As the 2024 US presidential election approaches, investors are grappling with uncertainty surrounding the potential outcomes and their implications for the financial markets. The political landscape is rapidly evolving, and the election outcome could significantly influence economic policies, market performance, and investor sentiment.

This article will explore three key risks associated with the election and outline three possible market scenarios that could unfold based on the election results. By understanding these factors, investors can better prepare their portfolios for the potential volatility ahead.

Our focus will be on highlighting the following three risks and its possible implications in three different election outcomes.

1. Inflationary risks

2. High interest rates and the US debt issue

3. US commercial real estate risks

We will explore how the upcoming US election might influence these risks. By examining these risks, this discussion will showcase the importance of staying invested in the market even amidst uncertainty.

1. Inflationary Risks

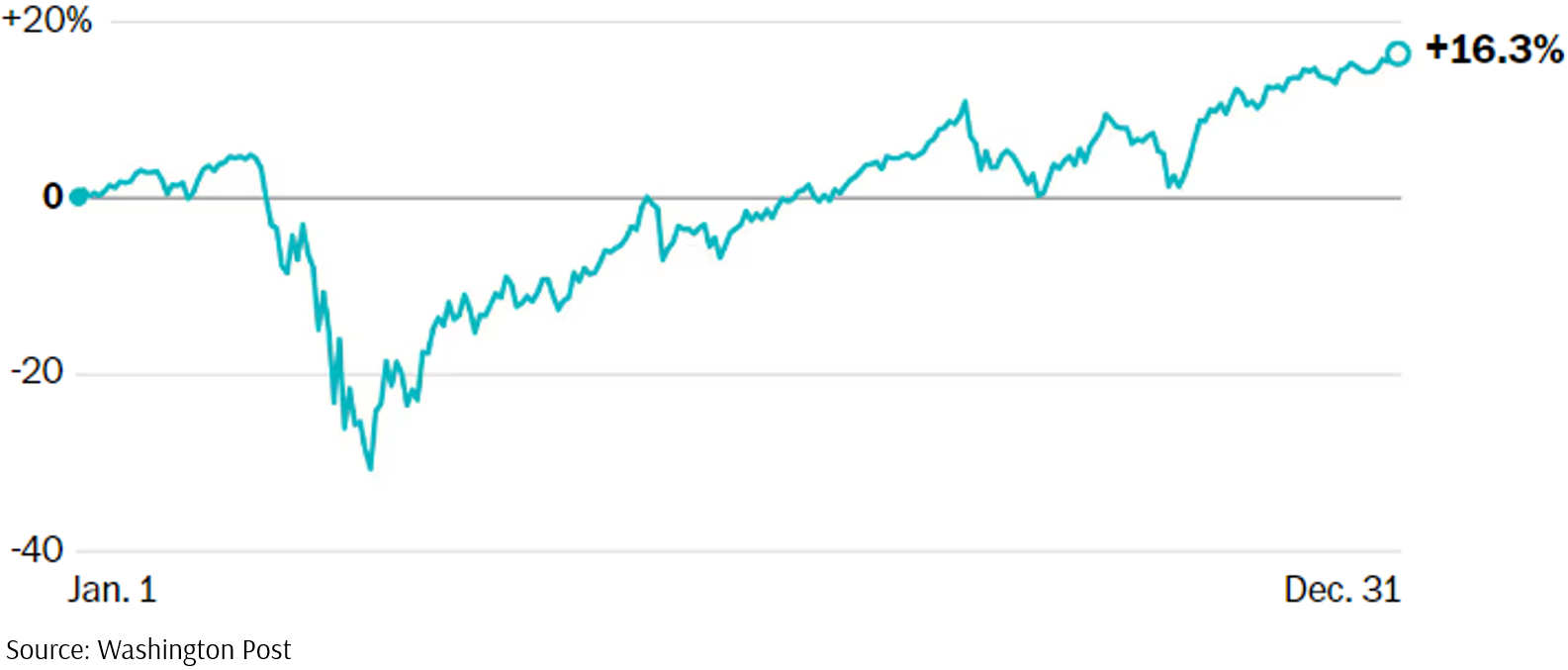

In March 2020, as the extent of the COVID-19 pandemic became clear, the stock market experienced a sharp decline, with stocks tumbling 34%. However, this downturn turned out to be the shortest in US history. Since the market bottomed on 23 March 2020, the S&P 500 has risen 68%, ending the year up 16.3% (Exhibit 1).

Exhibit 1 – The S&P 500 Performance in 2020

This rebound reflects market optimism about 2021 but also highlights the disconnect between the stock market’s success and the broader economic headlines. Several factors contributed to this recovery:

- Monetary Policy: Quantitative easing and near-zero interest rates boosted the stock market.

- Fiscal Stimulus: Significant fiscal stimulus towards US households increased consumption spending.

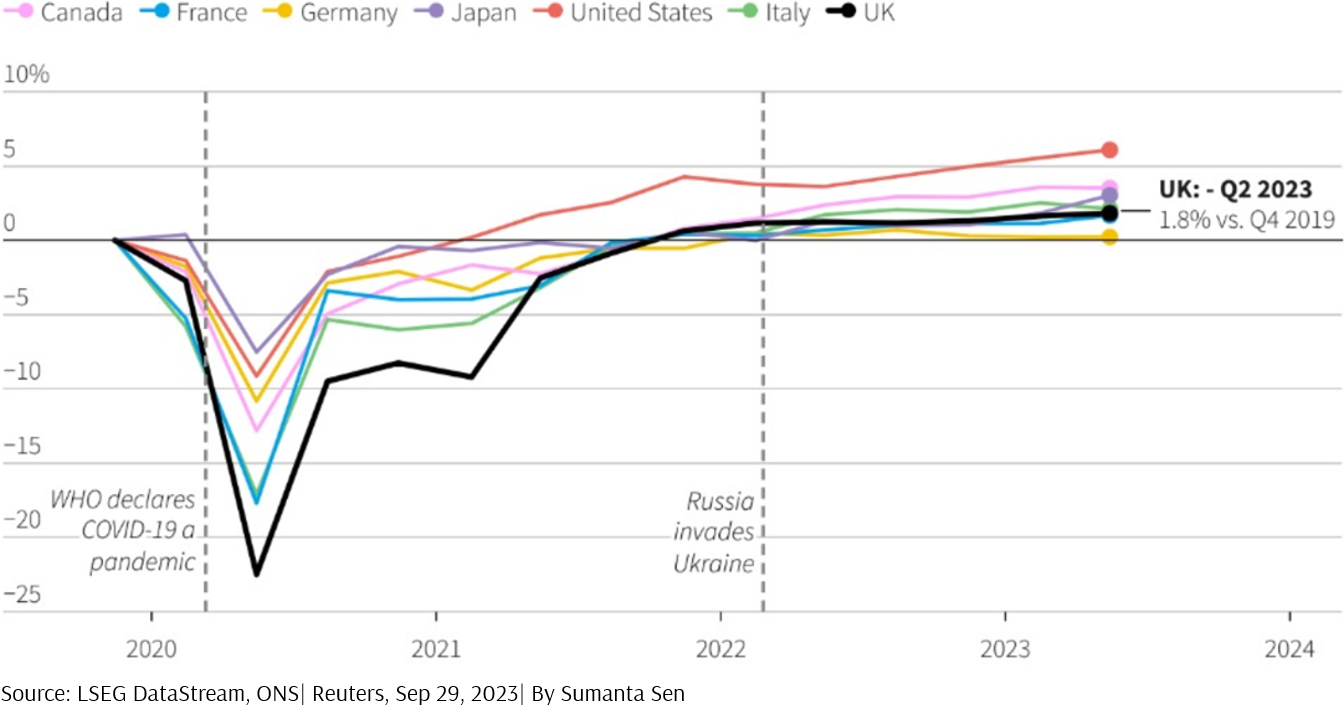

According to FactSet[1], 79% of the S&P 500 Index’s companies reported positive earnings surprises, marking the third highest percentage since FactSet began tracking this metric in 2008. The US economy remained strong going into 2021, rebounding most robustly among the Group of Seven (G7) countries (Exhibit 2).

Exhibit 2 – G7 Real GDP (Q4 2019 – Q2 2023)

However, inflation began to rise. From February 2021 to December 2021, headline inflation increased from 1.7% to 7%, primarily due to supply chain disruptions and strong demand. By June 2022, the Consumer Price Index (CPI) showed inflation peaking at 9.1%, exacerbated by the Russian invasion of Ukraine in March 2022, which impacted wheat, fertiliser, and energy prices.

Implications of Rising Inflation

Apart from potentially leading to rising interest rates, inflation can negatively impact equities in several ways:

1. Erosion of Purchasing Power: Inflation reduces the real value of money, decreasing consumer spending, and hurting company revenues and profitability.

2. Increased Costs: Higher costs for raw materials, labour, and other inputs can squeeze profit margins if companies cannot pass these costs onto consumers.

3. Reduced Investment Returns: Inflation can diminish real investment returns, making equities less attractive and reducing capital inflows in the stock market.

Although inflation has fallen to 3%[2] since its peak in June 2022, risks remain due to ongoing geopolitical tensions, such as the Ukraine-Russia war and the Israel-Palestine conflict. If these conflicts escalate, they could lead to higher shipping costs and import prices, exacerbating inflation and putting downward pressure on US equities.

Conclusion for Inflationary Risks

The persistent inflation from late 2020 to mid-2022, driven by factors like geopolitical tensions and supply chain disruptions, has significantly impacted the US equity markets. Inflation reduces purchasing power and increases costs for businesses, squeezing profit margins and potentially diminishing real investment returns. Although inflation has somewhat subsided, ongoing geopolitical conflicts pose a risk of renewed inflationary pressures, which could adversely affect consumer spending and corporate profitability, ultimately impacting equity markets.

In the next section, we will continue our recap by examining the impact of rising US interest rates on equities and the implications for the already high US debt.

2. High Interest Rates and the US Debt Issue

In response to the rising inflation rates, the US central bank hiked interest rates the most aggressively in 35 years[3] at the start of 2022. The rising interest rates spooked investors, who worried that higher borrowing costs could impact indebted companies, along with higher input costs caused by the ongoing Ukraine and Russia war and a shortage of labour supply.

Additionally, the US government estimated that its debt ceiling would be reached by the end of 2022. The closer the government gets to the debt ceiling, the more uncertainty it creates in the market. Investors tend to become cautious, leading to increased volatility.

A selloff ensues with the S&P 500 Index going down 4% on a single day on 13 September 2022, the worst day of the year. By the end of 2022, the S&P 500 Index had fallen 19% in 2022, marking one of the 10 worst-performing years for the stock index in at least 90 years.

Implication of the High Interest Rates and the US Debt Issue

The interplay between high interest rates and the US debt issue can have a complex and significant impact on US equity markets.

High Interest Rates

Reduced valuation multiples: Higher interest rates generally lead to lower valuations for stocks, especially growth stocks. This is because investors demand higher returns to compensate for the increased risk-free rate offered by bonds.

Increased borrowing costs: Companies with significant debt burdens may face higher interest expenses, reducing profitability and affecting stock prices.

Economic slowdown: Aggressive rate hikes can slow down economic growth, impacting corporate earnings and, consequently, stock prices. However, the Federal Reserve often aims for a “soft landing,” where growth slows enough to tame inflation without triggering a recession.

US Debt Issue

Investor sentiment: Concerns about the US government’s ability to manage its debt can erode investor confidence, leading to market volatility and potential selloffs.

Credit rating downgrades: A failure to address the debt ceiling or a significant increase in the debt-to-GDP ratio could lead to a downgrade of the US credit rating, impacting investor sentiment and increasing borrowing costs for the government and businesses.

Inflationary pressures: A rising debt burden can contribute to inflationary pressures, prompting the Federal Reserve to raise interest rates further, exacerbating the challenges for equity markets.

Conclusion for High Interest Rates and Debt Issue

The aggressive interest rate hikes by the US central bank, aimed at controlling inflation, have led to increased borrowing costs for companies and higher debt servicing costs for the government. These high rates can reduce stock valuations, particularly for growth stocks, and slow down economic growth, which in turn affects corporate earnings and stock prices. Additionally, concerns about the US debt ceiling and potential credit rating downgrades add to market volatility.

In the next section, we will be looking at the unexpected performance of US equities in 2023 despite the US Banking crisis. However, an additional risk is manifesting: the US commercial real estate.

3. US Commercial Real Estate Risk

In March 2023, aggressive interest rate hikes by the Federal Reserve led to a series of bank failures due to massive losses on government bond portfolios held by US banks. The SPDR S&P Regional Banking ETF, which tracks US regional banks, dropped over 40% from March to mid-May 2023. Despite this, the US stock market performed exceptionally well, with the S&P 500 index rising 24% in 2023.

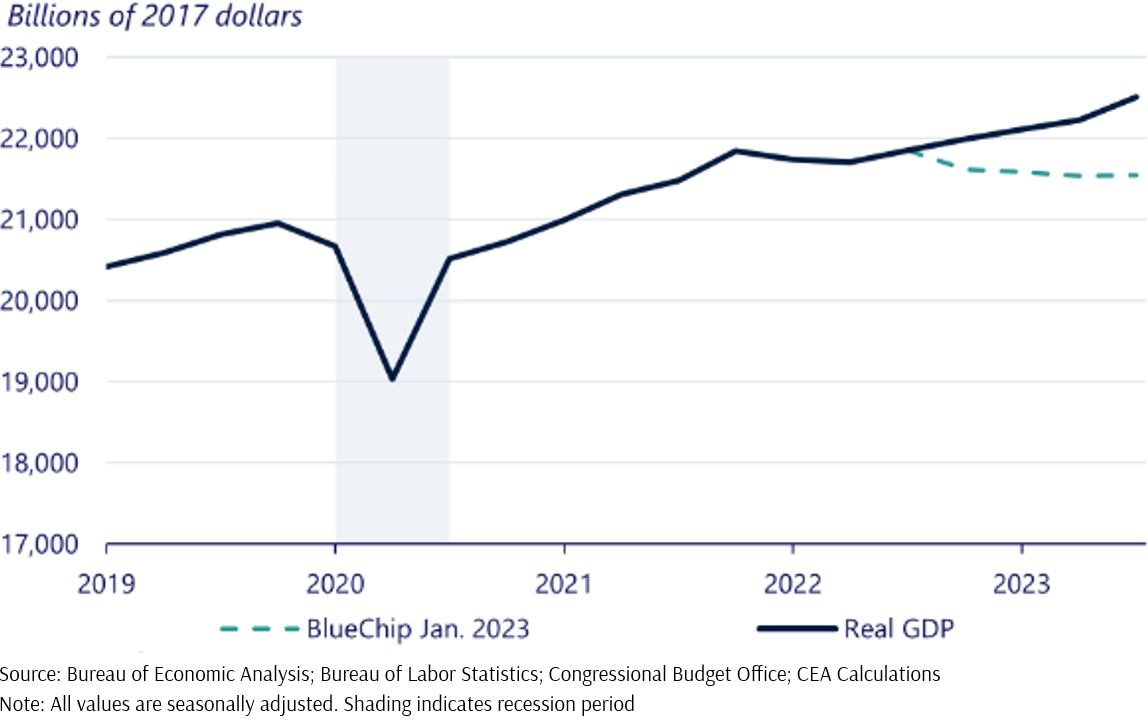

In October 2022, Bloomberg economists predicted a 100% chance of a US recession within a year, citing high interest rates, inflation, global unrest, supply chain issues, and an energy crisis. However, robust consumer spending helped the US economy grow significantly in 2023. The Blue Chip Economic Forecast had predicted -0.1% real economic growth for the year, but this was later revised to +2.6% (Exhibit 3), driven by consumer spending, a revival in manufacturing investment, and increased state and local government purchases.

Exhibit 3 – US Real GDP Growth: Actual vs Expected 2019 – 2023

However, US commercial real estate faced significant challenges. The shift to remote work resulted in less demand for office space, with about 50% of major global companies planning to reduce their office space within three years.

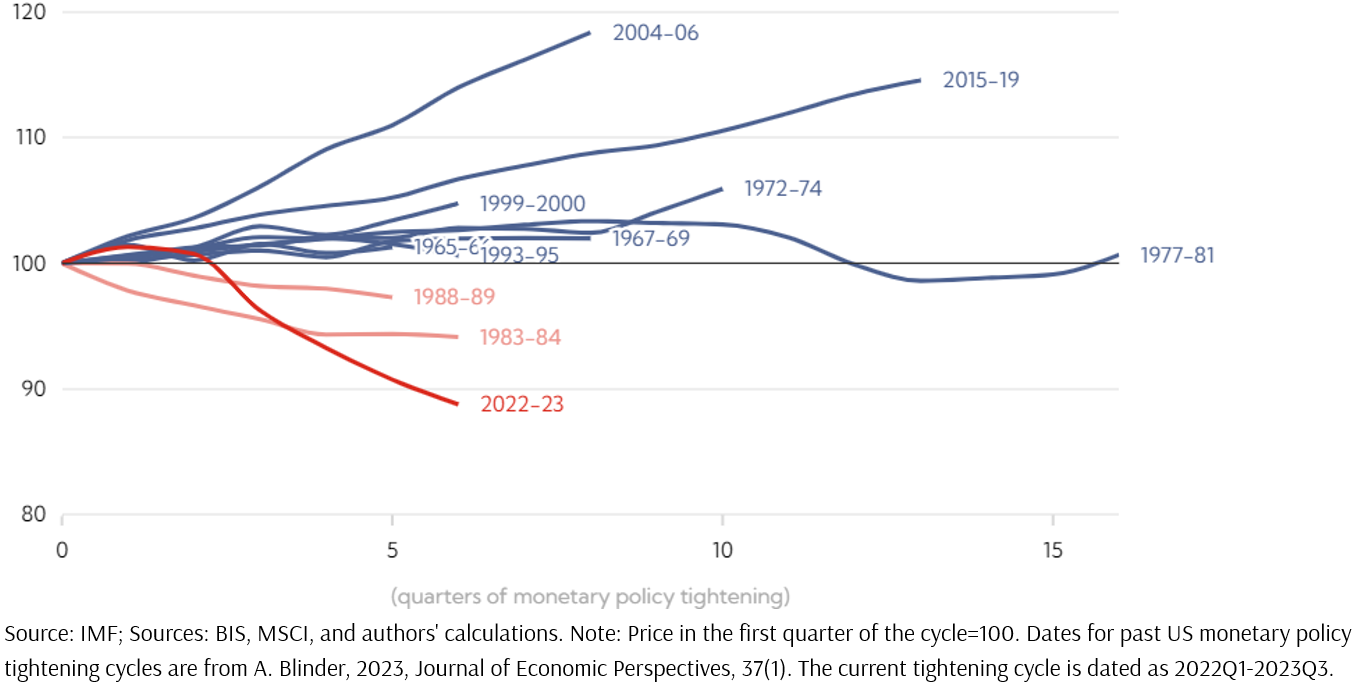

Knight Frank’s 2023 survey[4] of 347 companies indicated that firms with over 50,000 employees anticipated a 10%-20% reduction in office space. Historical data from the The International Monetary Fund (IMF) (Exhibit 4) showed that the 2022-2023 monetary policy tightening cycles led to the most significant plunge in US commercial real estate prices in recent history. This structural shift, exacerbated by the COVID-19 pandemic, has left American cities, especially San Francisco, highly vulnerable to vacant offices.

Exhibit 4 – US Real Commercial Real Estate Prices During Monetary Policy Tightening Cycles, Index

Implications of the US Commercial Real Estate Falling Prices

According to UBS[5] data and Visual Capitalist[6] charts, JPMorgan Chase, the largest US bank, has 12.6% of its loan portfolio in commercial real estate. Major banks like Wells Fargo are building larger cash reserves to buffer potential commercial property credit losses.

While major banks are somewhat insulated from commercial property shocks, averaging 11% exposure in their loan portfolios, smaller banks face greater risks, with about 21.6% exposure. For instance, just this month in August, a large office tower at 135 W. 50th St. in New York was auctioned off for $8.5 million, a significant decline from its $332 million purchase price in 2006[7]. New York Community Bancorp, a smaller regional bank with 57% of its total loans exposed to commercial property debt, reported a $2.7 billion loss in Q4 2023, leading Moody’s to downgrade its credit rating to “junk” status. The bank recently received a $1 billion capital infusion due to concerns over its commercial real estate loans.

Diminishing demand for office space is driving down property values and increasing vacancy rates, affecting the financial health of commercial property owners. This raises the risk of loan defaults, as the value of collateral depreciates. Consequently, banks could see a rise in non-performing loans, reduced profitability, and potential stock price declines. Investor confidence in these financial institutions may wane due to concerns over asset quality and loan loss provisions. Banks are likely to adopt a more cautious approach to commercial real estate lending, potentially restricting credit availability. A prolonged downturn in commercial real estate could lead to a broader economic slowdown, further challenging banks and impacting their stock performance.

Conclusion for US Commercial Real Estate Risk

The shift to remote work and subsequent reduced demand for office space have led to significant declines in commercial real estate values. Major banks with substantial exposure to commercial real estate loans are at risk of increased defaults, impacting their profitability and stock performance. Smaller banks are particularly vulnerable due to higher exposure levels. A prolonged downturn in commercial real estate could lead to broader economic challenges, further affecting the financial sector and overall market stability.

In the next section, we will explore how the upcoming US election could impact the risks we have discussed.

What does the Upcoming US Election Mean for These 3 Risks?

Here are three scenarios: one where Democrats win the House and hold the majority in the Senate, another where Republicans win the House and hold the majority in the Senate, and a third where there is a bipartisan split with one party controlling the House and the other the Senate. For each scenario, we analyse the potential impact on the identified risks based on reports from research bodies[8], considering the policies that might be enacted.

Scenario 1: Kamala Harris Wins the House and Majority in Senate

Inflationary Risks and Impact on US Equity Markets

Policies: Increased government spending on social programs, infrastructure, and green energy initiatives.

Impact: Potentially higher inflation due to increased demand and government expenditure. However, these policies may also stimulate economic growth, supporting equity markets in sectors like renewable energy, infrastructure, and technology.

High Interest Rates and the US Debt Issue

Policies: Continuation of current fiscal policies, potentially leading to higher debt levels.

Impact: High interest rates could increase the cost of servicing national debt, leading to concerns about fiscal sustainability. Equity markets might face pressure due to higher borrowing costs for companies, particularly those with significant debt.

US Commercial Real Estate Risks

Policies: Support for urban development and green building initiatives.

Impact: While these policies may provide some support to the commercial real estate market, ongoing challenges such as reduced demand for office space could continue to weigh on property values. Banks’ exposure to commercial real estate could lead to increased defaults, impacting financial sector equities.

Scenario 2: Trump Wins the House and Majority in Senate

Inflationary Risks and Impact on US Equity Markets

Policies: Tax cuts, deregulation, and tariffs on imports.

Impact: Tax cuts may spur economic activity, potentially leading to higher inflation. Tariffs could increase costs for consumers and businesses, contributing to inflation. Equity markets may benefit in the short term from tax cuts but face long-term inflationary pressures.

High Interest Rates and the US Debt Issue

Policies: Policies to stimulate economic growth, potentially increasing national debt.

Impact: High interest rates could exacerbate the debt issue, leading to higher debt servicing costs. Equity markets may face volatility due to concerns over fiscal sustainability and higher borrowing costs for businesses.

US Commercial Real Estate Risks

Policies: Deregulation and tax incentives for real estate development.

Impact: While these policies may provide some relief to the commercial real estate sector, the ongoing shift towards remote work could continue to depress demand for office space. Banks with significant exposure to commercial real estate might face increased risks, affecting their stock performance.

Scenario 3: Bipartisan Government (One Party Controls the House, the Other the Senate)

Inflationary Risks and Impact on US Equity Markets

Policies: Compromise policies with limited aggressive spending or tax cuts.

Impact: Inflation risks may be moderate as extreme fiscal policies are less likely to pass. Equity markets might experience stability due to balanced fiscal approaches, although growth may be slower compared to a unified government scenario.

High Interest Rates and the US Debt Issue

Policies: Compromise on fiscal policies, leading to moderate debt accumulation.

Impact: Interest rates might rise gradually, leading to manageable debt servicing costs. Equity markets could benefit from a more predictable fiscal environment, although sectors sensitive to interest rates may still face challenges.

US Commercial Real Estate Risks

Policies: Mixed policies with potential targeted support for real estate.

Impact: Continued challenges in the commercial real estate market due to reduced demand. Banks’ exposure to commercial real estate could lead to cautious lending practices, impacting their profitability and stock performance. However, bipartisan support for certain initiatives could mitigate some risks.

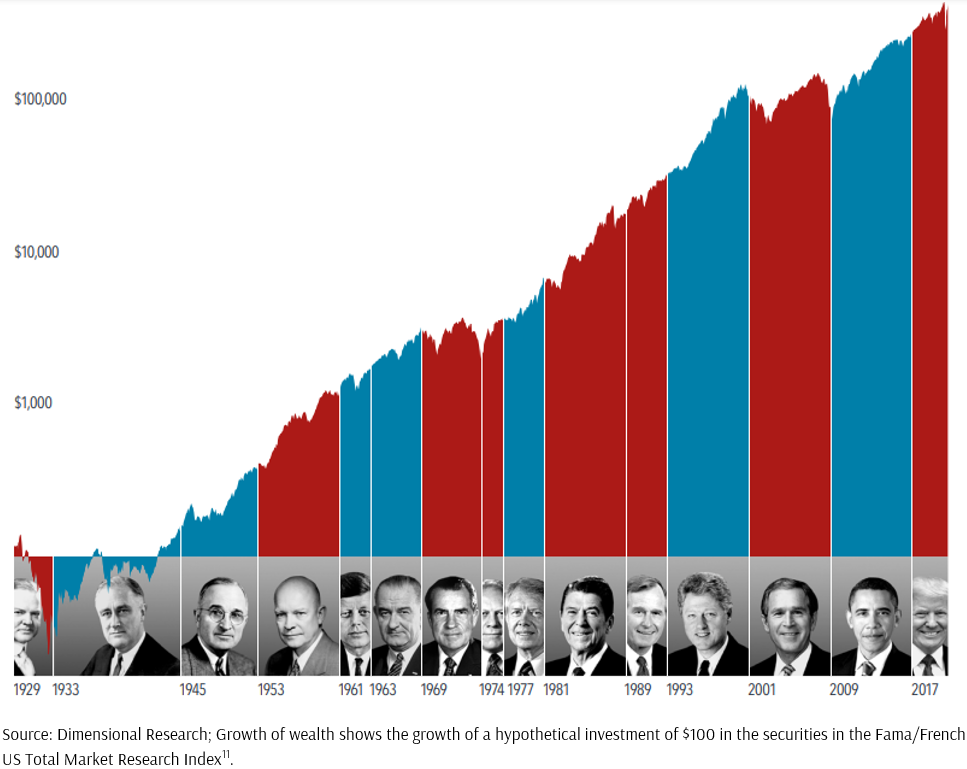

Does It Matter?

Investors often seek a link between the outcome of presidential elections and stock market performance. However, nearly a century of data shows that stocks have generally risen under administrations from both parties.

- Investors are buying into companies, not political parties. Companies focus on serving their customers and expanding their businesses, regardless of the occupant of the White House.

- While US presidents can influence market returns, many other factors also play a role, including the actions of foreign leaders, global pandemics, interest rate changes, fluctuations in oil prices, and technological advancements.

Stocks have consistently rewarded disciplined investors across Democratic and Republican presidencies (Exhibit 5).

Exhibit 5 – Growth of $100 in the US Stock Market (1929 – 2020)

You may also watch this video where I cover the three scenarios:

Conclusion

The dynamics of the 2024 US election underscore the significance of a long-term investment strategy amidst uncertainty. While the potential risks and market scenarios may create short-term volatility, a well-structured investment approach can help investors navigate these challenges more effectively.

By focusing on your long-term goals and maintaining a globally diversified portfolio, investors can better position themselves to weather the fluctuations that may arise from the electoral outcomes.

Ultimately, staying committed to a long-term wealth plan will be key to achieving your life goals, regardless of the political landscape.

[2] As of June 2024, CPI data.

[3] Comparing the Speed of U.S. Interest Rate Hikes (1988-2022)

[4] Half of the biggest global companies plan to cut office space. US cities will suffer most.

[5] Commercial real estate exposure at US banks

[6] Major U.S. Banks With the Most Commercial Real Estate Exposure

[7] From US$332 million to US$8.5 million: Office block’s price plunge captures Manhattan’s shocking office collapse

[8] Oxford Economics: 2024 US Presidential Election

Allianz Global Investors: US elections monitor: looking back to look forward

The writer, Lim Choon Siong, is Research Analyst at Providend Ltd, Southeast Asia’s first fee-only comprehensive wealth advisory firm.

For more related resources, check out:

1. Active Investing That Adds Value to the Client

2. Why Rolling Returns Could Increase Your Investment Conviction

3. Why a Robust Estimate of Future Returns Is Important for Investment Planning

Download our Investment eBook titled “A More Reliable Way to Get Enough Investment Returns: Even During Times of Market Uncertainty” here.

Through deep conversations with our advisers, you will gain clarity on what matters most in life and what needs to be done to live a good life, both financially and non-financially. Learn more about our investment philosophy here.

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current estate plan, investment portfolio, financial and/or retirement plan, make an appointment with us today.