“This time is different” is a common phrase I have heard over the course of my career each time when a financial crisis happens and I have gone through 4 major crises including the current one. But are they really different and what lessons can we learn from them? Let’s make a trip back to history.

The 1997 Asian Financial Crisis (AFC)

While the AFC affected East Asia and Southeast Asia (SEA) in 1997, it was Indonesia, Malaysia, Philippines, South Korea and Thailand that were the most affected. Between 1990 and 1995, these countries’ GDP were growing at as high as 9% p.a. and were expected to continue. With the relatively lower interest rate environment in the US and the financial world wanting a piece of the economic miracle in this region, money flooded into them. I still remembered vividly that many fund houses launched their own version of the SEA funds back then and investors were hungry to invest in them. These factors caused the stock markets and real estate prices in these countries (including Singapore) to surge. But when the US increased interest rates again in 1994, the USD strengthened and Asian countries which had their currency pegged to the USD became less attractive relative to other major currencies. To make matters worse, China then devalued the Yuan by 30% and these caused a slowdown in exports in SEA and Korea.

Back in 1993, wanting to be a financial centre, Thailand eased regulations and gave tax incentives. It then became a place where one can easily borrow foreign currencies to invest in local projects (based in Baht). But as the economy dwindled due to slowing exports, these investors defaulted on their payments and banks ran out of money. The central bank of Thailand had to lend to the financial institutions with its international reserves and its reserves were depleted. Simply put, a country will need to have enough reserves to maintain a currency peg and so on 2 Jul 1997, Thailand unpegged from the USD and the Baht devalued. Banks became technically bankrupt as their liabilities were in USD but the assets were in Baht which has devalued. This contagion effect spread to the rest of the region and the stock markets collapsed.

With the poor economic situation as well as banks lacking the funds to lend, businesses went bust and unemployment rose. Even though Singapore was not so badly affected, we went through a mild recession and retrenchments and unemployment rate rose. Singapore’s situation was made worse with investors not only losing money in the stock markets but also in the property market due to government intervention back in May of 1996 to cool the property market. Property speculators even had to top up their loans as the value of their properties fell below the loan amount.

By the end of 1999, Asia had recovered from the crisis.

The Tech Bubble in 2000

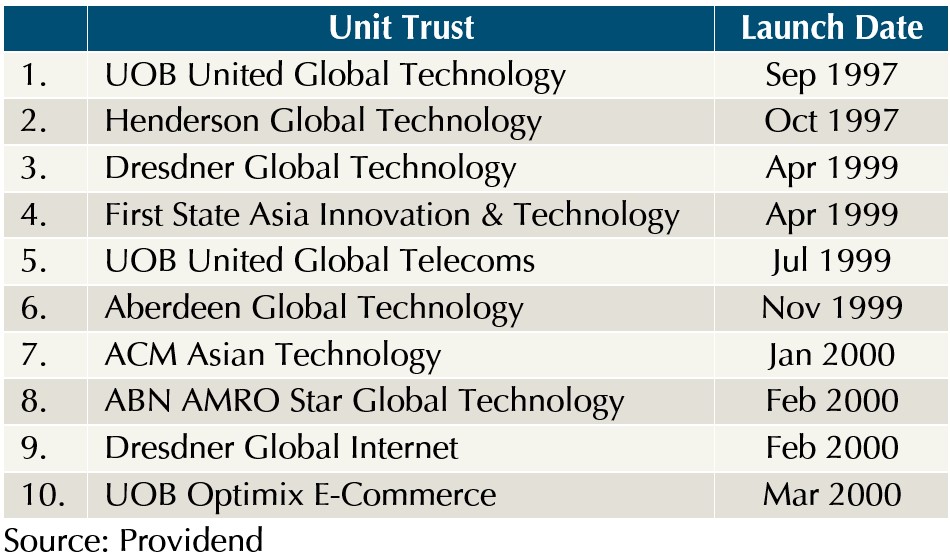

The advent of the World Wide Web in 1989 gave birth to many internet and tech-based businesses between 1995 and 2000. These startups needed capital to grow and the low interest rate environment between 1998-1999 facilitated venture capital investments. Even though they were not profitable and burning huge amounts of cash, investors believed in their growth stories and bought into anything that has an internet prefix or a .com suffix. At the height of the boom, it was possible for a promising dot-com company to become a public company via an IPO and raised a substantial amount of money even if it had never made a profit or, in some cases, realised any material revenue. This caused the NASDAQ to rise 400% between 1995 to 2000. In Singapore, prior to the bubble burst in March 2000, fund houses rushed to set up funds to sell to investors. (See table)

After the US Federal Reserve raised interest rates several times, capital to fund these growth start-ups dried up and investors realised that these businesses were overpriced especially with no earnings in sight. The bubble burst and NASDAQ fell 78% from its peak by October 2002. Although the bubble burst only caused a mild recession in the US, it affected investors globally. The NASDAQ wouldn’t fully recover what was lost since the burst until 2015.

The Global Financial Crisis of 2008

The Global Financial Crisis (GFC) was a banking-led crisis. Low standard lending policies and lax capital requirements by SEC allowed commercial banks to lend to both standard borrowers and subprime borrowers which caused housing prices to soar. These banks then securitised the subprime mortgages and sold it to investment banks (such as Lehman Brothers) who then repackaged them into complex and opaque structures called mortgage-backed securities (MBS) to sell to investors that rating agencies deemed as investment grade. As it turned out, retail investors who bought into these investment notes were the unwitting providers of insurance to counterparties, and were paid premiums that were marketed as low-risk income.

Eventually, housing prices peaked and demand for houses dropped, and prices fell. To make matter worse, the US Federal Reserve increased interest rates from 2004. Borrowers could not repay the loans and were also unable to sell their houses and defaulted their loans. The scale of the default bankrupted these investment banks even as MBS became worthless and institutions who sold Credit Default Swaps (CDS) could not pay as well. Commercial banks realised they could no longer sell their subprime mortgages to get liquidity and had to borrow from other banks, who were also in deep water. Most of the banks stop lending each other or charge a punitively high interest rate. The financial system collapsed and in turn, caused a recession globally. I remembered the fears in the market back then as investors into these structures lost their hard-earned savings and panicked as the stock markets crashed and one financial institution after another announced their fall. The situation was made worse when companies started retrenching their staff and unemployment rate grew.

While the US stock market started recovering from Apr 2009, the economy had to wait till mid 2009 before making its recovery.

History has shown us that while the causes of the 3 crises were different, what is the same is that lax regulations, investors and financial institutions’ greed in chasing returns and profits blindly were the main culprits of the crises. What is also similar is that no matter how bad a crisis, we always recover from it. But whether your investments will recover and give you the returns in the long run will depend on what you invest in and whether you are able to stay invested in them through the crisis. After managing clients’ money through the 3 crises, I have learnt that it is better to get sufficient returns from instruments with strong evidence of a high certainty of success than to pursue maximum returns from investments based on trendy themes which we don’t even understand. In addition, always be prudent in your short-term financial planning so that you can weather the storms to reap the long-term investment returns when the crisis passes. And all crises shall pass, including the current one.

The writer, Christopher Tan, is Chief Executive Officer of Providend, Singapore’s first fee-only wealth advisory firm and author of the book “Money Wisdom: Simple Truths for Financial Wellness“.

The edited version of this article has been published in The Business Times on 27th June 2022.

For more related resources, check out:

1. Keeping Faith Despite the Market Downdraft

2. Conversation with Clients One Year After the Crash

3. Providend’s Money Wisdom Podcast: In Crisis, Do the Right Thing

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current estate plan, investment portfolio, financial and/or retirement plan, make an appointment with us today.