To get ready for your retirement, or your financial independence, you will need a recurring stream of cash flow.

We often have clients seeking our help to evaluate certain financial products which can provide them with a regular income component. They would like to know how these products fare against their current portfolio of financial assets or even some of the solutions we recommend to them.

Below are two products which we find to be popular among clients and the general public to get a regular income:

- Whole life or endowment plans that provide income. These are plans sold by insurance companies whose objective is to provide a regular income. Here is how these plans typically work:

- An investor will contribute a lump sum or recurring capital for a fixed number of years. After 5 years, the plan provides a regular income to the investor. The regular income is partly guaranteed and non-guaranteed. The regular income can either go on forever, provided the plan still has value, or the regular income has tenure for 10 to 20 years. They are sometimes labelled broadly as a private annuity or retirement plans.

- Unit Trusts / Exchange Traded Funds (ETF) that provides a dividend income. These are funds actively or passively managed with an investment mandate in certain investment philosophies, particular geographical regions, sectors, asset classes. The unique thing is that they provide investors with monthly or quarterly income, which is not guaranteed and can be volatile.

For a lot of investors, they prioritize this income component as a key consideration when deciding whether to invest in investment A, investment B or investment C.

But in our opinion, while the ability to generate income is important, having a passive income should not be the main criteria in evaluating whether you should choose investment A over investment B or C.

Some of the funds that you are currently evaluating may not distribute an income by default. We often refer to these funds as accumulating funds, which are different from distributing funds that distribute a passive income on its own.

Accumulating funds are not worse off than distributing funds if you are seeking investments more suitable during your phase of accumulating for financial independence. We would argue that they can be better since they give you the option of withdrawing a smaller or large sum of passive income.

This article will explain to you how your accumulating funds can generate passive income and how that looks like in real execution.

Executive Summary

The key criteria when choosing whether to add an investment into your portfolio is not whether the investment provides an income. Instead, the investment should increase the long term returns of your portfolio or reduce the volatility of your portfolio or both. A certain level of liquidity is important but should not be the main priority when making portfolio decisions.

In an accumulating fund, the manager of the fund concentrates on making the investment decisions, based on their investment mandate to generate good total returns for the investors. Whatever income provided by the underlying bonds and stocks are reinvested into the accumulating fund.

The investor, together with his or her Client Adviser, makes the financial planning decisions on how much income they should get.

The investor can generate the passive income by selling a certain amount of units of the fund he or she owns. For example, if the investor requires $35,000 in income the next year, she can sell 35,000 units worth $1 to generate the income.

Investors do fear that by selling units, they may run the risk of depleting their capital. In this article, we will show that the investor will not deplete their capital if they are able to spend prudently. While the total units they own decreases over time, the value of each unit they own would have also increased dramatically over a span of 30 years.

The main advantage of separating the investment and the financial planning decisions is that clients can have a fund that concentrates on earning a higher total return, while they have the flexibility of having a passive cash flow that can be lumpy or inflation-adjusted or both.

Working with a Client Adviser that is trusted yet competent will allow the client to have greater peace of mind to have a more stable, reliable income.

Now let us investigate this in greater detail.

Firstly, here are some of the criteria you should look at when deciding what kind of investments to add to your portfolio.

The Criteria To Add An Investment Into Your Portfolio

First and foremost, an investment needs to have a high probability of giving you a positive expected return. The value of the investment can be volatile in short periods, but you have to see that there is strong evidence that over time, the returns are positive.

When you add an investment into your portfolio, the investment should either:

- Increase the long-term total returns of your overall portfolio. Your investment has an income yield and a capital gain or loss component over the long run. We need to compare investments by comparing the total return of their income yield and capital gain instead of just the income yield.

- Reduce the volatility of your overall portfolio. In financial terms, volatility is measured as the standard deviation. The standard deviation should be as low as possible.

Adding this investment should give your overall portfolio an even better risk-adjusted return.

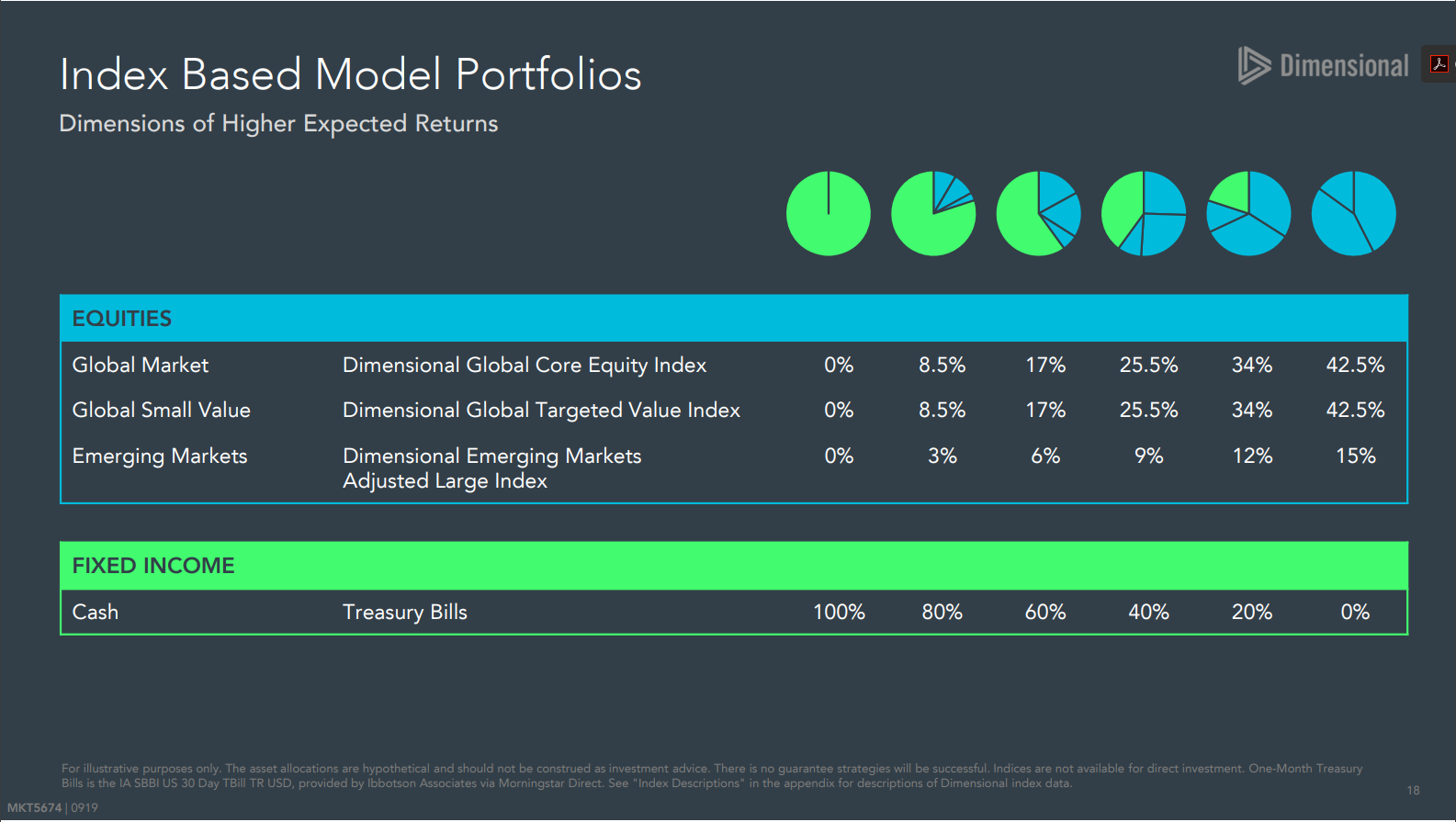

For example, we recommend Dimensional funds to our clients because Dimensional’s research has shown that the dimensions of smaller companies, value companies and companies with higher profitability tend to give higher returns over time. There is evidence of this over many periods of time, and across different markets. However, there is no free lunch, the volatility of the funds tends to be higher as well.

The table below shows the annualized long term returns and volatility (annualized standard deviation) of 6 portfolios with different amounts of equity and bonds:

The more faded annualized return and annualized standard deviation shows the range of returns and volatility of the portfolios if we make up our portfolio with low-cost funds that mirror broad-based indexes.

When we change out these low-cost index funds and replace them with low-cost funds that try to capture the dimensions of small, value and higher profitability, the portfolio has a good probability of generating higher annualized returns with only a slight increase in volatility.

How You Will Interact With An Accumulating Fund

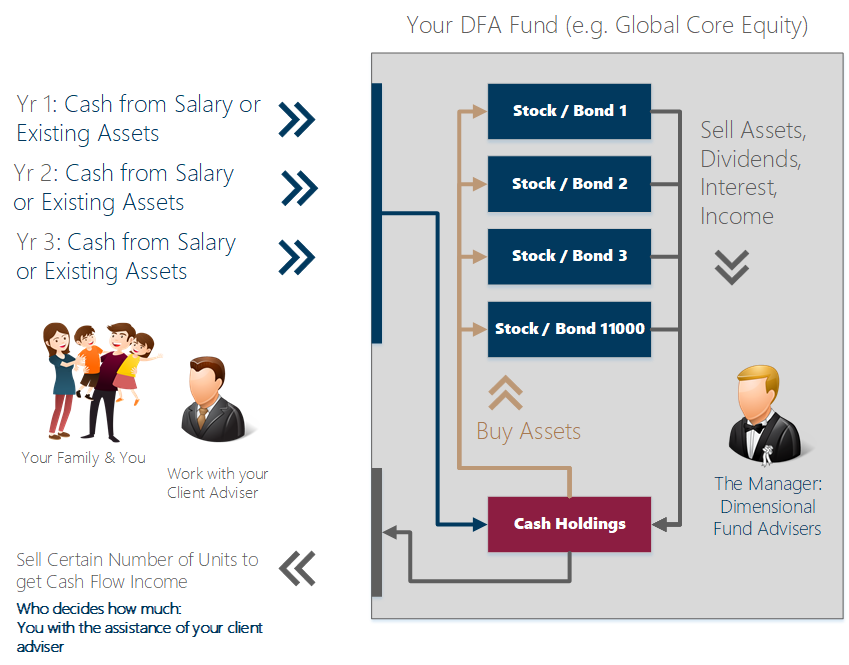

The following diagram shows how a typical investor lives with an accumulating fund investment:

The grey box represents what happens in a fund (we use a DFA fund here as an example) on a high level. You have worked with a financial planner to channel a certain part of your salary into a DFA fund on a recurring basis.

Within the fund, the manager takes the money from yourself as well as other investors and buys a set of stocks, or bonds, or other investments according to their investment philosophies/strategy. This can be either passive or active.

A fund, regardless of whether with a passive or active manager behind it, is one of the most passive ways to build wealth. You can focus on living your life, while the manager makes the investment decisions and some of your capital allocation decisions (where your money should go).

When these stocks or bonds regularly distributes dividend income, interest income to the fund, the manager farms these incomes back through the cash holdings and buys more stocks or bonds.

This is where an accumulating fund differentiates from a distributing fund.

The manager does not decide whether to pay out a passive income to the fundholders or how much to pay out.

As the unitholder, you will see the value of your fund grows.

You decide how much passive income you need. At Providend, our clients with work their Client Adviser to decide the right, prudent amount of passive income they should withdraw from the fund.

So an accumulating fund gives you a lot more control than a distributing fund.

How An Accumulating Fund Can Provide Income For You?

Typically, an investor will purchase a certain number of units of a fund at a certain price.

Sara has SGD$1 million.

She wishes to retire and hopes her SGD$1 million will be able to provide some income for her.

She worked with a Client Adviser and allocate this SGD$1 million into a single, low-cost DFA Global Core Equity fund.

This fund invests in a portfolio of 7,800 stocks that are diversified across the world. The current expense ratio is about 0.35%. This fund does not distribute a dividend on its own.

So Sara will purchase 1 million units, at a hypothetical price of $1.00.

She needs to withdraw 3.5% of her initial capital at the end of the first year, for her spending in the next year. This works out to be $35,000.

If the price is still at $1.00 at the end of the year, she will sell $35,000/$1 = 35,000 units. After the transaction is approved, $35,000 will end up in her bank account, which she can use to spend for year two.

At the end of year one, Sara will be left with 1,000,000 – 35,000 = 965,000 units worth $1.00.

The decision-maker of how much income to “give out” here is not the fund manager at DFA. The manager at DFA concentrates only on the investing aspect. He leaves the decision to Sara (and in this case with her Client Adviser).

If You Sell Your Fund Units, Wouldn’t Your Capital Go Down Over Time?

There is this fear among investors that if you sell the units, over time, you will have fewer units. Your capital has to go down.

While as you withdraw more units from the fund, the number of units do go down, but the value of each unit is going up as well.

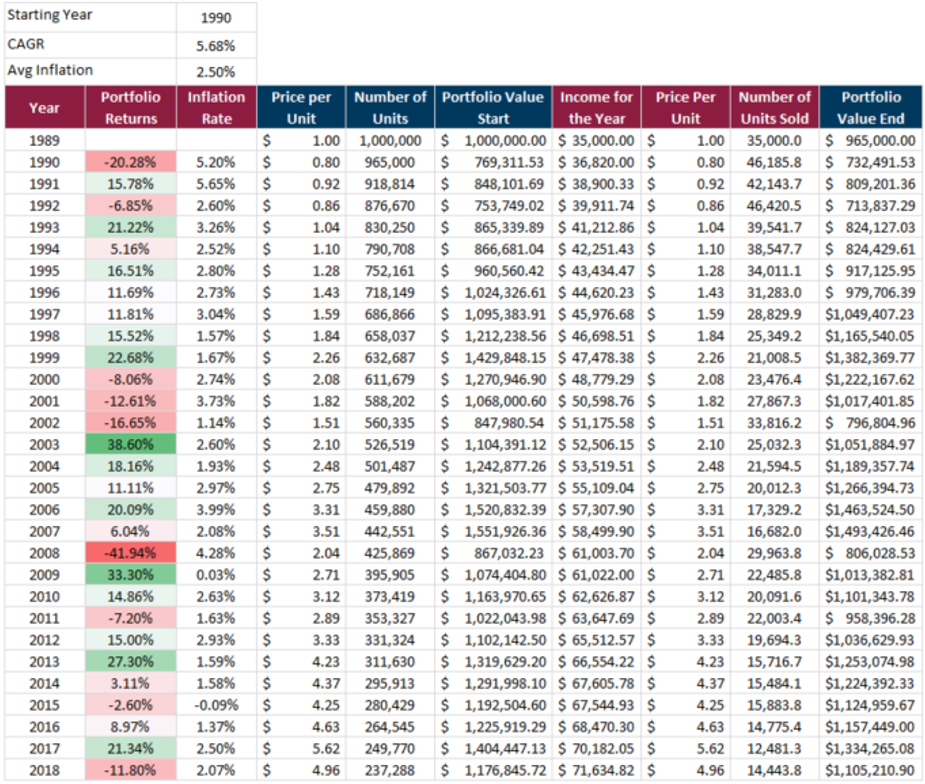

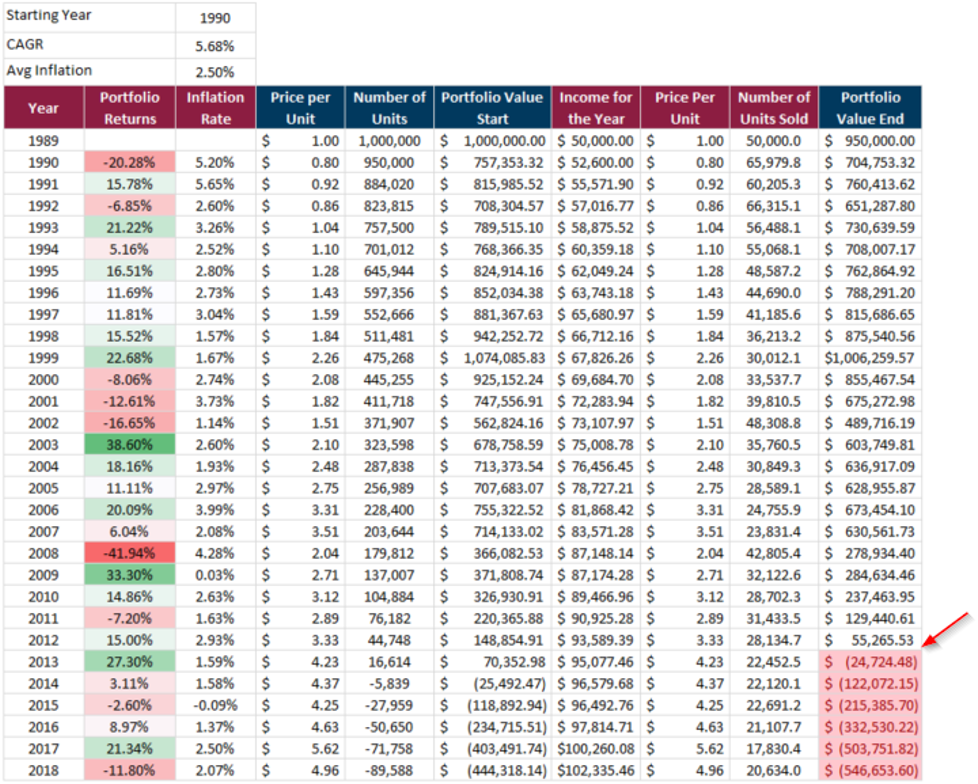

Let us continue to look at Sara and her Global Core Equity Fund and see what happens at the end of 30 years.

The same monies invested lived through the period of 1990 to 2018. The average compounded average growth of her Global Core Equity Fund is 5.68% a year, after factoring in 1.5% in total expense (expense ratio, platform fee, AUM fee) and an average inflation rate of 2.5%.

During this period, at the start, the fund experienced a 20% decline. Between 2000 to 2002, the fund experienced further 8%, 12%, 16% decline. During the Global Financial Crisis in 2008, the fund experienced a 42% decline. Suffice to say, it was not an easy period to live through.

Sara worked with her Client Adviser and decided to spend an initial 3.5% of her SGD$1 million funds in the first year, which works out to be $35,000.

In the subsequent years, Sara will adjust the following year’s spending by the inflation rate of the previous year. For example, if the previous year’s inflation is 5.2%, our client will withdraw $36,820 to spend in the second year. She will continue to do inflation spending adjustment throughout the years.

In this way, she is able to have an income that is adjusted to the prevailing inflation.

The table below shows the change in income withdrew by Sara and the portfolio value change over the past 30 years:

You would notice a few things.

At the end of the 30 years, Sara’s fund still has an ending portfolio value of $1.1 million. This is despite extracting $1.6 million in income over this 30 year period. If Sara is still alive, the fund can still provide her with income. If not, the next generation can inherit her fund.

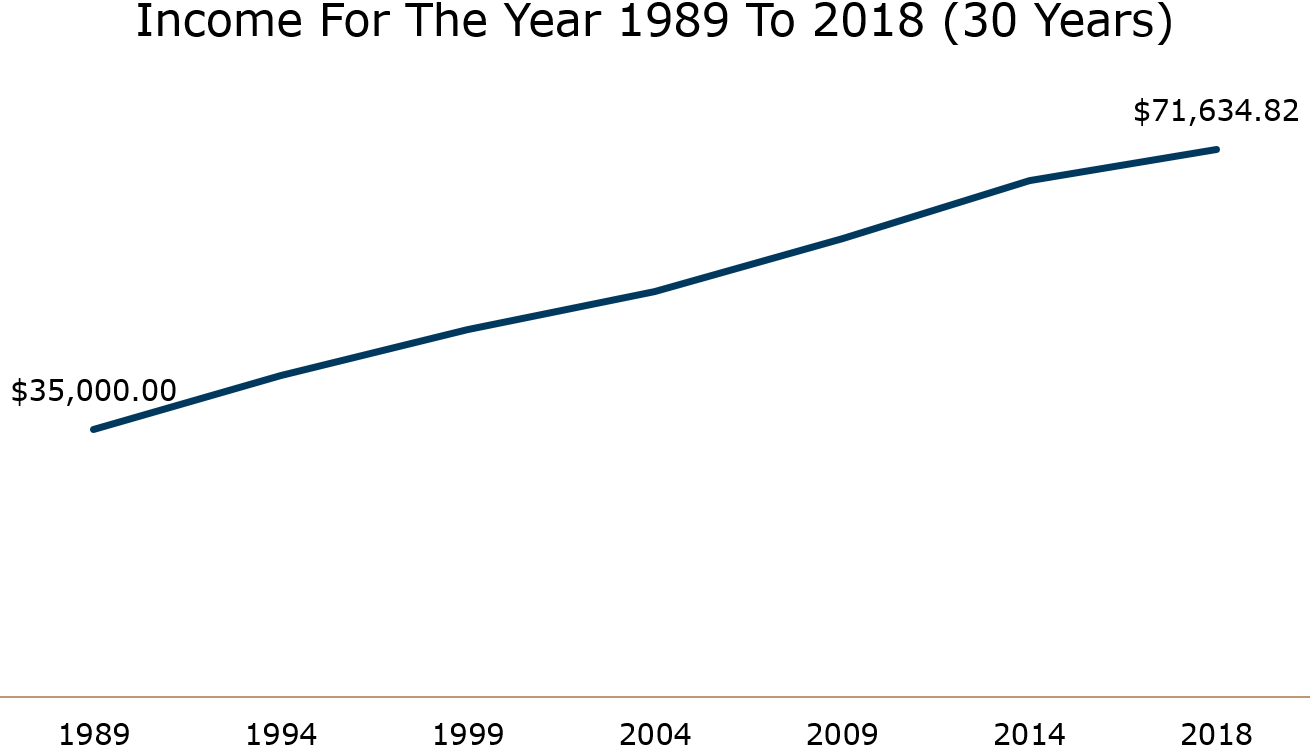

Despite the volatility in the portfolio returns, she managed to get an inflation-adjusted income. The following chart shows the growth of her income in nominal values:

Some other things we can observe:

- The price per unit of the fund went up from $1.00 to $4.96 overtime

- The number of units left in the fund (owned by the investor) went down from 1 million units to 237,288 units at the end

- The number of units sold, to provide the income every year gets lower and lower because, over time, each unit are sold at a higher price

- In the end, while Sara owns lesser units, but each of her units is worth more

The Main Advantage Of An Accumulating Fund Over Other Financial Options That Distributes Income

Sara’s example shows us a distinct advantage of an accumulating fund: We separate the role of investment management and financial planning.

A lot of funds out there do not pay an income.

They focus on their investment mandate and investment strategy to deliver returns to the investor.

If they deliver a high total return, the investor will have more money. When the investor has more money, it greatly secures his/her financial independence while maintaining the portfolio value.

The financial planning or wealth management role falls on the investor.

The investor can decide how much he/she wishes to spend and choose to withdraw more in certain years when there are sudden needs. The investor can also choose to spend less during years where his/her spending needs are lower. There is flexibility there.

In contrast, the other financial options for retirement may not have this flexibility:

- In a distributing fund, the fund needs to balance investment performance and distribution. If the underlying shares or bonds give less income, the manager will have to decide whether he or she wants to sell some capital to provide more income to the investor. This means that the income distributed will be volatile as with the performance

- In an endowment, bond, the income pay-out is rather fixed. In the case of endowment, part of the pay-out is guaranteed while the other portion is non-guaranteed. If you wish to keep up with inflation, you would need to look at other options.

- If you hold a portfolio of dividend stocks, the management team in the underlying stocks decide upon the capital distribution. They would have to be prudent to only distribute dividend that is below their earnings or free cash flow. Earnings and free cash flow are not constant, and when earnings fall (as in one of the 3 market fall in Sara’s example), typically, your dividend income may fall. Thus, dividend income is volatile as well.

- If your tenant refuses to pay a higher rent, or worse you cannot find tenants for some months, your rental income on your investment property may not adjust for inflation or be consistent.

Keeping the above in mind, an investor can achieve the same thing as an accumulating fund with a distributing fund, bonds and dividend stocks. He/she can sell some of the units, shares of the bonds, dividend stocks and fund units.

The Main Disadvantage: Over And Underspending

Because the wealth management or financial planning decision is separate from the fund, the investor has to decide on how much to spend.

If he/she spends too much, he/she runs the risk of depleting his/her fund. If he/she spends too little, he/she is short-changing herself.

If we revisit Sara’s example, instead of deciding to spend $35,000 in the first year, she chooses to spend $50,000, this is what will happen:

Given the same situation, spending drastically more would have resulted in Sara depleting her fund 6 years earlier. Her income per year went up from $50,000 to $93,589, but the combination of higher spending and challenging return sequences have resulted in the early depletion.

That said, overspending and under-spending may exist regardless of the kind of investment instruments you use. It is just that retirees tend to be more constrained by what the investment distributes to them.

A sustainable spending plan is one where you manage to integrate different sources of income, accurately assess your expense needs for the next year, and formulate an income that gives you a good chance of not depleting your portfolio yet keep your spending stable.

If you struggle with this, perhaps it is time to find a trusted, yet competent adviser to help you with it. Learn how to identify a good financial adviser here.

For more related resources, check out:

1. What Happened After The Global Financial Crisis

2. Retirewell® Part 5: Investment Philosophy for a Retiree Client

3. The Problem About Dividends

This is an original article written by Kyith Ng, Senior Solutions Specialist at Providend, Singapore’s Fee-only Wealth Advisory Firm.

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current investment portfolio, financial and/or retirement plan, make an appointment with us today.