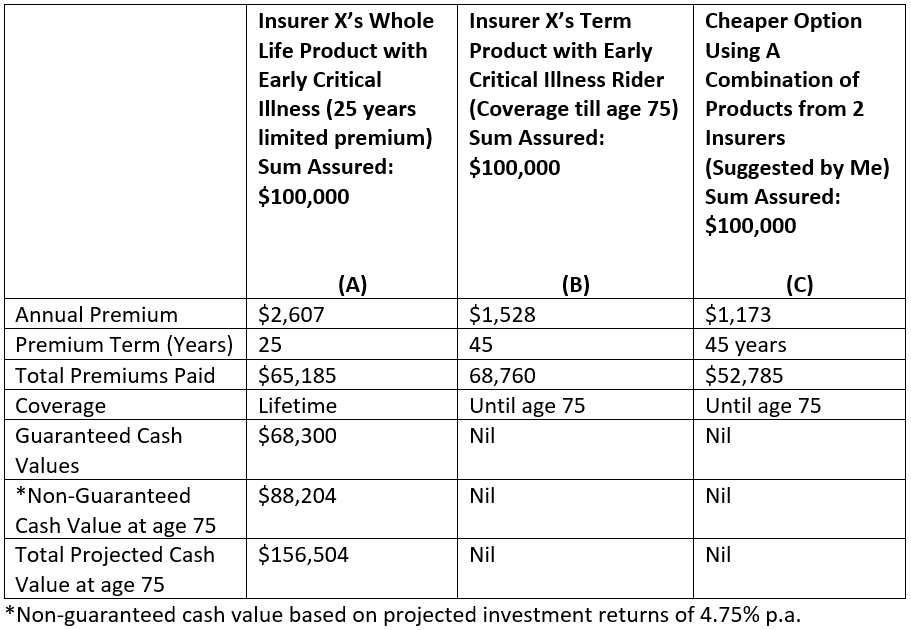

About a month ago, I gave a talk at the Seedly Personal Finance Festival entitled “Insurance – Cutting Out the Fluff” to an audience of almost 1200 young people. In the talk, I shared about how most of our needs can be solved by using low cost term insurances and there is no need to buy costly whole life plans. Almost immediately after the event, someone shared an article on Seedly Facebook page showing why what I shared might not be valid. The writer of the article reasoned that a whole life plan is actually cheaper than a term plan if you consider the cash value accumulated. The table below (column A and B) shows the writer’s analysis:

The writer’s conclusion is that the whole life policy provides better value in the long term with a projected cash value of $156,504 if you didn’t make a claim and live till age 75 and wish to surrender it, whereas for the term plan, you get nothing back at the end of the coverage term. And if one wants insurance coverage at that time at age 75, no insurance companies will insure you.

While the analysis above seems a pretty clever way to show why whole life might be a better choice over term insurance, the thinking is actually not sound and is biased towards the more expensive whole life plan. Let me explain.

- We need to go back to the fundamental reason why we buy insurance plan – it is for protection and not savings or investment. For if getting an investment return (like cash value) is what you want, there are other better instruments to use.

- So, if insurance is for protection, what are we protecting against when we buy a critical illness plan? The basic reason is really to protect against a loss of income due to the contracting of a critical illness. If our reason for buying a critical illness plan is to pay for medical expenses not covered by Integrated Shield Plans, then a whole life plan is suitable and there is no need to compare against the term plan. This analysis is then redundant.

- If we are buying a critical illness plan to protect against income loss, we don’t need whole life cover. We only need it until we no longer have an income to replace. For most, it would be till 65 years old, 70 years old or at most, 75 years old.

- In terms of amount of coverage, we probably need about 3-4 years of our income. So, if we earn say $80,000 p.a., we will need about $320,000 coverage.

In his article, the writer used a more expensive term plan to compare against the whole life plan. But I found a cheaper option by combining term insurances from 2 insurers (column C) and it was whopping 30% savings compared to the term plan he used (column B). So instead of paying $2,607 p.a. for a $100,000 whole life coverage, we only need to pay $1,173 p.a. for a $100,000 term coverage till age 75. But if we want to cover ourselves sufficiently (say up to $320,000 coverage), we will see at once why using a whole life plan becomes really unaffordable.

But what about the cash values we can get at age 75 when we surrender the whole life plan? Wouldn’t that make buying the whole life plan better than term insurance? Yes. But since insurance is for protection, one should focus on getting himself fully covered instead of the possibility of a cash value at age 75 years old. To sacrifice coverage for a future cash value goes against the primary reason why we buy insurance in the first place. That is not wise.

And by the way, we are only getting cash values from a whole life plan because we are giving the insurance company extra premiums and, in this example, an extra $1,434 p.a. (column A – C) for 25 years to invest. If we really want the same return ($156,504) like the whole life plan, we can invest the $1,434 p.a. from the savings of buying the term plan over the next 25 years (the same premium term as the whole life plan in this example), into a portfolio that can give 4.5% p.a. to give you almost the same cash value of the whole life plan at age 75. This can be reasonably achieved by a portfolio with an asset allocation of 60% equities, 40% bonds. But really, we are not buying term so that we can invest the rest to get a return. We buy term because it is the most affordable way to be fully covered.

Since 2003, I have been writing about using term plans instead of expensive whole life plans for protection. For that, I have drawn much flak from advisers. But why am I so conscious about lowering the cost of insurance? This is because we do not plan our insurance needs in isolation from our total financial planning needs. We all have limited financial resources but unlimited needs and wants. As an adviser, I need to ensure that after the insurance needs are taken care of, I leave enough money for the client to plan towards their other areas of needs such as retirement and funding their children’s tertiary education and still leave enough money to live a life now. Because life does not begin at retirement. Life begins today. Financial planning is not just about planning for the future, it is also about making sure we can live a meaningful life now.

The writer, Christopher Tan, is Chief Executive Officer of Providend, a Fee-Only Wealth Advisory Firm. Besides being financially trained, he is also an Associate Certified Coach with the International Coach Federation. The edited version has been published in The Sunday Times on 31st March 2019.

For more related resources, check out:

1. Here’s Why We Advocate Term Life Plan

2. The Basic Insurance Checklist For Retirees

3. The Case For Term Insurance

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current investment portfolio, financial and/or retirement plan, make an appointment with us today.