Launched on 9 January 2009 by Satoshi Nakamoto (no one really knows who he is or who they are; it is presumed to be the pseudonym for a person or a group of people), Bitcoin became the world’s first cryptocurrency. When it was first issued, its price was next to zero.

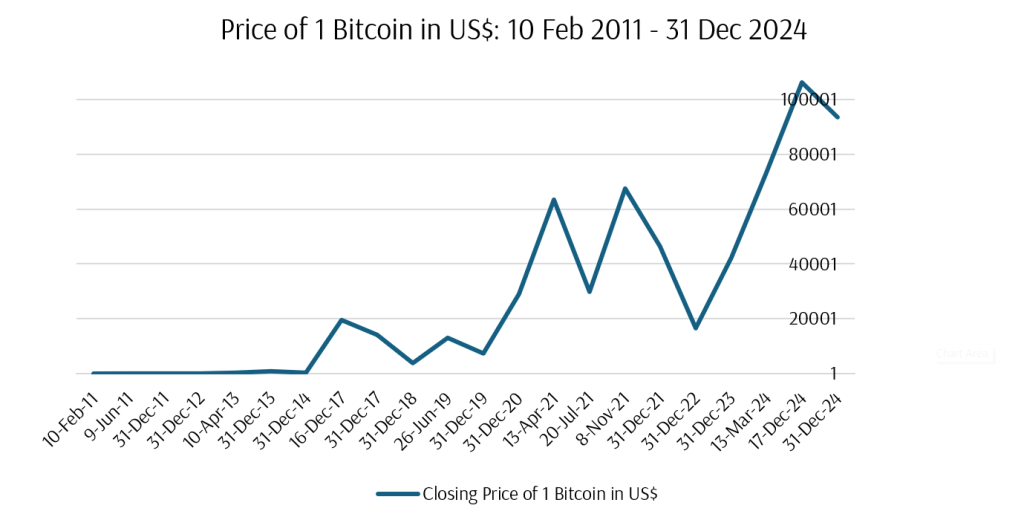

If you had invested in Bitcoin sometime in January 2011 and held it until 31 December 2024, your ROI would have been a whopping 165% p.a., provided your heart could withstand the rollercoaster ride and you had stayed invested. Because while the price has skyrocketed, it has been nothing short of extremely volatile (see chart below).

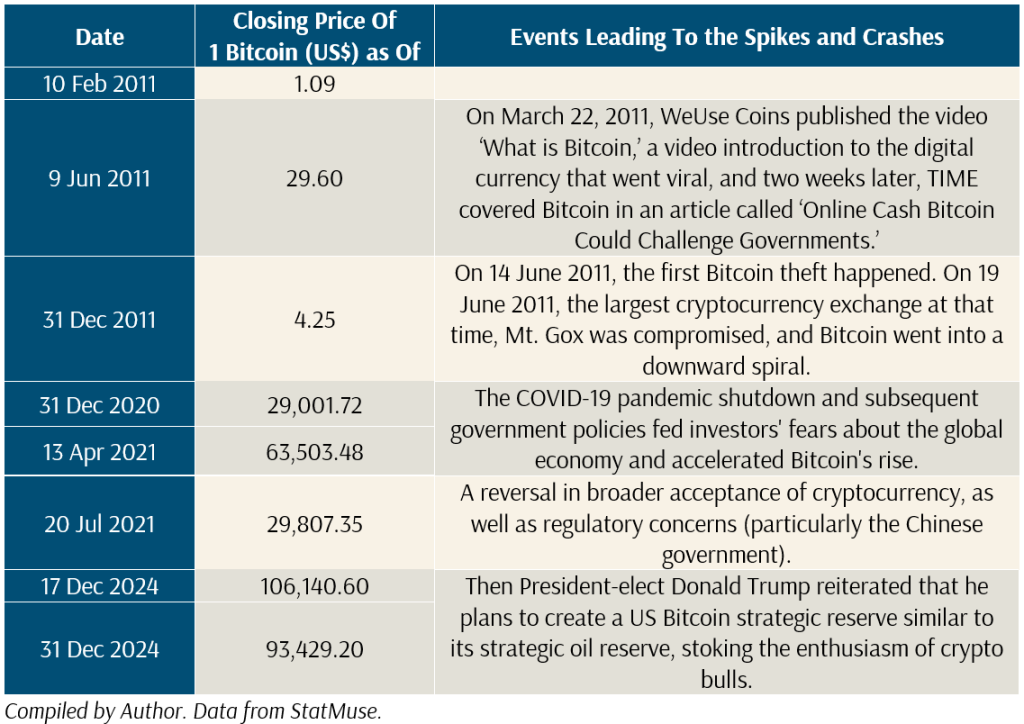

From the chart, you will notice a few “spikes” and “crashes,” all within a matter of months. But the chart does not do justice in showing Bitcoin’s volatility, so I have tabled some of the booms and busts of Bitcoin in the past 15 years, and you will notice that:

- From 10 February to 9 June 2011, Bitcoin rose by about 2616%.

- From 9 June to 31 December 2011, Bitcoin fell by about 86%.

- From 31 December 2020 to 13 April 2021, Bitcoin rose by about 119%.

- And about three months later, on 20 July 2021, it fell by 53%, back to the same level as seven months ago.

Sometime in the second half of 2021, a client asked me whether we would include cryptocurrency in our portfolio, and a prospective client who wanted to invest with us decided to invest half of his wealth in cryptocurrency instead. That was the period when Bitcoin and cryptocurrencies were doing well. Today, with US President Donald Trump being a big supporter of cryptocurrency, interest in Bitcoin and other cryptocurrencies is rising again.

But whether or not you should include cryptocurrencies in your portfolio really depends on your financial and investment objectives.

At Providend, we manage our clients’ money for their non-negotiable life events (such as retirement) and goals (such as taking a year of sabbatical to volunteer for a cause). So, the approach we use needs to give them the highest probability of success. As such, part of that approach includes looking for investments that will reliably give long-term expected returns.

Such investments must participate in and contribute to global economic production because returns are generated from the value created through positive contributions. If an investment does not create any added economic value, then we should not expect it to deliver long-term investment returns.

As an example, equities and bonds are ways for investors to provide capital to a company to conduct its business activities. The company is expected to create value for its customers through the delivery of goods and services. Investors receive returns if the business is successful and lose money if the business is not successful. Long-term returns from equities are based on their expected future earnings.

Cryptocurrencies, using Bitcoin as an example, are not such an investment. If you look at the table above, the returns from Bitcoin and its booms and busts have come from speculation due to news and events. There is no pattern and almost no way for one to reliably predict the future prices of Bitcoin.

You have to honestly ask yourself: Do you want to rely on this kind of speculative instrument to achieve your non-negotiable life events and goals? And given the volatility, if you had parked a sizeable amount into it, would you be able to stay invested through that crazy ride? If your answer is no to both questions, Bitcoin and other cryptocurrencies are not suitable to be included in your portfolio because they are simply too unreliable. And I have not even talked about the risks of your cryptocurrencies being stolen, the risks of crypto exchanges collapsing, and fraud yet.

So, is there no place for Bitcoin or other cryptocurrencies in your portfolio? My suggestion is that if you really want to invest in this “asset class,” do so after you have set aside funds for your non-negotiable life events and goals. Do not use money meant for this purpose to invest in this alternative “asset class.” It is simply too unreliable. Also, be prepared to lose money.

Not putting money into an investment that promises high-octane returns requires a heart of contentment, a philosophy that my firm believes in so much. Contentment is when you no longer crave or desire anything you don’t already have. But it is not a passive acceptance of your situation. Rather, it is a conscious choice to enjoy, appreciate, and accept what you have, while giving up the craving for things you do not have. It requires you to know what is important to you in your life and to accept that you can’t have everything. It requires you to take time to really consider what your non-negotiable life events and life goals are. Once your investment yields sufficient returns to achieve those objectives, you won’t need to look at others who may have earned higher returns elsewhere.

The writer, Christopher Tan, is Chief Executive Officer of Providend Ltd, Southeast Asia’s first fee-only comprehensive wealth advisory firm and author of the book “Money Wisdom: Simple Truths for Financial Wellness“. He is also a Certified Ikigai Tribe Coach.

The edited version of this article was published in The Business Times on 17 February 2025.

For more related resources, check out:

1. Active Investing That Adds Value to the Client

2. Investing in the S&P 500 Alone is Not the Silver Bullet

3. Why It’s Hard to Reallocate Assets with Conviction—and How to Overcome It

Download our Investment eBook titled “A More Reliable Way to Get Enough Investment Returns: Even During Times of Market Uncertainty” here.

Through deep conversations with our advisers, you will gain clarity on what matters most in life and what needs to be done to live a good life, both financially and non-financially. Learn more about our investment philosophy here.

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current estate plan, investment portfolio, financial and/or retirement plan, make an appointment with us today.