Executive Summary

August 2024 brought sharp market swings, driven by weak U.S. economic data and an unexpected rate hike from the Bank of Japan, which triggered a carry trade unwind and a global sell-off. However, as the month progressed, markets rebounded, fuelled by expectations of potential rate cuts from the Federal Reserve (Fed).

Despite early volatility, global equities finished the month strong, with major indexes like the MSCI All Country World and the S&P 500 gaining ground. This recovery highlights the importance of staying invested during turbulent periods. Whether the economy faces a hard landing, soft landing, or avoids a recession, maintaining a long-term perspective has historically been the best approach to navigate shifting market conditions. Staying the course through such fluctuations can help capture gains when markets recover.

August Performance

August proved to be anything but quiet for investors, with market volatility taking centre stage as disappointing U.S. economic data and a surprise interest rate hike by the Bank of Japan (BoJ) triggered a sharp sell-off across global markets early in the month. However, by the close of the month, markets had staged a strong recovery as the prospect of more aggressive policy easing by the Federal Reserve began to take hold.

At the start of August, weak U.S. data sparked fears of a recession. The July Institute for Supply Management (ISM) Manufacturing Index[1] came in well below expectations, and the jobs report revealed the smallest payroll increase in over three years. In addition, rising labour participation nudged the unemployment rate up to 4.3%.

Meanwhile, Japan made headlines as the BoJ unexpectedly raised its policy rate by 25 basis points. Governor of the BoJ, Kazuo Ueda’s hawkish tone prompted a rapid unwinding of carry trade positions, which had relied on borrowing at low interest rates in Japanese Yen (JPY) to finance investments in higher-yielding assets.

Against this backdrop, global equity markets experienced a significant sell-off, leading to a surge in volatility. The Volatility Index (VIX), often referred to as the “fear gauge,” spiked during this period, highlighting the heightened market uncertainty and investor anxiety. The VIX measures the expected volatility of the S&P 500 Index over the next 30 days based on options pricing, with higher values indicating greater anticipated volatility and market stress.

However, as the month progressed, the narrative shifted. Markets began to recover as investors priced in a more dovish outlook for the Fed, anticipating interest rate cuts in response to the slowing economy. Global bonds rallied, with the Bloomberg Global Aggregate Index gaining ground as weaker economic data and cooling inflation supported the case for lower rates.

By the end of August, it was clear that despite the volatility, investors had reason to stay optimistic. Equities rebounded, and fixed income markets provided stability, underscoring the benefits of patience and a long-term perspective during market swings.

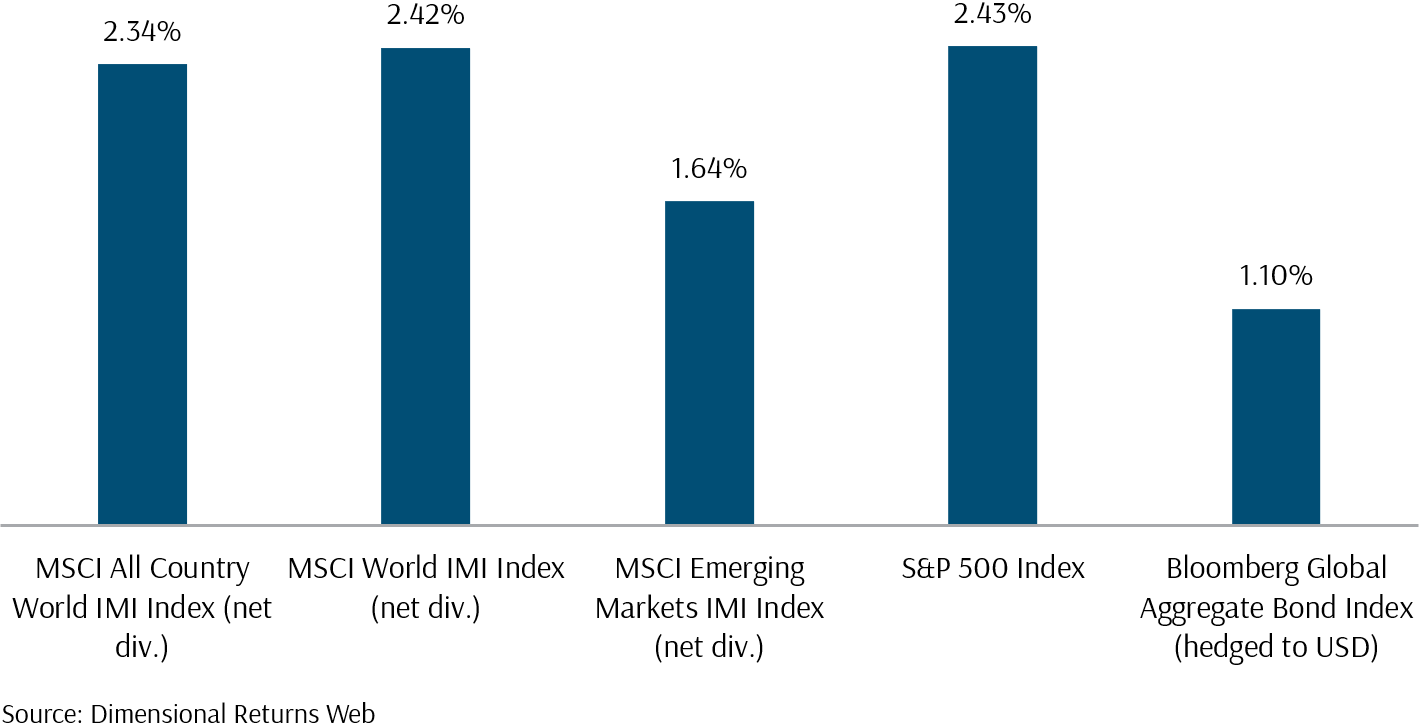

The MSCI All Country World IMI, the MSCI World IMI, the MSCI Emerging Market IMI, the S&P 500 Index and the Global Aggregate Bond Index all posted a positive performance, rising 2.3%, 2.4%, 1.6%, 2.4% and 1.1%, respectively, in August as investors reacted favourably to the prospect of easier monetary policy. This uplift was supported by lower bond yields, which helped equity valuations and bond prices.

Exhibit 1 – Market Index Performance: August 2024 (USD)

Dimensional Funds Performance

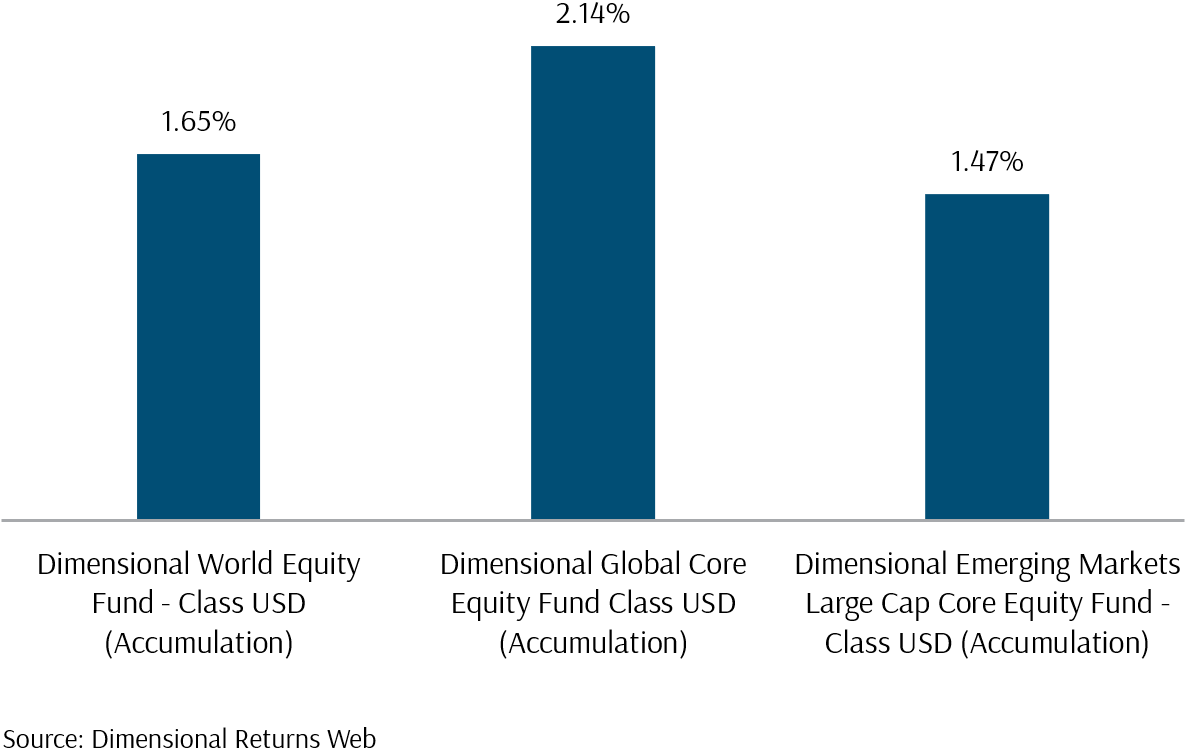

Dimensional equity funds lagged market indexes, primarily due to weak performance in small-cap stocks. The Dimensional World Equity, the Global Core Equity, and the Emerging Markets Large Cap Core Equity funds gained 1.7%, 2.1%, and 1.5%, respectively.

Large-cap stocks outperformed small-caps as investors sought stability. The Russell 2000 Index, tracking the smallest 2,000 U.S. companies, fell 1.5% in August, while the Russell 1000 Index, covering the largest 1,000 U.S. companies, rose 2.4%. This outperformance was largely driven by strong earnings in the technology sector, which makes up about one-third of the largest U.S. companies. The Technology Select Sector SPDR Fund, tracking the technology sector of the S&P 500 Index, rose 5% in August, doubling the S&P 500 Index’s performance.

Apple’s earnings exceeded analyst forecasts, with Q2 revenue increasing 4.9% to $85.78 billion, surpassing the $84.53 billion estimate despite a drop in iPhone sales. Meanwhile, Meta’s Q2 report outperformed Wall Street expectations and featured a positive revenue forecast, with revenue rising 22% to $39.07 billion from $32 billion last year. Apple and Meta share prices rose 3.8% and 9.8% in August, respectively.

Exhibit 2 – Dimensional Funds Performance: August 2024 (USD)

Fed’s Jackson Hole Meeting: Rate Cuts in Focus

The Jackson Hole symposium in late August saw Fed chairman Jerome Powell hint at the possibility of a rate cut, driven by weaker ISM manufacturing data and lower inflation figures. The softer tone from the Fed led markets to price in potential rate cuts as early as September.

A Double-Edged Sword: Weaker Economic Data

Weaker economic data creates a complex situation. While it bolsters the argument for interest rate cuts, it also signals deeper concerns about economic growth. A slowing economy could impact corporate earnings over time, particularly for sectors dependent on cyclical growth, such as consumer discretionary, industrials, and materials, which are more sensitive to economic fluctuations.

Early September ISM Data: Market’s Negative Reaction

In early September, markets reacted negatively to another round of weak ISM data, marking a departure from the market’s more optimistic reaction in August. This volatility underscores how quickly sentiment can shift based on economic headlines. Investors should avoid making decisions based solely on day-to-day market reactions or headlines. Instead, it is crucial to focus on long-term fundamentals and maintain a disciplined approach, recognising that short-term volatility often presents opportunities rather than reasons to panic.

Staying Invested Regardless of Economic Outcomes

As the debate around the economic outlook intensifies—whether the U.S. and global economies are heading towards a hard landing, soft landing, or avoiding a recession altogether—the key takeaway for investors remains the same: staying invested is the best long-term strategy.

1. Hard Landing Scenario:

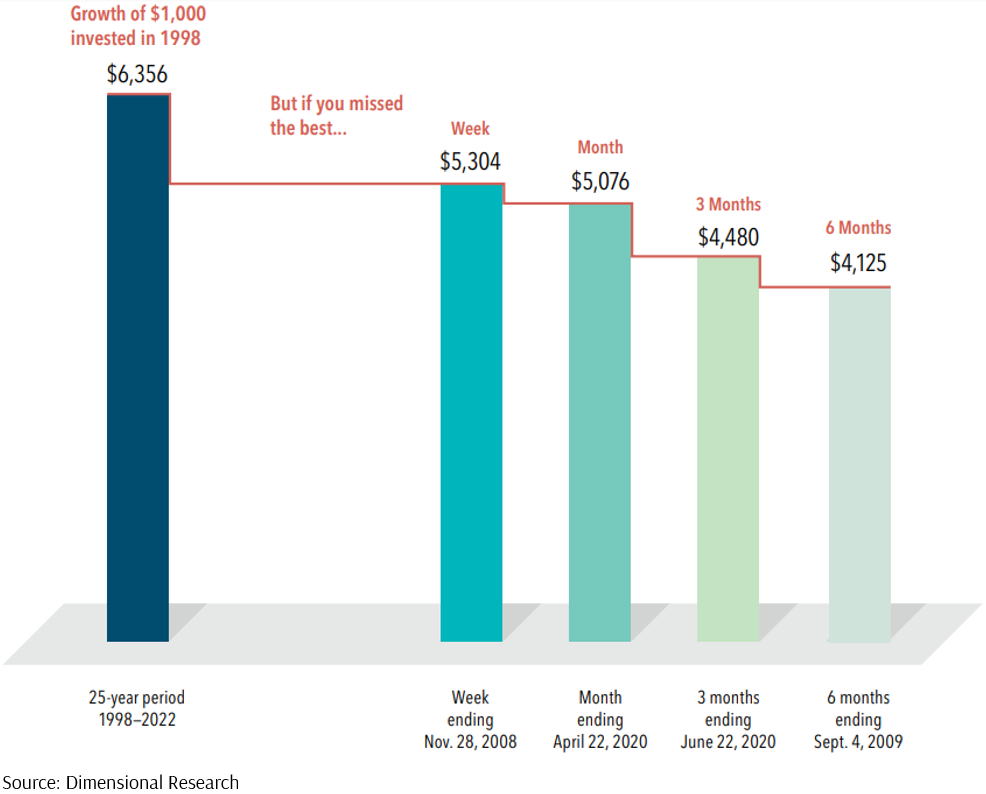

The weak ISM data from September 2024 has reignited fears of a potential hard landing, where economic growth sharply contracts, potentially leading to a recession. Historically, equity markets tend to perform poorly leading into a recession, but attempting to time the market by selling off during downturns is notoriously difficult. Many investors who exit the market during downturns fail to re-enter in time to benefit from the subsequent recovery. The sharp rebound after the early August sell-off due to the carry trade unwind is a prime example of how quickly markets can recover once conditions stabilise. Missing just a few of the market’s best-performing days can severely impact long-term returns.

Exhibit 3 – The Russell 3000 Returns From 1998 – 2002 (Missing the Best Consecutive Days)

2. Soft Landing Scenario:

On the other hand, soft landing scenarios, supported by the recent robust consumer spending[2], suggest that the economy could slow without entering a full-blown recession. In this environment, equities tend to perform well, especially as inflation moderates and interest rates potentially fall. Investors who remain patient during periods of uncertainty can capture these gains. The technology sector’s resilience in August, as seen from companies like Apple and Meta, illustrates how sectors can thrive even in a moderating economy.

3. No Recession Scenario:

Even in a scenario without a recession, where the economy grows at a slower pace, the advantages of staying invested remain evident. Historically, markets have favoured patient, long-term investors. A diversified portfolio can capture gains across various sectors, even during downturns, while offering protection against cyclical sectors like energy, materials, and technology. For instance, consumer staples have performed well, with the Consumer Staples Select Sector SPDR Fund, tracking this sector within the S&P 500 Index, rising 6% in August due to strong revenue and earnings from major retailers like Walmart and Costco. Moreover, sectors sensitive to interest rates, such as real estate and utilities, may benefit if the Federal Reserve starts cutting rates, as anticipated from recent communications at Jackson Hole.

Conclusion

The economic environment remains uncertain, but the lesson from both recent market events and historical data is clear: staying invested is the most reliable way to build wealth over time. Whether the economy faces a hard landing, a soft landing, or no recession, reacting to short-term news, like weak ISM data or interest rate adjustments, can lead to costly mistakes.

Market timing is challenging, and attempting to anticipate economic turning points can result in missing the best market days, which often occur close to periods of volatility. Instead, maintaining a long-term perspective and focusing on fundamentals, diversification, and discipline can help investors navigate through all market conditions.

We believe that our globally diversified portfolios are a prudent strategy to capture market returns and effectively support our clients’ wealth plans, where we have taken into consideration the potential short-term volatility with enough time to ride through market ups and downs

As always, if you have any concerns about the market conditions, please do not hesitate to reach out to your Client Adviser.

We thank you for your ongoing trust and support. We look forward to continuing to assist you in achieving your life goals.

– Footnotes –

[1] The ISM Manufacturing Index is a key economic indicator that measures the health of the manufacturing sector in the US. The index provides insights into trends in production, employment, and new orders, helping to gauge the overall economic climate and business conditions.

[2] An update on US consumer sentiment: Consumer optimism rebounds—but for how long?

For more related resources, check out:

1. Active Investing That Adds Value to the Client

2. Why Rolling Returns Could Increase Your Investment Conviction

3. Why a Robust Estimate of Future Returns Is Important for Investment Planning

Download our Investment eBook titled “A More Reliable Way to Get Enough Investment Returns: Even During Times of Market Uncertainty” here.

With a minefield of financial misinformation out there, we promise to be a safe pair of hands and a second pair of eyes to help you avoid costly financial mistakes. Learn more about our investment philosophy here.

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current estate plan, investment portfolio, financial and/or retirement plan, make an appointment with us today.