When we talk about retirement planning or our proprietary methodology, RetireWell, we always mention the 5 key risks that retirees face, namely 1) Longevity, 2) Inflation, 3) Healthcare, 4) Investing, and 5) Overspending. Many times, seniors have very little control over the first 3 risks, especially longevity.

There is an ancient Chinese poem saying “人生七十古来稀”, meaning that people who can live past 70 years old are rare. This may be true in Singapore 60 years ago, where the average life expectancy was less than age 65. However, it is no longer the case today as many of us are expected to live beyond age 80.

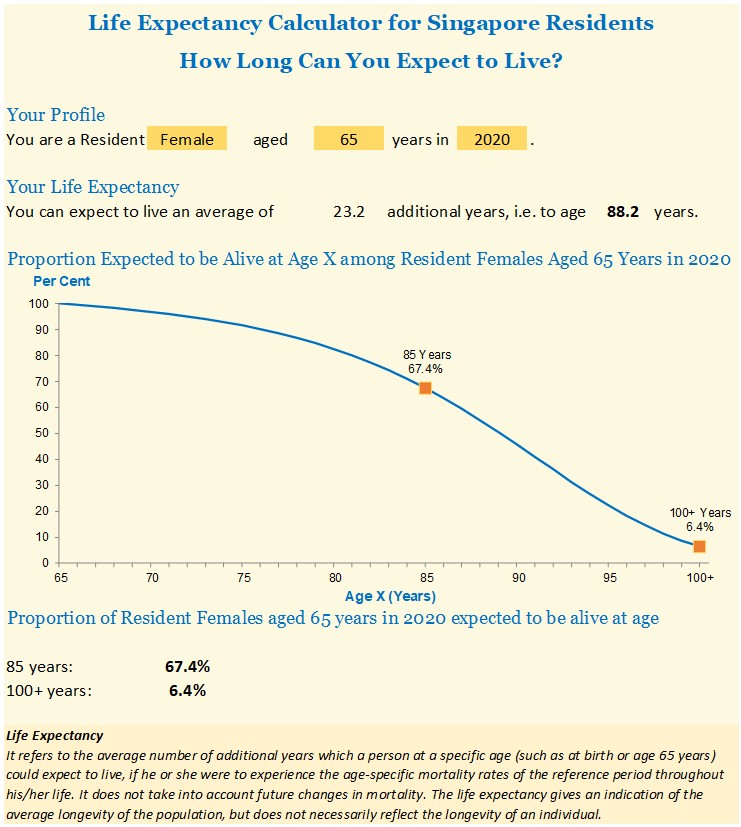

Figure 1 shows the life expectancy of females in Singapore at age 65 in the year 2020. At age 85, about 2 in 3 females of the age 65 cohort are expected to be still alive. In fact, more than 1 in 5 of them are expected to live beyond age 95.

Figure 1: Life expectancy of Singapore Resident Females aged 65 years in 2020. For more information, please refer to the ‘Complete Life Tables for Singapore Resident Population‘ publication.

My mother is at age 82 and my grandmother-in-law is 94 this year. Both are still enjoying their retirement years with relatively good health and it will not be surprising that they can live till 100. In general, their generation receives more support from their children in their retirement. In contrast, most Gen X value their independence more and will want to finance their own retirement.

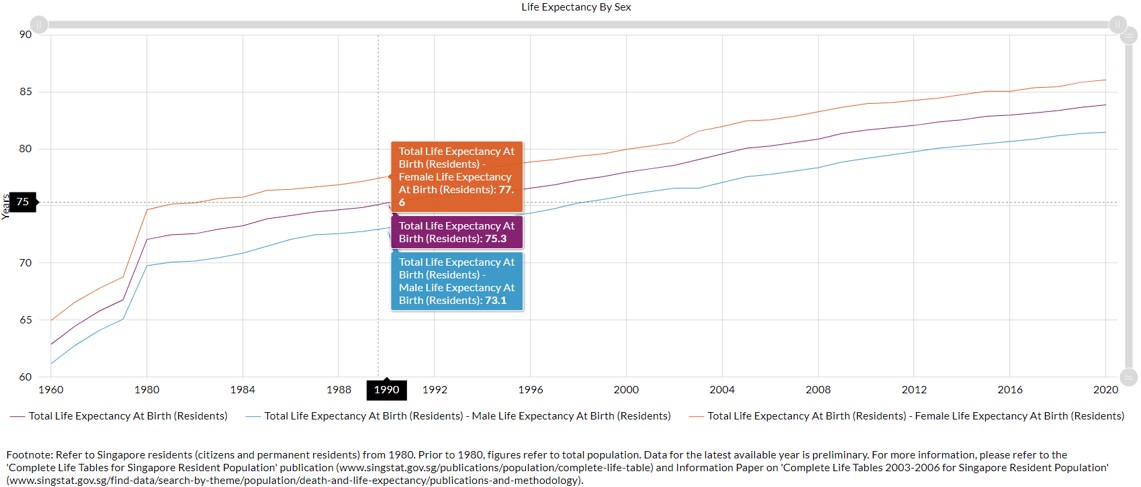

Figure 2: Trend of Singapore life expectancy. Singapore Department of Statistics.

As shown in Figure 2, life expectancy in Singapore has risen from age 75 in 1990 to age 84 today, among the highest in the world. Life expectancy has been increasing at a steady rate of 3 years every decade. Given the average age of first-time parents is about early 30s, this trend will mean that their children will live around 10 years longer.

The report (Singapore Public Sector Outcomes Review), prepared by the Ministry of Finance, also shows that the health-adjusted life expectancy at birth for Singaporeans is also one of the highest in the world. Measuring the number of years, if a person is expected to live in good health, the expectancy is 72.6 for men and 75.8 for women in 2017.

With this awareness that we are living longer than the past generations, we therefore need to act differently to seize the advantages that longer lives can bring. We may need to plan our careers and finances accordingly, also to think about what longevity could offer, and invest more in our longer future. The usual three-stage life of education, career, and then retirement may not be suitable for a retirement age of 60, where we need to finance a 35-year retirement. (Assuming we live till age 95)

We may need to actively invest in skills that will support a longer career, invest our savings over the long term, and build relationships and networks that will support our life purpose. Ultimately, longevity should be about celebrating life and not just about the end of life.

As Singaporean’s life expectancy trends up — it creates more financial risk for retirees, who must ensure their nest eggs last a longer time. Seniors can take measures to reduce longevity risk by working longer, creating a healthcare sinking fund for higher healthcare inflation and delaying CPF LIFE for a higher payout.

Retirement planning can be a daunting task due to its complexity. Giving a generic solution on how much to save for retirement is like asking a doctor to prescribe a medicine that you can take for any illnesses you may have over the next 30 years. It is likely that a pain killer will help, but unable to cure. By having longevity awareness and planning early, there are ways it can be simplified. Below are 3 areas that you can consider.

1. Consider extending your working career, but to be sustainable, even enjoyable, negotiate for greater flexibility like a 4 day work week. Rather than plunging over a retirement “cliff” predetermined by age, consider having a “transition phase” to retirement over the course of several years. You can gradually reduce your working hours while remaining in the workforce. This will be more sustainable and will contribute more to your retirement financial well-being.

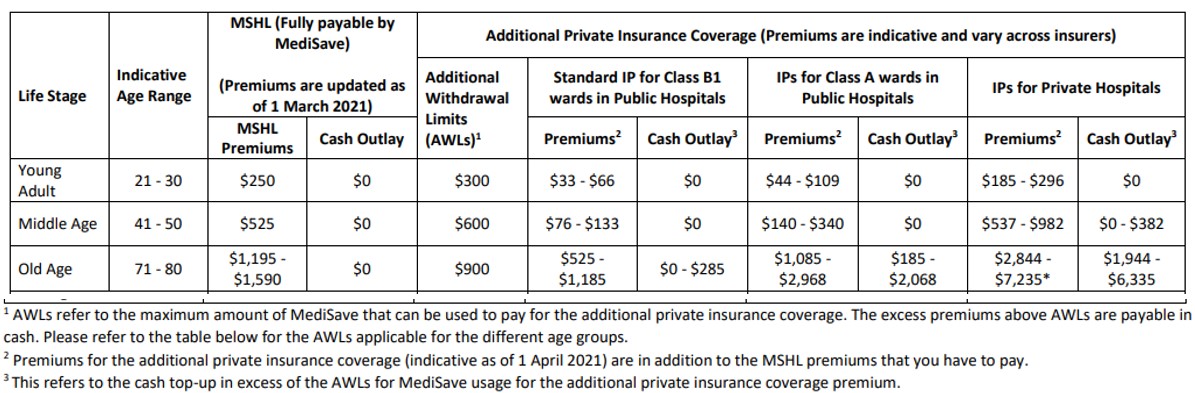

2. To mitigate against large medical bills and long-term care expenses due to severe disability, we are now automatically enrolled in MediShield Life and CareShield Life. Both plans will cover you for life, regardless of your age or health condition. If your healthcare expectation is Class A in public hospitals or private hospitals, you can consider upgrading to an Integrated Shield Plan. Similarly, for CareShield Life, you can increase the monthly payout by purchasing a supplementary plan. However, as premiums rise substantially with age for Hospitalisation and Surgical plan, you may want to maintain a medical sinking fund to offset the increase that is higher than inflation. See Figure 3 below for premiums comparison between the ages of 40s and 70s for the main plan. The rider premium that covers co-insurance and deductible could be up to five times your premiums when you are in your 50s as compared to when you are in your 80s.

Figure 3: Comparison of Premiums between MediShield Life (MSHL) and Integrated Shield Plans (IPs). Ministry of Health.

Figure 3: Comparison of Premiums between MediShield Life (MSHL) and Integrated Shield Plans (IPs). Ministry of Health.

Consider to topping up your MediSave to the Basic Healthcare Sum applicable to you and maintain a separate investment sinking fund for higher healthcare related expenses beyond age 80. As MediSave account gives an interest of 4% p.a., it will at least keep pace with inflation.

3. Make use of your CPF Special Account (SA) and Retirement Account (RA) cash top-up to the Enhanced Retirement Sum (ERS). As the intention is to mitigate longevity risk, you can consider deferring the CPF LIFE Escalating Plan payout by say 3 years till age 68. For each year that you defer, your payouts will increase by up to 7%.

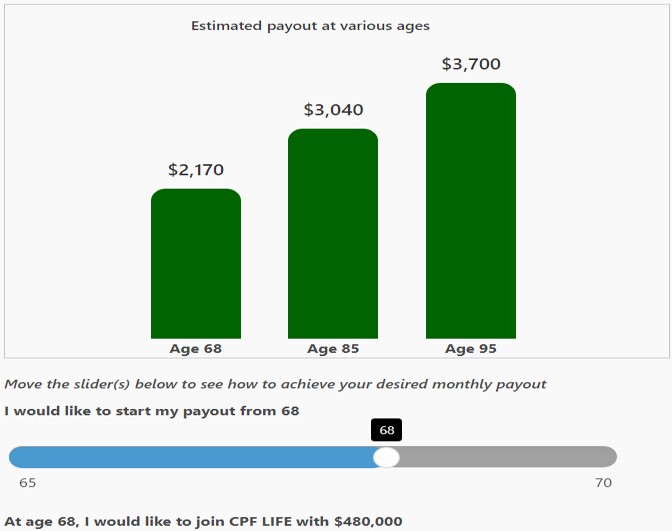

Escalating Plan monthly payout increases by 2% every year for life, to help protect you against rising prices. For a male CPF member aged 55, setting aside ERS of $288,000 (based on 2022 ERS), the payout at age 68 is about $2,170 per month and from age 85, it is about slightly more than $3k per month. See Figure 4 below for the estimated payouts at various ages. This CPF combo (SA/RA/CPF LIFE) is likely a better ‘product’ than insurance retirement income products.

Figure 4: Payout figures are estimates, based on a male member aged 55 setting aside ERS of $288,000 and computed as of 2022. Estimated RA sum at age 68 is $480,000.

Figure 4: Payout figures are estimates, based on a male member aged 55 setting aside ERS of $288,000 and computed as of 2022. Estimated RA sum at age 68 is $480,000.

If you can shield your SA at age 55 and use cash to top up your RA to the Enhanced Retirement Sum, you will then be able to use your SA as a sinking fund to supplement your retirement. The return of both accounts is at least 4% p.a. and your capital is guaranteed by the Singapore government.

Preparing for longevity requires proactive planning and accepting living a longer life positively. Having the awareness will then allow us to have an open mind to explore and follow one’s passions and purpose today, knowing that we can create new possibilities through all stages of life.

This is an original article written by Lee Chee Kian, Senior Client Adviser of Providend, Singapore’s First Fee-Only Wealth Advisory Firm.

For more related resources, check out:

1. Should You Buy Retirement Income Products?

2. Tackling the Complexity of Retirement Spending

3. Hiking and Wealth Management: The Great Adventure

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current estate plan, investment portfolio, financial and/or retirement plan, make an appointment with us today.