In the last article, we explained that our investment philosophy is largely driven by the needs of our clients. We developed a set of model portfolios to help our clients achieve a range of financial goals.

In this article, we would like to explain how wealth is built.

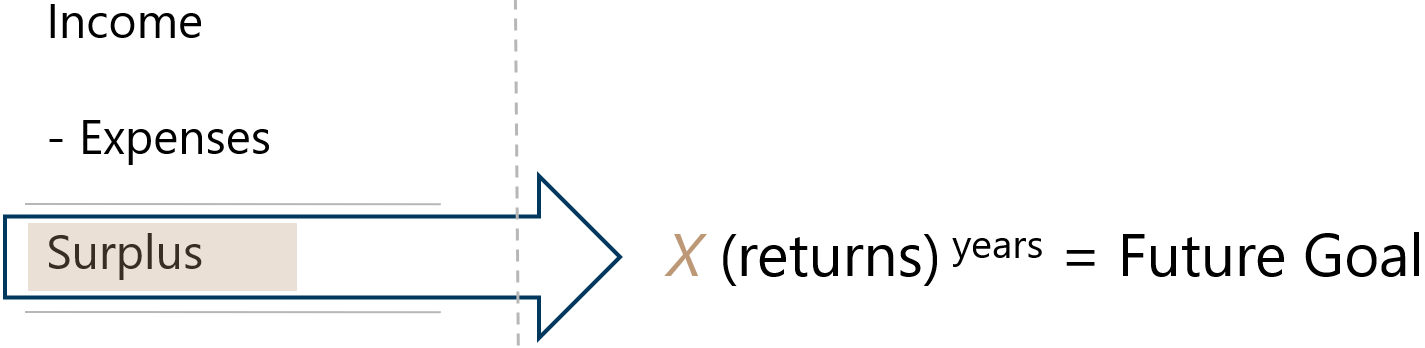

Our CEO of Providend, Christopher Tan often illustrate that to reach your financial goals, it boils down to how you manage your life with the following equation:

We believe that this equation explains how wealth is generally built well.

Expanding Your Surplus As Much As You Can

What separates a lot of the people that were able to achieve their financial goals, and those who struggled is the size of their surplus.

Surplus = Income minus Expenses

The surplus is the difference between your income and your expenses. A lot of you would call this your savings.

The larger your surplus, the more you retain from your income to allocate to fulfil your financial goals.

Here is a list of things you could do with your surplus:

- Contribute to your financial independence

- Fund your children’s education

- Increase debt payment to accelerate your debt payoff

- Funding for seminars, higher education to improve your future earnings potential

- Capital improvements to your home

Your financial goals might be similar to these and if they are important to you, then you should progressively improve your level of surplus.

To do that, you will need to:

- Increase your income. Improve your business, increase revenue and profits so that you can increase the business income paid to you. Improve your human capital, make yourself more valuable to your company/prospective companies so that your income can climb

- Optimize your expenses. Be a value spender. Value the goods & services that you need to spend on, determine the grade of goods & services you need, and try to spend as low as possible for the grade of goods & services you need

What we observe is that for many people, their income increases over time with inflation as well as excellence in career management. However, their expenses also increase proportionately as their income increases.

In some cases, they work in jobs that require great commitment, and thus part of their income is used to exchange for the time that they could not spend taking care of their children or to decompress from a high stress life.

A good metric to determine whether you are improving in this aspect of the equation is to track your surplus rate.

![]()

To build greater wealth, we can aim to consistently improve our surplus rate. Try our best to optimize our expenses and not expand our expenses on goods & services that we care less about. Improve our income.

Your Future Wealth = Current Wealth + Surplus Year 1 + Surplus Year 2 + Surplus Year 3 + … + Surplus Year 25

In a way, our future wealth is made up of the wealth that we currently have plus all the surpluses we have accumulated between now and when we need it. If we manage to accumulate good surpluses year after year, our wealth will build up.

The opposite of your surplus rate is your spending rate. The spending rate is the percentage of your income that you spend.

We will look at why improving your surplus rate is so important.

But first let us explain the laws of compounding.

Improve Your Rate Of Return And Let Time Work Its Magic

Improving your surplus rate is just one part of the equation.

(Current Wealth + Surpluses) x (Rate of Return)Time = Future Goal

To grow your wealth, you will need your current wealth and accumulated surpluses to grow at a decent average rate of return.

If you start young, you will be able to make use of the long duration of time between now and when you need the money to compound your wealth.

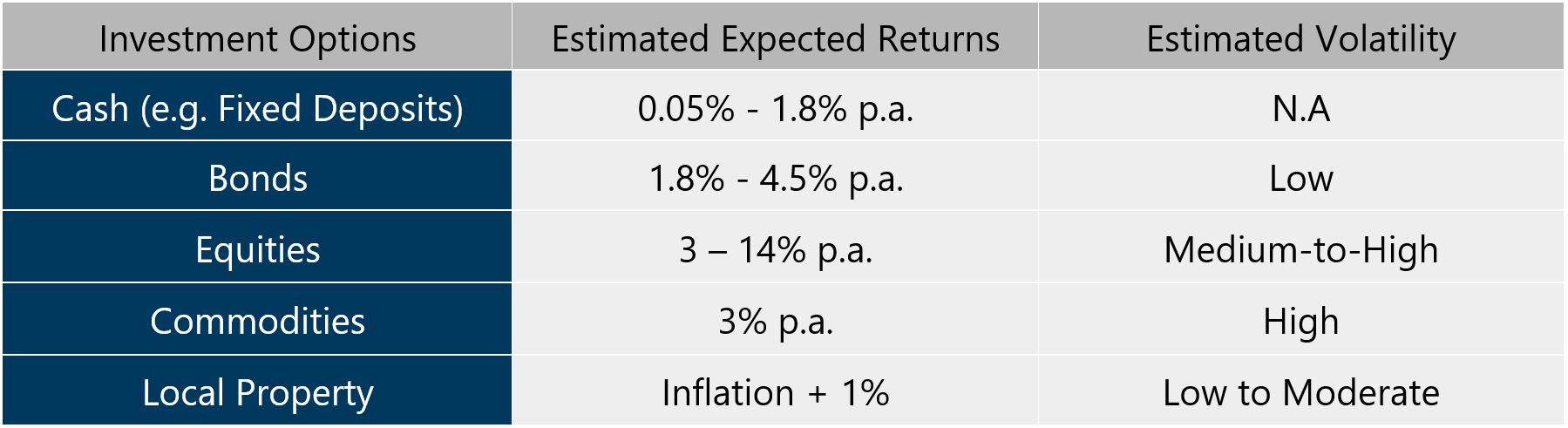

We can get a different rate of return by allocating our wealth into different investment options. Generally, the riskier the investment options, the higher the potential returns to compensate for the risks that you take with the investment.

The table below shows the estimated expected return of different investment options:

A person who wishes to build wealth will hold their wealth in a mixture of these assets and his/her rate of return will depend on the mix.

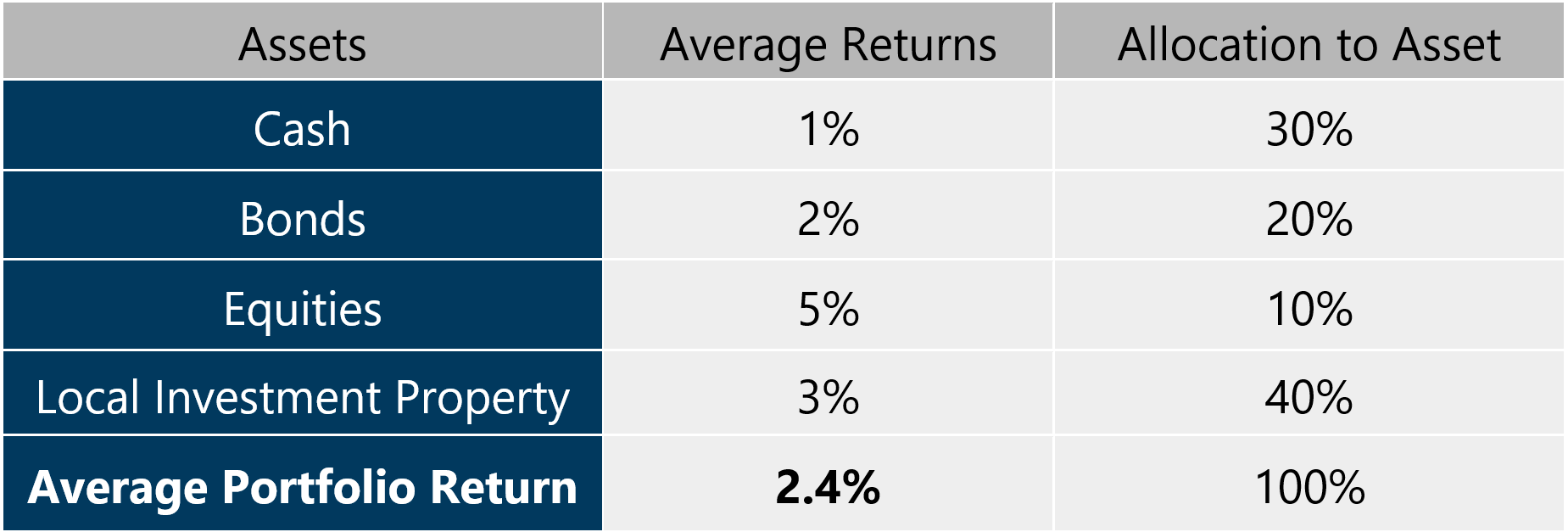

The table below shows the asset allocation of an investor named Jane:

Jane has a large portion of her wealth in property, cash and bonds. The average return that Jane could expect is 2.6%. The aggregate volatility of her portfolio would be rather low (since it is made up of almost all the investment options that have low volatility profile)

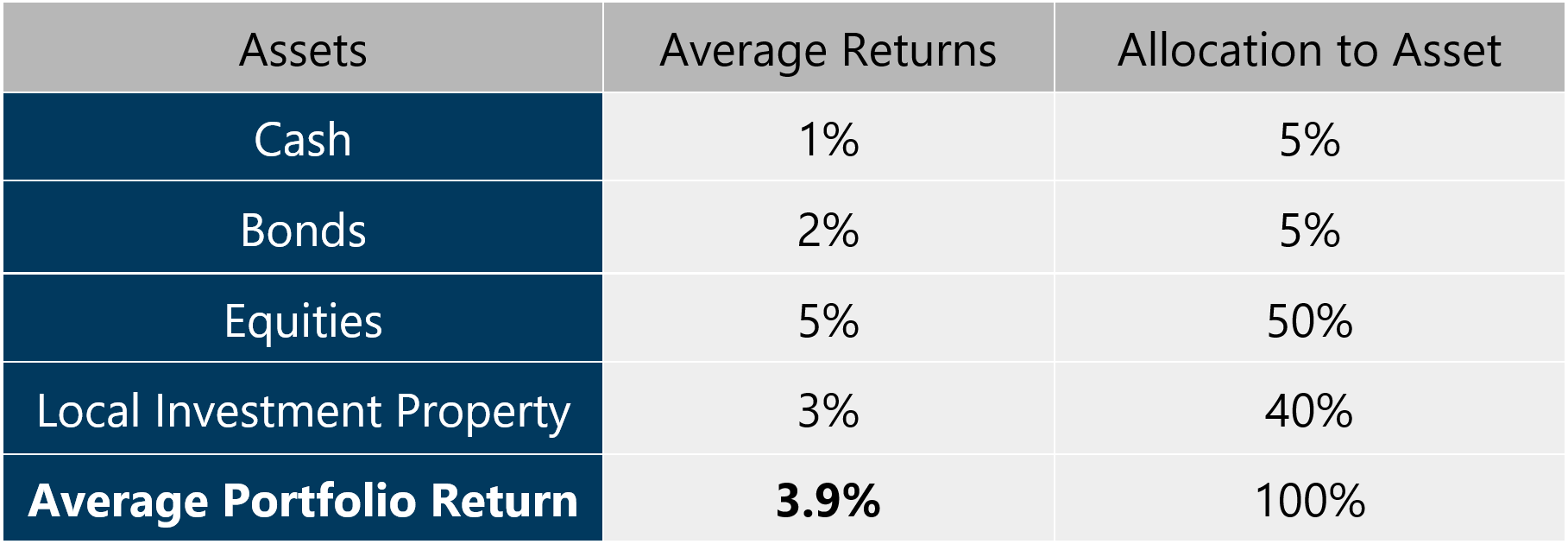

If Jane is looking to boost her average rate of return from 2.6% a year, she would need to shift a higher allocation into investment options that give higher expected returns.

Here is Jane’s allocation if she tries to optimize the allocation:

Jane boosted the rate of return of her wealth by 50% from 2.4% to 3.9% a year.

Time in Sensible Investments Compounds Your Money Over Time

A critical element that we will bring in to boost wealth building is time.

Albert Einstein reportedly described compound interest as “the most powerful force in the universe.” He suggested that compound interest is the 8th wonder of the world and that while it is often described positively, compound interest can work against you.

If your investment pays you interest and you re-invest the interest to purchase more investments, you will not only earn interest on your principal but also on your interest. Given enough time, you would be able to see your investment piling up.

For investments that do not provide an interest income, an investor such as Jane can experience the compound growth of the underlying assets.

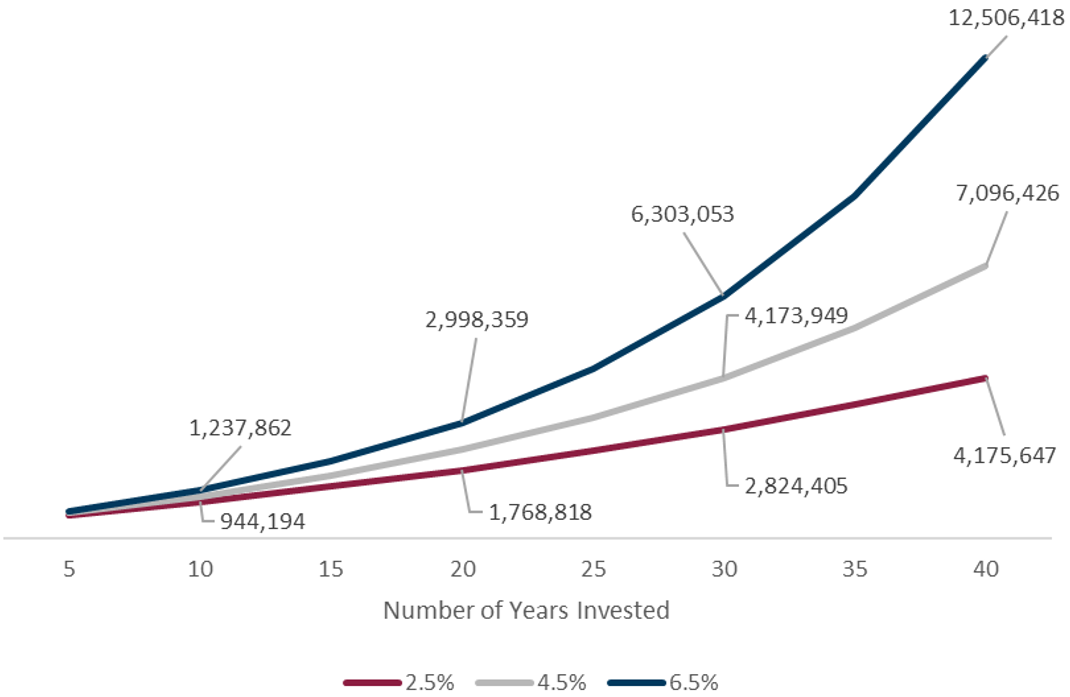

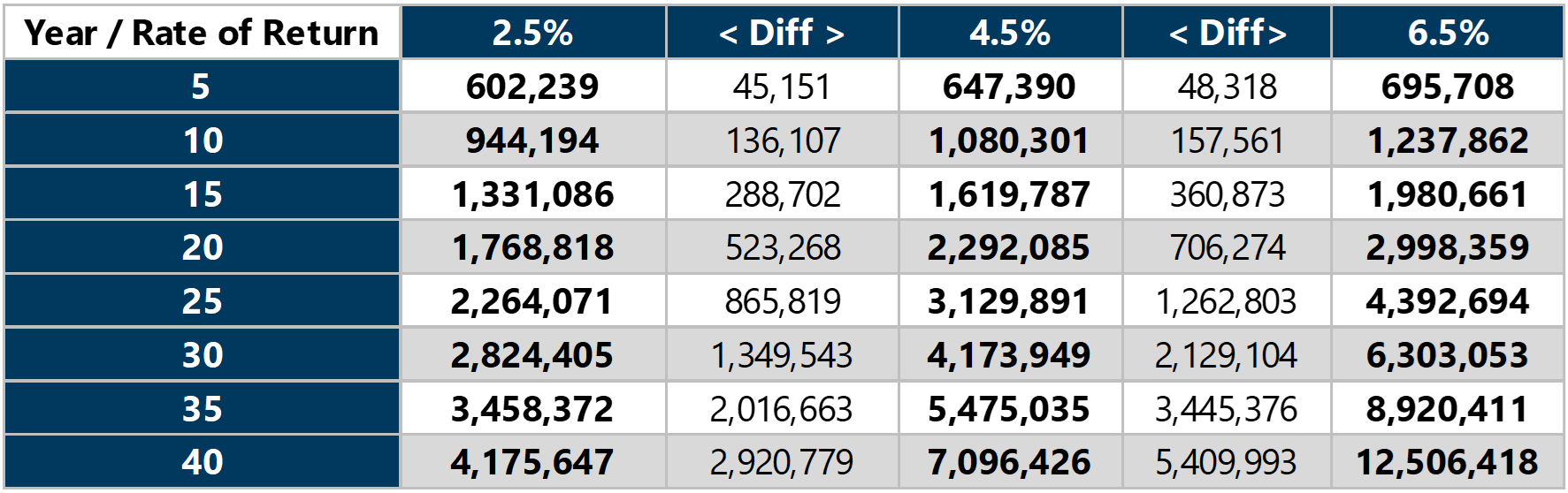

Eva has $300,000 as a lump sum at the start and wishes to build wealth so that she can be financially independent. She also decided to contribute $50,000 a year from her family’s annual income building towards financial independence.

She can have her choice of 3 allocations:

- Conservative: Rate of return of 2.5% a year

- Moderate: Rate of return of 4.5% a year

- Aggressive: Rate of return of 6.5% a year

Here is her wealth growth if she chooses these 3 different allocations:

Here is the growth of wealth in numerical detail:

If Eva invests for 10 years at 2.5%, 4.5% and 6.5% a year, she would grow her wealth to $944k, $1.08 million and $1.23 million respectively.

The difference between choosing different allocation to get a different rate of return is small.

But as you see, the longer Eva keeps to this way of building wealth, the difference between the various rate of returns becomes greater.

If she invests for 30 years, the difference between 2.5% and 4.5% a year is $1.35 million and the difference between 4.5% and 6.5% a year is $2.13 million.

This difference can mean

- An earlier financial independence

- Greater income during financial independence

- Opportunity to re-allocate to other financial goals

The difference is greater if you compare between 2.5% and 6.5% a year.

The difference between 5 years & 30 years, and 2.5% a year & 6.5% a year emphasize the power of compounding growth and why the rate of return Time is a vital element in building wealth.

Surplus And Rate Of Return: Which One Makes The Most Impact?

You may be wondering that out of the following:

- Surplus Rate

- Rate of Return

Which factor makes more impact on your wealth-building.

Both matters but for accumulators, the surplus rate would be more vital. However, at some point, the rate of return matters a lot as well.

I think it is better we explain this with some examples.

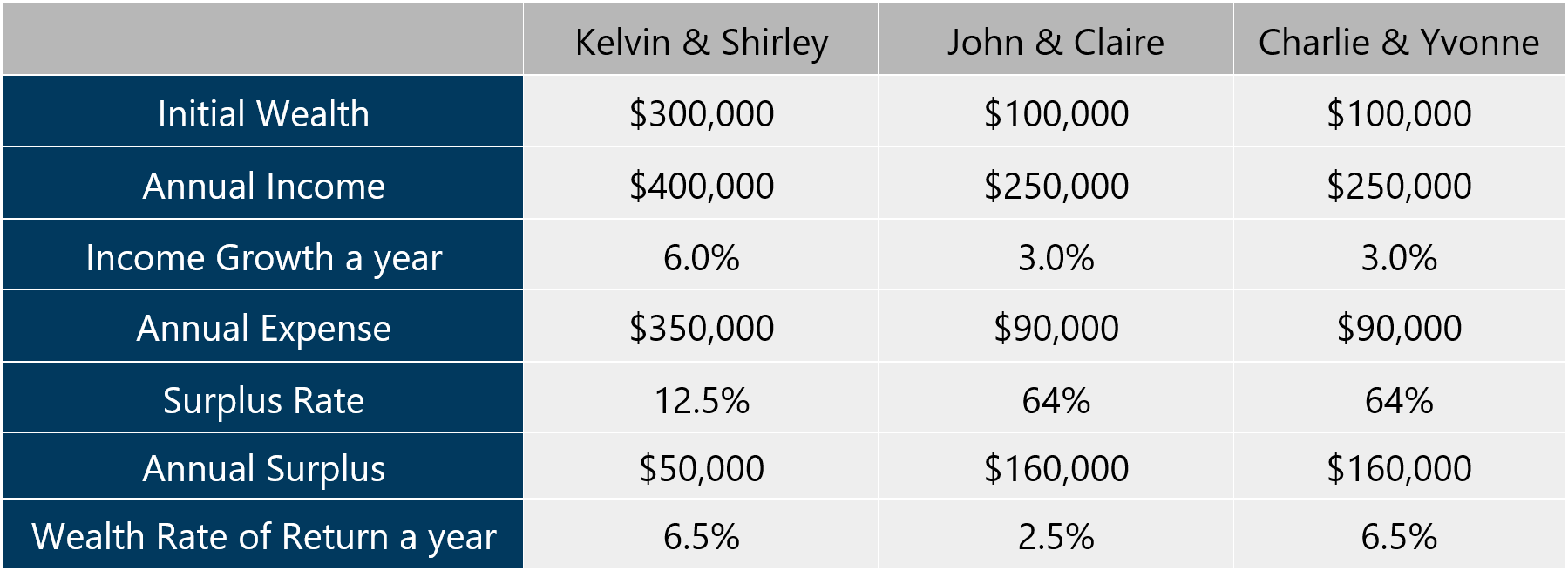

Let us apply the wealth equation to 3 different couples and observe the wealth that they build up respectively after 20 years.

Kelvin & Shirley are the high earning couple. They earn a combined $400k a year and holds jobs that they are likely to enjoy above-average income growth (6% a year). However, their surplus rate is low as their expenses are also high. Kelvin and Shirley are also more comfortable taking risks, so their wealth is allocated to assets of a higher risk spectrum.

John & Claire in contrast is more careful. They do not earn as high of an income as Kelvin & Shirley but still considered above average income. Their expenses are more controlled and thus enjoyed a 64% surplus rate. Their income growth is halved of Kelvin & Shirley but rather decent. They also started with less wealth then Kelvin & Shirley and due to their conservative nature, their asset allocation may only allow them to earn an average return of 2.5% a year.

Lastly, Charlie & Yvonne are similar to John & Claire but they have higher risk appetite and thus their rate of return is similar to Kelvin & Shirley.

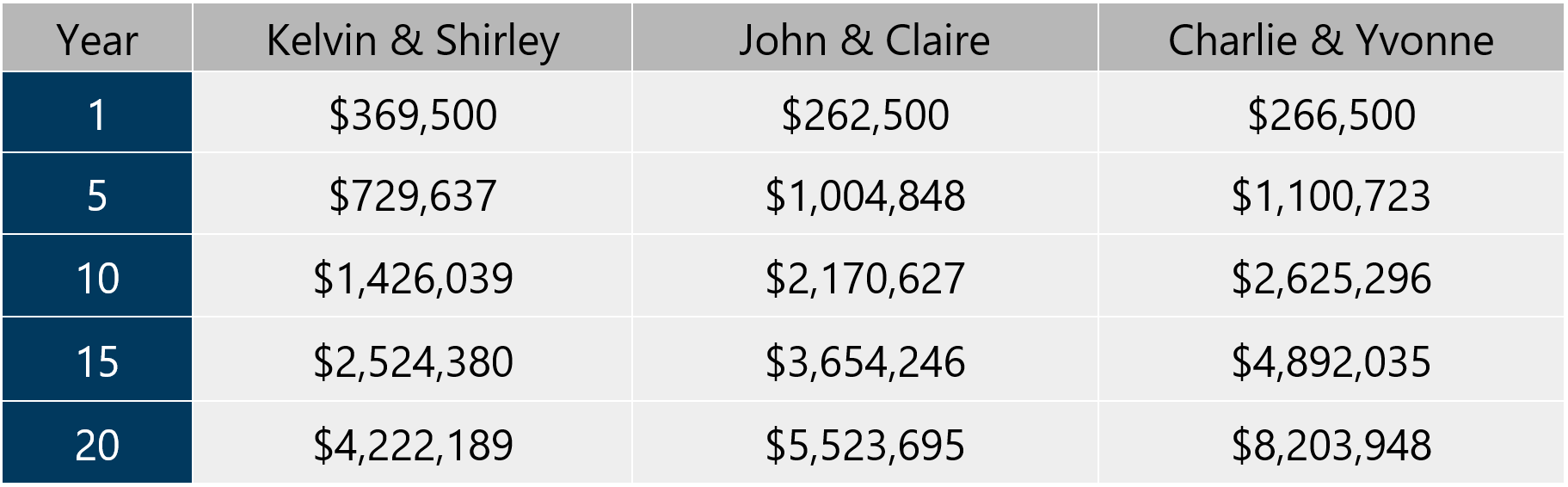

Here is the wealth accumulated for the 3 couples at different time intervals:

All 3 couples managed to build wealth after 20 years. (If you invest in sensible investments, following Chris’ formula definitely will help you build wealth)

Kelvin & Shirley didn’t build as much as the other 2 couple, despite having a higher income, greater income growth rate, greater starting wealth and higher expected return from their investments.

As a comparison here is their ending income:

- Kelvin & Shirley: $1.2 million

- John & Claire: $438,377

- Charlie & Yvonne: $438,377

High income and income growth rate give you a tremendous leg-up in wealth building. However, it is only good if you are able to keep your expenses in check so that your surplus rate is high.

John & Claire and Charlie & Yvonne’s frugality has allowed them to achieve an absurdly high surplus rate.

Let us zoom in on John & Claire and Charlie & Yvonne. What separates these 2 couples is their investment rate of return.

You would notice that for the first 10 years, the difference between the wealth built was not too different (Year 10: $2.17 million vs $2.63 million).

However, from year 10 onwards, the greater investment rate of return becomes very telling (Year 20: $5.5 million vs $8.2 million)

Your surplus rate is very important but at some point in the future, a higher investment rate of return will become crucial to your wealth-building.

Key Takeaways

We find that different experts will explain how to build wealth differently but they tend to be rather similar to our formula:

We learn from the 3 couples that to build wealth well, you need to

- improve your surplus rate

- increase your rate of return

- be able to stay invested for a long time to capture the rate of return in #2

Here is the thing: You would realize that the only factor that the Providend Investment Solutions Team have influence over is the Rate of Return.

We have no control over:

- Helping you earn more in your business and your job. You need a career coach or a business coach for that

- Optimize your expenses. Our client adviser can guide you on that

- Stay invested for the long term. Many investors could not stay invested to capture the returns. Our client advisers’ challenge is to accompany you on this journey and help you stay invested to capture the return

We are cognizant that our job is to develop fundamentally sound investment portfolios to capture the returns with different risk profiles.

But building wealth is bigger than just investment returns. A big part of wealth building is the wealth advisory portion and Providend is in an ideal position to help you with that. Learn about one of our client’s experience with us here.

This is an original article written by Kyith Ng, Senior Solutions Specialist at Providend, Singapore’s Fee-only Wealth Advisory Firm, and Chief Editor of InvestmentMoats, Singapore’s most well-read financial blog.

For more related resources, check out:

1. Positive Returns Do Not Mean Enough Returns

2. Providend’s Money Wisdom Podcast S2E7: The Way Providend Invests for Our Clients

3. Active Investing That Adds Value to the Client

*Providend is very excited to share that we are now ready to extend our service offerings to the younger accumulators who are looking for holistic, independent, conflict-free wealth advice!

For this group of younger accumulators, we know that it is not easy to make retirement planning a priority when other financial goals – buying a first home, for example, or saving for a child’s education – appear more pressing. Learn how we can help here.

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current investment portfolio, financial and/or retirement plan, make an appointment with us today.