In recent months, there have been a couple of inquiries coming from our prospective clients and clients who are interested to explore parking their money into a short-term endowment plan. One of the key reasons is that the yield is attractive, and the time of commitment is short (probably a 2 to 3 years period). In the past when the interest rate was low, there were limited options for the consumers who are constantly sourcing for a higher return to move their funds to even with a marginal increase in interest rate.

However, in today’s context, a rising interest rate environment, financial institutions and banks have become more competitive in launching shorter-term interest-bearing. Consumers now have more options for higher interest rates products. One of the competitive products in the market is short-term endowment plan.

A typical endowment plan usually extends at least 10 years of policy term (lock-in period) before the plan matures and it comes with guaranteed and non-guaranteed returns. In the past decade, insurance companies have started introducing shorter endowments which usually mature between 1 to 5 years, depending on the product feature. And often, these short-term endowments offer guaranteed returns that are comparable with fixed deposit rates.

Having said that, there are minor differences between a short-term endowment and a fixed deposit. For a short-term endowment, there is a lack of liquidity, and the early surrender charges can be exorbitant – it could range from 5% to 40%. In contrast, a fixed deposit is relatively liquid, however, with early redemption, the consumer will forfeit the interest return. In some cases, fixed deposits may have charges for early redemption apart from forfeiting the interest return. Hence, consumers will need to read the terms and conditions carefully before committing to these instruments.

In recent months, Singapore Treasury Bills (or T-bills) and Singapore Savings Bonds (SSB) are also gaining popularity. The returns are relatively high and most importantly, they provide liquidity to the consumers without having to pay any hefty redemption or surrender charges. This has garnered a lot of interest among consumers to place their savings into T-bills and SSB making it oversubscribed.

Here are some of the links to some of the news of T-bills and SSB:

- https://www.straitstimes.com/business/banking/singapore-savings-bonds-for-november-offering-record-high-rates

- https://www.straitstimes.com/business/t-bill-auction-attracts-strong-interest-record-number-of-bids-received-49-of-non-competitive-bids-allotted

As we know that SSB provide a much longer duration (10 years period) compared to other short-term products, hence while the interest in the initial years is lower, your interest is locked in over a longer period.

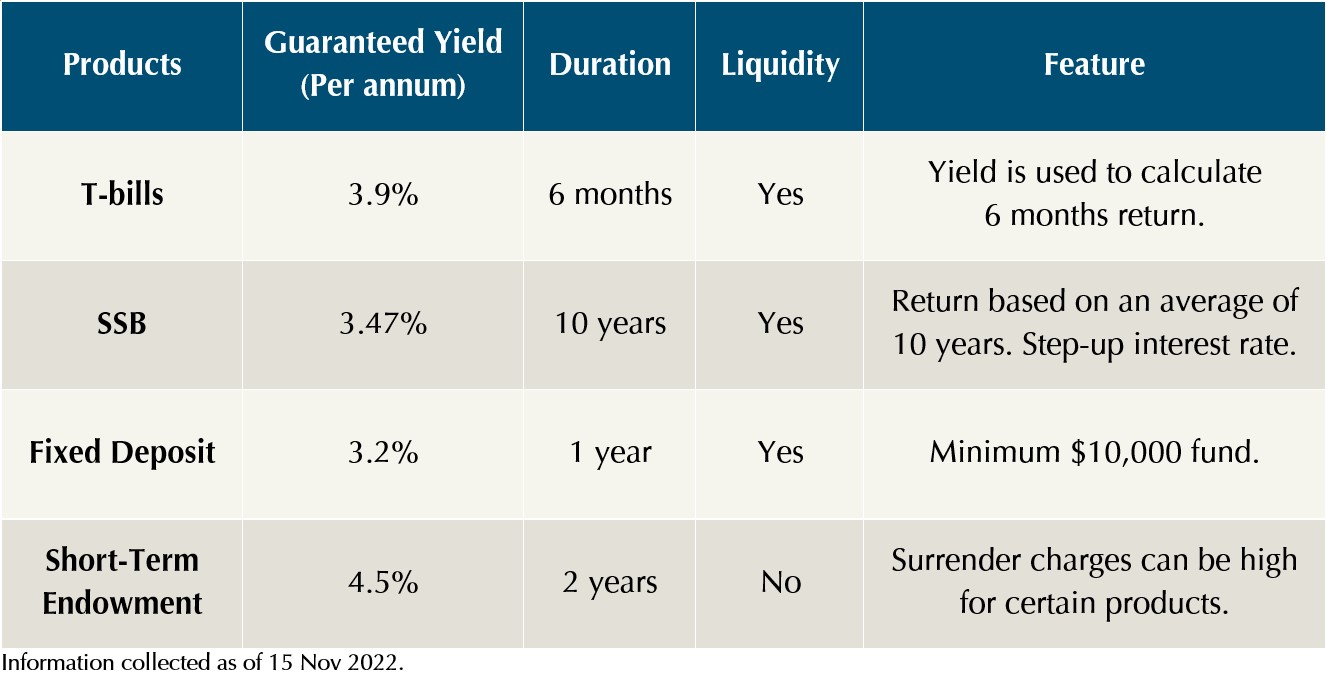

Here are some of the current returns from the recent short-term products:

From the table, we can see that short-term endowment return is the most attractive. Usually for such products, the take-up rate is based on a first come first serve basis and usually sold out within a short period of time, sometimes within a day. From a wealth planning perspective, there are a few considerations before making any buying decision. Instead of chasing after the highest return, you should spare some thoughts on the following questions.

- What is your financial objective?

- Will you be using the money in the next few months or within 1 year? (e.g., down payment for a property) A short-term product like the above table would be suitable.

- Is it for wealth accumulation? (e.g., planning for long-term retirement)

- Is this part of your emergency fund? If so, you must make sure that the product provides liquidity. You may want your cash to be as fluid as possible in case of any unforeseen event.

The good news is, if you are a risk-averse investor, or saving up for the short term, you are simply spoiled for choices as there is a wide range of products to choose from. However, you should not blindly chase after the highest return but also consider if the product is able to meet your needs.

This is an original article written by our Insurance Team at Providend, Singapore’s First Fee-Only Wealth Advisory Firm.

For more related resources, check out:

1. Money FM 89.3: How to Maximize Your Wealth with Safe Investments and Should You Be Investing Your CPF-OA in T-bills?

2. Retire Well in a High Interest, High Inflation Environment

3. Do You Need a Critical Illness Plan?

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current estate plan, investment portfolio, financial and/or retirement plan, make an appointment with us today.