We are all familiar with gold, but what determines its price? Where does its investment return come from? What is the logic of investing in gold? Why does the price of gold soar sometimes and remain stagnant at other times?

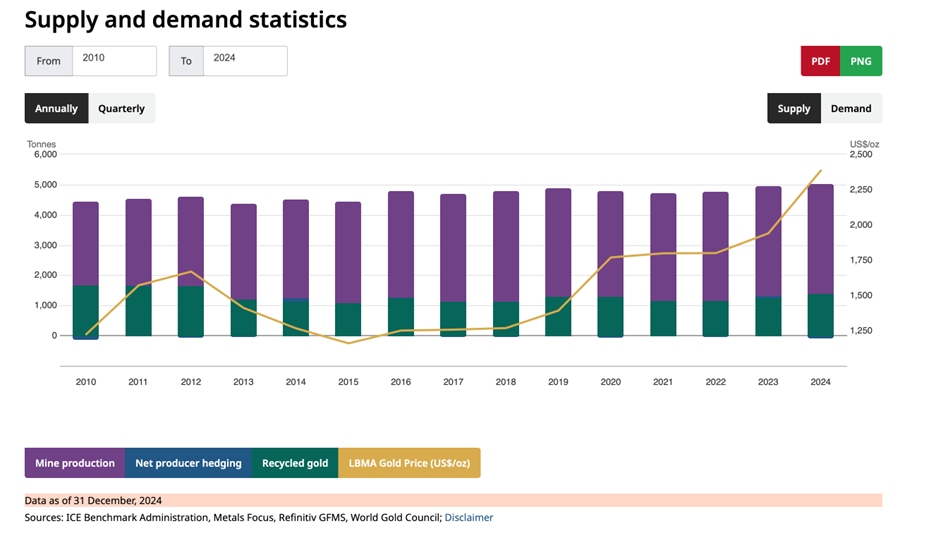

Gold is a precious metal, and its price is determined by market supply and demand. The price fluctuations of gold are mainly affected by supply and demand. The global supply of gold is approximately 5,000 tons per year. The sources of gold supply are basically twofold:

- One is obtained through mining, smelting, and extraction, which is the largest part, accounting for about 80% of the total supply.

- The remaining part comes from recycling.

For example, if my gold ring is worn out or I no longer want my gold necklace, I can recycle them. Gold in electronic components can also be recycled, and this part accounts for about 20% of the supply. Changes in the supply side are relatively slow. First, you need to discover a gold mine. Then, you have to extract it and smelt it. All these processes require investment. You need to establish a company, obtain licenses, find equipment for mining, and build a smelter to gradually smelt the gold. Therefore, it may take several years from the intention of gold production to the actual output of gold. Thus, in terms of the supply side, the change in its output cannot be rapid.

Table 1: Global Gold Supply 2010-2024

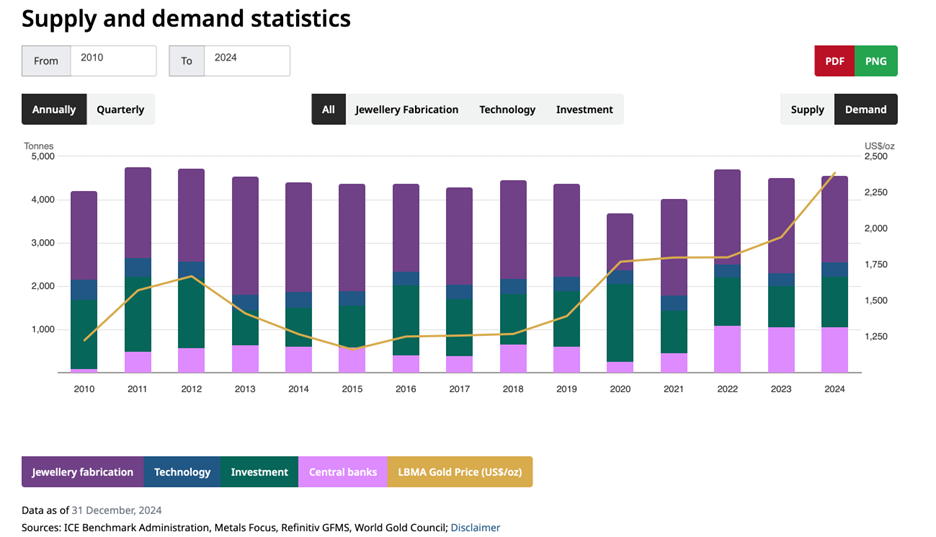

Table 2: Global Gold Demand 2010-2024

Source: Gold.org

The demand side (uses) of gold mainly has three aspects. First, it is used for making jewellery. Gold has always been an important part of jewellery and adornment, accounting for about 55% of the total annual gold demand, which is the largest use of gold on the demand side. In some countries and regions, including parts of China, there is a tradition of giving gold items on occasions such as weddings or when a child is born. India is also a very large consumer of gold jewellery.

Second, it has industrial uses. For example, gold is used as a conductor in electronic components (note: Gold has various uses in industry. It is often used as a conductive material, heat-conducting material, and reflector in electronic products, medical equipment, and aerospace technology). This use accounts for about 20% of the overall gold demand.

The third major use is investment. For example, retail investors buy gold bars and store them in safes as an investment. In fact, the largest gold investors in the world are central banks of various countries. You may have seen some movie scenes where central bank warehouses are filled with gold. Central banks purchase gold and store it as reserve assets. So, these are the three main uses of gold.

The demand side is quite interesting. Let’s take a look at the main demands for gold. First, the demand for jewellery. For example, when someone gets married, they may feel the need to have some gold items. Moreover, although gold is considered expensive, it is affordable for an increasing number of middle-class and upper-middle-class people.

Second, the demand for industrial products. The amount of gold used in this regard is related to the economy. When the economy is good, people consume more, factories need to produce more products, and accordingly, the amount of gold used will also increase.

The third important demand is for investment (or reserve). For example, we may buy gold bars and store them at home as a reserve. The reason is that we think there are risks in other ways of investing or storing our money. Some risks may include inflation. For example, if we deposit money in the bank or invest in stocks and bonds, but when inflation occurs, these assets will depreciate. In this case, it may be better to buy gold because it is a precious metal with certain value. There are also risks such as political instability or during a war. For example, the currency and the country that issues it may cease to exist. In such situations, we may not feel at ease storing our property in the form of paper currency, so we will choose gold instead. Precious metals may be more valuable and can be taken away easily. Central banks of various countries also hold this view when purchasing gold, using it as a reserve for emergencies and to hedge against risks.

Let me give you a very interesting example that has occurred in recent years. You can see that the use of gold as a reserve has increased significantly in the past four or five years. In the past, people used major currencies with good credit such as the US dollar, euro, Japanese yen, and Chinese yuan as reserves, with the US dollar having the largest proportion.

However, in the past three or four years, the proportion of gold as a reserve has been increasing. As of 2024, it has reached nearly 20%. More and more countries are choosing to use gold as their reserve instead of the US dollar, euro, Japanese yen, British pound, or Chinese yuan. Why? Part of the reason is that the international political situation has changed from the relatively peaceful situation in the past two or three decades to a more conflict-ridden one. Here is a practical example. When the conflict between Russia and Ukraine broke out, the Russian central bank had a lot of US-dollar-denominated reserve assets. As a result, these assets were frozen. But the gold reserves in its central bank could still be used. Therefore, due to the increase in geopolitical risks, more investors are increasing their gold reserves.

Looking at the long-term weighted average rate of return of gold, over the past 33 years from 1991 to the end of last year, it was approximately 5% per year. If we look at the US bonds during the same period, it was about 6%, and the US stocks were about 10%. So, gold can outperform short-term bonds and inflation, but it cannot outperform long-term bonds, let alone stocks. This is one of its characteristics.

That is to say, in the long term, if we wear gold as jewellery or store gold bars and don’t often pay attention to the gold price, we may feel that gold is quite good, with an annualised return of 5% and the ability to outperform inflation, making it a good asset. However, we should be aware that in the short term, the volatility of gold is quite high. Its annual volatility is about 15%, almost approaching that of stocks. The volatility of stocks is about 18%-20%, and 15%-18% is very close.

Therefore, in terms of the comparison of returns and risks, especially when you want to sell, since we pay a certain cost when buying, the short-term price fluctuations may lead to a situation where we can’t sell at a good price, which will naturally affect our rate of return. So, the volatility of gold determines that simply investing in gold is not very efficient.

This is the case for all bulk commodities. There is another interesting point. When people buy gold, they all have the consideration of risk aversion. But when everyone uses gold to hedge risks, the price of gold will rise because its supply is limited, and the short-term adjustment speed is not fast. So, we can see that the investment demand for gold from investors is directly proportional to the gold price. The higher the gold price, the higher the enthusiasm for investment. Because some retail investors tend to follow the trend of buying high and selling low. When they see the price rising and others buying, they may think they should also buy. But at this time, we should clearly understand the cycle of gold.

For example, if Xiao Yang has a gold mine, which is large, with good ore positions and low production costs. Suppose the market price is 400 yuan per gram, and his production cost is 300 yuan per gram, then he can make a profit. But if I also have a mine with lower gold content and more difficult smelting processes, and my production cost may be 450 yuan per gram. Then I can only start making a profit when the gold price rises to 500 yuan per gram. So, although the supply of gold has a certain lag, as long as the price goes up, many less-efficient smelting companies can also make a profit. At this time, more supply will be released, which will put downward pressure on the price.

So, the return of gold is higher than inflation, but not by a large margin. At the same time, its volatility is also very high. Therefore, we must pay attention to two points. First, if it is for investment purposes, don’t use short-term funds. Second, although gold is good, in the long term, it cannot outperform stocks, and its volatility is much higher than that of bonds. Therefore, if there are no other considerations and it is just for investment, it won’t be a large part of the investment portfolio. However, considering its hedging function, as shown in the international political examples mentioned above, gold can play a better role.

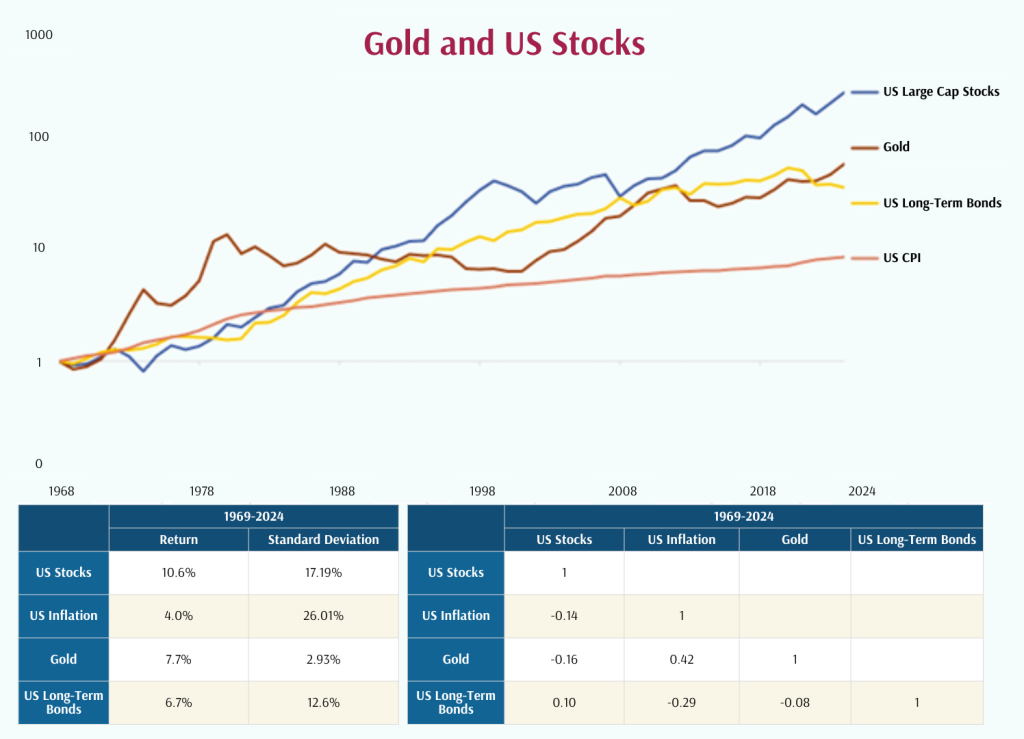

Next, we will focus on analysing the long – term risks and returns of gold, as well as its special hedging role. Since the history of the Chinese stock market and bond market is relatively short, we will use the US stock market and bond market, which have a longer history, to analyse the role of gold in an investment portfolio. From 1969 to 2024, over more than 50 years, the annual return of gold was 7.7%, lower than the 10.6% return of stocks and slightly higher than that of long – term treasury bonds. We can also see from the historical data from 1969 to 2024 that gold and stocks are negatively correlated (-0.14). Gold is a good tool for diversifying risks in a traditional stock-bond portfolio. At the same time, gold is positively correlated with inflation (0.42), that is, high inflation also corresponds to an increase in the price of gold.

Table 3: Stocks, Bonds, Gold, and Inflation 1969-2024

Source: SBBI Yearbook and Author

The return of gold also has a strong two-sided nature. When the purchasing power of paper currency is well-maintained and investors consider paper currency to be safe, the return of gold is usually much lower than that of stocks and bonds, approximately in line with inflation. When the risks of inflation or geopolitics increase, the credibility and purchasing power of paper currency are threatened, and the hedging function of gold will come into play. In such an environment, the return of gold may even be higher than that of stocks.

This two-sided nature is very similar to traditional insurance products. For example, when you buy car insurance, if you don’t have a car accident, the insurance won’t pay out, and it seems like an “investment with no return.” But when you have a car accident, the insurance will compensate you, and it becomes a “high – return investment.” The return logic of gold is very similar. Let’s review history to understand the two-sided nature of the gold price return.

The Two-Sided Nature of Gold Returns:

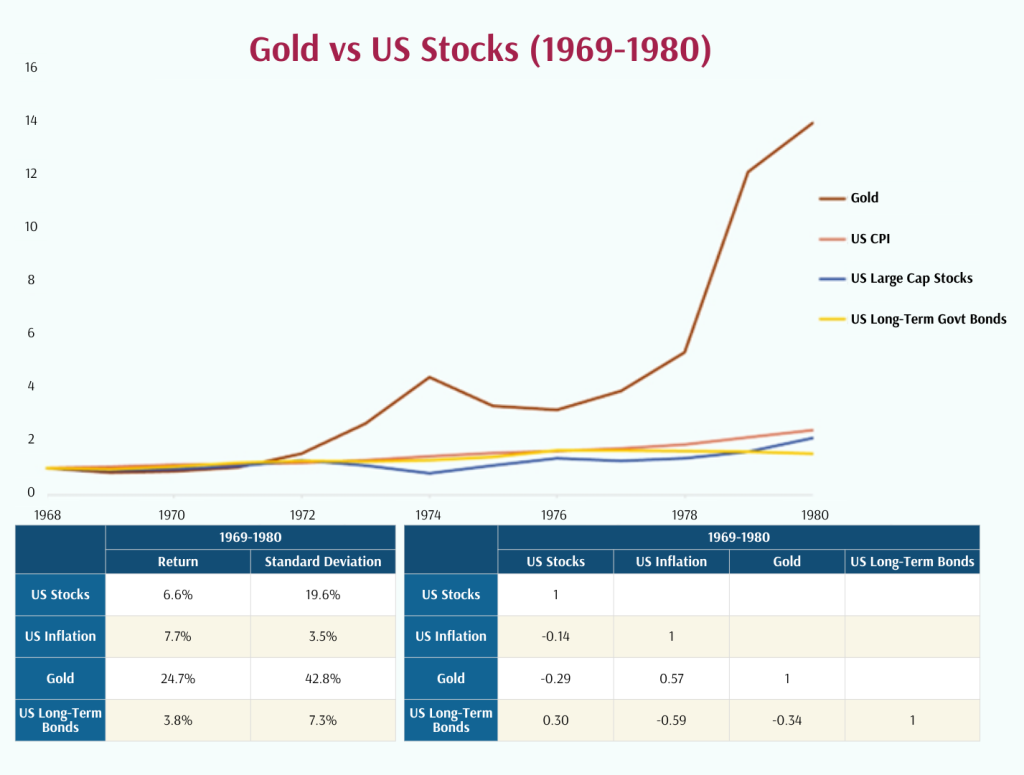

The 1960s–1970s with High Inflation and High Geopolitical Risks

After World War II, the global economic pattern changed significantly. The economies of European countries were severely weakened, while the United States became the world’s largest creditor country and the most economically powerful country. In July 1944, representatives of 44 countries held an international monetary and financial conference in Bretton Woods, New Hampshire, USA, and adopted the Bretton Woods Agreement, marking the establishment of the Bretton Woods system.

The agreement stipulated that the US dollar was pegged to gold, with 1 ounce of gold equal to 35 US dollars, and the US government was obliged to exchange gold at the official price. Other currencies were pegged to the US dollar, and each country’s currency maintained a fixed exchange rate with the US dollar, with a fluctuation range of ±1%. In the following 25 years, through these two pegs, the credit of the paper currencies of these 44 countries was directly guaranteed by the US government.

From the late 1960s to the early 1970s, the United States was mired in the Vietnam War, its economic strength relatively declined, it had a large number of international payment deficits, the oil crisis occurred frequently, and inflation soared. On August 15, 1971, the United States announced that it would stop fulfilling its obligation to exchange the US dollar for gold, marking the collapse of the Bretton Woods system. In 1973, countries abandoned the fixed-exchange-rate system and adopted the floating-exchange-rate system, and the Bretton Woods system completely disintegrated.

Table 4 shows the trends of stocks, bonds, inflation, and gold during the period of the collapse of the Bretton Woods system. We can see that the average inflation rate was as high as 7.7%. In just 12 years, the price of gold increased more than 10-fold relative to the depreciating US dollar, causing the return of gold to far exceed that of stocks and bonds.

Table 4: Stocks, Bonds, Gold, and Inflation 1969-1980

Source: SBBI Yearbook and Author

The Two-Sided Nature of Gold Returns:

The 1980s–1990s with Low Inflation and Low Geopolitical Risks

In the late 1970s, the United States and the global economy faced a severe “stagflation” problem. The inflation rate was as high as 13%, economic growth stagnated, the unemployment rate rose, and the public lacked confidence in the economy and the government. The original monetary policy was difficult to effectively deal with this complex situation.

On August 6, 1979, Paul Volcker became the 12th Chairman of the Federal Reserve of the United States. He changed the Federal Reserve’s long-standing practice of targeting interest rates to targeting the money supply. Through means such as open-market operations, he influenced the interest rates in the money market and thus controlled the money supply. He once raised the federal funds rate to 19.1%, and in July 1981, it even reached a record-high 22.36% to curb inflation.

He successfully reduced the inflation rate from its peak in 1980. By 1983, it had dropped to 3.7%, enabling the US economy to get rid of the severe inflation pressure and enter a new period of growth and low inflation. At the same time, with the disintegration of the Soviet Union, the 40-year-long Cold War between the East and the West ended, the bipolar world pattern ended, and the world pattern developed towards multi-polarisation. Geopolitical tensions eased the pressure on surrounding countries, and the world entered a relatively long-lasting peaceful environment. However, it also triggered new geopolitical conflicts and contradictions in some regions. More and more countries and economies were involved in the trend of developing a market economy, and economic globalisation accelerated.

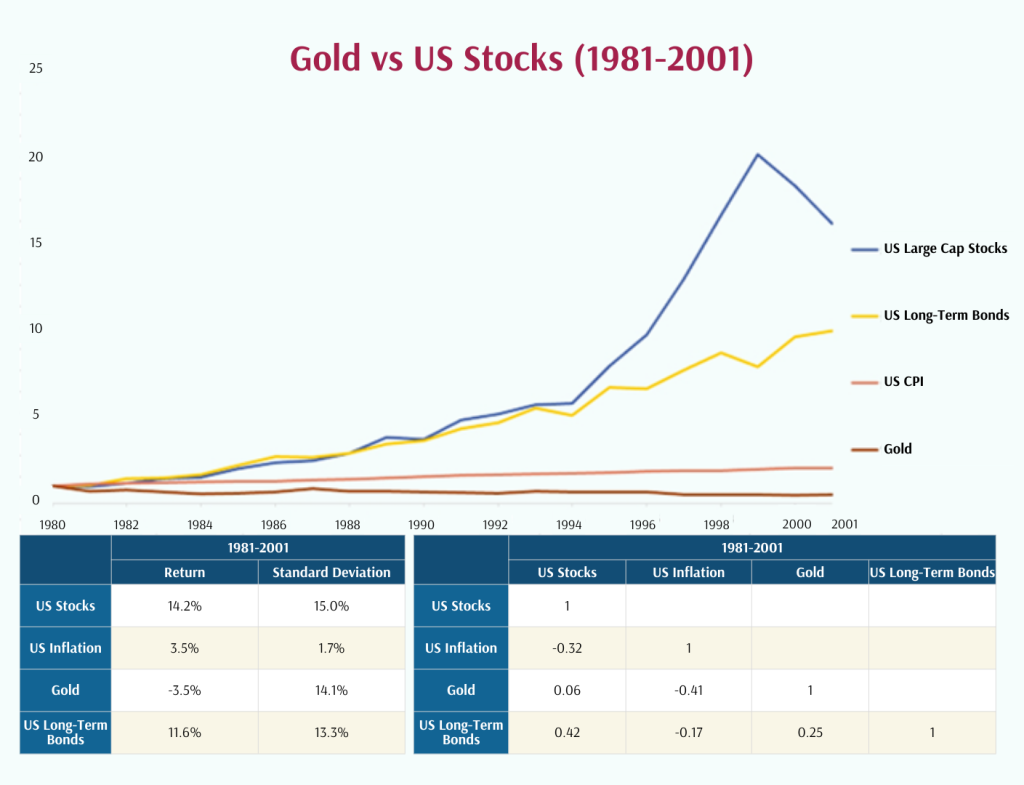

Table 5 shows that during this period, the average inflation rate was only 3.5%. Gold depreciated relative to the US dollar (paper currency), and the return on investing in gold was negative. However, stocks and bonds achieved returns of over 10%.

Table 5 Stocks, Bonds, Gold, and Inflation 1981-2001

Source: SBBI Yearbook and Author

The Two-Sided Nature of Gold Returns:

2001–2024 with Low Inflation and High Geopolitical Risks

With the burst of the first Internet bubble, the United States suffered the September 11 terrorist attacks, followed by the military conflicts in Afghanistan and Iraq, the global financial crisis in 2008, Brexit, the election of Donald Trump as President in 2016, and until the Sino-US trade war in recent years, the Russia-Ukraine conflict. The US federal government debt has exceeded $36 trillion (with an average burden of over $100,000 per citizen). We have entered another period: low inflation, high geopolitical risks, and high risks of the US dollar’s depreciation.

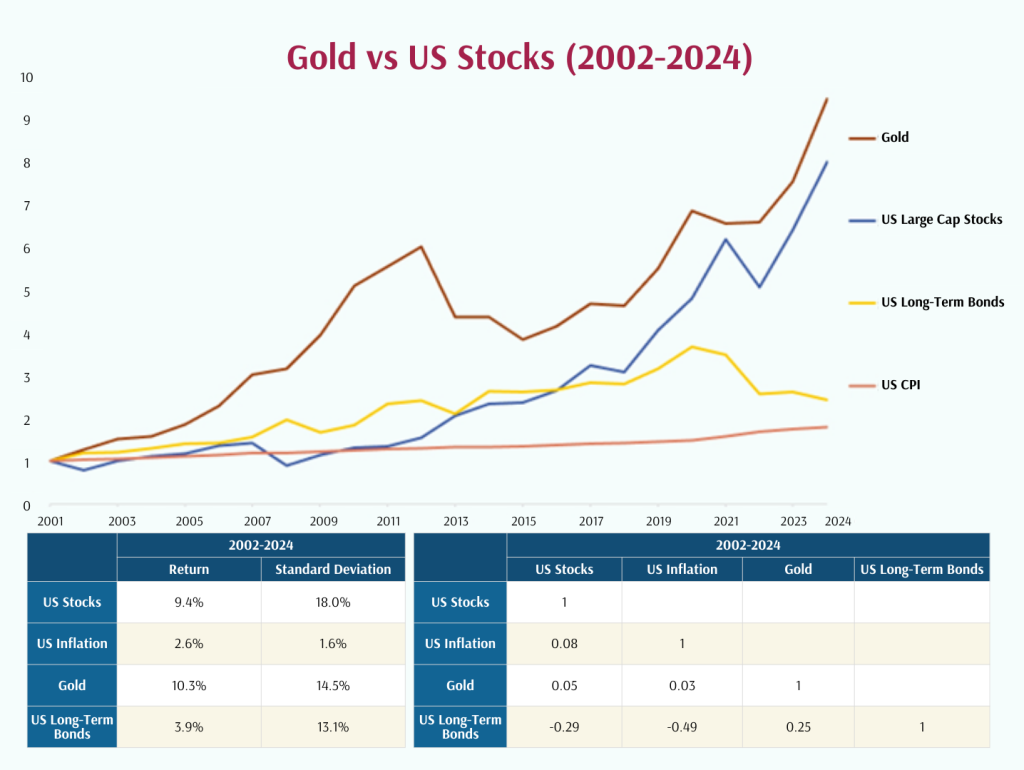

During this period, inflation remained low, geopolitical conflicts emerged one after another. With the increase in the scale of US debt, the risk of the US dollar’s depreciation has returned. Both gold and stocks had an average return rate of around 10%, showing relatively good performance.

Table 6 Stocks, Bonds, Gold, and Inflation 2002-2024

Source: SBBI Yearbook and Author

What About After 2024?

By the end of 2024, the price of gold hit record highs, with an annual return rate approaching 30%. Many investors are considering whether they should invest in gold. However, they are also worried about investing at what could be the peak of the gold price. We still need to return to the two-sided, insurance-like return logic of gold to explain this issue.

Let’s take another example. At the start of 2025, should we buy gold? It depends on your judgment of the two-sided nature of gold. For example, if you think that the overall environment in 2025 will enhance the credibility of paper currency, that is, the risks of inflation and geopolitics are decreasing, then you may not need to buy gold.

Conversely, if you think that the overall environment will reduce the credibility of paper currency, that is, the risks of inflation and geopolitics are increasing, then you may need to allocate some gold.

Generally speaking, since it is difficult to predict the risks of inflation and geopolitics in advance, many investors will allocate some gold for the long term. This is very similar to the logic of buying insurance. You have no way to ensure that nothing will go wrong at home, and even less to ensure that other drivers on the road will be problem-free. That is to say, you can’t predict whether a car accident will occur. If a car accident has a significant impact on your wealth, then you should buy appropriate insurance. Further, if you judge that the road environment for your future driving is high-risk (with many unlicensed large trucks), then you should buy insurance even more. Similarly, if you think that the future environment will see higher inflation and a weaker creditworthiness of paper currency, then you should invest more in gold.

In this article, we focused on analysing gold. The basic investment logic here also applies to other precious metals, such as silver.

Summary

Gold is a very unique investment category. In the long term, the return rate of gold is not outstanding, lagging behind stock and bond investments. Sometimes, the return rate of gold may even fail to outperform inflation (when the risks of inflation and geopolitics are low). The uniqueness of gold lies in its insurance-like property. When the risks of inflation and geopolitics rise, the performance of gold will increase significantly. For investors who are sensitive to the risks of inflation and geopolitics, they can allocate a small amount of gold for the long term. If investors believe that the risks of inflation and geopolitics will increase in the future, they can also allocate gold.

This is an original article written by Dr Peng Chen, Senior Advisor and Director at Providend, Southeast Asia’s first fee-only comprehensive wealth advisory firm.

If you have Mandarin-speaking friends who are interested in whether gold will continue to rise and its ups and downs over the past 60 years, you can listen to this 有知有行 audio podcast, where Dr Peng was a guest.

For more related resources, check out:

1. Is Gold a Good Investment in 2025?

2. Why Do Investors Turn to Gold? Is Gold a Good Investment?

3. Why a Robust Estimate of Future Returns Is Important for Investment Planning

Download our Investment eBook titled “A More Reliable Way to Get Enough Investment Returns: Even During Times of Market Uncertainty” here.

To ensure a good investment experience, Providend is committed to delivering reliable returns, prioritising this over maximising returns and taking unnecessary risks that do not meet your needs. You can learn more about our purpose-driven approach towards Wealth Management and Investment Management.

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current investment portfolio, financial and/or retirement plan, make an appointment with us today.