Gold has been recognised as an important instrument to store, exchange, and preserve wealth since ancient times across different countries. Today, even though we no longer use gold as a currency, investors continue to view gold as an important investment instrument to preserve and grow wealth. In fact, recent financial market innovations have made it much easier, even for retail investors, to invest in gold: through the purchase of physical gold, or through gold-tracking ETFs.

So, how should an individual investor view gold in their investment portfolios? We will answer this question in this article.

Supply and Demand

Similar to other investment instruments, the price of gold is determined in the market by supply and demand. First of all, let us take a look at the basic demand and supply of gold.

Gold supply mainly comes from two sources: mine production and recycling. The total annual supply is fairly stable around 5,000 tons a year, with mine production representing around 80% and recycling representing the rest, 20%.

The stability of supply demonstrates the difficulty of increasing supply significantly in the short run; this continues to support gold as an instrument to store and preserve wealth without significantly losing its value due to a flood of supply.

The demand can be broken down into four areas:

- Jewellery represents roughly 40%

- Industrial at 10%

- Central bank reserve investment at 20%

- Non-central bank investment 20%

Chart 1: Annual Gold Supply and Demand 2010-2023

Source: Gold.org

The demand fluctuates more compared to supply over time. Therefore, the increase or decrease in the price of gold is mostly driven by the demand side. Let us take a detailed look. First, the industrial use of gold is fairly stable. The jewellery demand naturally increases as the living standards of people increase over time. The more interesting demand components are the two investment demands.

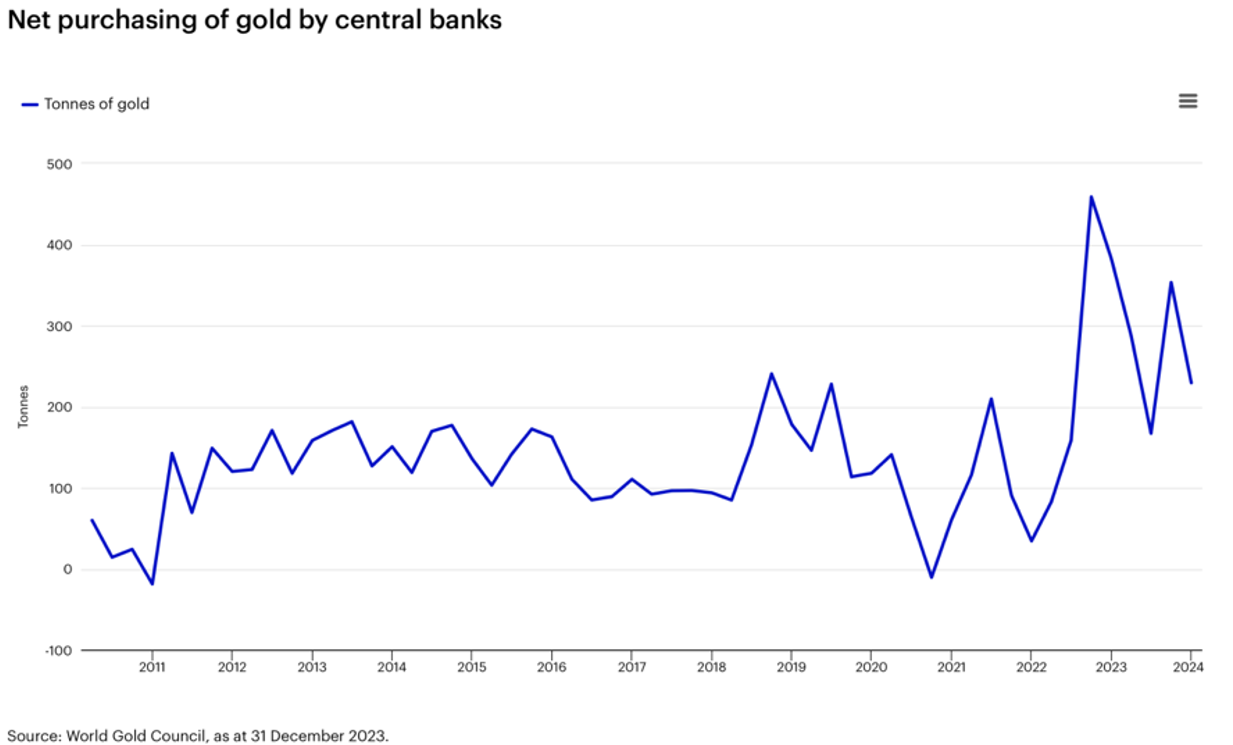

Chart 2: Central Bank Net Gold Purchases

Why would central banks or investors want to invest in gold, especially physical gold?

Compared to other investments, the cost of buying, selling, and storing gold is much higher. For example, the bid-ask spread for buying and selling physical gold can be as high as 3%. This means that to complete a round trip buying and selling, the bid-ask spread alone will cost investors 3%, while other financial instruments, such as stocks or government bonds, cost a few basis points.

We will take a detailed look at the risk-return characteristics and the roles gold plays in a diversified portfolio in the next section.

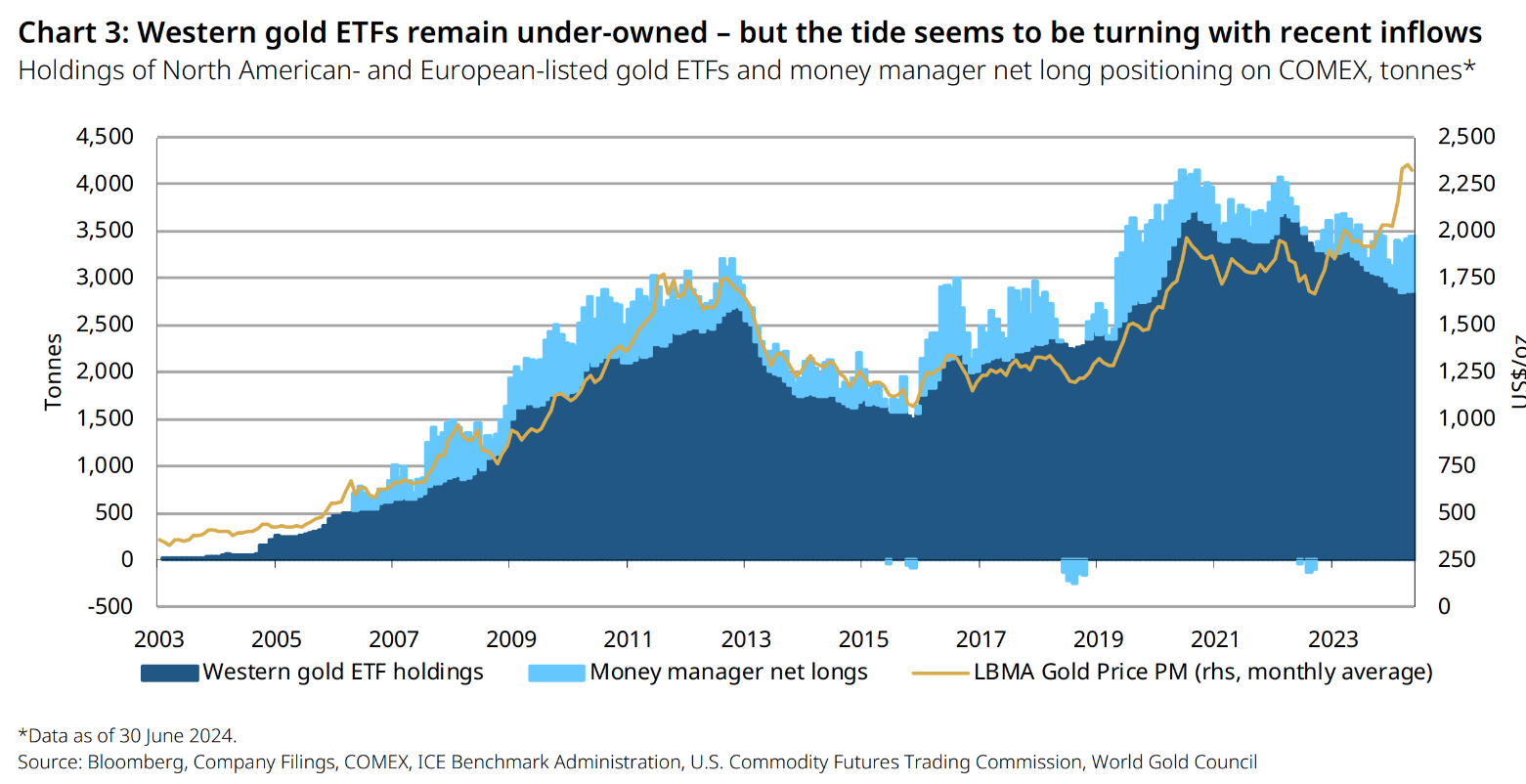

Non-central bank demand is highly correlated with the gold price; when the gold price increases, more investors are drawn to invest in gold. In recent years, Chart 3 shows that non-central bank demand for gold has increased.

Chart 3: Demand for Gold by Non-Central Banks

Source: World Gold Council, Gold Demand Trends Q2 2024

Historical Return and Risk

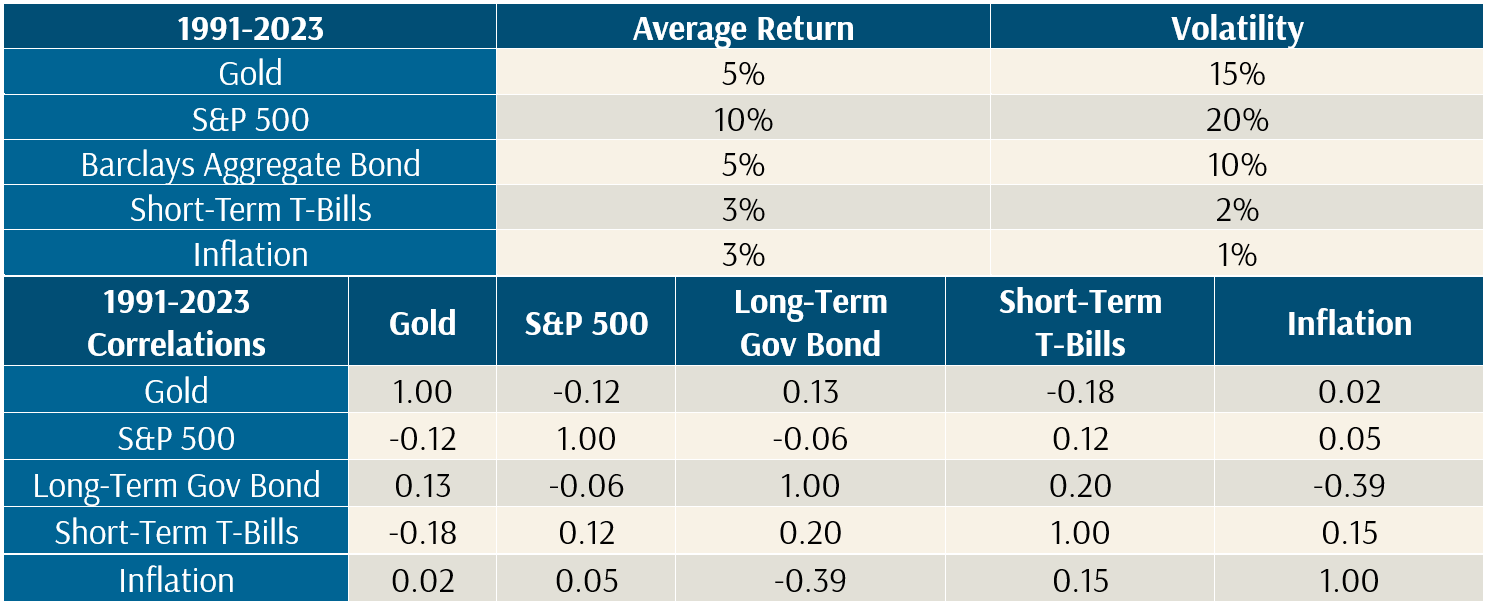

Next, let us take a look at the historical risk and return characteristics for gold (assuming buy and hold), along with traditional stocks and bonds. Gold price volatility and returns: The annualised return of gold has been about 5% in the past 33 years (from 1991 to the end of 2023), and the volatility of gold is about 15%, which is slightly lower than the volatility of stocks.

Table 1: Compounded Annual Return, Volatility, and Correlations (1991-2023)

Source: Author Compiled

Source: SBBI Yearbook and Author

Role of Gold: Diversification and Risk Hedge

Gold plays two roles in a long-term portfolio:

- Gold can help further diversify a long-term portfolio, enhancing the risk and return trade-off

- To preserve value in extreme risky situations. Historically speaking, gold has not offered very attractive risk-adjusted returns. In fact, gold has returned about half the return of stocks, but at roughly the same level of volatility (refer to Table 1). That leads us to the second reason people invest in gold: to hedge against risk scenarios. The table below shows the correlations among gold and major stocks and bond indexes. Specifically, the correlation between gold and the S&P 500 is the lowest, -0.12, which shows that gold is an excellent hedge compared to other asset classes.

The ability to hedge risky scenarios not only includes market risk but also other non-market risks, such as geopolitical risk scenarios. Gold is universally accepted across countries and cultures. This is exactly the reason we have seen that central bank demand over the last two to three years has increased significantly from 100-200 tons a year to 300-400 tons a year. This increase is because central banks across the world are increasingly using gold as their reserves instead of US dollars and other currencies.

More and more countries are choosing to use gold as their reserves, rather than using dollars, euros, yen, pounds, or yuan. Why? I think it’s because international politics has moved from a relatively peaceful twenty or thirty years to a more conflict-prone situation today, where trust between countries and trust in other countries’ currencies has become lower. In addition, some countries are actively involved in regional armed conflicts. For those countries, the need for gold has significantly increased.

Summary

Gold, on a long-term stand-alone basis, does not represent a very attractive investment option. However, as part of the portfolio, it can provide a hedge against inflation and extreme risk scenarios.

What are the different ways for individual investors to invest in gold? What are their advantages and disadvantages?

- Physical Gold – Bars and Coins: Maintain value and resist inflation, but it is not easy to trade and store. The buying, selling, and storage costs can be a few percentage points, thus diminishing the returns. For example, the bid-ask spread for retail investors buying and selling gold can be 3%. This means that to complete a round trip buying and selling, just the bid-ask spread will cost 3%.

- Gold Futures: Hedging and anti-inflation, the cost of trading and storage is low, but the investment knowledge requirements for investors are higher.

- Gold-Linked ETFs: Maintain value and hedge against inflation, the cost of trading is lower than buying physical gold, and there is no need to worry about storage.

For individual investors, how should we think about how much to allocate to gold? There are a few considerations.

First of all, how will the existing portfolio perform against inflation and extreme risk (e.g., political risk) scenarios? For example, for the average Singaporean investor – the Singapore government has done a very good job navigating the geopolitical waters. In addition, Singapore has one of the largest per capital financial reserves (professionally managed by the Monetary Authority of Singapore (MAS), Government of Singapore Investment Corporation (GIC), and Temasek Holdings) to help guard against inflation and systematic financial risks. Therefore, with this “extended” total portfolio view, the risk exposure for the average Singaporean is actually smaller than in many other countries.

Secondly, what are the options available for investors: if the option is to invest in physical gold, then the high costs could completely remove the potential benefits of investing in gold.

Conclusion

In summary, gold is not a very attractive long-term investment on a stand-alone basis – it offers much lower long-term returns than stocks but with similar risk levels. Therefore, investors should not use gold as a cornerstone investment or invest a large percentage of one’s portfolio in gold.

Gold can be useful as a diversification tool in a broadly diversified portfolio:

- To provide diversification and an additional hedge against inflation (or depreciation of fiat paper currency)

- To hedge the overall portfolio against extreme risk (e.g., geopolitical risk) scenarios.

This is an original article written by Dr Peng Chen, Senior Advisor and Director at Providend, Southeast Asia’s first fee-only comprehensive wealth advisory firm.

For more related resources, check out:

1. Long Term Risk Premiums and Expected Returns: Evidence From US and China

2. Providend Video: Is Gold a Good Investment?

3. Why a Robust Estimate of Future Returns Is Important for Investment Planning

Download our Investment eBook titled “A More Reliable Way to Get Enough Investment Returns: Even During Times of Market Uncertainty” here.

To ensure a good investment experience, Providend is committed to delivering reliable returns, prioritising this over maximising returns and taking unnecessary risks that do not meet your needs. You can learn more about our purpose-driven approach towards Wealth Management and Investment Management.

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current investment portfolio, financial and/or retirement plan, make an appointment with us today.