In early September, Deputy Prime Minister Tharman Shanmugaratnam revealed that over the past ten years, more than 80% of CPF investors would have been better off leaving their money in the CPF Ordinary Account which earns a guaranteed 2.5% per annum and that 45% of CPF investors actually lost money. He highlighted that there were two reasons for this – high fees and behavioural biases. In this article, we will explore whether funds with lower fees would indeed deliver better returns for investors.

There are two types of fees involved in investing into funds: transactional fees which are incurred when buying and switching funds, and annual expense fees which include the salaries of the fund managers, trading expenses, marketing expenses and so on. Naturally, where transactional fees are concerned, there is no debate – the lower the better. It is with regards to the annual expense fees, also known as total expense ratios or ongoing charges, that there is usually a debate. If fund managers – with their education, intelligence, and superior resources – can consistently deliver high returns, why shouldn’t they be justified in being paid high fees? Arguably, that is true. Most of us would be happy to pay more for a product or service which is of better quality. However, as we shall see, the historical data reveals that most fund managers which charge higher fees do not consistently deliver better returns than funds which charge low fees.

What Are Low-Cost Investments?

Firstly, let us define what low-cost investments are. Low-cost investments are usually passive in that they seek to replicate the performance of an index, such as the Straits Times Index, and are therefore typically called ‘passive’ funds, or index funds. So when you invest in an index fund which is replicating the Straits Times Index, you are effectively investing into the thirty biggest companies listed in Singapore. Investing into index funds usually refers to a buy-and-hold approach to investing and requires one to believe that markets are efficient – meaning that the prices of securities already reflect all the knowledge and expectations that investors have of the securities in aggregate and that therefore it is difficult to consistently find mispriced securities. They usually have annual expense fees of about 0.5%p.a. or lower. In contrast, fund managers usually seek to beat the index’s performance through stock picking and market timing, and therefore the funds are usually called ‘active’ funds. So a fund manager who is trying to beat the Straits Times Index will not just limit himself to the thirty biggest companies but will invest into any stocks that are listed in Singapore that he feels will give the highest returns. ‘Active’ fund managers believe that they can consistently find mispriced securities – buying them while they are cheap and selling them when they are higher – as well as predict whether markets will go up or down in the future and make profitable decisions based on their forecasts. They usually have annual expense fees of 2%p.a. or more.

Active vs Passive Funds

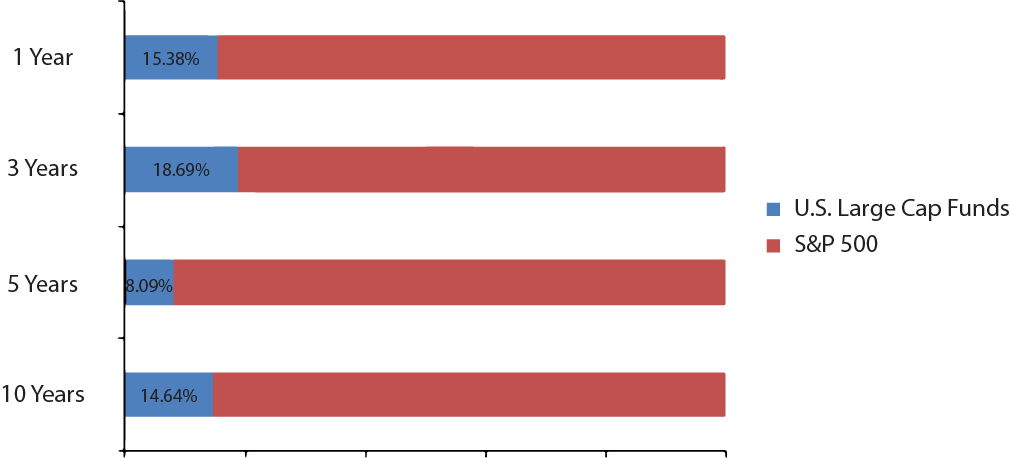

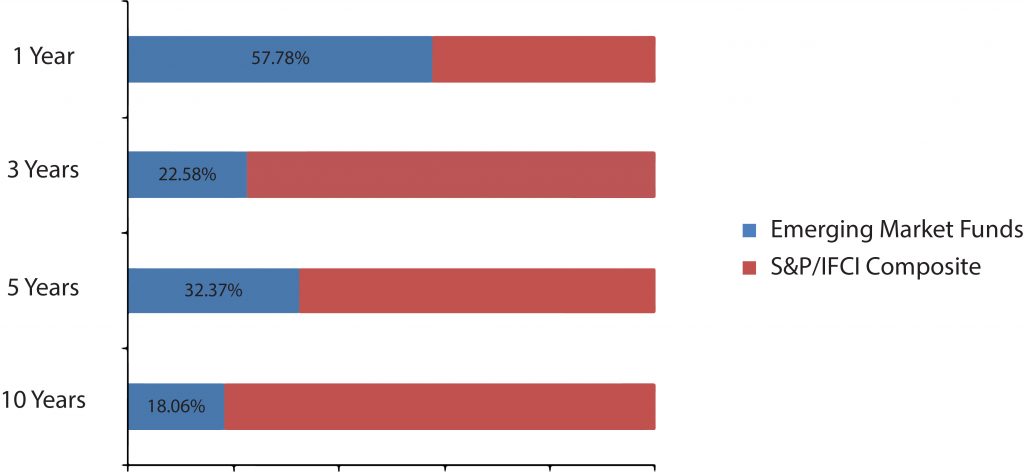

Whether ‘active’ funds or ‘passive’ funds deliver better returns for investors is a debate that has raged on for decades, and is unlikely to end anytime soon. However let us look at the data compiled by S&P Dow Jones Indices: as of June 2016, the number of actively managed U.S. Equity funds which beat the S&P 500 index over ten years is 14.64%[1]. In other words, an overwhelming majority of active funds failed to beat the index, also known as their benchmark. There is a widely-held belief that active managers should outperform in less efficient markets such as in Emerging Markets; however, the data does not appear to support this: the percentage of actively managed Emerging Market funds in the U.S. which beat the S&P/IFCI Composite benchmark over ten years was only 18.06%[2]. The percentage of active funds which beat their benchmarks improved when viewed over shorter durations such as one and three years, but once viewed over longer durations their lack of consistency in doing so was evident. Additionally, over ten years, only 54.35% of the U.S. funds benchmarked against the S&P 500 survived, with the rest closing or merging with other funds[3]. So choosing an active fund that might outperform an index fund is one challenge – choosing an active fund that will still be in business after ten years is another.

Percentage of U.S. Large Cap Equity Funds in the U.S. that Outperformed the S&P 500 Benchmark

Source: S&P Dow Jones Indices LLC, CRSP. Data as of June 30, 2016. Chart is provided for illustrative purposes.

Past performance is no guarantee of future results.

Percentage of Emerging Market Funds in the U.S. that Outperformed the S&P/IFCI Composite Benchmark

Source: S&P Dow Jones Indices LLC, CRSP. Data as of June 30, 2016. Outperformance is based upon equal-weighted fund counts. All index returns used are total returns. Chart is provided for illustrative purposes. Past performance is no guarantee of future results.

Why Do Most Active Funds Underperform Their Respective Benchmarks?

One clear reason is fees. Eugene Fama, Nobel Laureate in Economic Sciences, pointed out that before costs, an active investment must be a zero-sum game, in which active investors who have positive returns must have made it at the expense of other active investors. After costs, however, in terms of net returns to investors, the active investment must be a negative-sum game.[4]

Another reason is that many fund managers simply may not have the skill required to beat their benchmarks over the long run. Moreover, while there may be fund managers who have the skill to beat their benchmarks consistently, identifying who they are is a challenge. The obvious route would be to look for funds or fund managers who have performed well in the past few years and infer that they are likely to have done so due to skill. However, the history of financial markets is littered with star fund managers whose outstanding performances proved to be unsustainable over the long term. Fund managers Richard Dennis, Bill Miller, and John Paulson are just a few examples of fund managers who became legendary due to their investing performance, only for their funds to perform poorly thereafter – typically after investors rushed to put their hard-earned money with them. Mark Carhart’s study in 1997 concluded that there was no evidence of outperformance among active funds over the long term, and highlighted that expense ratio, portfolio turnover, and load fees had a significant and negative impact on performance.[5]

Let us look at the latest data compiled by S&P Dow Jones Indices which shows the persistence of U.S. equity fund performance over the past five years. The data and the conclusions we can draw from it could not be clearer: out of the 664 funds which were in the top 25% of U.S. equity funds in March 2012, only 11.90% remained in the top 25% in the very next year.[6] By March 2016, only 0.30% – 2 out of the initial 664 funds – was still in the top quartile. This shows the inconsistency of active fund managers, and how a strategy of simply looking for the best fund performers in any given year is likely to fail.

Source: S&P Dow Jones Indices LLC. Data for periods ending March 31, 2016. Past performance is no guarantee of future results. Table is provided for illustrative purposes.

Summary

Based on the data compiled by the S&P Dow Jones Indices, on average, low-cost, passive investments have largely outperformed and should continue to outperform, high-cost, active investments over the long term due to their lower fee structure. While it can be tempting to try to pick the exceptional fund manager who can outperform an index over the long term, academic research and the data from S&P Dow Jones Indices show the difficulty in finding one who can perform consistently over a long period. This is why, at Providend, we have always recommended that our clients invest into low-cost, well-diversified funds for the long term as we believe that this will give them the greatest probability of obtaining the highest investment returns.

This is an original article written by Sean Cheng, Solutions & Investments Executive at Providend, Singapore’s Fee-only Wealth Advisory Firm.

[1] https://us.spindices.com/documents/spiva/spiva-us-mid-year-2016.pdf [2] https://us.spindices.com/documents/spiva/spiva-us-mid-year-2016.pdf [3] https://us.spindices.com/documents/spiva/spiva-us-mid-year-2016.pdf [4] Fama, Eugene F., and Kenneth R. French, 2009, Luck versus Skill in the Cross Section of Mutual Fund Returns, The Journal of Finance, forthcoming. [5] Carhart, Mark M., 1997, On Persistence in Mutual Fund Performance, Journal of Finance (March 1997), 57-82. [6] http://us.spindices.com/documents/spiva/persistence-scorecard-august-2016.pdfWe do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current investment portfolio, financial and/or retirement plan, make an appointment with us today.