I love managing my money, no surprises about that. But I also do have a fascination towards psychology, particularly in behavioural economics and cognitive biases. And along the way, I started to wonder whether I can trust the stuff between my ears to make the right decisions when it comes to money.

As an Introduction

Behavioural economics talk about how decisions are made to maximise utility (or personal satisfaction), taking into account psychological and cognitive factors or biases that can divert outcomes from pure rational thinking. Influential people in this field includes Amos Tversky, Daniel Kahneman and Richard Thaler (highly recommend to read up on them!) amongst many others.

While we like to think of ourselves as perfectly rational human beings with highly intelligent brains, the reality is that the brain is rather primitive when it comes to making decisions.

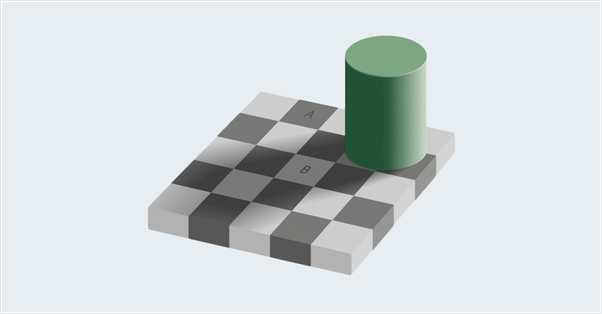

Here is a fun optical illusion that was shared with me. The objective is to guess whether square A or square B is darker. As you probably figured out with most optical illusions, they are both in fact the exact same colour. However, the more interesting part is, even if you now know that they are of the same colour, can you actually see it? The reason for this is because the brain uses certain templates or shortcuts to help us make faster decisions but may not always be right. And even if we are conscious of our errors, it is still very difficult to override this function!

Source: http://persci.mit.edu/gallery/checkershadow

There are many cognitive biases discovered till date, but for the purpose of this article, I would like to focus on a few of the most prevalent ones that are related to finance.

Self-Serving Bias and the Significance of Luck

Investing has a lot to do with probabilities but not enough people are thinking about them. One reason is that the brain struggles to think about odds and large numbers in an intuitive manner. Studies, on the other hand, show that luck plays a far greater role in our success or failure than we imagine. We often erroneously tend to think of outcomes being a direct result of the decisions made, attributing good outcomes to good decisions (or skills).

The same is true when it comes to investing. We often assess whether we have made the right decision, in stock picking or market timing, solely from the outcome of whether the investment made or lost money. Imagine if you just so happen to hear about Bitcoin in 2008, and decided to put down your life savings of 20 years into the digital asset just because you “had a good feel for it”, you certainly would have a very good outcome today. But would you really consider it to be a great decision? (If you are wondering, the answer is no, because putting your life savings based on having a good feel is never a good decision.) Decisions and outcomes are correlated but separate, and when assessing investment decisions, you always want to think very objectively, how the role of luck has been factored in the outcome. Additionally, you want to think very critically, how robust the investment decision framework is, while being very careful not to fall for the confirmation bias (looking for confirmatory evidence that aligns with what we already believe and ignore contradictory ones).

Availability Bias

The next one I would like to talk about is the availability bias, which is basically a mental shortcut that gives higher weightage to information that is more readily accessible to them (a personal encounter, for example, can be very powerful) and the tendency to overestimate the likelihood of something similar happening in the future. For example, after hearing about several news reports of airplane crashes, your brain immediately associates air travel with being highly dangerous. We tend to rely on the availability bias as a shortcut because we typically do not have immediate access to larger datasets of information or statistics to make a more accurate judgement.

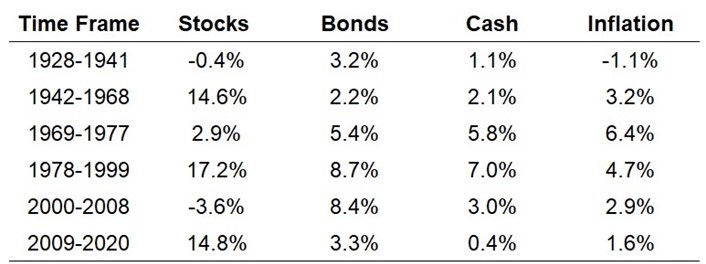

The same applies in investing. Take a look at the following chart below that illustrates the historical performance of various asset classes. If you were to be invested from 1969 through to 1977, you would have encountered high inflation coupled with low returns from stocks, while if you had started your investment journey subsequently from 1978 to 1999, you would think that the stock market was the best thing ever. Likewise, you have similar observations when you compare investments from year 2000 and ending with the 2008 global financial crisis compared to the years that followed.

Source: https://awealthofcommonsense.com/2021/01/stock-bond-cash-returns-1928-2020/

Therefore, when it comes to evaluating your own investments, always be mindful of your personal experiences that might incorrectly skew your expectations of the future. As Morgan Housel said in his book, “The Psychology of Money”, “Your personal experiences with money make up maybe 0.00000001% of what’s happened in the world, but maybe 80% of how you think the world works.”

Instead, you want to be objective and consider the longer-term data, and humble enough to accept the difficulty in predicting the future.

Mental Accounting

The third concept is about mental accounting when it comes to money. By definition, it is about assigning different values on different pots of money based on subjective criteria, which leads to irrational decisions. To give you a common example, when a person gambles at a casino and wins money, he will often refer to his winnings as “house money” and tend to take higher risks with it. However, money is fungible, meaning that every dollar is the same, regardless of where it came from, and should be treated in exactly the same way.

We also often observe this in investing, when we hear someone say that they are waiting for their investments to “break even” before selling or that they can “afford” their investments that are in positive territory to lose some because they are already in profits. However, a drop in value is the same loss, whether it comes from your winning or losing investments. The prices you bought in has no relevance to your current decision to buy or sell because you are assessing on their future prospects and whether you should continue to be invested in them. That being said, it is often not easy to overcome mental accounting, but a good way to help think about this is to imagine if all your investments were converted to cash today, would you still buy back the same investments you hold today?

Dunning-Kruger Effect

The last cognitive bias that I think deserves special mention is the Dunning-Kruger Effect. It is an irony described by social psychologists David Dunning and Justin Kruger that people with less knowledge in a particular subject, tend to overestimate their competence. This is because these people do not know enough to recognise their own incompetence, and therefore, remaining ignorant. Alongside other influences from the overconfidence bias, you get a rather dangerous combination when it comes to investing your lifelong savings.

I mention this because, not only do you want to be fully aware of your own personal biases that can hurt your investment journey, you also want to incorporate critical thinking and skepticism in your thought process. The investing arena is full of noise, uncertainty and complexity. Always be objective and ask a lot of questions before arriving at a conclusion. Be open and keep learning.

As a Conclusion

So, after saying all that, can you really trust your head when you invest? I think the answer is yes, but you have to also recognise that our brains are not perfect and figure out ways to mitigate our natural tendencies to use mental shortcuts that might not be correct. I highly recommend reading “The Psychology of Money” by Morgan Housel, which should give you a good start to your journey. I hope that it “blows your mind”!

This is an original article written by Tan Chin Yu, Client Adviser of Providend, Singapore’s First Fee-Only Wealth Advisory Firm.

For more related resources, check out:

1. 9 Investment Lessons That Make Me a Better Cyclist

2. My Realisations of What Wealth Planning Is Really About

2. Are You a Beneficiary of an Unexpected Inheritance from Your Loved Ones?

We do not charge a fee at the first consultation meeting. If you would like an honest second opinion on your current investment portfolio, financial and/or retirement plan, make an appointment with us today.