would likely retrace sharply.

Q3: How has the crisis changed the monetary policy outlook?

The spike in bond yields was a highly significant development for financial markets in March. Before the Iran strikes, the market was pricing in multiple rate cuts from the Fed, ECB, and Bank of England in 2026. In the space of a few weeks, markets shifted from pricing in cuts to pricing in potential hikes, particularly from the ECB and Bank of England, as inflation expectations surged alongside energy prices.

However, bond markets saw some relief on 30 March, when Fed Chair Powell spoke at Harvard University. He signalled that the Fed’s inclination is to “look through” the energy shock, arguing that monetary policy works with long lags and that tightening now would weigh on the economy after the oil shock has passed. He emphasised that the approach depends on inflation expectations remaining well-anchored. After his remarks, market-implied probabilities of a rate hike collapsed from above 50% to near zero.

Q4: What does the oil shock mean for Asia and emerging markets?

The impact is differentiated and depends heavily on each economy’s energy import profile. Asian and EM oil importers face the most direct exposure to higher energy costs, which tighten financial conditions and strain external balances. Several countries have already implemented emergency measures.

However, there are important mitigating factors. India has received waivers allowing it to continue purchasing Russian oil, and both India and China have successfully negotiated some degree of safe passage for their ships through the Strait. China has strategic reserves, is rapidly electrifying its transport sector, and the relatively low 0.93% decline in the China A50 index in March is evidence of the market’s assessment of its energy resilience.

Major research houses believe EM growth will remain robust and see no secular reason for this to change. Fiscal and macroeconomic metrics in emerging markets are improving, with macroeconomic normalcy returning to many EM economies. The structural trends driving Asian outperformance, particularly the AI semiconductor buildout, improved financial conditions, and the broader diversification of global capital flows away from US-centric allocations, remain intact. A prolonged oil shock would certainly test these tailwinds, but the medium-term investment case for Asia and EM diversification is generally unchanged for now.

Q5: What does a de-escalation look like for markets?

De-escalation would require a resolution to the conflict, whether through diplomatic agreement, US naval protection for commercial tankers, or Iran permitting broader safe passage.

If tensions ease, oil prices should normalise quickly, and the assets currently under the most pressure would be among the fastest to recover. Research analysts note that cyclical sectors, AI-related infrastructure names, and growth-oriented equities have all been de-rated well beyond what their underlying earnings trajectories would justify. Broad AI data centre infrastructure, for instance, has significantly lagged its earnings revisions, creating potential for sharp re-ratings on any positive shift in sentiment.

Accordingly, should a de-escalation occur, global markets have a number of strong upside catalysts in the pipeline, and will be moving from a more reasonable valuation base after the clearing event of the last month.

Q6: Why is the S&P 500 only down about 6% from its all-time highs despite the scale of the Iran conflict and the surge in oil prices?

WTI Oil spot has risen 66% to $112 since the Iran war began in late February, but the 12-month futures contract is up only 11% to about $70, roughly where it traded in early 2025. Over the past week, a 12% spike in WTI spot was accompanied by the 12-month contract falling 6% and Brent futures dropping 3%. Hence, the market continues to treat the disruption as temporary event rather than a structural change. Corporate earnings are also more sensitive to the expected path of oil prices over the next year than to spot levels today.

Looking Forward to April 2026

Markets have been excessively reactive to headlines over the past weeks, with outsized moves in both directions on every development from the White House, the battlefield, and diplomatic channels. The S&P 500 surged 3.7% over two sessions in late March on hopes of de-escalation, only to give back most of those gains within 48 hours after the President’s primetime address struck a more hawkish tone. Korea’s KOSPI has seen several single-day swings of 5% or more. Oil has moved $10 or more intraday. This headline-driven volatility is likely to persist until the conflict is resolved.

The White House has been a major source of uncertainty. Over the course of ten days, the President announced a five-day pause on strikes against Iranian energy infrastructure, suggested the US might walk away without reopening the Strait, claimed “great progress” on a comprehensive deal, and then threatened to destroy Iran’s energy grid within two to three weeks if no agreement is reached. Each pronouncement moved markets sharply, and in several cases the reversal came within hours. For investors, positioning based on any single headline in this environment is extremely unreliable.

There are, however, constructive developments beneath the noise. Pakistan has emerged as a key intermediary, relaying messages between Washington and Tehran and hosting a quadrilateral meeting of foreign ministers from Saudi Arabia, Turkey, and Egypt in Islamabad. A joint Chinese-Pakistani peace proposal has been shared with both sides and received broad regional support. Iran has so far stopped short of agreeing to formal talks but has allowed Pakistani ships to transit the Strait, a small but symbolic step. Separately, Iran and Oman have been developing a protocol to regulate commercial navigation through Hormuz, reports of which prompted a sharp intraday rally on 2 April.

On the monetary policy front, the picture has stabilised. Powell’s Harvard remarks on 30 March removed the threat of a near-term rate hike, and bond markets have found some footing since then. Treasury yields have pulled back from their March peaks, and equity volatility, while still elevated, has retreated from its worst levels.

While physical oil markets remain in acute stress, geopolitical outcomes are uncertain, and further volatility in either direction is likely in the near term. However, recent developments in the form of extreme backwardation in oil futures, the growing diplomatic momentum, and Powell’s clear signal on monetary policy, suggests the market will soon begin to position for a conflict resolution in one form or another.

With a comprehensive plan already in place with your Client Adviser, covering near-term spending needs while allocating capital at a level of risk suitable for your longer-term goals, you can have the peace of mind to navigate market volatility and stay invested for the long term, allowing your wealth to compound and fulfil your ikigai. If you have any questions, please do not hesitate to reach out to your Client Adviser.

The writer of this market review, Glenn Tan, is Portfolio Manager at Providend Ltd, Southeast Asia’s first fee-only comprehensive wealth advisory firm. He is also a CFA Charterholder and a Certified Financial Risk Manager (FRM).

For more related resources, check out:

1. Active Investing That Adds Value to the Client

2. Staying the Course: Investing With Confidence in Uncertain Times

3. Here’s Why We Charge a Higher Fee Than Robos

Download our Investment eBook titled “A More Reliable Way to Get Enough Investment Returns: Even During Times of Market Uncertainty” here.

With a minefield of financial misinformation out there, we promise to be a safe pair of hands and a second pair of eyes to help you avoid costly financial mistakes. Learn more about our investment philosophy here.

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current estate plan, investment portfolio, financial and/or retirement plan, make an appointment with us today.