After almost a year of waiting, the CPF Special Account (SA) was finally closed on 19 January 2025 for approximately 1.4 million CPF members.

Over the past month, as Singaporeans above 55 years old prepare for this eventuality, I received many questions on what one should do with their CPF money, which will be transferred to their Ordinary Account (OA) from their SA when it closes. At the same time, I have noticed financial institutions and their representatives encouraging CPF members to invest their OA money to get “better returns.” In this article, I hope to provide some clarity on what you should do with your hard-earned CPF money.

When CPF members turn 55 years old, the amount up to their Full Retirement Sum (FRS) is transferred to their Retirement Account (RA) from their SA first, and if insufficient, the remaining amount will be funded from their money in OA. Previously, if there is still excess money in their SA and OA after that, members could withdraw it anytime they wanted or leave it in the accounts to enjoy at least 4% p.a. or 2.5% p.a. respectively. Money in the RA will attract interest rates of between 4% p.a. and 6% p.a. , and when members turn 65 years old, they can start their CPF LIFE payouts to enjoy a lifelong income stream till their unfortunate demise.

When planning for retirement spending, one should broadly categorise their expenses into expenses that are absolutely necessary (essential) and the remaining, being good to have (discretionary). They can then deploy their accumulated capital for retirement to appropriate financial instruments to fund these expenses. Where financially possible, one should also have a sum of money set aside as reserves to cope with unexpected situations beyond the normal spending.

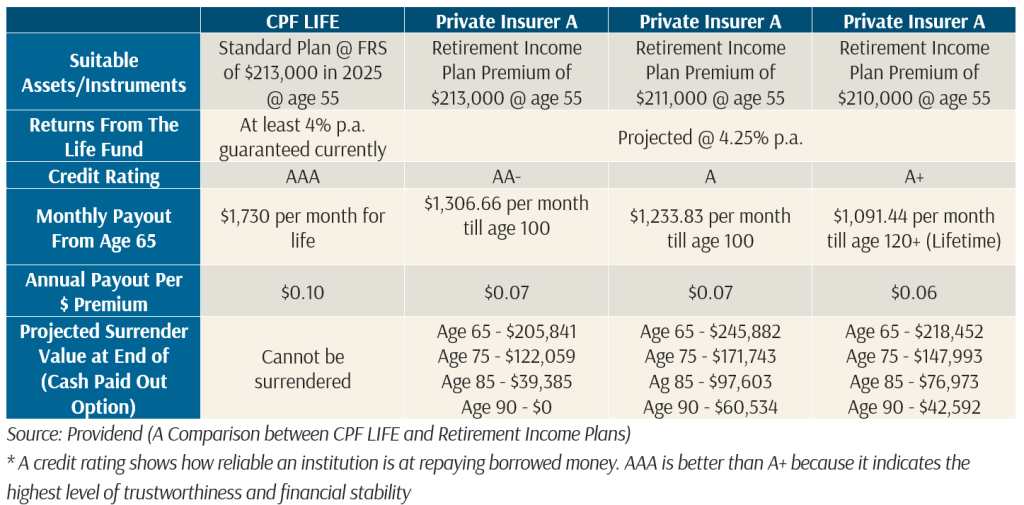

To fund essential expenses in retirement, we will often recommend annuities as one of the instruments because it mitigates longevity risk and also pays a reliable income regardless of financial markets volatility. Since it is without a doubt that CPF LIFE is the best annuity in terms of annual payout per dollar of premium (see table below), CPF members typically use CPF LIFE as the annuity to fund part or all of their essential expenses.

Alternatively, you can buy private insurance offering equivalent benefits to CPF LIFE and apply to be exempted from setting aside the retirement sum and withdraw all your CPF retirement savings. However, as demonstrated through the comparison, it is quite difficult to find policies that are better than CPF LIFE these days. For members with excess money left in their SA and OA, they would typically use it to fund their expenses from age 55 to 65 until they receive payouts from CPF LIFE, or they leave it in their accounts as reserves since they offer attractive interest rates at almost no risk.

However, with the closure of the SA for members above age 55, excess money left in the SA will be transferred to the OA. So instead of 4% p.a., members can only earn 2.5% p.a.

What one should do now will really depend on the original intention for their CPF money if SA was still open.

Original Intention 1: To Keep It in SA and Only Transfer to RA When One Wants to Start CPF LIFE Payouts.

I know of some CPF members who would keep the excess cash in SA to earn the 4% p.a. interest and only make a decision on whether they want to transfer an amount up to the prevailing Enhanced Retirement Sum (ERS) when they want to draw down on their CPF LIFE to get a higher payout. If this is the case, you may now want to top up your RA up to ERS (currently $426,000). However, you may want to consider topping up your RA first with cash in your savings accounts (if you have any) before using money in your OA to do so because your OA should be earning a higher interest than your savings accounts.

Original Intention 2: To Use It for Immediate Drawdown From Age 55 Till CPF LIFE Payouts Start.

If this was your original intention, I would suggest that you keep it in your OA and not invest it. At a guaranteed 2.5% p.a. with near-zero risk and full liquidity, it is as good as it gets. Yes, perhaps you can still invest in SGS T-bills at a slightly higher interest rate than 2.5% p.a., but you probably won’t be able to get this kind of yield for too long.

Original Intention 3: To Set Aside as Reserves for Emergency Use

Since you may not need this money so soon, you potentially have a longer time horizon and thus have a higher ability to take risks. You can consider keeping part of your money in OA to have that liquidity in case of an emergency, but you can invest the other portion into, say, a globally diversified portfolio of equities and bonds, which should beat the 2.5% p.a. or even 4% p.a. But you need to have a time horizon of at least eight years.

Personally, I am not too excited about getting clients to invest their CPF money unless they absolutely need to do it. And if you have been asked to do so, I would sincerely ask you to take a pause and consider the above points before making the decision. It is, after all, still your hard-earned money.

The writer, Christopher Tan, is Chief Executive Officer of Providend Ltd, Southeast Asia’s first fee-only comprehensive wealth advisory firm and author of the book “Money Wisdom: Simple Truths for Financial Wellness“. He is also a Certified Ikigai Tribe Coach.

The edited version of this article was published in The Business Times in January 2025.

For more related resources, check out:

1. How To Make The Most Of CPF LIFE For Your Retirement

2. CPF Special Account Closure After 55: How to Prepare for 2025

3. RetireWell™ Part 1: Drawing Down Retirement Money

Providend promises to be a safe pair of hands and a second pair of eyes to help you avoid costly financial mistakes. You can find out more by reading our RetireWell™ eBook.

Through deep conversations with our advisers, you will gain clarity on what matters most in life and what needs to be done to live a good life, both financially and non-financially. Learn more about our investment philosophy here.

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current estate plan, investment portfolio, financial and/or retirement plan, make an appointment with us today.