Executive Summary

October was marked by heightened uncertainty surrounding the US election and a notable rise in US Treasury yields, driven by expectations of increased government debt and fiscal spending from both political parties. This led to a sharp increase in borrowing costs, with the 10-year US Treasury yield climbing by nearly 0.5%. For the first time since April, both global stocks and bonds experienced simultaneous declines, as equities contended with valuation pressures and bond markets adjusted to the yield increase. Major equity indexes—including the S&P 500, the MSCI World, and the MSCI Emerging Markets—posted losses amid the volatility, with Europe and China seeing particular downturns due to disappointing earnings and underwhelming economic stimulus respectively.

Despite these market challenges, portfolios designed with lower risk profiles—such as those holding short-term bond funds—demonstrated resilience, underscoring the importance of maintaining risk-aligned portfolios in turbulent times. Lower-risk allocations helped cushion the impact of volatility, highlighting the value of tailoring investments to individual risk tolerance and goals.

October’s declines serve as a reminder that macroeconomic conditions can change and swiftly impact market expectations and prices. Embracing this uncertainty and focusing on long-term wealth goals keeps investors well-positioned to navigate both gains and setbacks. Uncertainty is a powerful driver of long-term rewards, and our dedicated Client Advisers are here to support you in pursuing your unique life goals—helping you stay focused on what truly matters in your investment journey.

October Performance

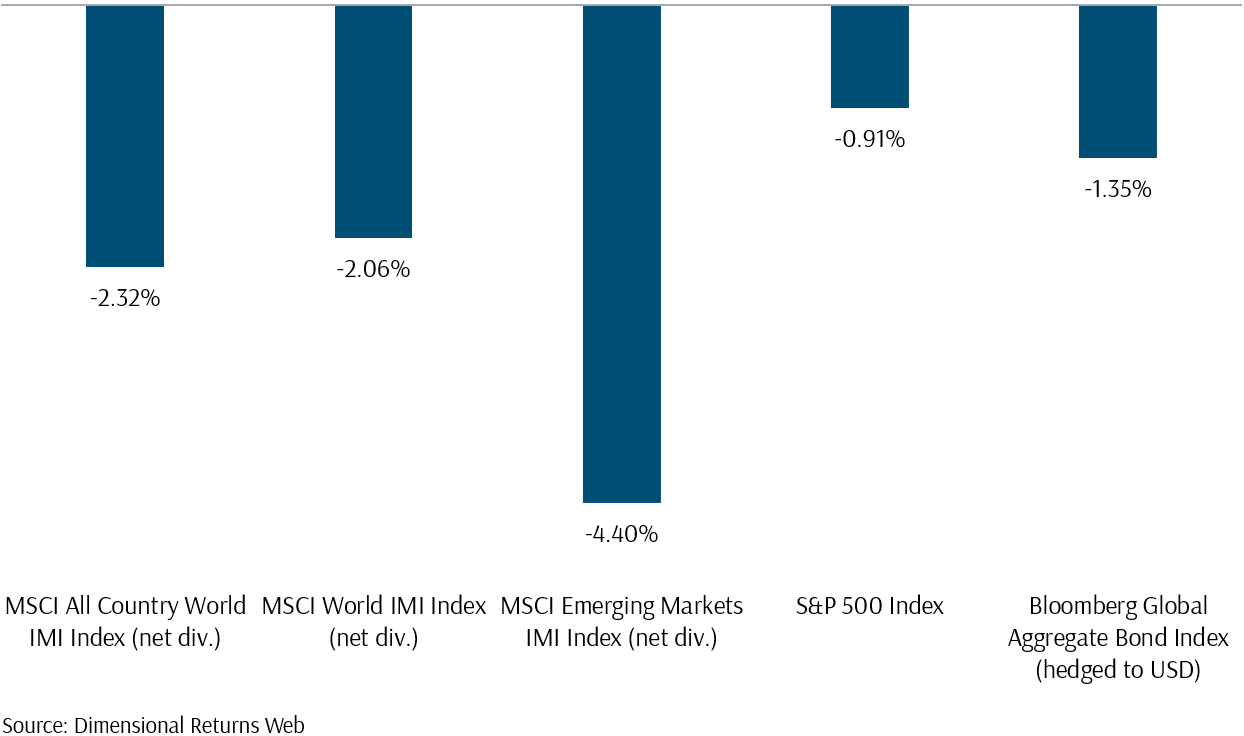

October proved to be a challenging month for both stocks and bonds, primarily driven by heightened uncertainty surrounding the 2024 US presidential election. A major factor was the anticipated increase in US government bond issuance and rising national debt, as both political parties advocated for expanded fiscal spending to support the US economy. This led to a significant rise in 10-year US Treasury yields, which increased by 0.48%, contributing to a 1.35% decline in the Global Aggregate Bond Index (Exhibit 1). As borrowing costs rose in the US, equities also took a hit, with the S&P 500, which represents the top 500 US companies, dropping by 0.91% (Exhibit 1).

In Europe, disappointing earnings reports fuelled the largest monthly decline year-to-date for the Stoxx 600, which fell by 3.35%. The Stoxx 600 is a broad European equity index that tracks the performance of the 600 largest companies across 17 European countries. Notable declines included Anheuser-Busch InBev, which dropped 7.41% after its Q3 revenue missed forecasts, and Deutsche Lufthansa AG, which fell 3.34% due to rising costs and intensified competition. This weakness in European equities contributed to a 2.06% decline in the MSCI World IMI Index, which tracks 99% of the investable market in developed economies (Exhibit 1).

In Asia, China’s underwhelming stimulus measures triggered a significant pullback in Chinese equities.Major tech giants such as Tencent, Alibaba, and Pinduoduo saw significant losses of 9%, 14%, and 10.6%, respectively. Given that the MSCI Emerging Markets IMI Index allocates about 25% of its weight to Chinese stocks, it too was impacted, declining by 4.40% (Exhibit 1).

On a global scale, the MSCI All Country World IMI Index, which tracks 99% of the investable market worldwide, fell by 2.32% (Exhibit 1).

Exhibit 1 – Market Index Performance: October 2024 (USD)

Dimensional Funds

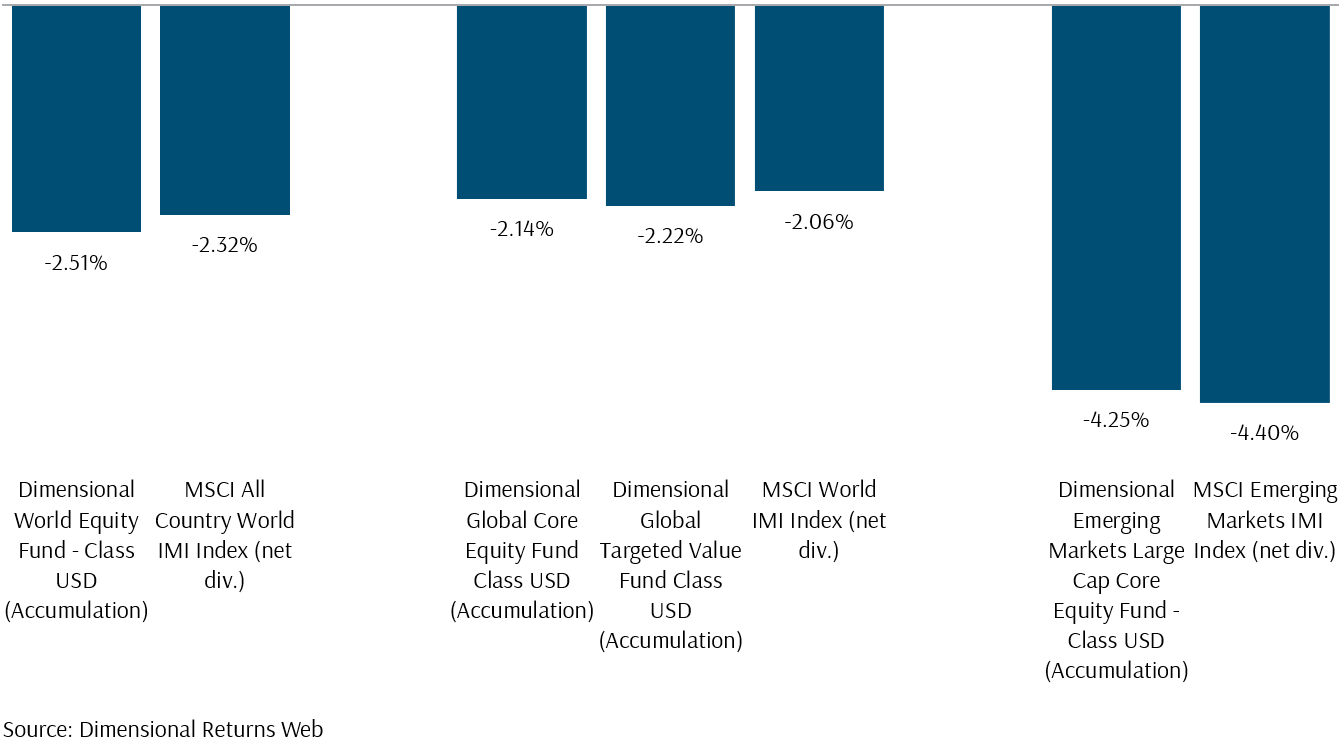

Dimensional Equity Funds Performance Largely Aligned with Indexes

Dimensional Equity funds tracked the indexes closely in October, with the Dimensional World Equity Fund trailing the index by a modest 0.19%. The rise in borrowing costs has had an uneven impact on large- and small-cap companies. Since small-cap companies generally carry a higher proportion of floating-rate debt compared to large-cap companies, the increase in borrowing costs has weighed more heavily on smaller companies. As a result, Dimensional’s developed market equity funds with higher small-cap exposure, such as the Dimensional Global Core Equity and Dimensional Global Targeted Value Funds, slightly lagged their respective indexes (Exhibit 2). Conversely, the Dimensional Emerging Markets Large Cap Core Fund outperformed the MSCI Emerging Markets IMI Index, benefiting from its higher allocation to large-cap stocks compared to the broader index (Exhibit 2).

Exhibit 2 – Dimensional Equities vs Market Indexes

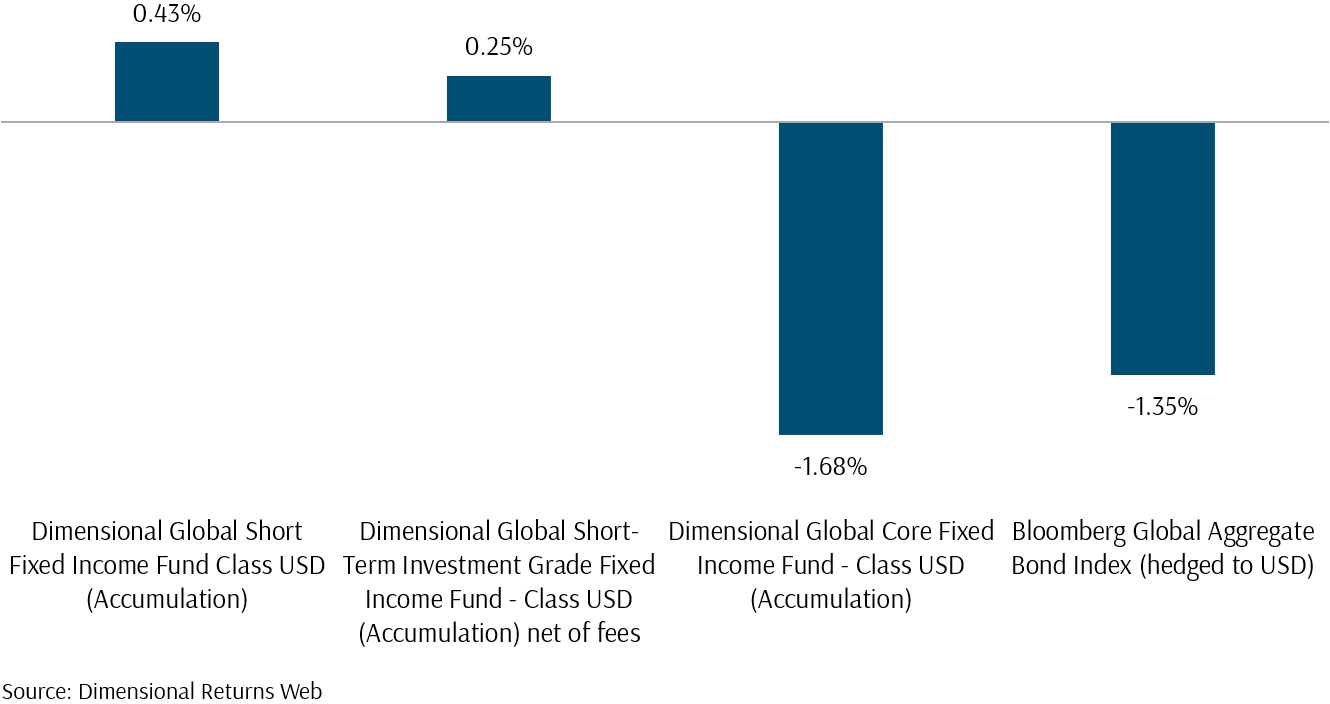

Dimensional Short-Term Bond Funds Help Offset Losses from Rising Yields

Intermediate-duration bond funds can capture term premiums over time, but they tend to experience larger drawdowns than short-term bond funds when yields rise. October serves as a clear example of this trend.

Exhibit 3 compares the returns of the Dimensional Short-Term Fixed Income and the Dimensional Short-Term Investment Grade Fixed Income funds with those of the Dimensional Global Core Fixed Income and the Global Aggregate Bond Index, which have intermediate durations. As shown, the Dimensional short-term bond funds achieved positive returns despite rising yields, while the Dimensional Global Core Fixed Income and the Global Aggregate Bond Index declined by over 1%.

Incorporating short-term bond funds into portfolios with shorter time horizons—such as Index Plus Low Risk, Conservative, and Balanced portfolios—can mitigate the effects of rising yields. This approach is essential for aligning wealth goals with a lower risk tolerance. More conservative portfolios provide enhanced stability, fostering peace of mind and contributing to a more favourable overall investment experience.

In the next section, we examine how the strengthening of the USD against the SGD has helped mitigate declines for SGD-denominated funds. However, this currency-driven cushioning effect should not be considered true diversification, as currency fluctuations are unpredictable and can quickly reverse.

Exhibit 3 – Dimensional Short-Term Bonds vs Global Core Fixed Income and Global Aggregate Bond

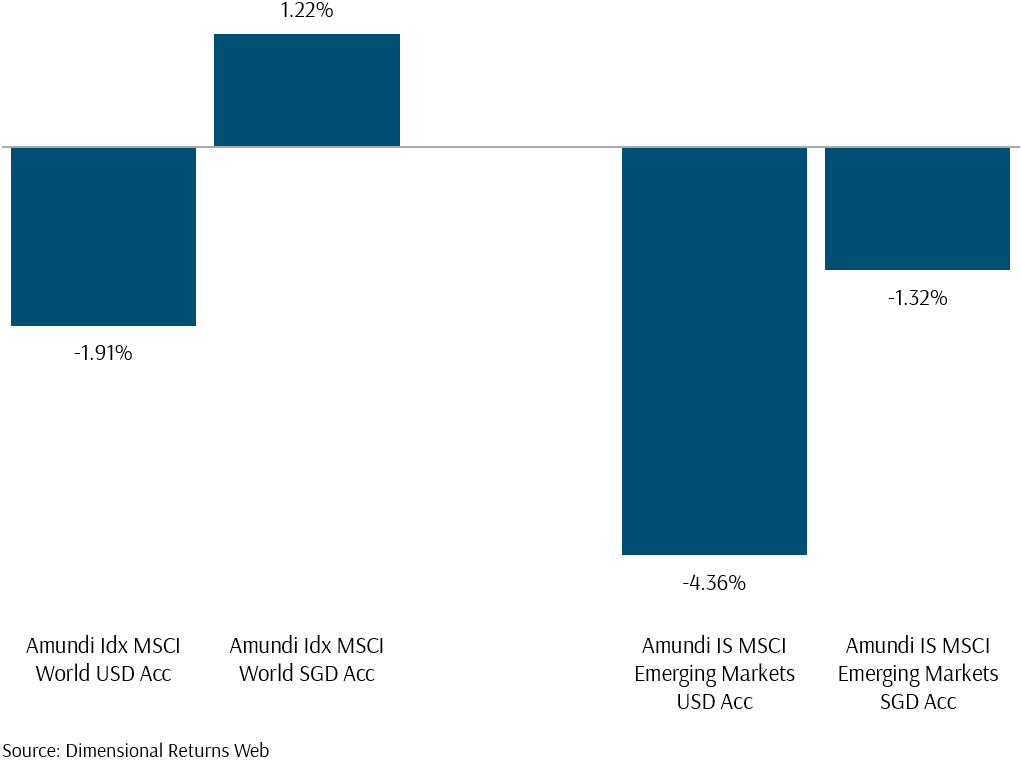

USD Rally Boosts Performance of SGD-Denominated Funds

Due to the rising US yields, the USD strengthened against the SGD by 2.7% in October. This currency movement helped offset losses in equity funds, as gains from USD appreciation provided a cushion. Exhibit 4 compares the Amundi Index equity funds in USD and SGD. As shown, while the Amundi Index MSCI World USD and the Amundi Index MSCI Emerging Markets USD both declined by 1.91% and 4.36% respectively, their SGD-denominated counterparts performed comparatively better, with returns of 1.22% and -1.32%, marking an outperformance of over 3%.

However, this effect is not guaranteed; if the SGD strengthens against the USD—for example, if US yields decline—the recent gains could reverse. Currency fluctuations are inherently unpredictable, and investors in stocks and bonds should avoid relying on them as a consistent source of returns.

Exhibit 4 – Amundi Index Funds SGD vs USD

October’s Market Key Takeaways – Managing Volatility Through Diversified and Balanced Strategies

October underscored the importance of navigating market volatility with a well-diversified approach that aligns with individual risk tolerance and wealth goals. While uncertainty around the US presidential election, rising yields, and geopolitical tensions across regions affected global markets, a diversified portfolio with thoughtfully selected assets—such as short-term bonds—can offer greater resilience.

Additionally, currency fluctuations, like the recent USD rally, may temporarily cushion returns for SGD funds but are unpredictable and should not be relied upon as a primary source of gains. Maintaining a balanced, risk-aligned portfolio is key to weathering these periods of instability and achieving long-term investment success.

November Market Begins with an Upbeat Start – US Small Cap Show Strength

November kicked off on a high note, with US markets rallying after Donald Trump’s presidential election victory. Investors showed optimism, anticipating that his proposed policies, such as individual and corporate tax cuts, could provide a boost to US businesses. Small-cap stocks, which are often more closely tied to the domestic economy, led the charge.

On top of that, the Federal Reserve’s 25-basis point rate cut added another tailwind, easing monetary policy and prompting further positive reactions in the markets. By 7 November, the Russell 2000 Index, which tracks the smallest 2000 US stocks, climbed 8.5%, well above the S&P 500’s 4.7% gain. This strong small-cap performance highlights investor confidence in US-centred growth as favourable policy changes come into focus.

Meanwhile, in China, the Hang Seng Index surged by 3.13%, driven by an influx of positive economic data that supported market sentiment. China’s exports grew at their fastest pace in over two years, with outbound shipments rising 12.7% year-over-year—far exceeding the 5.2% increase forecasted by a Reuters poll. This export strength reflects China’s resilience in global trade, while rising imports of raw materials signal steady demand, even as economic growth moderates. Markets are now watching for potential new stimulus announcements from the Chinese government on Friday, 8 November.

The first week of November has certainly set a strong tone, and I look forward to sharing more insights in the upcoming November market review. Next month’s edition will take a closer look at how these early movements evolved so stay tuned for a deeper dive into these market developments and their impact on our outlook for 2024.

Embracing Uncertainty: Staying Focused on Long-Term Goals Amid Market Fluctuations

The recent market movements and positive economic data are encouraging. Investors need to stay grounded and avoid getting swept up in short-term enthusiasm. Just as markets surged post-election and on strong export growth in China, they could quickly reverse if economic or policy expectations shift.

In October, stocks declined despite similar optimism about China’s stimulus in September, which ultimately fell short of expectations. Surprises like unexpected inflationary pressures or delays in stimulus measures could weigh on markets just as easily. Embracing this uncertainty is essential—by staying focused on your long-term wealth goals and remaining invested, you’re better positioned to navigate the inevitable ups and downs.

Uncertainty is a powerful driver of potential rewards; without it, there would be no surprises, no joy in the process, and no market premiums in the stock market over the past century.

Staying invested in a volatile market can be challenging, but you do not have to do it alone. Our dedicated Client Advisers are here to work with you every step of the way to reach your unique life goals. Embracing uncertainty becomes simpler and more meaningful when you have a trusted adviser by your side, empowering you to stay focused on what truly matters: achieving your life goals with more certainty.

For more related resources, check out:

1. How Much Impact Does The President Have On Stocks?

2. US Election 2024: 3 Key Risks and 3 Market Scenarios

3. Will the US Mega Tech Stocks Bring About a Dot-Com Bubble Burst?

Download our Investment eBook titled “A More Reliable Way to Get Enough Investment Returns: Even During Times of Market Uncertainty” here.

With a minefield of financial misinformation out there, we promise to be a safe pair of hands and a second pair of eyes to help you avoid costly financial mistakes. Learn more about our investment philosophy here.

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current estate plan, investment portfolio, financial and/or retirement plan, make an appointment with us today.