Long-term severe disability is one of the health risks that may befall a person. Usually, this is most likely to occur when a person is older.

When someone suffers from long-term severe disability, he/she would be so affected that it would be a challenge to perform even one of the following activities of daily living (ADLs):

- Washing. The ability to wash in the bath or shower (including getting into and out of the bath or shower) or do a sponge/ bed bath.

- Dressing. The ability to put on, take off, secure and unfasten all garments and, as appropriate, any braces, artificial limbs or other surgical or medical appliances.

- Feeding. The ability to feed oneself food after it has been prepared and made available.

- Toileting. The ability to use the toilet or manage bowel and bladder function through the use of protective undergarments such as diapers, or surgical appliances if appropriate.

- Walking or Moving Around. The ability to move indoors from room to room on level surfaces.

- Transferring. The ability to move from a bed to an upright chair or wheelchair, and vice versa.

It will have a huge impact on the person’s quality of life and is likely that he/she will require constant assistance for his/her day-to-day activities, either from a caregiver, helper or to move into a nursing facility.

To put things into context, 1 in 2 healthy Singaporeans aged 65 stands a chance of becoming severely disabled in their lifetime and may need long-term care.

So how can we address this risk?

The answer is through long-term care insurance. Long-term care insurance typically provides monthly cash flow for the policyholder to get assistance in the form of a helper or move into a long-term care facility.

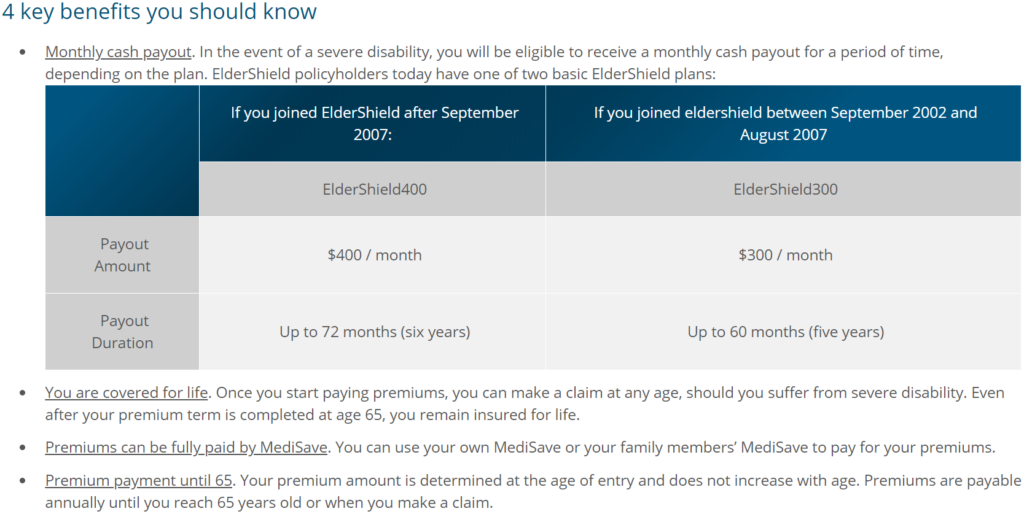

In Singapore, ElderShield was introduced in 2002 as a basic long-term care insurance scheme targeted at severe disability, especially during old age and has been revised once in 2007.

The snippet above is taken from the Ministry of Health (MOH). It explains the current cash flow payout structure when a policyholder is eligible for claims.

As there was a lot of feedback that the current ElderShield is not sufficient to address today’s long-term care needs, a committee was appointed to review the ElderShield insurance scheme in 2016. The committee published their recommendations on how the current ElderShield could be enhanced to better address the needs of disabled Singaporeans, especially during old age.

One of the main considerations when reviewing the current ElderShield was to be more inclusive, affordable and sustainable.

Here are the recommendations:

- The Scheme should be renamed to CareShield Life

- The enhanced scheme should be made universal and include a future cohort of Singapore residents. Cohorts to be enrolled would start from age 30 instead of 40

- Existing cohorts should be encouraged to join the scheme and made optional to them

- Lifetime payouts (versus the 5-6 years currently) should be provided for as long as the claimants remain alive

- Increase the payout from S$400/month to S$600/month

- The payouts for future cohorts should increase over time, as long as the policyholder has not started taking payouts

- Premium payment needs to be spread out over a longer duration (30 to 67 years old) to be sustainable

- The government should allow Medisave to continue to pay for the premiums

- The government should provide means-tested subsidies.

- The government should administer the scheme rather than private insurers (currently for ElderShield)

- The claims and re-assessment process should be simplified

Minister of Health Provides Updates on CareShield Life in Parliament

On 2nd September 2019, Minister of Health in Singapore, Mr. Gan Kim Yong, has provided us with further clarification on the recommendations of the ElderShield Review Committee.

In this article, we will provide you with a summary of Mr. Gan’s elaboration.

Who will be Enrolled in the Scheme when CareShield Life is Launched?

Singaporeans and Permanent Residents who are born after January 1980 will be automatically enrolled in CareShield Life. This auto-enrollment will start in the middle of 2020.

Singaporeans and Permanent Residents who turned 30 years old next time will be automatically enrolled. This will ensure that future generations will be covered under CareShield life, regardless of whether they have pre-existing conditions or pre-existing disability.

New Singaporeans and new Permanent Residents would be automatically enrolled after CareShield Life is established.

Singaporeans who are existing ElderShield policyholders and do not have any pre-existing severe disability, born between 1970 to 1979, would also be auto-enrolled. For this group of ElderShield policyholders, they can choose to opt-out if they wish. The deadline for them to opt-out is 31st December 2023.

What about those that are not automatically enrolled?

The scheme is open to those that were born in 1979 or earlier. They can join the scheme, provided that they do not have a pre-existing severe disability.

The enrollment for those born in 1979 and earlier will start in mid-2021.

The Payout from the CareShield Life Scheme

The key feature of ElderShield and CareShield Life is that the payout will be in cash. This gives the claimant the freedom to decide their preferred care arrangement.

They can choose to remain at home or in a facility and still receive the cash payout.

Safeguards will also be put in place to prevent abuse.

For policyholders who lack the necessary mental capacity to administer, a deputy can be appointed to receive and manage the payouts. If there is no designated deputy, the bill will only allow certain family members to make claims on behalf of these policyholders.

To safeguard against the risk of misuse or fraud, the classes of person who can be an administrator will be a tight list approved by the Minister and generally limited to family members who are caregivers for the policyholders. They can only receive the payouts for a limited period of one year, subject to appeals for an extension, if necessary, to give them time to apply to be appointed as a deputy for the policyholder.

The Government will also allow policyholders or their deputy to nominate healthcare institutions caring for the policyholders, such as nursing homes, as approved payees under the Bill. This will ensure the continuity of their care. These third-party payees will have to first apply the payouts for the policyholder’s care. Not doing so without reasonable excuse is a punishable offence.

These payouts for the policyholders will be protected from creditors with two tight exceptions. The first will allow premium debt to be netted off from the payouts. This is to prevent wilful defaulters from benefiting from the payout without paying the premiums. The second is where there is money owed by the policyholder to a healthcare institution, for instance, a nursing home, arising from the care provided to the policyholder, if the policyholder or deputy has already directed the payouts to this institution. This ensures that healthcare institutions providing care to the policyholder can continue to be adequately resourced to do so.

The Government will provide Transitional and Participating Incentives for Policyholders

To ease the transition for those born after January 1980, there will be transitional subsidies for the first five years from CareShield Life’s commencement. For those born in 1979 or older, they will be given participating incentives to encourage them to participate early in the scheme.

For Seniors who are part of the Pioneer and Merdeka generation, they will receive an additional participation incentive, on top of other incentives to participate in the scheme. The incentives for them can amount up to S$4,000 in participation incentives.

The seniors will be able to use the incentives to net off their premiums payable over a period of 10 years, thereby reducing the number of premiums that they need to pay.

Should these premiums be still unaffordable for the individual, additional help and funding will be provided through further funding from the Government.

A Discretionary Fund to be Setup to help Low Income and Severely Disabled who are Unable to Join CareShield Life

On January 2020, a discretionary government assistance scheme called ElderFund will be implemented. ElderFund seeks to provide assistance to low income and severely disabled Singaporeans who are aged 30 and above.

S$5.1 billion dollars will be set aside for this fund which will be administered by the Ministry of Health. The ElderFund will be used to fund premium subsidies and incentives for the CareShield Life scheme and to provide financial support for severely disabled persons with low Medisave balances and face financial difficulties to meet their long-term care needs.

This fund will provide up to S$250/month in cash to them. This is in addition to government subsidies of up to 80% for long-term care services such as nursing homes and various government disability assistance.

ElderShield and CareShield Insurance fund

The premiums will be means-tested.

For those who need help with their CareShield Life premium payments, there will be means-tested premiums subsidies of up to 30% to help lower- to middle-income Singaporeans with their premiums. However, there may be a small group of wilful defaulters, who refuse to pay their CareShield Life premiums despite having the means to do so, even after reminders have been sent to them. This will place an additional burden on other policyholders. Therefore, a premium recovery framework, similar to MediShield will be put in place. Penalties will also be implemented.

Premiums collected under CareShield Life and ElderShield will flow into the CareShield Life and ElderShield Insurance Fund. The insurance fund will be a self-sustaining fund managed by the CPF.

Severely Disabled Singaporeans to Be able to Withdraw from Their Medisave for Long-Term Care Needs

From mid-2020, Severely disabled Singapore Citizens and Permanent Residents who are at least 30 years old will be able to make cash withdrawals from their own and their spouses’ MediSave Accounts to support their long-term care needs. To ensure that members have sufficient MediSave balances for other medical treatments, the exact amount that can be withdrawn for long-term care will be based on their prevailing MediSave balance, and up to S$200/month for each severely disabled individual.

Government to Take Over ElderShield and CareShield Life from Private Insurers

By mid-2021, the private insurers, who are administering ElderShield will have to transfer the plans to the Government.

This will enable CareShield to be operated on a not-for-profit basis and facilitate a smooth upgrading from ElderShield to CareShield Life for those who choose to do so.

This Bill will dis-apply the Insurance Act to the transfer, as otherwise the ElderShield portfolios cannot be transferred to the Government because the Government is not included in the definition of “Transferee” in the Insurance Act. However, in practice, we will take reference from the requirements MAS has put in place, in governing the transfer to protect policyholders. This includes appointing an independent external auditor to audit the transfer and providing MAS with the full audit reports.

Those who choose not to upgrade to CareShield Life will remain covered by their existing ElderShield policy, with the terms remaining the same. Their existing private insurer will not be transferred too. In addition, they will also benefit from the improvements to the claim process that will be implemented for CareShield Life.

CPF to take Over the Financial Administration of CareShield Life from Private Insurers

CPF will take over the issuance and servicing of the insurance policy. Currently, for ElderShield, this is administered by the private insurer.

This includes:

- Premium collection

- Payment of benefits

- Management of the CareShield Life and ElderShield Insurance Fund

Appointing AIC as the Operational Administrator

Agency of Integrated Care (AIC) will be appointed as the administrator.

AIC will be responsible for the assessment of an individual’s eligibility for the claim by ascertaining his or her disability status. Currently, AIC administers all of MOH’s disability schemes, AIC will be the natural touchpoint for seniors. They are best placed to advise disabled seniors and their caregivers on the various forms of long-term care services and financing schemes they can tap on.

Claims Processes to Be Simplified

Disability assessors, who are designated to verify if the policyholder is eligible for claims, will be doubled to 300.

The Government will be working with healthcare institutions to further expand the types of disability assessments that can be accepted for claims so that policyholders need not undergo another disability assessment if we already have similar data on their disability status.

Senior Minister of State for Health, Edwin Tong, said that MOH has been working with experts to improve the disability assessment framework in order to explicitly recognize the impact of cognitive impairment on physical disability for example.

Under the new assessment framework and revised training curriculum, assessors will be guided more explicitly on the aspects they should take into consideration if policyholders are suspected to have a cognitive impairment, including whether their problem-solving ability and memory impacts their ability to carry out the ADLs.

CPF and AIC will also be allowed to assess the policy holder’s health information. This is to allow relevant parties to inform the policyholder that he /she is eligible for claims (not just for CareShield Life but also other disability schemes as well).

Policyholders can choose to opt-out of this assessment and disclosure. They will, however, lose some convenience- for example, severely disabled individuals will not receive any pro-active outreach to apply for claims, because the Government do not know their disability status, and they may need to go for a separate disability assessment even if they had been assessed for disability recently by a healthcare institution.

Caregivers can also apply to make the claims.

Setting up of CareShield Life Council

The Council will review and make recommendations on policy and scheme parameters to ensure the whole scheme provides protection at an affordable premium for Singaporeans.

This includes:

- Reviewing CareShield Life premiums

- Payout increases beyond 2025

- Review the administration of the schemes

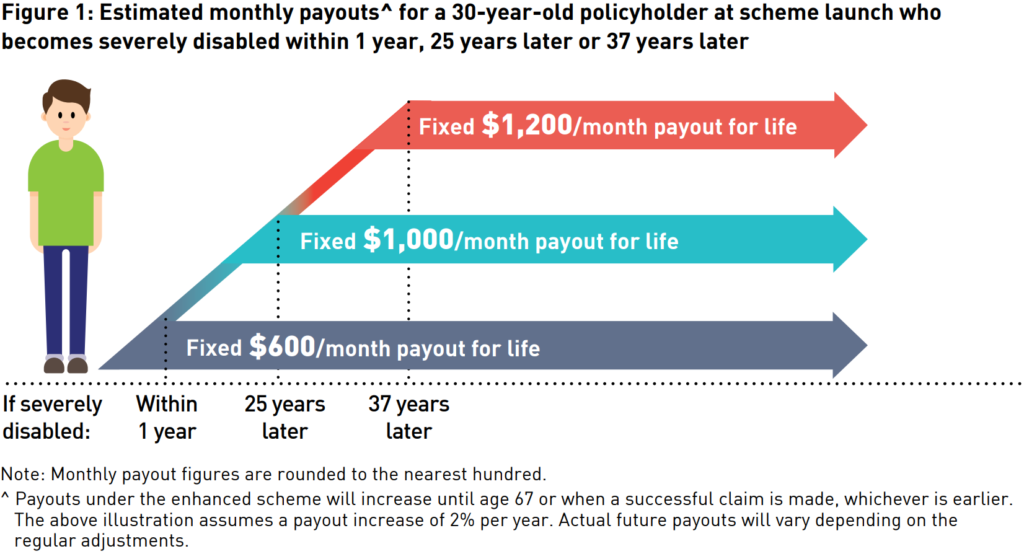

For the first five years of CareShield Life’s implementation until 2025, both premiums and payouts will increase at 2% per year. Adjustments thereafter will be reviewed by the Council.

This Council will be appointed by the time the CareShield Life scheme takes effect.

Here are Some Considerations for You

Mr. Gan has provided greater clarity into how the ElderShield Review Committee’s recommendations can be implemented. There are also clearer timelines set.

From the announcement, we gathered that the future CareShield Life policyholders would mostly be free from existing severe disabilities. CareShield Life, like many insurance systems, is set up based on a risk pooling mechanism. When we are young and less likely to suffer from severe disability, we will pre-fund the “insurance fund” administered by CPF. This is to build up the fund over the years so that we can mitigate our risks in the future when we may more likely need it.

Providend’s Guidance on The Launch Of CareShield Life in 2020

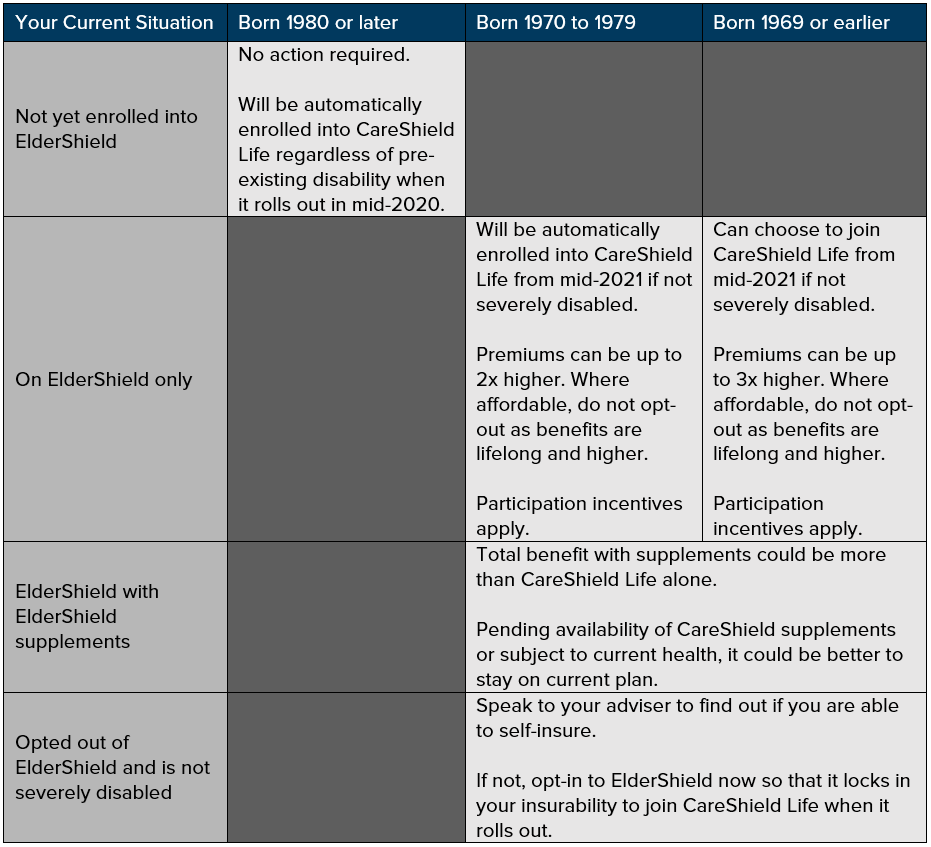

For most of our clients and their children, when CareShield Life is launched in 2020, you will either be:

- Auto-enrolled because you are between 29-39 years old this year

- Auto-enrolled because you were born 1970 to 1979, and currently enrolled in ElderShield.

- Not enrolled but can choose to enrol because you do not have a pre-existing severe disability

If your child or you are 29 to 39 Years old this year

You do not have a decision to make. This is because you will be auto-enrolled when CareShield is implemented in 2020. There is no information revealed by private insurers or the Government regarding how private insurer will supplement CareShield Life. If there are plans brought on to the market or there is more clarity, our advisers will work with you to discuss if these private plans are necessary for you (or your child).

If you were born between 1970 to 1979 and currently enrolled in ElderShield

For those of you who are in this group, you may be most affected by this change when CareShield Life is launched in 2020 This is because you must decide whether you wish to opt-out of CareShield Life. There are a few scenarios:

- You only have ElderShield – In this case, CareShield Life will offer you a higher benefit albeit at a higher premium. Based on benefit, you should switch over to CareShield Life (unless you are unwilling to pay the new premium)

- You have ElderShield with ElderShield Supplement (bought from private insurers)– Currently, ElderShield with ElderShield Supplement should offer you better coverage than CareShield Life alone. So if there is no CareShield Life Supplement being offered by private insurers (we currently do not have any information about this) or you cannot buy it due to pre-existing conditions and your ElderShield Supplement cannot be carried over to supplement CareShield Life, it might be better that you stay on with your current ElderShield and ElderShield Supplement

- IF you don’t have ElderShield and you are not severely disabled – It could be that you have sufficient financial resources to self-insure and that was why you opted out when you were 40 years old. In this case, we encourage you to still have a discussion with your adviser to decide if you really should not join CareShield Life when you can. But if this is not your situation and you will want to join CareShield Life in 2020, you might want to apply to be in ElderShield now while you are still healthy. This will ensure that you can convert to CareShield Life in 2020 without exclusions from any pre-existing conditions.

You were born in 1969 or earlier and you are not severely disabled

For those of you who are in this group, you can only join CareShield Life if you want to, in 2021. There are a few scenarios as well:

- You only have ElderShield – In this case, CareShield Life will offer you a higher benefit albeit at a higher premium. Based on benefit, you may want to opt into CareShield Life (unless you are unwilling to pay the new premium)

- You have ElderShield with ElderShield Supplement (bought from private insurers)– Currently, ElderShield with ElderShield Supplement should offer you better coverage than CareShield Life alone. So if there is no CareShield Life Supplement being offered by private insurers (we currently do not have any information about this) or you cannot buy it due to pre-existing conditions and your ElderShield Supplement cannot be carried over to supplement CareShield Life, it might be better that you stay on with your current ElderShield and ElderShield Supplement and not opt into CareShield Life.

- You don’t have ElderShield and you are not severely disabled – It could be that you have sufficient financial resources to self-insure and that was why you opted out when you were 40 years old. In this case, we encourage you to still have a discussion with your adviser to decide if you really should opt into CareShield Life in 2021. But if this is not your situation and you will want to join CareShield Life in 2021, you might want to apply to be in ElderShield now while you are still healthy. While we have no information on whether you can change to CareShield Life in 2021 without medical underwriting and all pre-existing conditions will be accepted, if it is, it will at least ensure that you can convert to CareShield Life in 2021 without exclusions from any pre-existing conditions.

Whichever your situation, when CareShield Life is launched in 2020/2021, we would encourage you to speak with your adviser to decide what is the best course of action that you should take whether you have or do not have ElderShield now. If you do not have an adviser, reach out to us for a first non-obligatory discussion today. We are always happy to help!

This is an original article written by Kyith Ng, Senior Solutions Specialist at Providend, Singapore’s Fee-only Wealth Advisory Firm.

For more related resources, check out:

1. The Basic Insurance Checklist For Retirees

2. Embrace Longevity, Be Well Prepared to Celebrate Life

3. What You Should Know About CareShield Life (Part II)

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current investment portfolio, financial and/or retirement plan, make an appointment with us today.