A common question posed to me at conferences and panel discussions is: “Can we retire in Singapore?” It seems that many Singaporeans are worried that they can’t.

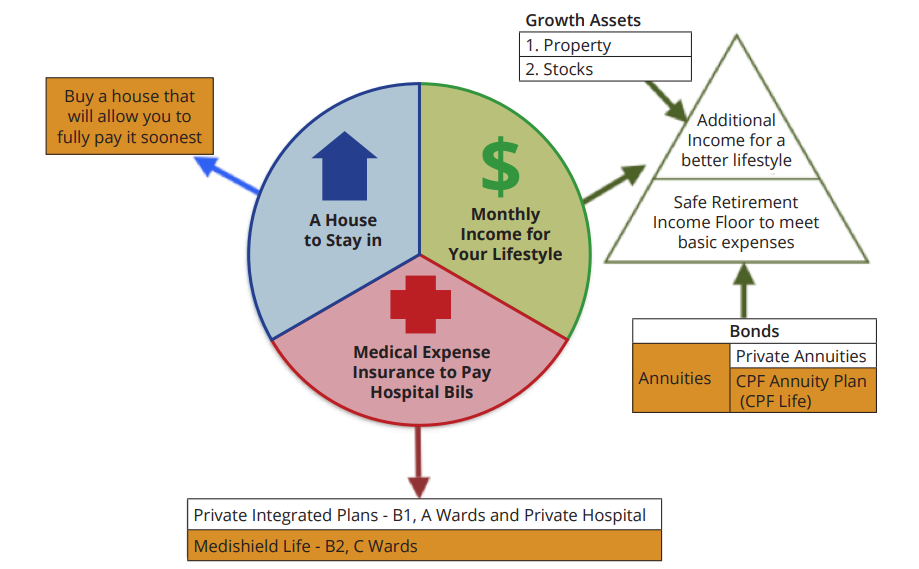

So what does it take to retire in Singapore, or for that matter, anywhere in the world? We need to have 3 things (see diagram above):

- A fully paid house

- Medical expense insurance to pay hospital bills

- Monthly income for all your needs

According to the department of statistics, more than 90% of the Singaporean households own their own homes and over 80% of our lower-income households (those in the bottom 20% of income) also own their own homes. And by the end of this year, every Singaporean will have basic medical expense insurance called Medishield Life. So that leaves one final part of the equation: will we have sufficient monthly income when we retire?

That depends on what is sufficient for us.

According to the department of statistics, the average monthly household expenditure per household member for the 21st to 40th expenditure quintile will be about $657 in 10 years’ time. And for the 61st to 80th expenditure quintile, it will be $1,338. We can assume that the former are individuals with lower income and latter with higher income in their working years. This is a good guide for what you will at least need for a basic retirement.

The Retirement Plan

In our opinion, our retirement income portfolio must be divided into 2 portions. The first portion must give us a reliable income stream to give us a basic retirement. The second portion is meant to give us additional income for a better lifestyle, which we can get by investing in higher return instruments spread over a few buckets for drawdown at different periods.

One of the best instruments to give us a reliable income stream for a basic retirement is the annuity. It pays an amount regardless of market volatility and for life, to hedge against longevity risk. In this regard, the best annuity in Singapore is CPF LIFE. It has a very low issuer risk (it is from the Singapore government!), zero distribution cost (you don’t pay commissions to buy it) and yield the best returns (it is still guaranteed at 4% p.a. currently). When the recommendations by the CPF Advisory Panel are made operational, you will be able to buy different annuity payouts based on your needs and ability.

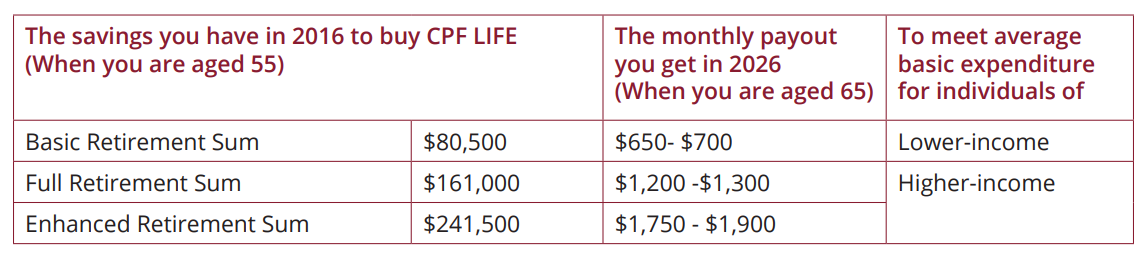

So how can you save towards these sums at aged 55? The best way is through your CPF contributions, of course! It is truly tax-free to save and tax-free when you take out. In addition, every dollar you put in earns a minimum of 2.5%-5% p.a. guaranteed. And with Budget 2015 just announced, it is now easier to reach these sums:

- From 2016, the CPF salary ceiling will be raised from $5,000 to $6,000. According to DPM and Finance Minister Tharman Shamugaratnam, this means an additional $60,000 saved at aged 65, if you are an aged 45 worker earning $6,000 or more today.

- Workers aged 50-55 will have their CPF contribution go up by 2%. Those aged 56-60 will have their contribution go up by 1% and workers aged 61-65 will have their contribution go up by 0.5%.

- Paying an extra 1% p.a. interest on the first $30,000 of CPF balances from the age of 55.

Even before the budget announcement, it is expected that among the cohort of CPF members turning 55 in 2020, 7 in 10 active members will accumulate enough CPF savings to meet the Basic Retirement Sum then. With these new budget initiatives, it simply means that more will be able to reach our retirement sums.

But the above may not help those low-income elderlies who currently still fall short of having enough CPF savings to meet the Basic Retirement Sum at 55. Their wages were generally lower in the past so the amounts set aside via the CPF were correspondingly less. These older members also had a shorter runway to benefit from the 1% extra interest on the first $60,000 of balances, introduced in 2008, and the Workfare Income Supplement Scheme introduced in 2007 which tops up the CPF accounts of lower-income members. Their low balances may only give them a payout of say $200 per month.

This is where the recently announced Silver Support Scheme comes in. It is meant to help this group of people when they turn 65 and also people in similar situations in the future. With an average payment of $200 per person added to their own CPF payouts and perhaps, some giving by their children, they may still be able to retire today.

And if all these still don’t help, we have one more card: Since most Singaporeans own our homes, we can still monetize our homes to supplement our retirement income.

Over the years, our CPF has helped us own our own homes, fund the premiums of medical expense insurance through our Medisave and accumulate a sum to buy the annuity (CPF LIFE) that we need. I think the latest budget announcements further complete the picture, helping the lower-income households and even those that may have low balances. I am therefore convinced that we can at least have a basic retirement. For those who are able, we should buy better medical expense insurance to afford us better medical care. We can invest beyond CPF to give us additional income for the above basic lifestyle.

But one final thought: A good retirement is not just about having enough money. It is also about living a purposeful life. So while you plan for the money part, do consider how you purpose to live the last phase of your life.

The writer, Christopher Tan, is Chief Executive Officer of Providend, a Fee-only Wealth Advisory Firm. Besides being financially trained, he is also an Associate Certified Coach with the International Coach Federation. The edited version has been published in The Business Times on 28 February 2015.

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current investment portfolio, financial and/or retirement plan, make an appointment with us today.