I always wondered why we need to pay a king’s ransom for an omakase (“I leave it up to you”) meal where the chef decides what is good for me. Should not the premium be justified only if the chef prepares the meal based on what I want as a customer? I call this ‘reverse omakase’ (“I tell you what I want, and you do exactly as you are told”).

For our 11th wedding anniversary in July 2023, I decided to surprise my wife by bringing her to an exquisite culinary experience where the chefs who are decked in their immaculate chef’s uniforms prepare our lunch right in front of us based on our preferences.

It was a strange wedding anniversary lunch. Despite my best efforts, my wife was totally preoccupied with something else. Her digital arsenal (comprising two laptops, one iPad, and three mobile phones) was blazing in full glory in preparation for the key battle. To secure Taylor Swift concert tickets using the UOB advance sale promotion on 5 July 2023.

The best-laid plans of man and mice often go awry. My wife did not get any concert tickets that day. She was not impressed with the exquisite culinary experience at Subway. And she surprised me by telling me to sleep on the living room sofa that day. Laying on the sofa that night under the hypnotic swirling of the enlarged shadows of the ceiling fan blades cast onto the ceiling, I wondered why my wife was so obsessed with Taylor Swift.

What is the Fear of Missing Out (FOMO)

FOMO mean fear of missing out on something which is of certain importance which is why experiencing FOMO can affect certain people negatively. These important matters include social belonging and deals too good to be missed out.

Emily Laurence did a brilliant job of describing the psychology behind FOMO in her article titled “The Psychology Behind the Fear of Missing Out (FOMO)”. She opined that a sense of belonging is a fundamental human need which is important for both physical and mental health. Thus, experiencing FOMO can affect certain people such as avid social media users more negatively. Patrick J. McGinnis popularised the term FOMO in 2004 while writing for the Harbus, a non-profit self-funded news organisation of Harvard Business School run by students.

Examples of FOMO in the Financial World

Even Sir Isaac Newton, the brilliant physicist and mathematician, succumbed to FOMO. The announcement by the British government that the South Sea Company would take over most of the British national debt in early 1720 precipitated the extraordinary rise and fall of the value of the stock in 1720. In a classic example of FOMO, Sir Isaac Newton re-entered his positions in a bigger way at the peak of the stock price in June to July 1720 after exiting with a profit in April 1720. The stock suffered a drawdown (peak to trough) of 85% from July to December 1720 and Sir Isaac Newton’s fortunes took a big hit.

Closer to living memory, I witnessed a FOMO movie playing out in full splendour in the unfolding of the Dot-com bubble when I was an Accountancy undergraduate at Nanyang Technological University (NTU). The price earning (PE) ratio of Nasdaq reached an astounding 200 with the most valuable company, Cisco Systems, trading at a much saner PE of only 125! The PE ratio of the three largest companies by market capitalisation, Apple, Microsoft, and Nvidia, is about 36, 39, and 74 respectively on 17 July 2024 (You are welcome!).

I recalled vividly grandparents in walking sticks in long snaking queues at the old Exchange building on Cecil Street, eager to open a broking account to invest in anything related to the Internet with high hopes of making hundreds of thousands of dollars with little to no effort. Opening an account online was not possible then. Everyone in town especially the taxi drivers became financial gurus whose eyes glowed like “Gollum” when they proclaimed in a secretive, hushed voice, “THIS TIME IS DIFFERENT”.

I personally benefited from the Dot-com bubble. I exited the market before its peak in March 2000 with some profits I had made from my pitiful savings as a poor student. Unlike Sir Isaac Newton, the market crashed before I “FOMOed” and had a chance to get back into the market.

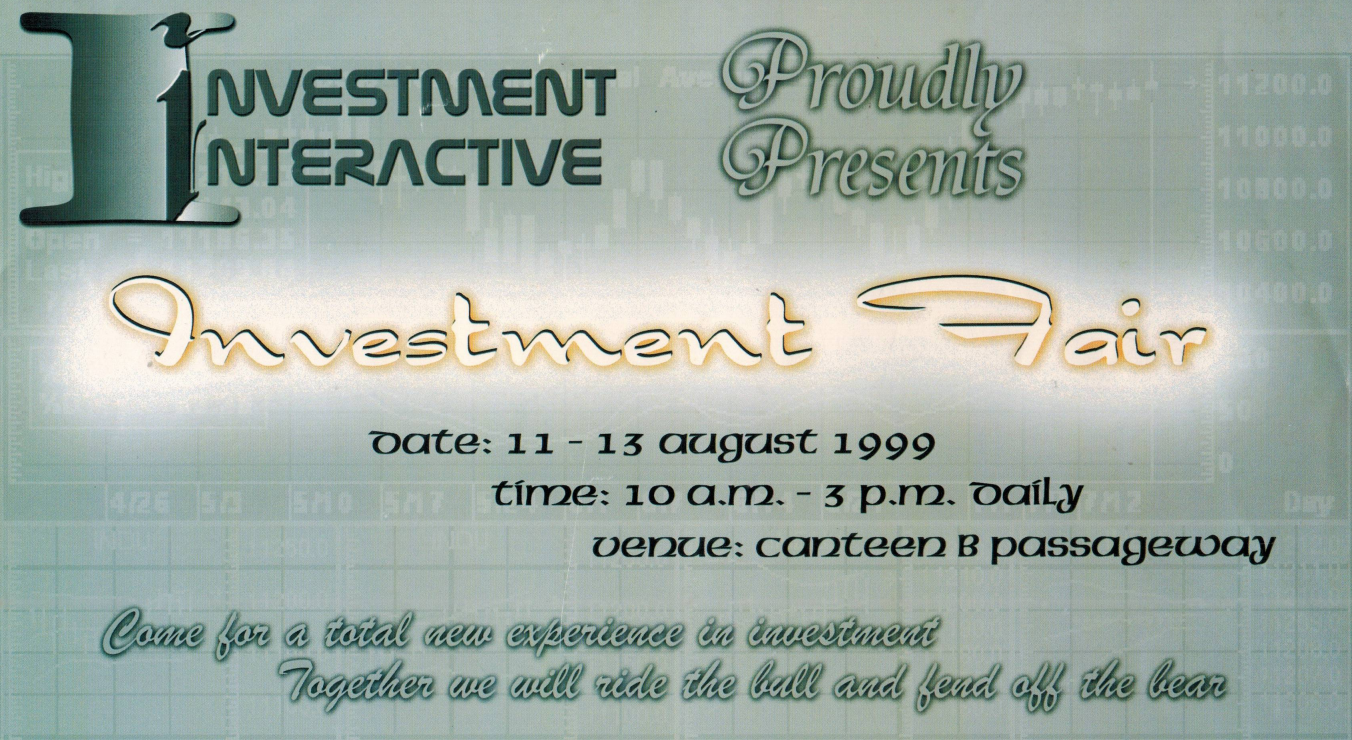

As one of the founders and the Director of Investment Promotions for Investment Interactive Club in NTU, the first investment club in a tertiary institution in Singapore which was formed in 1999, our recruitment drive and all the events I organised were overwhelmingly oversubscribed. Hundreds of students turned up for our investment talks with many without tickets happy to stand or sit on the steps. The Investment Fair I organised was so successful that faculty members and students were happy to miss lessons to form long snaking queues to open broking accounts, just like their parents or grandparents at Cecil Street.

To be clear, I was talking about the students. While excited, the professors who missed their lessons appeared to be genuinely apologetic.

Enjoy these nostalgic photos from the past:

Why We Get FOMO in the Financial World

I opine that there are two reasons why we suffer from FOMO in the financial world.

1) Self-Interest

There is an army of self-interested people who would evangelise and glorify certain messages to their advantage. We only see opportunistic influencers who drum up sexy stories of Artificial Intelligence (AI), technology, or meme stocks dominating the social media world and not well-meaning influencers who espouse the value of long-term and globally diversified portfolios due to the natural selection of social media algorithms that gravitate towards addictive content with high retention.

The songs of the financial sirens (traditional media, social media, “FOMOers”) would be seductively strong, sensational, and satisfying at times. Do you expect Keith Gill (the “Roaring Kitten”) to give a boring and traditional analysis of GameStop stock using the latest audited financial statements? In the wise words of Warren Buffet, “Don’t ask the barber whether you need a haircut.”

2) Rewards Without Efforts

We want to make our wealth as fast as possible with as little effort as possible. This is why the universal catchphrase of all Singaporeans is ‘HUAT AH’ (meaning to prosper). It seems perfectly appropriate to shout this catchphrase at weddings, at prayers during Qing Ming Festival in remembrance of our ancestors, or at any community or corporate events. Somehow, some celestial beings or our deceased relatives would bestow great fortune on us when we simply shout out this magical catchphrase.

The Straits Times reported in June 2023 that a study by a Wealth Manager posited that affluent Singaporeans take an average of 21.3 years to climb the wealth ladder to the level of financial freedom (“having sufficient assets to generate enough passive income for life”) and an average of 32.3 years to reach the level of financial abundance (“having more than enough income for one’s lifetime”).

At Providend, a colleague is well-known for achieving financial independence (FI) in his thirties. The reasons why he succeeded. He does not suffer from FOMO, and he treats Howard Marks, David Blanchett, and Michael Finke (doyens in the investment and financial planning fields) as Taylor Swift. The reason I think why even affluent Singaporeans are not able to match up to my colleague with the earliest ones achieving FI only in their forties, they suffered from FOMO and they treat Taylor Swift as Taylor Swift.

On an anecdotal level, I know of many friends whose “Gollum” surfaced in the darkness of the night when Wall Street was bustling with life. Seduced by the bewitching and dancing flashes of green tickers on their screens that validate the songs of the financial sirens, they uncontrollably shouted “MY PRECIOUSsssssss” and re-entered the positions they had exited earlier with small profits but this time as the stock price reached record highs, just like Sir Isaac Newton. They are reminded of their “Gollum” moments each time they see their investment statements with familiar names such as Alibaba, GameStop, and Sea Ltd. And the great teacher “Gollum” taught them the most important investment secret which well-meaning academics could never impress upon their students, to become a really, really long-term investor!

Personal Experience

I am proud that I do not suffer from FOMO, usually. As an example, I spent a fair amount of time studying blockchain technology and cryptocurrencies to be aware of what others are interested in or are talking about. I was intrigued to read books and articles about this subject and to watch the full series of the online course “Blockchain and Money” offered by MIT comprising 23 sessions of about 1.5 hours each that is taught by Professor Gary Gensler (now the Chairperson for U.S. Securities and Exchange Commission). I even bought a Ledger Nano X to better appreciate how a hard wallet works.

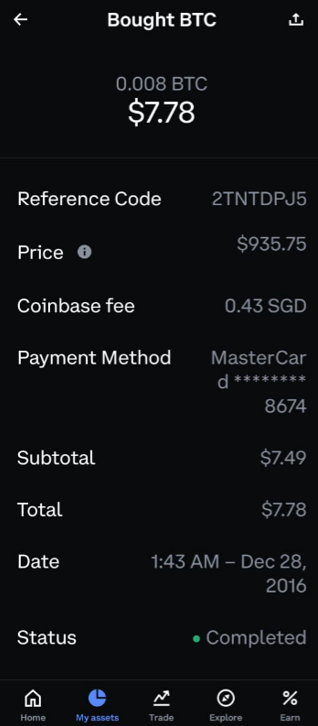

You must be wondering how much I have invested. My wife was full of admiration when I told her I made close to a phenomenal 10,000% return on my bitcoins in October 2021. That is a hundred bagger in five years! My “genesis” and only Bitcoin trade was on 28 December 2016 when I spent S$7.78 (which includes Coinbase Fees of S$0.43) to buy 0.008 units of Bitcoin. I recalled she instinctively blurted out, “Poor judgement, as always. Imagine you have invested $30,000. We could have retired already”. I also instinctively blurted out, “Yeah, you knew that the day I married you”. To keep a long story short, I slept on the sofa that month.

To the naysayers, I understand the rationale in terms of comparison to physical gold as a store of value and inflation hedge. Physical gold does not offer any yield with high holding cost and yet has performed well with an average annual return of 7.98% between 1971 and 2024 according to Statista. Cryptocurrencies that have become mainstream like Bitcoin and Ethereum may have their place as a small diversifier in portfolio construction and asset allocation of a well-diversified portfolio. However, it should not be a core investment vehicle or holding for most people.

Keep to Basics

I believe in keeping to the basics as the best way to steadily achieve financial independence. I count my blessing to read a short online article by WallStraits.com titled “Don’t Buy Insurance” on 17 July 2000 which I have saved in my hard disk drive. Unfortunately, natural selection by web browser engines and social media algorithms means this masterpiece could no longer be found on the internet. 24 years later, the four simple concepts in that article still ring true for me:

- Don’t buy any insurance that doesn’t directly protect you and your family against a catastrophic event you can’t afford to face on your own.

- Don’t buy life insurance that is considered an investment.

- Invest Sagely. Set up a long-term stock portfolio with your regular savings that is free from other obligations.

- Be disciplined about your savings and investments.

I got lucky again when I first came to know about Providend in May 2003 from a physical Business Times (“BT”) Article which I have cut out and kept. I have followed Providend since then as their values and philosophies resonated strongly with me. The four simple concepts I first came across in the WallStraits.com article are applied in Providend with great rigour and in the best interests of our clients.

In 2023, the ultimate bootlicker in me showed my interviewer, Christopher Tan (CEO of Providend), the 20 years old BT article cut-out which has shifted house with me multiple times and I told him I have followed Providend and him since 2003. My interview was effectively over at the 8-minute 88-second mark.

Conclusion

To the three most important readers of this article – my children. If you were to forget everything I have written, just remember this. If you want to improve your odds of achieving financial independence, do not suffer from FOMO and keep to the basics. While I cannot predict the future, I hold the highest conviction that my children’s children (not yet born) would in time to come appreciate this wisdom as the biggest legacy given to their parents by their parent’s parent.

It is never easy to have delayed gratification especially when we are talking about something that will take years or even decades to play out. I hope you will be enlightened by this quote from an influencer in China, Dong Yu Hui (董宇辉), who is highly respected for his personable, scholarly, and motivational style, “People who are afraid of hardship typically toil for their whole life. People who are not afraid of hardship usually only need to endure hardship for a period.” (怕辛苦的人往往辛苦一辈子,不怕辛苦的人往往辛苦一阵子). I believe this quote resonates strongly with the founders in Providend and many of our clients who have toiled and eventually succeeded because they are not afraid of hardship and are disciplined in keeping to time-tested winning strategies.

Fast forward one year in July 2024 and I am now driving my wife to a conventional and boring omakase dinner for our 12th wedding anniversary celebration. Surely, I would not make any mistake by playing it safe this year. While driving over to the restaurant with my Spotify App playing the music in the background, my wife asked, “What kind of lousy, cheesy, cringy song is this? What do you mean by shake this and shake that?” I replied hesitantly, “Errmmm, this is Taylor Swift Shake It Off, Your Majesty!” To my children’s children, if your parent has FOMO genes, do not blame your grandfather as you know which side of the family they have got it from.

I think I am sleeping on the sofa again this month when my wife reads this article.

This is an original article written by Foo Jit Hwee, Associate Adviser at Providend, the first fee-only wealth advisory firm in Southeast Asia and a leading wealth advisory firm in Asia.

If you are interested in joining our Providend Associate Adviser Programme, kindly visit this link to find out more: https://providend.com/careers

For more related resources, check out:

1. A More Reliable Way to Get Enough Investment Returns

2. Investing in the S&P 500 Alone is Not the Silver Bullet

3. Stop Making New Year Resolutions Which Will Fail!

*Providend is very excited to share that we are now ready to extend our service offerings to the younger accumulators who are looking for holistic, independent, conflict-free wealth advice!

For this group of younger accumulators, we know that it is not easy to make retirement planning a priority when other financial goals – buying a first home, for example, or saving for a child’s education – appear more pressing. Learn how we can help here.

Through deep conversations with our advisers, you will gain clarity on what matters most in life and what needs to be done to live a good life, both financially and non-financially. Learn more about our investment philosophy here.

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current investment portfolio, financial and/or retirement plan, make an appointment with us today.