“Can I still buy insurance? Which insurance companies are willing to cover me?”

These are the questions I recall having asked by a prospective client who suffered from a heart condition while I was still a financial adviser with my previous financial advisory firm more than 5 years ago. In the span of my financial advisory career, I have met different clients who have been diagnosed and suffered from different types of medical conditions. However, not all conditions are considered uninsurable. Some insurers are still willing to undertake certain health risks without conditions, whereas, others might simply reject the application, postpone, impose exclusions, or even premium loading.

In this article, I will explain more details about how an individual can be insured through different approaches even with some pre-existing health conditions.

Types of medical conditions

Basically, I classify medical conditions into 2 types:

- Major medical conditions – Will cause major disruption and some alterations to your daily life activities.

- Minor medical conditions – May cause some minor to no disruption to your daily life activities.

For major conditions, I further classify them into 2 categories – Less severe and severe conditions. Severe conditions are the advanced stage critical illnesses such as stage 3 cancer, and less severe conditions are early to intermediate stage critical illnesses such as stage 1 or 2 cancer.

For minor conditions, I also classify them into 2 categories – Common illnesses and chronic conditions. Common illnesses are usually light conditions that are discovered during our routine health checks or visits to the doctor when we feel unwell – Allergies, sinus, eczema, dry eyes, cold, cough, flu, etc., whereas chronic conditions are diabetes, hypertension, osteoporosis, raised cholesterol, asthma, etc.

Top medical conditions in Singapore

Based on the Ministry of Health (MOH) statistics, the top Minor medical conditions gathered in the recent years are as follow:

- Raised Cholesterol

- Hypertension

- Diabetes

From the data above, we can see an increase in hyperlipidaemia which is also known as “raised cholesterol” and hypertension conditions from the year 2010 to the year 2017. There was also a slight increase in diabetes during the same period. Based on the result shown, it seems that more Singapore residents are suffering from these conditions.

On the flipside, obesity and daily smoking ratios have dropped from the year 2010 to 2017.

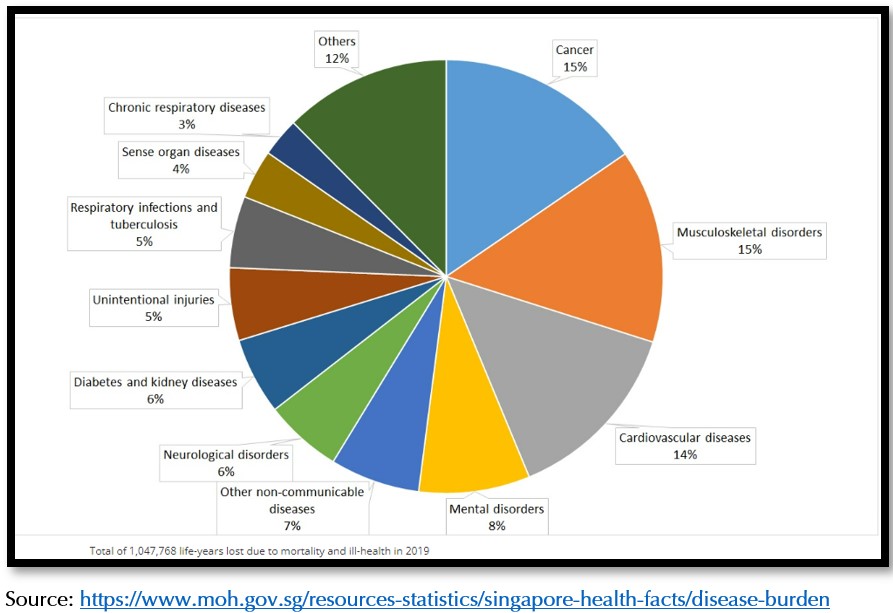

If we further break down the type of Major medical conditions that cause life-years lost due to mortality and ill-health, we can draw a few observations from the chart below.

Based on the statistics provided by MOH in the year 2019, the top 3 leading conditions which made up 44% of ill-health and death to Singapore residents are cancer diseases, musculoskeletal disorders as well as cardiovascular diseases.

[1,2,3] Many minor and major medical conditions are caused by unhealthy diet or habits as well as lack of exercise. By making changes to our lifestyle, we could reduce the risk of developing these medical conditions.Under-declaration of medical condition

As we know, having a minor medical condition is getting more common these days. However, it is not an area that we should ignore especially when it comes to health declaration during our insurance application. It is not advisable to hide or provide a selective declaration of any information with regard to our health conditions to the insurer. It is very important to disclose all the material information for the insurer to assess.

When we purchase an insurance plan, it is meant to give us a peace of mind rather than to worry about any potential issue with claims due to an inaccurate declaration of our health conditions at the point of application.

Taking a shortcut by not providing such information to the insurer for assessment can be very detrimental in the future should a claim arises. Some individuals may find it inconvenient as they might need to undergo a medical examination or retrieve medical documents if they were to declare every detail. Insurance plans are ultimately a contract between the insurer and the individual. Hence, any non-disclosure, fraud, or misrepresentation could allow the insurance company to reject any claim, and even void the policy in the future. With that, we shall not let all the effort, time, and money be wasted because of under-declaration of our medical conditions.

Types of Insurance coverage

With rising standard of living and more indulgent lifestyles, it is becoming more common for people to have some or minor health issues. The question is – Are insurance companies ready to undertake the risk of insuring this group of individuals?

The answer is yes. There are insurers that are more forward-looking in regard to insuring people with pre-existing conditions.

1) Medical Insurance for chronic conditions

Raffles Health Insurance is the only unique Integrated Shield Plan provider that offers individuals who suffer from chronic conditions such as Diabetes, Hypertension, and Hyperlipidemia to have the option to purchase their Raffles Shield plan with either Premium loading or Exclusion. Individuals who take up the plan must undergo the “Raffles Care Management Programme (RCMP)” to have regular monitoring of their chronic conditions. If the individual health becomes better through RCMP, they will get to enjoy the reduction of their original premium loading.

2) Life Insurance for diabetes

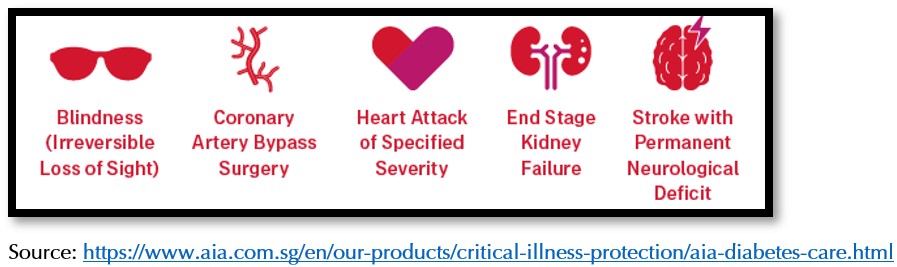

AIA Singapore offers a “AIA Diabetes Care” plan specifically for individuals who suffer from Type 2 Diabetes and Pre-diabetes. There is an additional lump sum payout as well as add-on protection with cancer coverage. The plan has even extended to cover any 5 of the diabetes-related critical illnesses as follows:

3) Life Insurance for 3 chronic conditions – High blood pressure, raised cholesterol, Type 2 Diabetes or Pre-diabetes

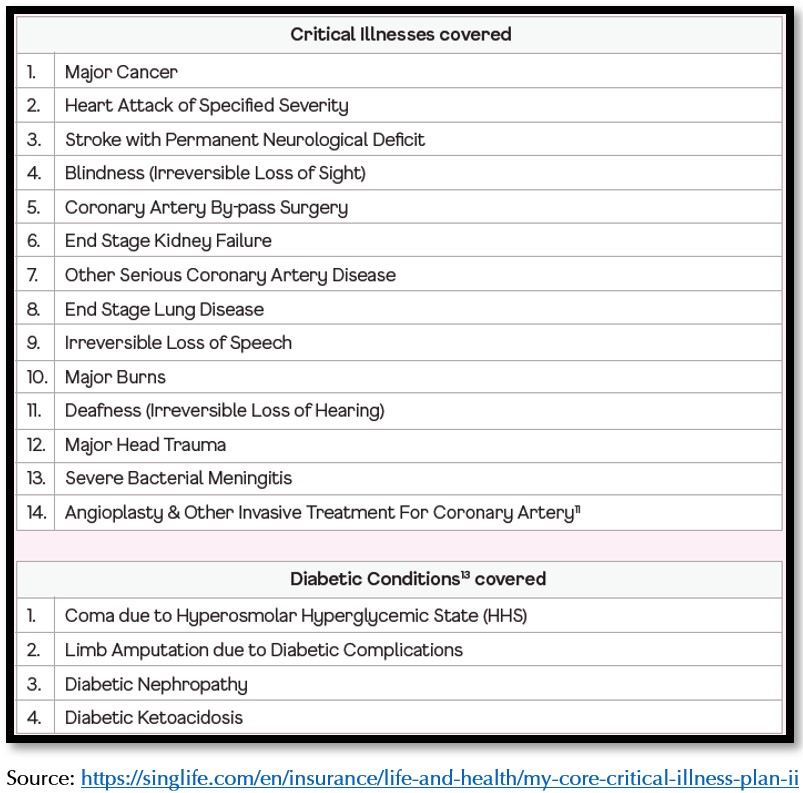

Prudential and Singlife with Aviva offer a special critical illness plan for individuals who have pre-existing conditions such as Type 2 Diabetes, Pre-diabetes and/or 3 Highs (High blood pressure, high cholesterol, and high Body Mass Index). Below is an example of a Singlife with Aviva plan which covers 14 different types of critical illnesses, and 4 diabetes conditions.

4) Life Insurance covering Cancer only condition

There are several insurance companies offering products to cover only Cancer related illness such as Tokio Marine, Etiqa, NTUC Income, and some other general insurance companies.

Here are some attributes when applying for this type of plan:

- Require minimum health declaration, usually 5 to 10 health questionnaires.

- Must not have suffered any cancer condition before.

- Most of these insurance companies’ cancer only plan is able to cover multi-stage cancer condition.

5) Life Insurance covering individual who has recovered from a Cancer illness

AXA is the first insurer to offer such a plan in Singapore that provides coverage for the recovered cancer patients.

Some key points when applying for such a plan:

- The individual must only suffer cancer condition once.

- The individual must be in remission for at least 3 years.

- Cancer diagnosed previously must be between stages 1 to 3 except for brain cancer.

This could be a huge deal-breaker for the ex-cancer patient who is seeking to be insured again.

As insurance companies become more experienced in dealing with some of the medical conditions and managing the risk, it is expected that they are willing to design products that cater to a certain group of individuals who has a certain type of pre-existing conditions. [4] In the US, the Prudential Life Insurance company from America has begun to offer insurance for patients who suffered from HIV.

Unable to be insured due to serious conditions

From the insurance company’s point of view, it is about how they manage the risk of insuring an individual with a serious condition. Insurers need to protect the policyholder’s premium that is collected under the Insurance fund. If today, insurance companies start insuring individuals with serious conditions, they are exposing themselves to a higher chance of claim rate in the future which will create financial stress for themselves as the Insurance fund will get smaller and smaller. Also, allowing individuals with serious conditions to be accepted will create unfairness to the policyholders who bought insurance years ago when they were in good health. In such a case, this will discourage policyholders to purchase the insurance when their health is good and only purchasing it when they started to have some sort of condition. Having said that, the insurance companies collect less premium in the earlier years from the policyholder to generate their liabilities (for future expected claims).

Hence, it is critical for the insurance companies to assess and evaluate every health condition on a case-by-case basis and to consider carefully if they are able to undertake the risk.

Those who are uninsurable may consider setting up their own medical sinking fund for the future to self-insure against potential medical bills. Such medical sinking fund amount depends on the healthcare expectation that the individual wishes to have. Another area of consideration is to have the medical sinking fund to fight against healthcare inflation. You may discuss this area of concern with your adviser to get more insights on how you may execute this using some of the financial strategies.

Preliminary Underwriting instead of Full Insurance Application

For those with pre-existing conditions, some insurers provide what is called preliminary underwriting, which is a quick process for insurers to assess if they are willing and able to accept you as a client without going into the elaborate application process. This is an extra step undertaken by the adviser, but it cuts down the time for you to have a quick idea on whether your pre-existing conditions are insurable and what are the counteroffers. You can then make a better assessment if you would like to proceed or reapply with another insurer.

In the preliminary underwriting process, it requires you to inform the insurer what are the exact medical conditions that you have and the amount of coverage and plan you are looking to insure. This process is usually faster in knowing what the insurer is willing to offer.

Choose the best underwriting result you prefer and with the preliminary underwriting result, you can make an official application with the insurance company.

Lastly, it is important to work with an adviser who is willing to go the extra mile to help and guide you in your journey of getting yourself sufficiently insured.

This is an original article written by our Insurance Team at Providend, Singapore’s First Fee-Only Wealth Advisory Firm.

For more related resources, check out:

1. Our Wealth Solution – Risk Mitigation

2. The Basic Principle of Insurance Planning

3. A Comprehensive Guide to Buying Insurance for Your Child

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current estate plan, investment portfolio, financial and/or retirement plan, make an appointment with us today.