Executive Summary

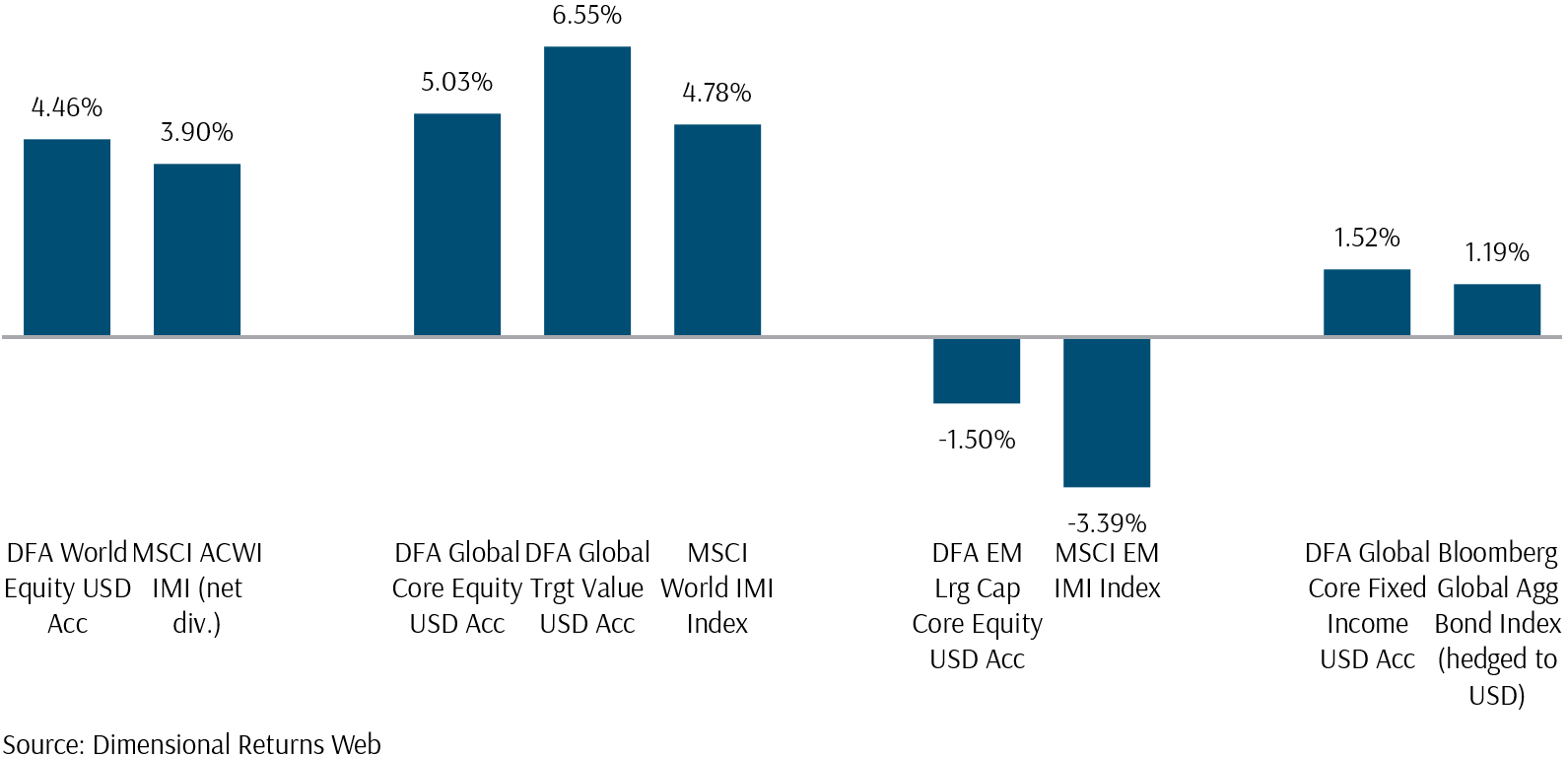

U.S. equities surged, led by small-cap stocks, which outperformed in anticipation of benefits from Trump’s policy priorities, such as tax cuts and deregulation. The Russell 2000 Index, representing small caps, rose 10.97%, compared to a 6.44% gain for the Russell 1000 Index, tracking large-cap stocks. Dimensional Equities, with more focus on smaller caps, like Global Core Equity and Global Targeted Value, outperformed the broader market indexes.

On the flip side, some economies are burdened by the potential impact of Trump’s policies, particularly trade tariffs. European companies, in particular, were hit hard, as their USD-denominated net returns fell in November due to a 2.8% weakening of the euro against the dollar, despite posting positive returns in euro terms.

In Fixed Income, U.S. Treasury yields dropped by 0.11%, benefiting longer-duration bonds, while tightening credit spreads further supported bond markets. The combination of lower Treasury yields, and narrower credit spreads drove bond prices higher. Narrower credit spreads reflect improved investor confidence in corporate issuers and favourable economic conditions. The Global Core Fixed Income, with higher duration and a greater allocation to corporate bonds to capture credit premiums, outperformed the Global Aggregate Bond Index.

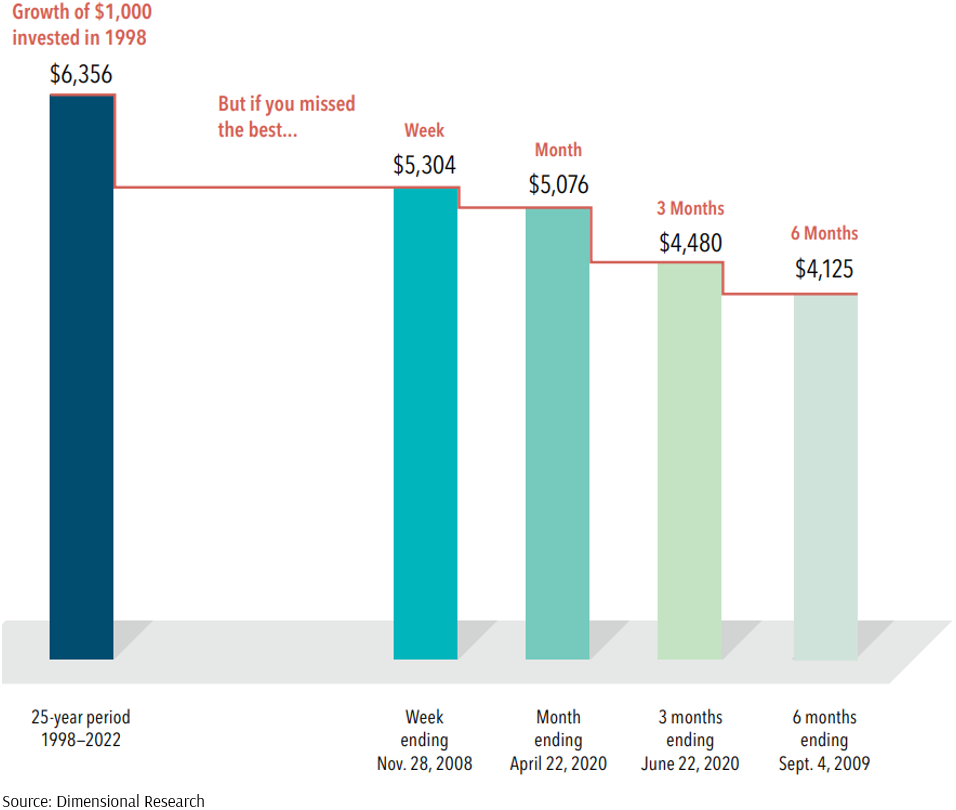

November 2024 highlights the importance of staying invested, as demonstrated by the MSCI World IMI Index’s 4.78% gain and the Dimensional Global Core Equity Fund’s 5.03% rise. Missing key market opportunities can significantly impact long-term wealth, as shown by a hypothetical $1,000 investment in the Russell 3000 Index growing to $6,356 by 2022 but falling to $5,304 by missing its best week and $4,480 by missing its best three months. This emphasises the high cost of market timing and the value of remaining invested.

November Performance

After a disappointing October for both stocks and bonds, November saw a continuation of the equity rally, further boosting the strong double-digit returns for 2024. Fixed Income also rebounded from its October slump.

The S&P 500 Index, which tracks the top 500 U.S. companies, surged by an impressive 5.87%, driven by expectations that Trump’s policy priorities, such as tax cuts and deregulation, would benefit U.S. equities. Similarly, the MSCI World IMI Index, which represents 99% of the investible market capitalisation of developed markets, rose by 4.78%. However, its returns were slightly dampened by negative performance in European and Japanese stocks when measured in U.S. dollars.

In Europe, although the Stoxx Europe 600 Index rose by 1.13%, but its USD counterpart, the Stoxx 600 USD, declined by 1.62%. This was primarily due to a 2.8% drop in the euro against the U.S. dollar, which led to a negative returns for European stocks when measured in USD. Europe’s weak growth outlook, coupled with concerns over the potential of higher tariffs under Trump, further dampened investor sentiment.

In Japan, the situation was different. Japanese stocks, including the Nikkei 225 Index, fell by 2.72%, driven by concerns over Trump’s tariffs, particularly as U.S. is Japan’s largest export partner. However, the decline in Japanese stocks was partially offset by a 1.49% rise in the Japanese yen against the U.S. dollar. Rising inflation prospects fuelled speculation that the Bank of Japan might raise interest rates, strengthening the yen. Despite this, the returns for Japanese stocks in USD terms remained negative.

Emerging Markets also faced a challenging month. The MSCI Emerging Market IMI Index fell by 3.39%, largely due to weak earnings from Chinese tech companies and ongoing tariff concerns. Chinese eCommerce giants such as PDD and Alibaba saw declines of 19.93% and 11.53%, respectively, due to disappointing revenue growth. Meanwhile Baidu’s performance was hindered by a drop in advertising revenue as business confidence waned. Additionally, key semiconductor holdings in the MSCI Emerging Market IMI, including TSMC and Samsung Electronics, declined by 3.30% and 8.45%, respectively, as concerns over U.S. tariffs impacted their performance.

Overall, the MSCI All Country World IMI Index, which tracks 99% of both the investible market capitalisation of the developed and emerging markets, rose by a strong 3.90%, driven primarily by the robust performance of U.S. equities.

In Fixed Income, the Global Aggregate Bond Index rose by 1.19%, recovering from October’s losses. U.S. 10 Year Treasury yields fell from 4.29% to 4.18% in November boosting the prices of longer-duration bonds. Additionally, narrowing credit spreads provided additional support to the bond market. The drop in Treasury yields, combined with tightening of credit spreads, drove bond prices higher. This narrowing of credit spreads signals increased investor confidence in corporate issuers and reflects favourable economic conditions, which further bolstered bond performance.

Exhibit 1 – Market Index Performance: November 2024 (USD)

Dimensional Funds Outperformed Indexes

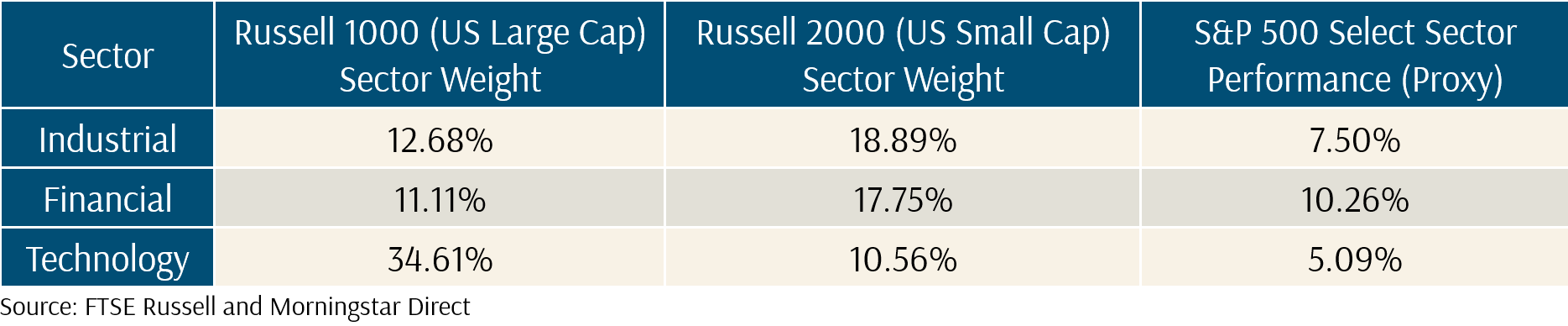

Dimensional Funds outperformed market indexes in both equities and fixed income (Exhibit 3). In equities, U.S. small caps led the rally, boosting the performance of the Global Core Equity and Global Targeted Value funds. These funds exceeded the MSCI World IMI Index by 0.25% and 1.77%, respectively. The strong performance of Dimensional Equity funds can mainly be attributed to their higher allocations in industrials and financials – the top-performing sectors in November. These sectors tend to have a higher concentration of small-cap stocks, in contrast to the technology sector, which is dominated by large-cap stocks.

Exhibit 2 illustrates the sector weightings and November returns for industrials, financials, and technology using U.S. large-cap and small-cap stocks, with the S&P 500 Select Sector as a proxy for returns.

This sector positioning in the Dimensional funds has contributed to their relative outperformance, highlighting the advantage of being more aligned with sectors that hold a higher proportion of small-cap stocks.

Exhibit 2 – Russell 2000 vs 1000 Sector Weights and S&P 500 Select Sector Performance

In Emerging Markets, despite a 1.5% decline, Dimensional’s funds outperformed the MSCI Emerging IMI Index by 1.89%, primarily due to an underweight position in semiconductor stocks such as TSMC and Samsung Electronics. Overall, the World Equity Fund outperformed the MSCI ACWI IMI by 0.56%, driven by the stronger performance of U.S. small caps relative to large cap stocks.

On the Fixed Income front, the Global Core Fixed Income Fund benefitted from falling yields and tightening credit spreads, outperforming the Global Aggregate Bond Index by 0.33%. This outperformance stemmed from its longer duration, which allowed it to capture term premiums as well as its higher allocation to corporate bonds, which benefited from the narrowing credit spreads and helped capture credit premiums.

Exhibit 3 – Dimensional Equities vs Market Indexes (USD)

Capturing the Best Months by Staying Invested

November 2024 serves as a powerful reminder of the value of staying invested. With the MSCI World IMI Index rising 4.78% and the Dimensional Global Core Equity Fund increasing 5.03%, it marks the best month of the year to date for both the developed market index and the Global Core Equity funds. This highlights how quickly markets can deliver significant returns. Missing such opportunities can have a significant impact on long-term wealth creation. As illustrated in Exhibit 4, a hypothetical $1,000 investment in the Russell 3000 Index in 1998 would have grown to $6,356 by the end of 2022. However, missing the index’s best week reduces this to $5,304, and missing the best three months further lowers it to $4,480. These scenarios demonstrate the high cost of market timing and underscore the importance of staying invested to capture the market’s most rewarding days and months.

Exhibit 4 – Russell 3000 Index Total Returns from 1998 – 2022

As We Reach the Year’s End: Staying Informed to Stay Ahead of Market Swings

As we approach the end of the year, it is crucial to stay informed about global developments, especially as political and economic events can create market turbulence. Recent developments in South Korea, France, and China at the start of December highlight the uncertainty that is inherent in the world today.

In South Korea, initial concerns arose following President Yoon’s declaration of martial law, which led to political unrest. However, the situation was swiftly resolved within the same day. While the South Korean Won initially fell sharply against the U.S. dollar, it has since rebounded and stabilised. Although the Kospi Index, which tracks the performance of South Korean large-cap companies, faced some declines, the government quickly reassured markets by announcing its readiness to deploy substantial market stabiliszation funds—worth 10 trillion Won ($7.1 billion) for the stock market and 40 trillion Won for the bond market, if necessary. These measures demonstrate the government’s commitment to supporting the market and preventing further instability, providing reassurance to both local and international investors.

In France, political challenges have raised concerns about growth and rising borrowing costs. However, the French government continues to benefit from strong institutional backing within the Eurozone, which helps ensure its fiscal and economic stability. While political developments may introduce temporary uncertainty, France’s position within the broader European framework mitigates these risks, helping to maintain investor confidence despite internal challenges.

On a more positive note, China’s economic outlook has shown encouraging signs of recovery. Recent PMI readings above 50 for two consecutive months suggest that the manufacturing sector may be stabilising, indicating that the deflationary trend could slow or even reverse. This data offers hope for both the Chinese economy and global growth, signalling a potential rebound in a key global economy.

So far, despite some geopolitical instability, markets have remained relatively calm as we approach the end of 2024. While we hope for a smooth conclusion to the year, we recognise that challenges may arise in 2025. However, rest assured that our Client Advisers will continue to be by your side, guiding you through any turbulence, helping you maintain a steady hand, remain invested, and be prepared for whatever the future holds.

For more related resources, check out:

1. Active Investing That Adds Value to the Client

2. Providend’s Money Wisdom Podcast S2E8: Our Pursuit of the Perfect Portfolio for Long-Term Investors

3. Long Term Risk Premiums and Expected Returns: Evidence From US and China

Download our Investment eBook titled “A More Reliable Way to Get Enough Investment Returns: Even During Times of Market Uncertainty” here.

With a minefield of financial misinformation out there, we promise to be a safe pair of hands and a second pair of eyes to help you avoid costly financial mistakes. Learn more about our investment philosophy here.

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current estate plan, investment portfolio, financial and/or retirement plan, make an appointment with us today.