As of 20th May 2022, the S&P 500 has fallen 18.36% since the beginning of the year. The MSCI ACWI which includes the emerging markets is down 17.61% for the year. Even bonds were not spared. The Bloomberg Global Aggregate Bond Index came down 6.66% year to date. So why are both stocks and bonds falling? The main culprit is inflation. Governments all over the world have been injecting cash into the global economy by “printing money” and using them to buy bonds from financial institutions. This caused interest rates to fall, and banks flushed with cash aggressively extended credit to corporates and consumers. Demand for goods and services then increased, and made inflation go up. To make matters worse, supply chain disruptions caused by lockdown of cities such as those in China reduced supply and caused inflation to rise further. Then with the Russia-Ukraine conflict, food and energy prices skyrocketed (Russia was the world’s second biggest oil and largest natural gas exporter while Ukraine exported large amounts of soft commodities such as corns). To combat inflation, central governments have been increasing interest rates at lightning speed, with the hope of now doing the opposite – slowing down demand. The result: An expectation that companies’ earnings will drop and so equities fell and on the bond side, higher interest rates and higher inflation expectations pushed up the return demanded by bondholders to hold a bond, i.e., the yield and so bond prices fell in tandem with equities.

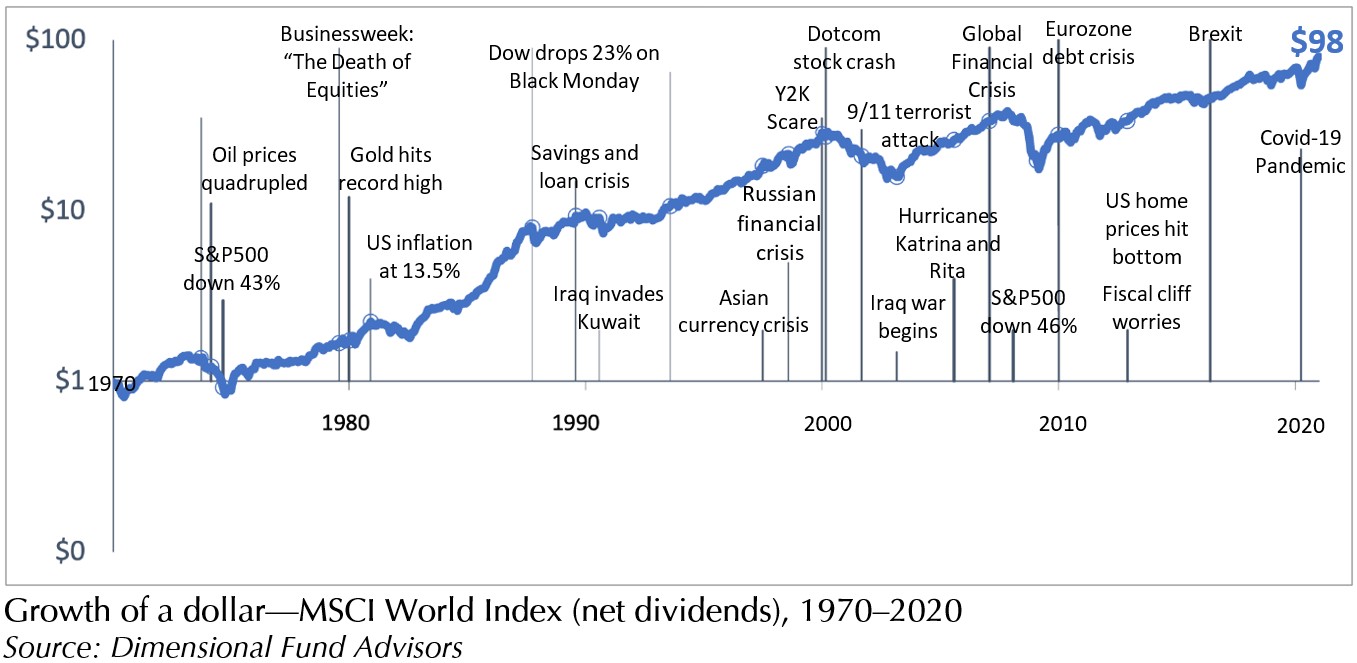

While many things can happen in the short term, one thing is for sure. Governments will continue to raise interest rates if inflation remains high (The US Fed funds rate is expected to be raised from the current 0.75% -1% to 2.5%-2.75% by end of the year). This may tip the global economy into recession, and it is this fear that will cause financial markets to be very volatile. But the world has experienced similar crises before (See chart). Over the past 50 years, we have seen stock market crashes, high inflation, financial crises, natural disasters, terror attacks and wars. While each situation might be different, through it all, one thing remained sure – the markets were resilient and grew. This time will be the same. The governments cannot increase interest rates forever. The pandemic will end. Lockdowns will be over and supply chains restored. Prices will stabilise and companies will continue to trade and make profits and the markets will rise again.

However, the greater fear now is the escalation of the Russia-Ukraine war. Russia has started moving nuclear-capable missiles towards its border with Finland after both Finland and Sweden have announced their plans to join NATO. What is going to happen if a nuclear war breaks out? Honestly, no one can be really sure. During WW2, when the US dropped 2 atomic bombs on Japan, the world survived because the devastation was isolated and even then, Japan recovered economically. But if the current conflict results in a nuclear war of a much larger scale involving more countries, then it is not likely that the financial system will hold together and it would mean that all financial assets can likely become worthless. That means that your strategy to mitigate the risk of a large scale nuclear war should then be to focus on survival being the top priority instead of protecting financial assets. One of the things you can do is to buy a farmland in a country with strong military power and good medical system (countries like the US or Canada comes to mind. You can’t easily buy land in China, unfortunately). You then need to build your house (perhaps far enough from strategic installations but not too far from medical facilities) and perhaps even bunkers deep underground and store enough food to last your through the war. The nice thing about farmland is that it is a cash yielding asset and also has appreciation potential as prices may go up overtime when everything is over. But between now till the catastrophic event happens, you may need to engage farmland management companies to manage the place for you. The minimum investment to set this whole thing up would be at least US$1 mil. But before we let our minds wonder too far, let us be rational and ask ourselves if we should really spend so much resources for an event with a low probability of happening? Besides, it is perhaps too late now to embark on this if you have not already done so.

How then should you respond?

1. If you are still accumulating towards your financial goals, knowing that markets are resilient and will rise over the long term, stay invested, keep investing in tranches and do not panic sell. However, this only works if you are invested into broadly diversified portfolios of securities with the track record and evidence of rising in the long term. Cryptocurrencies, concentrated and thematic portfolios of stocks or bonds and actively managed funds may not fit the bill here.

2. In order that you can weather through this storm, you must be financially healthy in the meantime. This is the time for financial prudence as recession looms. Make sure you have enough emergency fund to meet your family expenses for between 6-12 months in case you lose your income. It is not a good idea to over-leverage yourself to buy big ticket items that you do not need. Also, make sure you are comprehensively insured to mitigate life risks.

3. But for those who needs money in the next 1-3 years, do a review with your trusted adviser. If your investment portfolios have already met your return objectives, you may want to consider cashing out. Otherwise, find alternative funding or delay your goals or re-budget to spend lesser during this period.

Since the beginning of the year, we have been spending extended time communicating with our clients. Instead of busily trying to make changes to the investment portfolios, our focus has been on ensuring that our clients have the financial and psychological ability to weather through the turbulences. We can do that because every client has a “flight plan” drawn out based on their need, ability, and willingness to take risk. Furthermore, in the past years when it was easy to jump into the bandwagon of high risks assets such as growth stocks, high yield bonds and cryptocurrencies, we stayed on course with boring low-cost, globally diversified portfolios of equities and investment grade bonds. When we do that, we can then “maintain unwavering faith that we can and will prevail in the end, regardless of the difficulties, and at the same time, have the discipline to confront the most brutal facts of our current reality, whatever they might be.” – Jim Collins, Good to Great.

The writer, Christopher Tan, is Chief Executive Officer of Providend, Singapore’s first fee-only wealth advisory firm and author of the book “Money Wisdom: Simple Truths for Financial Wellness“.

The edited version of this article has been published in The Business Times on 23rd May 2022.

For more related resources, check out:

1. Where to Invest Your Money When Inflation is High

2. Investment Lessons from a Trip Down Memory Lane

3. A Double Whammy for Markets Amid Double Barrelled Reactions

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current estate plan, investment portfolio, financial and/or retirement plan, make an appointment with us today.