Executive Summary

In September 2024, the stock market marked its first positive month in five years, largely due to a 50-basis point rate cut from the Federal Reserve (Fed) and stimulus initiatives from China. This resulted in substantial gains for major indices, especially the MSCI World IMI and MSCI Emerging Market IMI.

In Q3 2024, Dimensional funds, which tilt towards value and small-cap stocks in developed markets, significantly outperformed broader indices, with the Dimensional Global Targeted Value fund posting an impressive 8.2% increase. This strong performance indicates a shift in investor sentiment towards undervalued stocks amid concerns over high valuations in large-cap growth equities. Additionally, the Dimensional Global Core Equity Fund demonstrated a positive premium over the risk-free rate in Q3, underscoring the importance of remaining invested during periods of market volatility.

September Performance

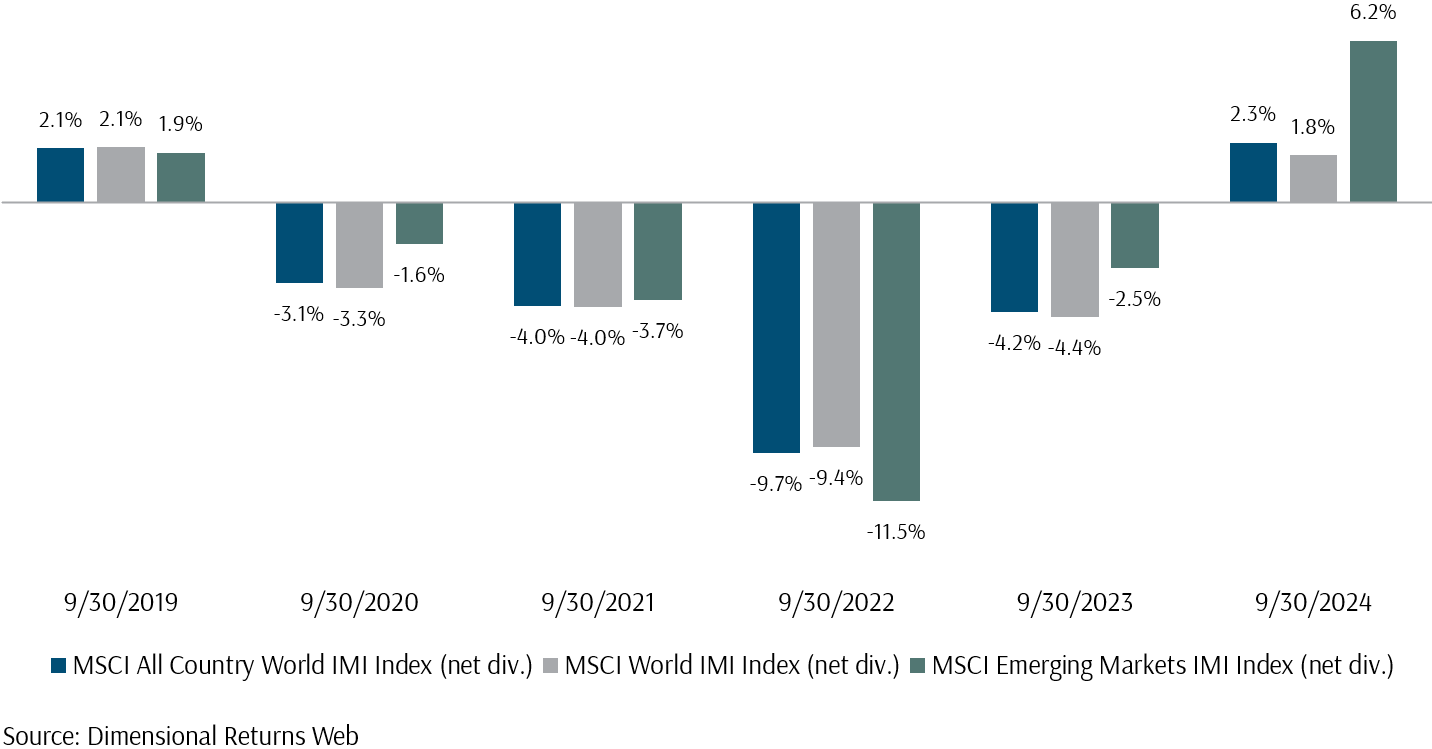

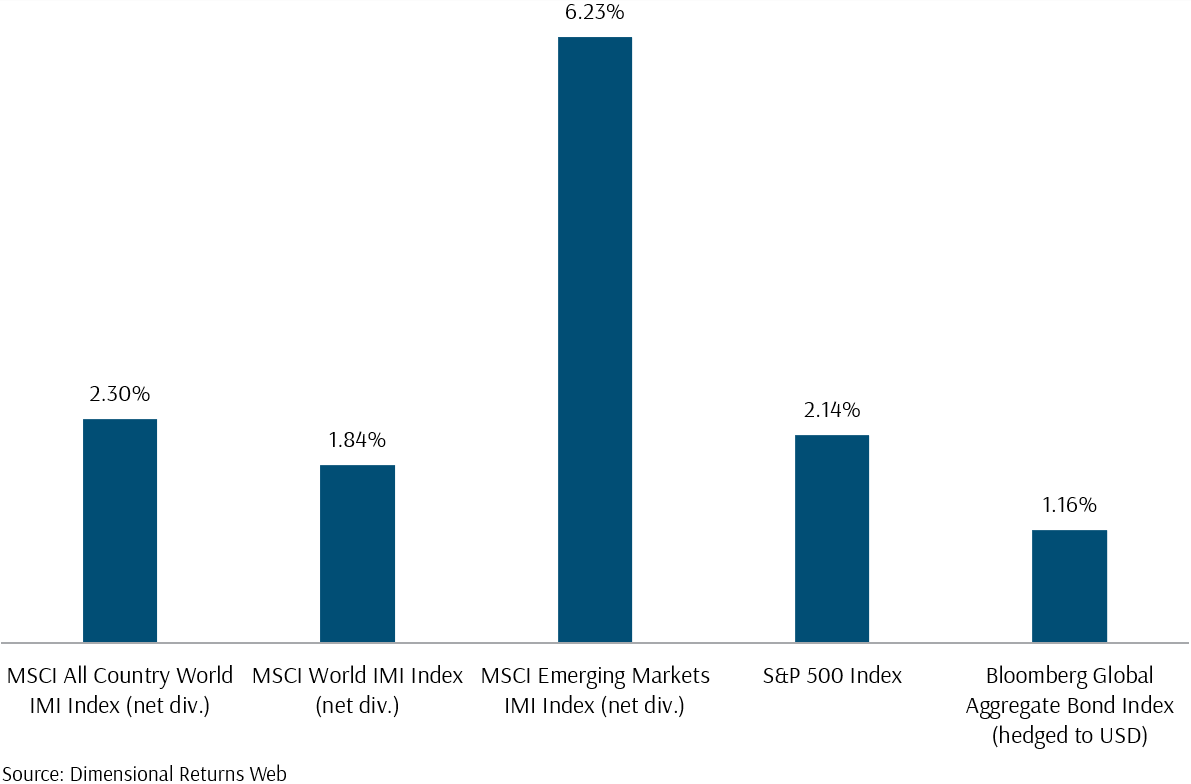

In September, the stock market saw another robust rally, marking its first positive performance for the month since 2019 (Exhibit 1). As shown in Exhibit 2, the MSCI All Country World IMI, the MSCI World IMI, the MSCI Emerging Market IMI, and the S&P 500 gained 2.3%, 1.8%, 6.2%, and 2.1%, respectively. Meanwhile, the Bloomberg Global Aggregate Bond Index increased by 1.16% as yields declined.

After more than a year without a rate hike, the Federal Reserve (Fed) implemented its first rate cut in September, reducing rates by 50 basis points. This move came on the heels of softer-than-expected inflation data for August, with the Personal Consumption Expenditures Price Index rising 2.2% year-over-year, falling short of the economists’ projection of 2.7%[1]. The lower inflation data fuelled a stock market rally. In addition to the Fed’s significant rate cut, Emerging Market equities received a boost from China’s announcement of a stimulus package aimed at spurring GDP growth and supporting its stock market. The Hang Seng Index climbed 17.5% in September, while the four largest Chinese stocks in the MSCI Emerging Market IMI—Tencent Holdings, Alibaba Group, Meituan, and PDD Holdings—jumped by 16.4%, 35.05%, 45.52%, and 40.27%, respectively.

Exhibit 1 – 2019 to 2024 September Equity Market Index Performance

Exhibit 2 – Market Index Performance: September 2024 (USD)

Q3 Summary: Staying Invested in Equities Through Volatility: Your Patience is Paying Off

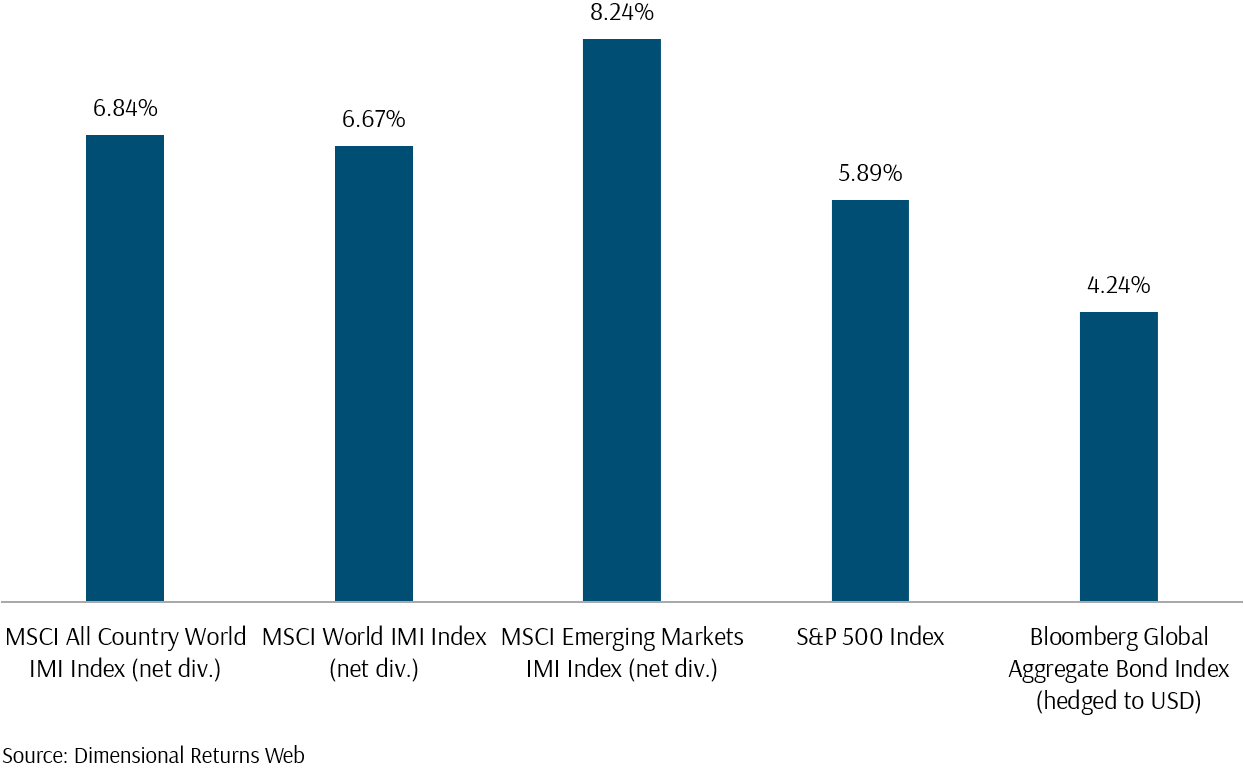

As we move into Q4, let us review the market’s performance so far. As illustrated in Exhibit 3, Q3 saw strong gains across the board, with the MSCI All Country World IMI, the MSCI World IMI, the MSCI Emerging Market IMI, and the S&P 500 rising by around 6.8%, 6.7%, 8.2%, and 5.9%, respectively. The Bloomberg Global Aggregate Bond Index also posted a solid gain of 4.24% as yields fell. Despite a rocky start in August—driven by a sharp drop in stocks following Japan’s central bank rate hike and the subsequent carry trade unwind—markets bounced back as softer inflation and jobs data fuelled expectations of a rate cut.

In retrospect, the Fed’s unexpected 50 basis points rate cut contributed significantly to equity returns in developed markets. Emerging market equities surged in the final stretch of Q3, propelled by news of China’s stimulus measures, leading to their outperformance compared to developed market counterparts. Investors who weathered this period of uncertainty have been rewarded, as both equity and fixed income markets posted impressive gains.

Exhibit 3 – Market Index Performance: Q3 2024 (USD)

Dimensional Developed Markets Funds Performance in Q3 2024: Value and Small-Cap in Developed Markets Shines

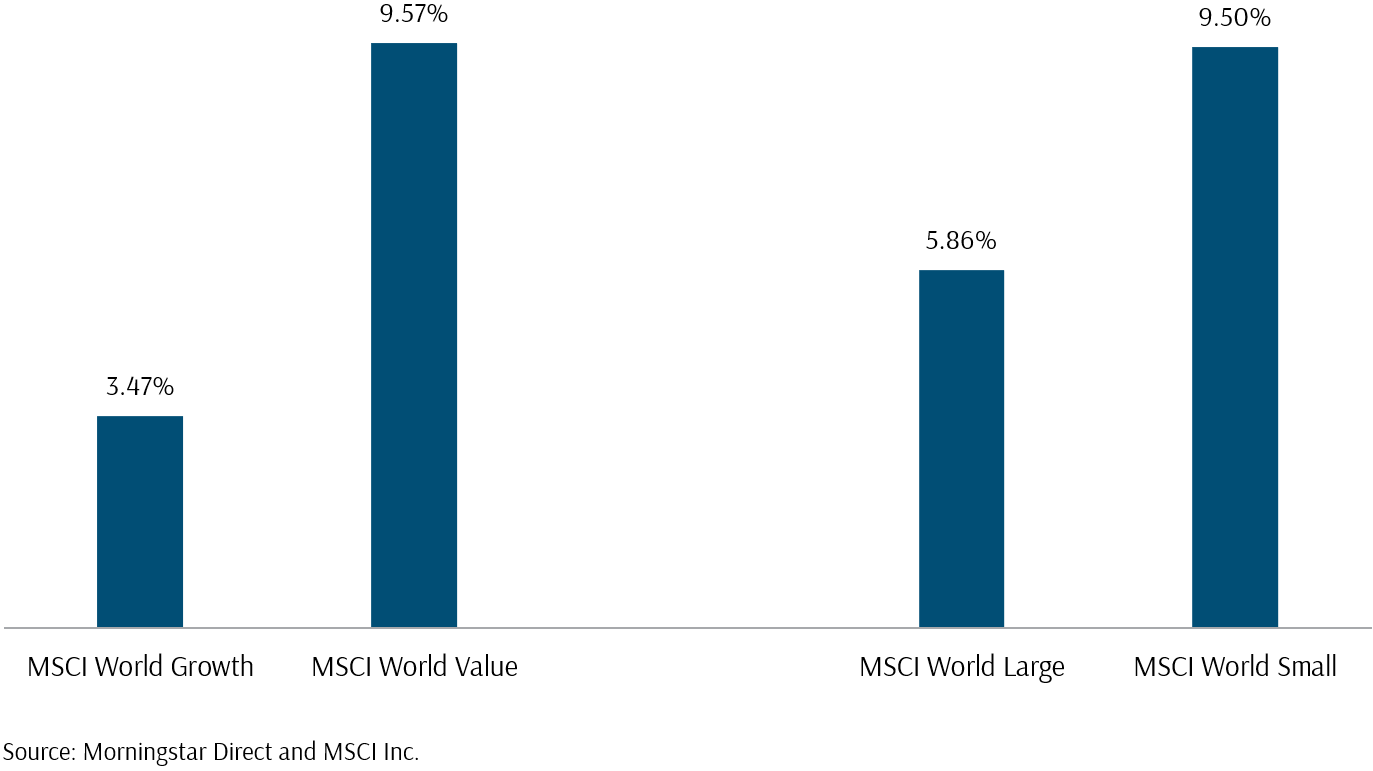

As shown in Exhibit 4[2], value and small developed market stocks rose by around 9.6% and 9.5%, respectively. In contrast, growth and large developed market stocks gained only around 3.5% and 5.9%. The breadth[3] equity returns show signs of widening, following concerns over the high valuations of large-cap growth stocks in developed markets. This shift in sentiment may have led investors to seek opportunities in undervalued small-cap and value stocks, driving their outperformance as they are perceived to offer better returns at more attractive valuations.

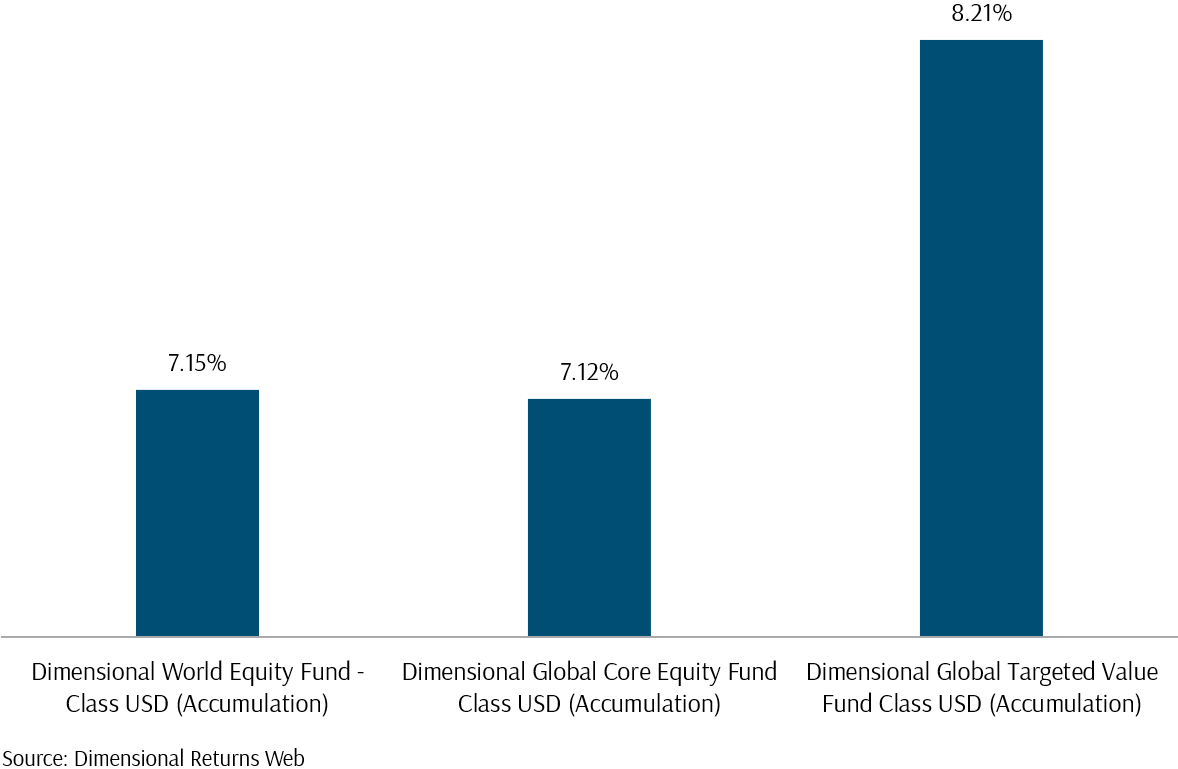

Consequently, Dimensional developed market equities, which are tilted towards value and small-cap stocks, outperformed the broader indexes (Exhibit 5). The Dimensional World Equity, the Global Core Equity and the Global Targeted Value rose by around 7.2%, 7.1% and 8.2% respectively. The Global Targeted Value did notably better due to its higher tilt towards value and small-cap companies, as compared to the Global Equity funds.

Exhibit 4 – Developed Market Indexes Growth vs Value and Large vs Small in Q3 (USD)

Exhibit 5 – Dimensional Developed Market Equity Funds Performance: Q3 2024 (USD)

Q3 Premium over Risk-Free Rate Returns: The Market Offers a Premium for Taking Risks

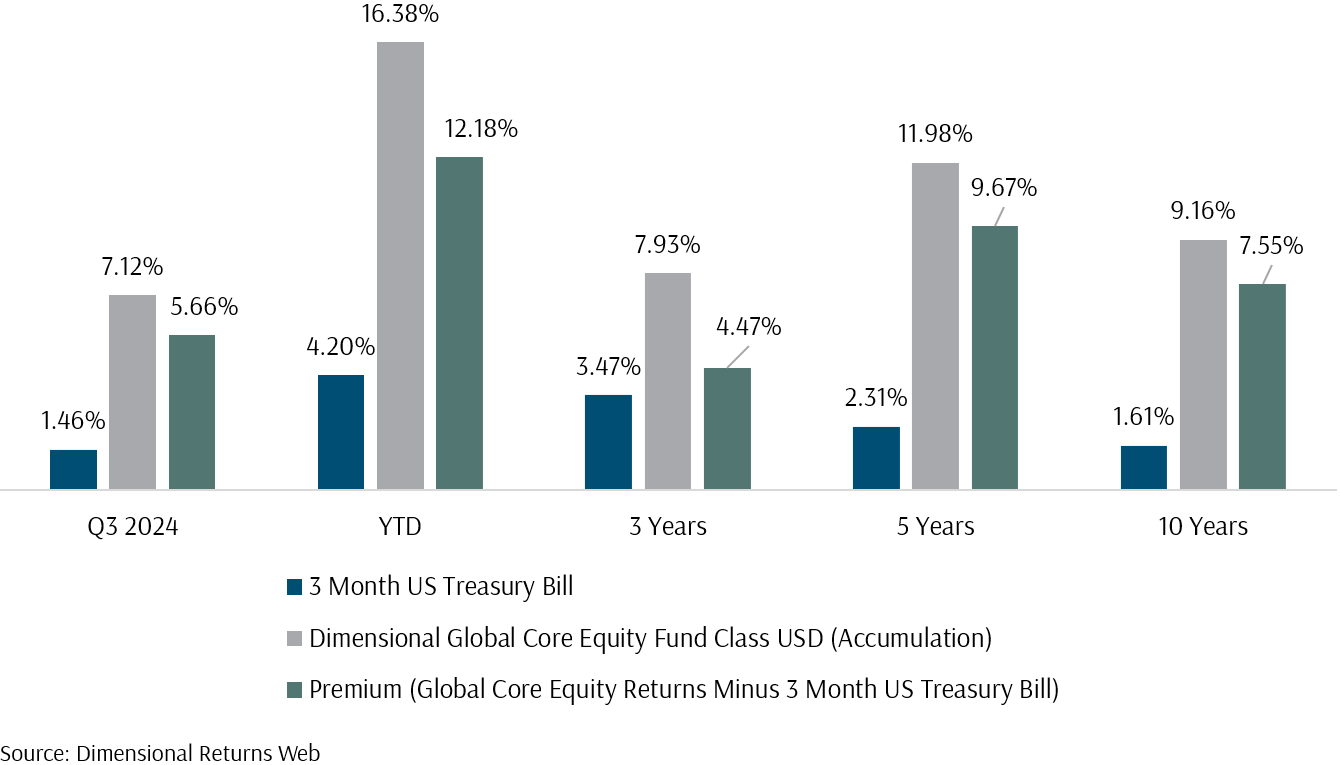

Exhibit 6[4] compares the returns of a 3-month US Treasury Bill index against the Dimensional Global Core Equity Funds in Q3, YTD, 3-years, 5-years and 10-years respectively.

Across the 10-year period of investing in the Global Core Equity while the premium over the risk-free rate is positive, this comes at a price of high volatility. For example, in 2022, Global Core Equity dropped by around 15.2%, while the 3-Month US Treasury Bill gained around 1.1%, resulting in an outperformance of around 16.3% for the Treasury Bill. Despite this, the 3-year premium, which includes 2022’s performance, is only around 7% lower than the year-to-date premium. Nonetheless, patient investors who remained invested in the Global Core Equity fund enjoyed an annualised outperformance of around 7.6% over the 3-Month Treasury Bill.

This highlights a key takeaway: staying invested in the market, even during volatile periods, can ultimately reward investors with higher returns over the long term. In the next section, we will explore scenario analysis comparing indexes from 2001-2010 and 2010-2020, further illustrating why staying invested and diversified is critical for capturing long-term gains across different market conditions

Exhibit 6 – Dimensional Global Core Equity vs Risk-Free Rate (as of 30 September 2024)

Key Insight from Scenario Analysis: Stay Invested and Diversified

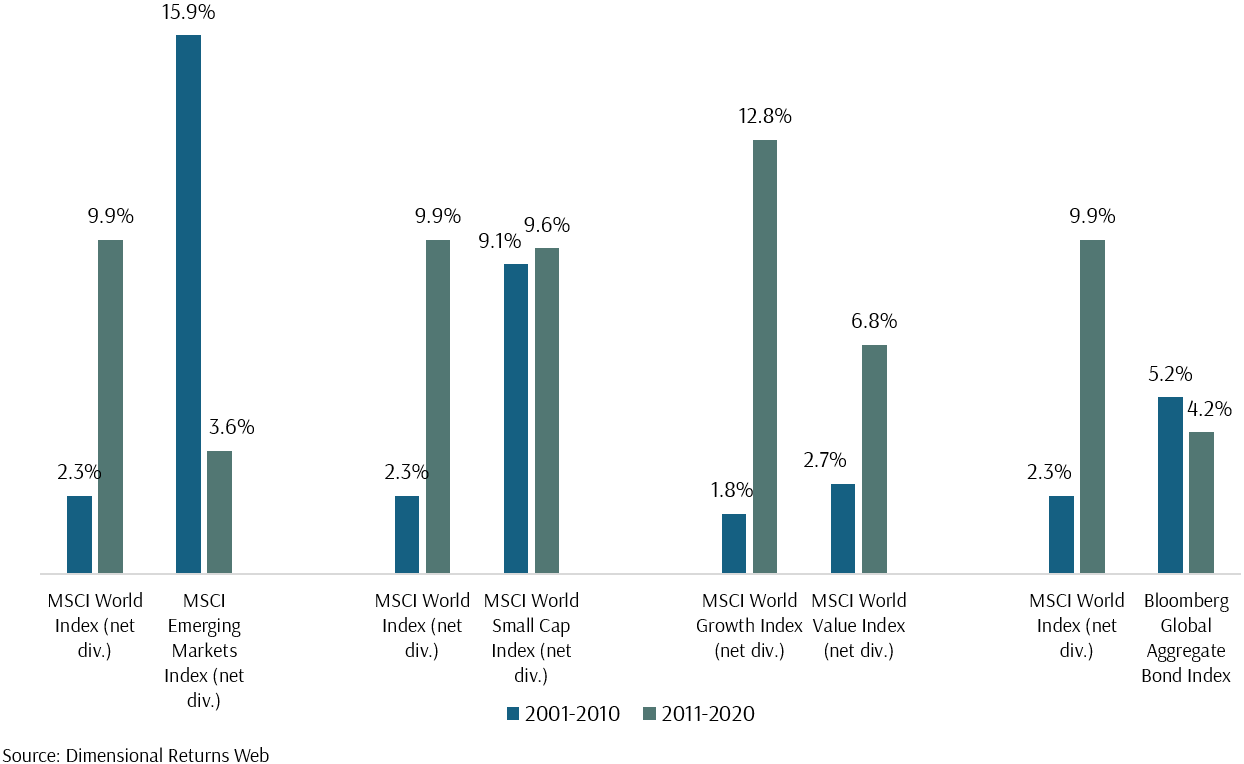

Exhibit 7 – Indexes Performance 2001-2010 vs 2010-2020

Exhibit 7 shows comparisons of indexes between 2001-2010 and 2010-2020. The main goal of this exhibit is to show why it is pointless to make investment decisions based on past performance. Instead, believing in empirical evidence, staying invested and diversified helps you to capture market returns over time:

- MSCI World Index vs. MSCI Emerging Markets Index (2001-2010 vs. 2011-2020): Investors who invested in the MSCI World Index during 2001-2010 would have experienced a modest return of 2.3%. If seeing the impressive 15.9% return of the MSCI Emerging Markets Index over the same period, the investor switched to emerging markets for 2011-2020, they would have been disappointed as the MSCI Emerging Markets Index delivered only 3.6%, underperforming the MSCI World Index, which achieved 9.9% in the 2011-2020 period.

- MSCI World Small Cap Index (2001-2010 vs. 2011-2020): Investors who saw the strong performance of the MSCI World Small Cap Index (9.1%) in 2001-2010 might have expected similar returns going forward. However, if they switched their investments away after that period, they would have missed the continued high performance of 9.6% during 2011-2020, which remained almost as strong as the previous decade.

- MSCI World Growth Index vs. MSCI World Value Index (2001-2010 vs. 2011-2020): Investors who stayed invested in the MSCI World Growth Index during the 2001-2010 period would have been disappointed by its low 1.8% return. If they switched to the MSCI World Value Index, which showed better returns (6.8%) during 2001-2010, they would have missed the surge in growth stocks, which delivered a much stronger return of 12.8% from 2011-2020, far outpacing the value index’s 2.7%.

- Bloomberg Global Aggregate Bond Index (2001-2010 vs. 2011-2020): Investors invested in the MSCI World Index experienced a modest 2.3% return from 2001 to 2010, while the Bloomberg Global Aggregate Bond Index delivered a stronger 5.2% gain during the same period. However, had they shifted to the bond index for the following decade, they would have faced a lower return of 4.2%, missing out on the MSCI World Index’s impressive 9.9% return from 2011 to 2020.

Investors who chased returns by making decisions based on past performance and frequently switching their investments during these periods often missed out on more favourable opportunities, highlighting the importance of staying invested and diversified across different market conditions.

Every premium comes at a price, and that price is risk. Whether you aim to capture market, value, or small-cap premiums, taking on risk is an inherent part of the process. While recent years may not have delivered the same level of returns for some factors like value or small-cap companies, the empirical evidence shows that, over time, these premiums do materialise. The volatility and underperformance seen in shorter periods are the costs investors pay for the potential of higher long-term returns. It is crucial to remain patient and remember that these premiums tend to reward investors who stay invested through different market cycles.

At Providend, we remain committed to helping our clients capture market premiums—whether through market, small-cap, value, term, or credit exposures—by ensuring they stay invested and diversified. While the nature of market behaviour is often unpredictable and tested over time, one fundamental truth persists: the market rewards patience. By maintaining a long-term perspective and holding steadfast through volatility, investors are positioned to benefit from the potential premiums that arise across market cycles.

If you would like to explore your wealth goals further, our Client Advisers are here to work closely with you every step of the way.

As always, if you have any concerns about the market or your investments, please don’t hesitate to reach out to your Client Adviser.

– Footnotes –

[1] Economist at Bank of America expect a 0.15% increase in the PCE, which would translate to a 2.7% reading on an annual basis.

[2] The MSCI World Growth, Value, Large, and Small Indexes are used as proxies for comparing the respective factors. Please note that these indexes serve as estimates and should not be considered an exact representation of actual returns, as fees are not included.

[3] Breadth in equity markets refers to the extent to which the movement of an index or a broader market is driven by many stocks rather than just a few. When market breadth is strong, it indicates that many stocks across different sectors and sizes are participating in the rally, suggesting a more balanced and sustainable rise. In contrast, narrow breadth means that only a handful of stocks, often large-cap companies, are driving the overall market performance, which can signal vulnerability if those few stocks falter. A widening breadth, as noted in the context of small and value stocks outperforming large growth stocks, suggests that more sectors and stock types are contributing to returns, which may be a healthier indicator for long-term market performance.

[4] The comparison between the 3-month US Treasury risk-free rate and the performance of the unit trust, the Dimensional Global Core Equity Funds, presented is for illustrative purposes only and should not be considered a precise reflection of actual returns. The 3-month US Treasury rate is used as a proxy for a risk-free rate, while unit trust returns are subject to market risks and fluctuations. This comparison does not take into account the following factors that may significantly impact the actual returns of unit trusts:

- Management fees, performance fees, and trustee fees charged by the fund managers.

- Sales charges, redemption fees, or trailer fees typically associated with unit trust transactions.

- Any applicable custodian fees for holding the units.

- Currency exchange rates or other foreign investment risks that may apply to international equity or bond funds.

- Taxation implications, such as withholding tax on dividends or capital gains, depending on the jurisdiction.

Past performance is not indicative of future results, and the estimation provided does not guarantee similar performance or outcomes in the future. Investors should consider these variables before making any investment decisions.

For more related resources, check out:

1. Active Investing That Adds Value to the Client

2. Why Rolling Returns Could Increase Your Investment Conviction

3. Why a Robust Estimate of Future Returns Is Important for Investment Planning

Download our Investment eBook titled “A More Reliable Way to Get Enough Investment Returns: Even During Times of Market Uncertainty” here.

With a minefield of financial misinformation out there, we promise to be a safe pair of hands and a second pair of eyes to help you avoid costly financial mistakes. Learn more about our investment philosophy here.

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current estate plan, investment portfolio, financial and/or retirement plan, make an appointment with us today.