Earlier this year, widespread job cuts were announced across various industries in Singapore. The technology and financial services sectors, in particular, were among the hardest hit. In response, many companies opted to streamline their operations, prioritising efficiency and profitability, often at the cost of jobs.

Unfortunately, two of my clients were among those affected. When they each informed me of their retrenchment, I witnessed two contrasting realities.

One client was well-prepared, with substantial savings and investments that allowed for an early and comfortable retirement. The other client, Dan (fictional name), aged 60, was caught off guard. After more than 15 years of service and having cultivated close relationships with his colleagues and superiors, being laid off was the last thing he expected.

Dan reached out to me shortly after receiving the news. He asked to revisit the retirement plan we had put in place years ago. Together, we set out to re-evaluate his financial roadmap and prepare for what comes next.

1. First things first: Assess Immediate Financial Stability

We began by taking stock of Dan’s current financial position. Our discussion centred around the following:

a) Severance Package:

Is the package sufficient to cover essential, non-negotiable financial obligations such as loan repayments, insurance premiums, income taxes, and family support for the following months in between jobs?

b) Emergency Savings:

Beyond the severance payout, does Dan have adequate emergency funds, in line with the reserves we initially planned?

c) Spouse’s Income:

Can his spouse’s income temporarily support the household’s expenses?

d) Other Income Sources:

Are there alternative income streams—such as rental income or annuity payouts—that can help bridge the gap until CPF LIFE begins at age 65?

2. Reassess Monthly Expenses

We worked together to categorise their household spending, identifying areas where adjustments could be made.

a) Essential Expenses:

Items such as food, utilities, housing, healthcare, transportation, and support for dependants.

b) Discretionary Spending:

Expenditures on non-essentials, including travel, entertainment, online services (e.g. GrabFood), gym memberships, and personal grooming.

3. Revisit the Retirement Plan

The retrenchment introduced new risks and shortened Dan’s investment horizon, necessitating a thorough reassessment of their retirement strategy.

a) Risk Tolerance & Time Horizon:

Given the possibility of early retirement, can Dan afford to maintain riskier investments, or should his portfolio be de-risked?

b) Lifestyle Sustainability:

If Dan stops working now, can they still maintain their desired retirement lifestyle? This includes understanding whether they can continue contributing to their retirement goals or if they need to begin drawing down from their existing portfolio sooner than expected.

4. Evaluate the Options

a) Retire Now:

Given Dan’s current financial standing, is immediate retirement feasible if job prospects remain uncertain?

b) Consider Trade-Offs:

If Dan is unable to secure a role with a comparable income, what are the alternatives? Would he be willing to scale back his lifestyle or accept a lower-paying job to continue working and allow his investments more time to grow?

Replanning with Real Numbers

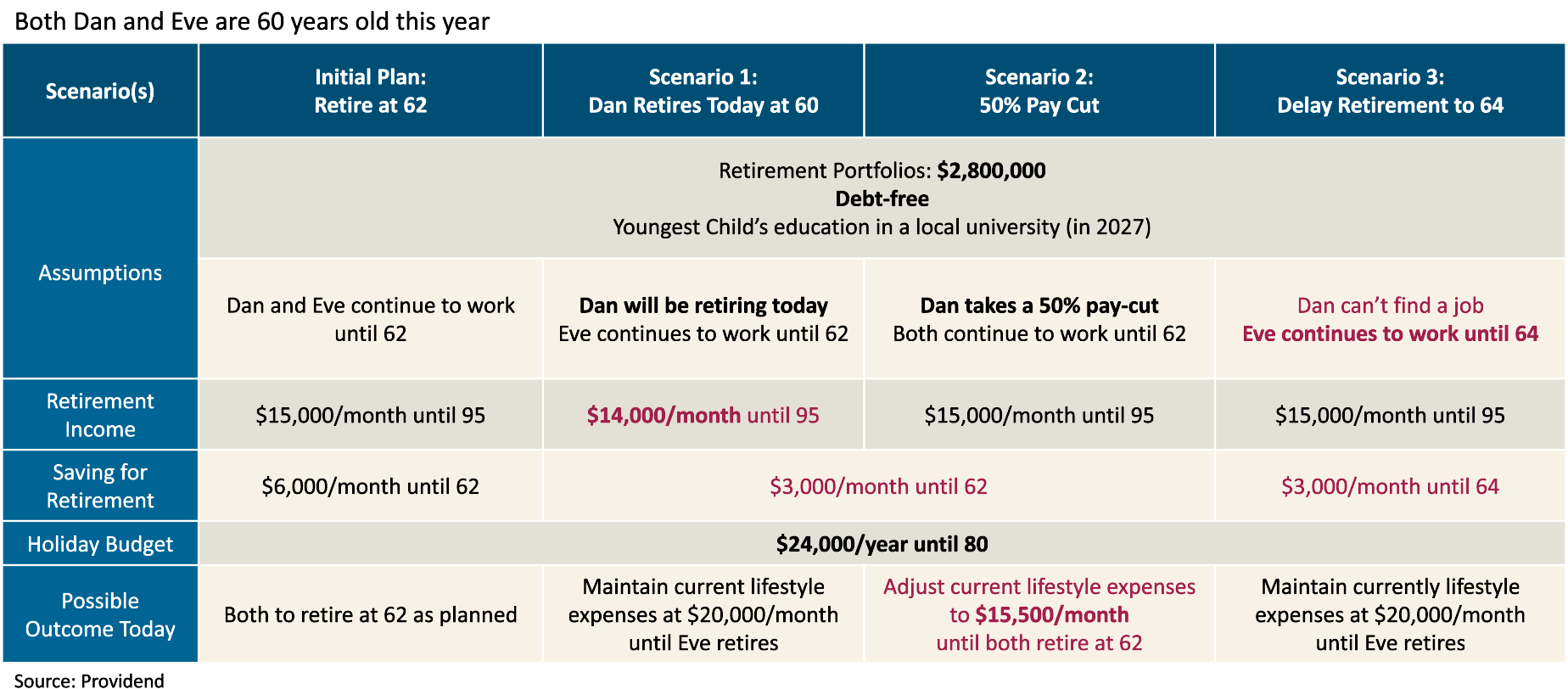

Several years ago, Dan and his wife, Eve (fictional name), also aged 60, had planned to retire at age 62. Their plan was to sustain a monthly lifestyle cost of $15,000 until both turn 95 and enjoy an annual holiday budget of $24,000 until age 80. Based on these goals, they required a capital sum of approximately $2.8 million, which they had started building through investments with Providend and monthly savings of $6,000 until age 62.

Now, with Dan’s employment disrupted, we needed to revisit this plan and assess how these new circumstances affect their retirement ambitions. The goal was to present them with feasible scenarios, highlighting both the options and the necessary trade-offs.

Clarifying Their Priorities

Before diving into the numbers, I asked Dan and Eve to reflect on what mattered most to them, their non-negotiable life goals. They were clear:

- Their youngest child’s education must remain fully funded.

- Their travel plans during early retirement are deeply important to them, representing a long-awaited reward for decades of hard work.

They were open to adjusting other expenses, if necessary, but preserving these two goals remained non-negotiable.

Fortunately, Eve continues to work in a stable job she enjoys and intends to remain employed until at least age 62, providing an important anchor for their financial strategy.

Scenario Planning

Now, let’s take a quick glance at the assumptions and possible outcomes for different scenarios. The table below shows a summary of various scenarios and trade-offs:

The red text in the table highlights changes in scenarios and indicates the trade-offs involved.

Scenario 1: The “Worst-Case” Reality

Dan described the first scenario as the “worst-case” situation—one where he is unable to secure another job and is, in a sense, “forced” into early retirement. In contrast, Eve hopes to continue working until their originally planned retirement age of 62 so that they can retire and travel together.

In this scenario, Dan and Eve would need to adjust their expectations. Instead of the planned retirement income of $15,000 per month, they would need to settle for $14,000 per month. This reduction is primarily due to a shortfall in contributions towards their retirement goal, as Dan would no longer be earning an income to support their savings.

Their current lifestyle requires around $20,000 per month, and without Dan’s salary, they would need to rely more heavily on Eve’s income and existing savings. This decision reflects a balance between maintaining some degree of lifestyle continuity and accepting a more conservative retirement plan.

Scenario 2: Taking a Pay Cut, Staying on Track

Dan then asked, “What if I don’t mind a pay cut? Can we still achieve the $15,000 monthly retirement lifestyle?”

The answer was yes, but with a trade-off.

If Dan accepts a 50% pay cut, they could still potentially achieve their desired retirement income of $15,000 per month. However, this would require them to cut back on current expenses and avoid tapping into their savings prematurely. Drawing on savings now would reduce the funds available later in retirement, especially without the ability to replenish those savings at the same rate.

This scenario highlights the importance of lifestyle adjustments in the short term to preserve long-term financial sustainability.

Scenario 3: Maintaining the Lifestyle, Without Returning to Work

Dan also asked a more challenging question:

“What if I can’t get a job at all, but we still want to maintain our $15,000 monthly lifestyle?”

Here, the answer became more difficult. There are no avoiding trade-offs. I asked them candidly,

“If maintaining that lifestyle means Eve has to delay her retirement, would that be something you’re both comfortable with?”

Without hesitation, Eve shook her head.

“I want to enjoy retirement as early as possible. I want to travel further and longer while I’m still fit. I do love my job but seeing Dan at home while I’m still working hard makes me want to join him as soon as I can.”

This emotional response was powerful. It reminded me that financial decisions are never just about numbers. They are about people, values, and life goals.

Choosing Peace of Mind Over Perfection

At the end of our meeting, Dan and Eve made a clear decision. They chose to revise their retirement income goal from $15,000 to $14,000 per month. They agreed to assume that Dan may not return to the workforce. While this is a conservative approach, it also alleviates the emotional pressure of urgently needing to find a job.

With the pressure lifted, I suggested a different perspective:

“What if this is the time to explore what you’ve always been passionate about? Could a hobby or long-standing interest evolve into something meaningful, and perhaps even income-generating?”

This moment of transition can be seen not just as a setback, but as an opportunity to realign one’s purpose with the next chapter of life.

Summary of Changes and Next Steps for Dan and Eve:

- Revised retirement income goal: $14,000/month (down from $15,000)

- Assumption: Dan will not return to work for now, until he finds a role that he might enjoy working in

- Eve keeps working until 62, with plans to retire and travel together

- Financial plan updated to reflect a slightly lower income and revised contributions

- Explore meaningful pursuits for Dan—possibly hobby-turned-income opportunities

- Focus on sufficiency: Aligning lifestyle choices with values, not just financial goals

This experience reminded me that, as client advisers, our role goes beyond helping clients chase their goals. It’s also about being honest, grounded, and helping them navigate reality with clarity, to be the guide on their life journey—not just helping them fulfil their desires but leading them towards what truly matters most in their lives.

At the heart of our work lies the Philosophy of Sufficiency. It is a conscious choice to enjoy, appreciate, and accept what you have, while giving up the cravings for the things you do not have.

This is an original article written by Joyce Chng, Client Adviser at Providend, the first fee-only wealth advisory firm in Southeast Asia and a leading wealth advisory firm in Asia.

For more related resources, check out:

1. Navigating Retrenchment: How to Regain Control

2. Navigating Financial Challenges Post-Retrenchment

3. How to Know If You Are Financially Secure and Don’t Need a Job Anymore

Being a trusted adviser to our affluent clients for over two decades, we know that our clients need the reliability and sufficiency of investment returns to meet their needs. You can learn more about our purpose-driven approach towards Wealth Management and Investment Management.

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current estate plan, investment portfolio, financial and/or retirement plan, make an appointment with us today.