Whenever some of my friends meet out for lunch, our topic of conversation will sometimes gravitate to what I am most preoccupied with recently.

I would ponder about that and tell them how most of us underestimate how much our lives can change during our lifetime and how that will affect the way we plan out our life financially.

I had one of the most linear kind of life that you can imagine. I was born to a lower-middle-income family, went to school, did relatively OK, scraped through university, graduated with a degree in IT, then worked in one IT company for 15 years before getting off the conveyor belt, calling quits to join Providend.

Honestly, I think living this standard track of life coloured my philosophy on how people should plan their finances so that they can achieve their life goals.

However, as I hear more life stories from readers and clients of our advisers, I wonder if it is true that most of us live a life that follows the standard script. If life is less linear, then how would it affect the way we efficiently plan our money to enable a richer life?

In this article, I will bring everyone through some of the materials on a less linear life, and some thoughts about its implication to financial planning.

Life is less linear than we think

My interest in trying to understand the right framework to look at how people live their life led me down to Bruce Feiler’s materials.

Bruce wrote a wonderful, relatively new book called Life Is in the Transitions. He believed that the way we frame life may be quite wrong and due to that, we may struggle to navigate life successfully.

Bruce strongly feels that life is less linear partly because of his reflections on his own life. He wrote stories (books, articles and television programs) that were published around the world for 2 decades. Then he spent 1 year as a circus clown and another year travelling with Garth Brooks.

He was then diagnosed with a rare, aggressive bone cancer in his left leg. Frightened and face-to-face with death, he spent a brutal year battling 16 rounds of chemotherapy and a 17-hour surgery to remove his femur and replace it with titanium and move his fibula from his calf to his thigh. The next 2 years were spent on crutches before a year later using a cane.

He nearly went bankrupt as the modest real estate business his father built was destroyed by the Great Recession. That probably affected the future of three generations.

The internet then decimated the world of print he worked in afterwards.

What hit him the hardest recently was the phone call from his mom that his dad, who is suffering from Parkinson’s disease, was trying to kill himself.

Your life might be less dramatic than Bruce’s, but you might experience similar milestones as him if you lived long enough.

Thus, Bruce put together a book about many real-life stories of people recollecting the non-linear paths that they live.

Before we explore why we think most of our life is less linear, we got to define how a linear life looks like.

How does a linear life look like?

In his research, Bruce found that our obsession surrounding time has a big influence on how we live our life. Since the early modern era, we have been very obsessed with time. We started eating when the clock told us to eat, and slept when the clock told us to sleep. Over time, humans began tracking our lives based on time as well.

If we want to give some sort of “shape” to our life, it would either be a “line” or something that represents a very sequential life.

It did not help that we went through an industrial age, human development also became liken to cars or washing machines. At the start, we were not yet done, then we became ready for use, and somewhere down the line, we became obsolete.

In the early 1900s, a plethora of new time periods became popular:

Then Jean Piaget and Sigmund Freud both identified different stages of life before the adolescence stage, with their own studies, conditions, and self-improvement recommendations. However, the general premise remains the same: Everything is in sequential order.

Given this is how the thought-leaders of the past influences the way we view the world, it is not surprising that this is how we look at the world.

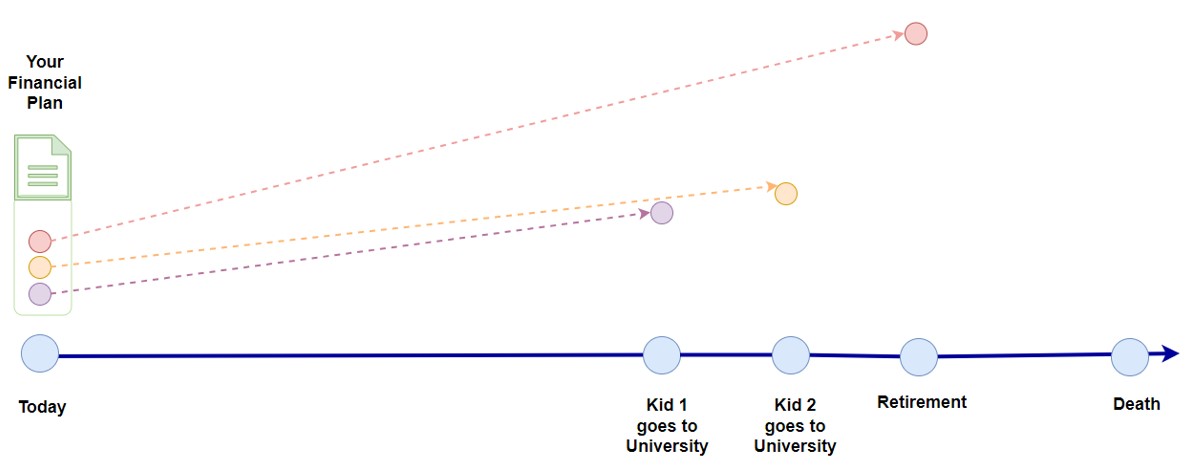

And if our view of the shape of our life is an uninterrupted, sequential straight line, this is how we go about in financial planning as well:

At some point, your spouse and you felt that the responsible thing to do is to find a financial planner to help your family craft a financial plan to get you to where you would like to go, which tends to be rather linear.

And for some of you, you might think at this point that your life does not change much, and the value of the advice is wholly contained in that financial plan crafted at the start.

Your family income only goes up from this point, and your expenses do not change much. Your contribution to your portfolios does not deviate much from what was originally earmarked. Your desired lifestyle projected 30-40 years into the future does not change and so do the tuition and living expenses for your child when they attend university.

We will be disrupted in our lives more than we can remember well

Deep down, we all know that the last paragraph that I wrote sounds rather unbelievable. Even for those who lived a seemingly very sequential life up to this point.

I felt that… our lives are filled with disruptions. Some of these disruptions are rather small such as being fired from a job, you moved on to another a month later. Case closed.

But some of these disruptions would eventually be rather big, both financial-wise and also emotionally. That same retrenchment 15 years from now would be more pivotal because you are much more expensive, there is also higher ageism and technology disruption.

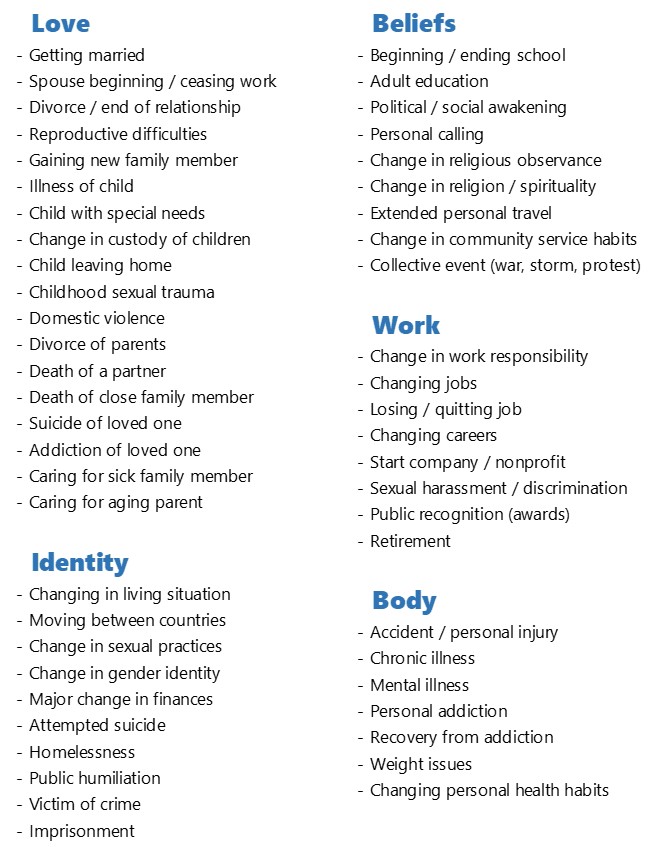

Bruce defines a disruptor to be an event or experience that interrupts the everyday flow of one’s life. This is a better word than some of the less neutral terms such as stressors, crises and problems.

Bruce combed through 225 life stories to generate the following master list of the events that meaningfully redirected people’s lives. He categorised them according to five different storylines that emerged through the conversations: Love, identity, beliefs, work, and body.

How big each of these is a disruptor to you depends on your personal, family situation then and the degree of the disruption. After many of these disruptions, your view of the world might have altered to such a degree that you might change how your family live your life.

And that invalidates the original financial plan.

It is also interesting to note that if you think about it:

- Many got life insurance for the first time after buying their first home, having their first child, or when someone close to them passes away

- People had an idea to do up their will after becoming a couple or being away from their child for a long time

- We decided to do a financial review after changing jobs or after a financial meltdown

- Some decided to do a retirement review after someone close to them passed away

I would say, not all these disruptors will have the power to alter your original plan in a big way.

But there may be enough of these major disruptors that were unnerving and they become rather unsettling.

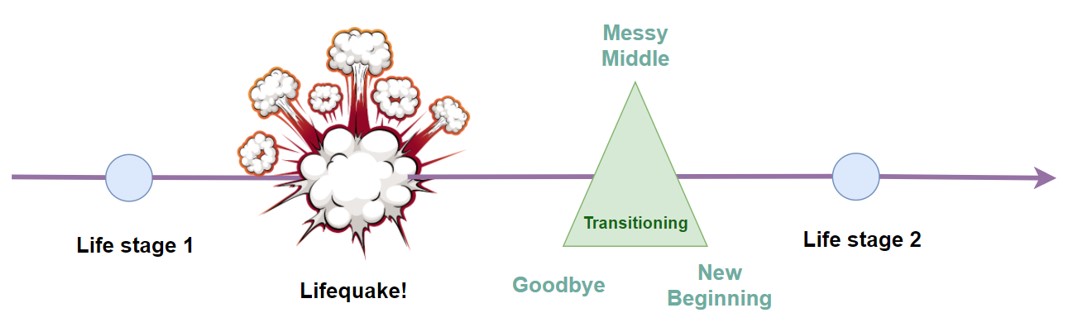

Bruce called these kind of disruptors “Lifequake”. They are major curveballs in life that is enough to eventually take your life to another direction.

Here are some good examples of Lifequakes experienced by famous people:

- Beethoven was 31 and already the virtuoso composer of his first symphony when he learnt that he was going deaf

- Scott Fitzgerald, the bestselling author of The Great Gatsby, was 38 while suffering from marriage woes, financial worries, drinking problems, and tuberculosis when he fled to the mountains of North Carolina

- Mark Felt was 59 when he was passed over to become head of the FBI by Richard Nixon, prompting him to flip and help bring down Nixon as the anonymous mole Deep Throat

At a different time in our lives, we may view our lives in different shapes

When researchers tried hard to capture how the world works, they kept circling back to looking at things in terms of shapes.

In my university lessons on Chaos Theory, we found that within the seemingly chaotic stuff in life, you can find patterns and shapes if you look hard enough. In the midst of the orderly stuff in life, researchers found chaos as well.

This fascination with shapes led Bruce to ask people about what shape best captures their lives and people gave him all sorts of shapes.

Eventually, he classified the shapes identified into 3 different categories:

-

- Shapes that reflect some sort of trajectory. People who characterise their lives as moving through time. The dominant shape is lines.

- Shapes that are spatial in nature. Shapes that are enclosed with borders, outlines, walls such as heart, house, basket, and in Christian’s case: a bowl. The dominant shape is circle.

- Shapes that are some sort of object. This could be a symbol, logo, which represent a guiding principle or commitment in their lives. We can use stars to represent them.

Those who chose lines tend to be more focused on their agency. They are more work and achievement oriented. Those who chose circles are more focused on belonging, making them more relationship oriented. Those who chose stars tend to be more cause focused, saving the world, serving others is something that resonated with them.

Christian Picciolini, an Italian immigrant who used to be the leader of America’s neo-Nazi movement, before suffering from depression and then having a career with IBM, describes the shape of his life:

“A bowl is a place for people to spill their guts into. It’s a place to fill with your thoughts, your demons, your dreams. It’s the place I was looking for as a boy, sitting in my grandparents’ closet. And it’s the place I help provide today, where you hold people in your hands and help them feel like they belong.”

What a person eventually picked that describes his or her life does not mean they value other areas of their lives less. For many of us, we played many roles, and thus it is common that we may have more than one identity.

After Lifequakes, you may be jolted to re-evaluate the weight between agency, belonging and cause.

This means that you go through a period of shapeshifting, from one focus to another:

- Agency -> Cause. Darrel Ross was running an insurance company in Michigan, but he was so shaken by the murder of a friend that he sold his company and started a non-profit to promote affordable housing.

- Agency -> Belonging. After graduating with a double-degree in business and medicine, Jan Egberts eventually became a CEO of a publicly traded pharmaceutical company, but after his estranged wife killed herself following an extended mental illness, he stepped down to care for his adolescent boys.

- Belonging -> Cause. Lisa and Mary, both moms in New York, were so shaken when their children started going to college that they started a Facebook group called Grown and Flown to offer guidance to struggling empty nesters.

- Belonging -> Agency. Peggy Battin was a philosophy graduate student in Southern California who had never been that committed to what she called “husband and children and conventional country club life”. When a great job opens up in Utah, she left her children with her husband and went to pursue her career.

- Cause -> Agency. John Austin spends 25 years in federal law enforcement, eventually becoming an assistant special agent at the Drug Enforcement Administration. A health scare prompted him to give up the precious job security and open a risk management firm.

- Cause -> Belonging. Susan Pierce devoted her life to higher education and was starting her second decade as president of the University of Puget Sound when her husband had two strokes in three months, leading her to reject pleas to stay in her job and instead move to Florida to care for him.

By right, our lives should be rather balanced between agency, belonging and cause. But sometimes, we venture through lives being so focused in some areas. Shapeshifting allows us to restore some balance to our lives. But that is only given if the Lifequake is voluntary.

We live a life of volatility and transitioning between different stages is a regular part of life

A key reason as to why we would want a more linear life is because of the regularity of such a life. Regularity would make a lot of our life and financial planning straightforward.

A non-linear life brings about a mixture of booms, busts, ampersands, exclamation points, monster curveballs, lucky breaks and every other conceivable life detour and twist.

The primary side effect of all this volatility is unease, a low state of anticipation and dread, and a lingering sense of anxiety over whether what is coming next is good or bad.

Bruce defines transitions as a vital period of adjustment, creativity, and rebirth that helps one find meaning after a major life disruption.

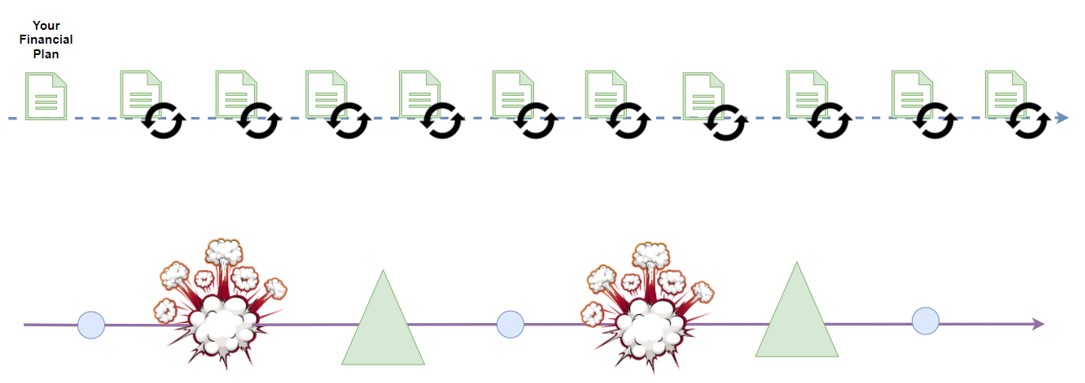

If we were to define how everything adds up, it should look like this:

A change in life stage often happens with a Lifequake. Transitioning should be a phase of accepting internally and externally that you have to leave, doing what is necessary to transit and experiencing that change in your life. This should be rather linear but in reality, transitioning is not linear as well. Some may think they have left and be in a role as part of their new stage of life, but they struggle to accept that they have left the workforce.

Sometimes, leaving your previous life is tough because it has been part of your identity for so long. Thus, we might need to revisit the processes again and again.

In the interviews that Bruce did, the average length of transitions is 4 to 5 years, with some taking longer than 10 years.

Planning your wealth in a non-linear world

Life Is in the Transition is not meant to be a financial self-help book but reflecting upon the stories (There are a lot of personal stories of transitions in the book!), I think it has implications on how wealth management should be implemented. By drawing parallels from the story to what some of my friends went through, it makes me have greater empathy for the paths they had to take.

If a closer reflection of our clients’ lives is one that is filled with life disruptions, then we may need to rethink how we frame wealth planning.

Some areas might become more important given this different view of their world.

1. The importance of seeking acceptance that they live in a non-linear world and this affects how their wealth will be managed

I think the first thing you would have to determine is whether the world is truly linear or not. If you disagree with the experiences people shared in the book, then the traditional way of planning your wealth might still work.

But I think the only constant in life and financial planning is changes, surprises and failures.

If a client or a prospective client feels strongly that this is not how they view the world, then we might struggle to communicate well and add value in the long term.

We will struggle to figure out a good solution if a client insists that despite the range of economic and market scenarios that could happen, the portfolio had to hit X% compounded returns in Y years. They cannot just accept that their lives can have volatility but not accepting that the eventual portfolio value can be similar as well.

2. The original financial plan is less valuable unless constantly updated

How we view your financial plan would have to change. Many prospective clients or clients would still view a large part of the value of their plan to be in THAT original plan. Given the disruptions that could occur in your life, the original financial plan would be obsolete very soon.

And an obsolete financial plan does not have much value.

A financial plan has to be constantly updated but the plan itself is just a conduit for the adviser to provide ease, reduce anxiety while the client moves through a life filled with different disruptions, Lifequakes and transitions.

Specifically, a large part of the recurring value lies in:

- Thinking through and making sound life decisions together. Sometimes, it is helping you validate your original plan so that you don’t make catastrophically bad decisions.

- Reallocating your financial resources as your life changes with sophistication. A plan should reflect how you want to live your life going forward, and not show remnants of what you wish to say goodbye to.

- Tracking your progress towards your goal. In a linear world where everything is predictable, it is a forgone conclusion that doing financially sensible things should get you to where you want to be. But what happens when the contribution from work income to your portfolio gets disrupted on and off? What happens if we lived through a more volatile market, where the inflation regime may look different from the past 10 years? Assessing how on track or off track you becomes very important.

- Motivating and helping you stay focused on your life goal.

- Be your life and financial historian.

- Let you know that you will be alright financially (or not quite alright).

It may be challenging to find a wealth adviser that fits this profile. The challenge locally is that most of the advisers are remunerated for their efforts upfront and not tied to an iterative value structure. The products recommended are meant more for a long-term linear life structure with a high cost of early exits.

3. Financial planning needs to play as important of a role as investment selection to ensure clients reach their life goals despite non-linear financial markets

What I feel would be more challenging to tackle is that in a non-linear financial world, some clients may be unlucky to have to live through a period where the market sequence of returns may not be favourable.

Clients and prospective clients look towards investment strategies, and products to alleviate potential unlucky market returns but in truth, this has proved to be challenging.

There needs to be a framework in financial planning to systematically improve the outcome for the clients so that they can achieve their life goals despite the uncertainty of the financial markets.

I will explore more about this aspect in my upcoming article.

4. Plain-old sound financial advice is important to take away the sting of Lifequakes

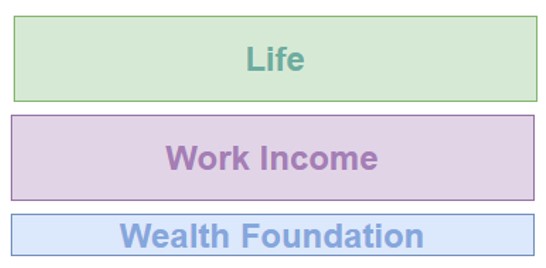

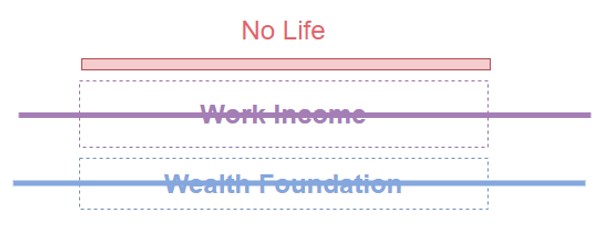

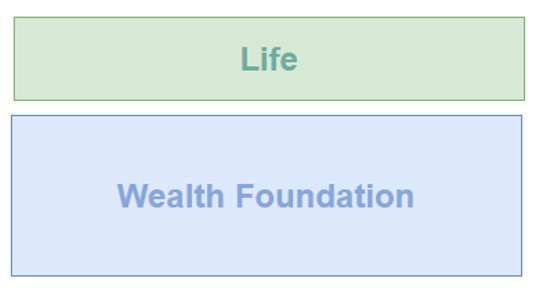

Finally, the important thing to remember about money is that it is an enabler of life.

Many of us stood upon our work income to support our life. The prudent ones will try to build as solid of a wealth foundation as possible.

If you failed to build any wealth foundation, losing your work income, or the prospect of not having your work income, you will have little optionality in life and that would mean no life.

For those who are privileged to earn a good income, and have taken steps to build up your wealth, even though you have not utilised it efficiently, an expanded wealth foundation gives greater breadth to the kind of life you can live. You would be able to tolerate more negative life disruptions or Lifequakes as well.

This is an original article written by Kyith Ng, Senior Solutions Specialist at Providend, Singapore’s first fee-only wealth advisory firm, and Chief Editor of Investment Moats, Singapore’s most well-read financial blog.

For more related resources, check out:

1. On Life Transitions, Legacy and Money

2. To Live the Good Life, Make Life Decision First Before Wealth Decisions

3. The Providend Conversation: Living the Good Life with Tham Why Keen

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current estate plan, investment portfolio, financial and/or retirement plan, make an appointment with us today.