In early September, Deputy Prime Minister Tharman Shanmugaratnam revealed that over the past ten years, more than 80% of CPF investors would have been better off leaving their money in the CPF Ordinary Account which earns a guaranteed 2.5% per annum and that 45% of CPF investors actually lost money.

He highlighted that there were two reasons for this – high fees and behavioural biases.

In my previous article, we looked at what kind of investment vehicles are likely to give us better returns, which is what a lot of investors tend to focus on. However, there is another key to investment performance, which was highlighted by DPM Tharman – investor behaviour. It is a little similar to driving – choosing a great vehicle is well and good, but if you do not drive it well, you may still end up taking a very long time to get to your intended destination, which for most of us is a comfortable retirement.

In this article, we will explore some of the behaviours that investors exhibit that inhibit them from reaching their retirement goals, and what they should do instead to improve their investment returns.

Investor Returns vs Fund Returns

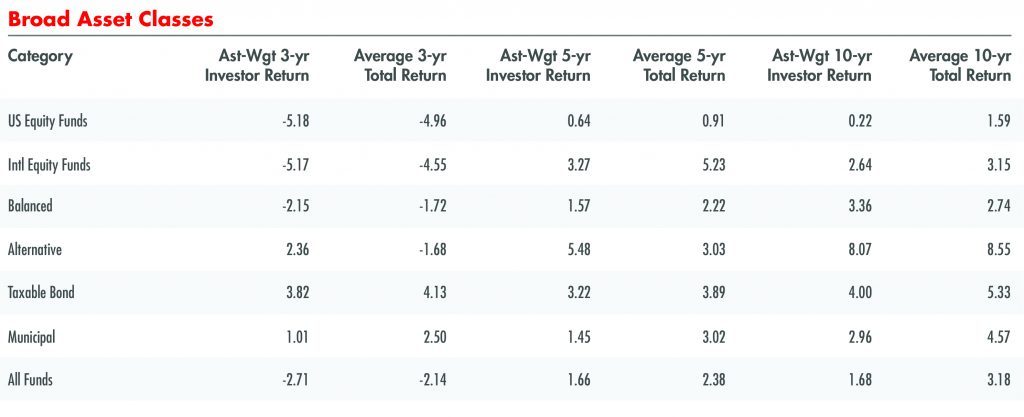

In 2010, Morningstar released a study showing the difference between the returns the average fund investor made and the returns of the average fund made in the previous decade. The difference between the two returns can be attributed to the timing of the average fund investor’s investments; if investor returns were lower than the funds, it means that they timed their investments poorly and vice versa.[1] The table below shows that if investors simply used a buy and hold strategy for U.S. Equity funds for ten years up till 31st December 2009, they would have earned the fund’s returns of 1.59% per annum. However, the average fund investor only earned 0.22% per annum. For International Equity Funds, a buy-and-hold strategy would have yielded a return of 3.15% per annum over ten years, but the average fund investor earned only 2.64% per annum.

Source: Morningstar, Inc. 2010.

Source: Morningstar, Inc. 2010.

Interestingly, Balanced Fund investors made slightly more than the funds over ten years, with 3.36% per annum returns compared to the funds’ 2.74% per annum. Balanced funds have a mix of both equities and bonds, leading to moderate volatility and returns, which may have encouraged investors to simply leave their investments in the funds as they were rather than to actively engage in buying and selling which they appear to have done with all-equity or all-bond funds. In fact, they seem to have added to their positions at the right times, leading to better results than the funds themselves.

Overall, across all funds over the previous decade, due to market timing, the average investor made 1.68% per annum while a buy-and-hold strategy would have made 3.18%. How significant is this difference? If an investor made 1.68% per annum on his $100,000 investment over ten years, he would have made $118,128.69 by the end of it. If he had made 3.18% per annum, he would have made $136,758.79 instead – more than double the capital gains. Clearly, the average fund investor would have been much better off with a buy-and-hold strategy, rather than jumping in and out of the market.

Why Do So Many Investors Choose To Engage In Market Timing?

One reason is that investors may be overconfident about their ability to pick market highs and lows. Many investors are undoubtedly intelligent, in some cases highly intelligent, but is it actually possible to tell when markets are going to crash, and when markets are at their bottom?

I have met many investors over the years who have told me the various indicators they use to predict that markets are about to crash. The technically-inclined ones will mention yield curves, volatility indices, or moving averages. The not-so-technically-inclined ones will simply say “I feel it in my gut.” And then there are those who don’t know and know that they don’t know but their friend happens to know, because he is very experienced, and he told them that the market is going to crash so they pulled their funds out.

Nobel Laureate Daniel Kahneman points out that the problem with overconfidence is that when people believe that they know something that they do not actually know, they end up trading too much, which leads to higher costs, and therefore lower returns. Of course, if their trading ideas were correct, they would be more profitable, but the evidence shows otherwise. Behavioural theorist Terrance Odean studied ten thousand accounts from a large brokerage house over several years and found that on average, the stocks that investors sold actually did much better afterwards than the stocks they bought.[2] In addition to paying brokerage fees for buying and selling stocks, the stocks they sold outperformed stocks they bought by an average of 3.3% over a one-year horizon, which is huge.

Terrance Odean and Brad Barber also discovered in another study[3] that due to overconfidence, men on average traded 45% more frequently than women and this led to them having poorer investment returns.

Another reason investors tend to jump in and out of the market is due to a combination of greed and fear. When newspaper headlines highlight how markets are doing really well when financial experts appear on television claiming the bull market will continue, and when one’s friends and family mention how much money they have been making from the stock market, that’s usually a sign of a market that may be getting a little too exuberant.

However, many investors make the mistake of jumping into the markets at precisely this time due to the greed for what appears to be easy money. During market crashes and when the headlines turn pessimistic, many unfortunately jump out because of the fear of losing even more. With the benefit of hindsight, it is clear that an investor should have done the opposite, but that is far easier said than done when one is entrapped in the emotions of fear and greed.

Even if investors know that buy-and-hold strategies have been proven to outperform market timing, there is still a likelihood that they will try to time the markets anyway. Nobel Laureate Paul Samuelson calls this the “gambling instinct” in people. “I tell people investing should be dull,” he said. “It shouldn’t be exciting. Investing should be more like watching paint dry or watching grass grow. If you want excitement, take $800 and go to Las Vegas.” Unfortunately, many investors tend to treat the stock market as a casino and more often than not, end up losing money or not making as much as they would have if they had just let the market do the work for them.

So How Should Investors Invest?

The evidence shows that staying invested for the long term gives you the best odds of success. There are two ways that one could do this: one is to put a lump sum into the market and hold it for the long term while occasionally rebalancing the asset allocation; the second way is through dollar-cost averaging, which involves investing fixed sums at regular intervals for the long term rather than putting one large lump sum at the beginning. Dollar-cost averaging can help one to obtain the average returns of the market in a systematic and less emotionally stressful manner.

To be sure, these are unexciting strategies. Using the driving analogy again, investing for your retirement and for your children’s education is similar to driving with your family – driving in a smooth, steady and boring manner allows your wife and children to be comfortable and secure while giving you the highest odds of getting to your destination. The alternative is to try to drive as fast as you can to try to get to your destination more quickly, which can be very exciting but also riskier, and if you make mistakes along the way you could end up taking a much longer time to get to your destination. The legendary investor Peter Lynch once said, “Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections than has been lost in corrections themselves.” So, resist the temptation to jump in and out of the markets and simply enjoy the ride.

This is an original article written by Sean Cheng, Solutions & Investments Executive at Providend, Singapore’s Fee-only Wealth Advisory Firm.

[1] The methodology used for the study can be found here: https://corporate.morningstar.com/US/documents/MethodologyDocuments/MethodologyPapers/InvestorReturnsMethodology.pdf [2] Odean, Terrance, “Do Investors Trade Too Much?” The American Economic Review (December 1999). [3] Barber, Brad and Terrance Odean, “Boys will be Boys: Gender, Overconfidence, and Common Stock Investment,” The Quarterly Journal of Economics (February 2001).We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current investment portfolio, financial and/or retirement plan, make an appointment with us today.